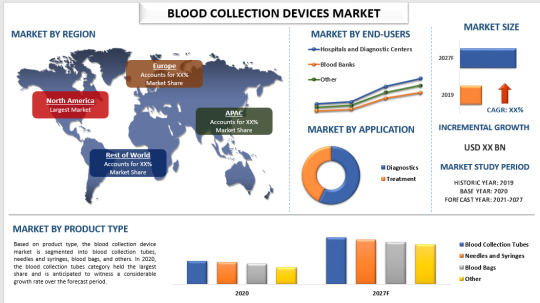

#Blood Collection Devices Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

69% of Tumblr users are millennials.

Text

Blood Collection Devices Market: Trends, Challenges, and Future Outlook

The blood collection devices market plays a crucial role in the healthcare sector, supporting diagnostic testing, transfusions, and research. This market encompasses a variety of devices, including needles, syringes, blood collection tubes, and lancets. With the rising prevalence of chronic diseases, increasing healthcare expenditures, and advancements in medical technology, the blood collection devices market is poised for significant growth. This article delves into the current trends, challenges, and future outlook of the blood collection devices market.

Current Market Trends

1. Technological Advancements

Innovations in blood collection technology are significantly enhancing the efficiency and safety of blood collection processes. Automated blood collection systems, for instance, minimize human error and improve the accuracy of blood sample volumes. Advanced materials and designs are also making blood collection devices more user-friendly and less painful for patients.

2. Increasing Prevalence of Chronic Diseases

The rising incidence of chronic diseases such as diabetes, cardiovascular diseases, and cancer is driving the demand for blood collection devices. Regular blood tests are essential for monitoring these conditions, thereby boosting the market for blood collection products.

3. Growing Awareness and Health Check-Up Programs

Increased awareness about the importance of regular health check-ups is leading to higher demand for diagnostic tests, which in turn fuels the need for blood collection devices. Government and private health check-up programs, especially in developing countries, are contributing to market growth.

4. Home Healthcare and Point-of-Care Testing

The trend towards home healthcare and point-of-care testing is gaining momentum, driven by the convenience and efficiency these options provide. Portable and easy-to-use blood collection devices are becoming popular for home use, enabling patients to perform routine tests without visiting healthcare facilities.

For a comprehensive analysis of the market drivers, visit https://univdatos.com/report/blood-collection-devices-market/

Challenges in the Market

1. Risk of Blood-Borne Infections

The risk of blood-borne infections remains a significant challenge in the blood collection process. Ensuring the safety and sterility of blood collection devices is paramount to prevent the transmission of infections. This requires stringent regulatory standards and compliance, which can be a hurdle for manufacturers.

2. High Cost of Advanced Devices

While technological advancements have improved the functionality of blood collection devices, they have also led to increased costs. High-end automated systems and advanced materials can be expensive, limiting their adoption in cost-sensitive markets.

3. Regulatory Compliance

The blood collection devices market is highly regulated, with stringent requirements for product approval and quality control. Navigating these regulatory landscapes can be complex and time-consuming for manufacturers, potentially delaying the launch of new products.

4. Shortage of Skilled Healthcare Professionals

The effective use of blood collection devices requires skilled healthcare professionals. A shortage of trained personnel, particularly in developing regions, can impede the efficient utilization of these devices and impact market growth.

Future Outlook

1. Expansion in Emerging Markets

Emerging markets present significant growth opportunities for the blood collection devices market. Increasing healthcare investments, improving healthcare infrastructure, and rising awareness about early disease diagnosis in countries like India, China, and Brazil are expected to drive market expansion.

2. Innovations in Device Design

Future developments in device design are likely to focus on improving patient comfort and ease of use. Innovations such as painless needles, micro-collection devices, and integrated data management systems are anticipated to revolutionize the blood collection process.

3. Integration with Digital Health Technologies

The integration of blood collection devices with digital health technologies will enhance the efficiency and accuracy of diagnostics. Devices equipped with IoT capabilities can automatically upload data to electronic health records (EHRs), facilitating real-time monitoring and analysis.

4. Sustainable and Eco-Friendly Products

As environmental concerns gain prominence, the development of sustainable and eco-friendly blood collection devices is expected to rise. Manufacturers are exploring biodegradable materials and reusable components to reduce the environmental impact of their products.

For a sample report, visit https://univdatos.com/get-a-free-sample-form-php/?product_id=22608

Conclusion

The blood collection devices market is set for substantial growth, driven by technological advancements, increasing prevalence of chronic diseases, and expanding healthcare access. While challenges such as regulatory compliance and high costs persist, the market's future looks promising with innovations in device design and integration with digital health technologies. By addressing these challenges and leveraging growth opportunities, the blood collection devices market can significantly enhance healthcare delivery and patient outcomes worldwide.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411x

Website -www.univdatos.com

#Blood Collection Devices Market#Blood Collection Devices Market Size#Blood Collection Devices Market Growth#Blood Collection Devices Market Forecast

0 notes

Link

#market research future#venous blood collection#venous blood collection device#blood collection device market#venous blood size

0 notes

Link

#market research future#venous blood collection#venous blood collection device#blood collection device market#venous blood size

1 note

·

View note

Text

Breaking Down Growth Patterns: Trends in the Arterial Blood Collection Devices Market

Market Overview –

According to forecasts, the arterial blood collection market would grow at a 10.2% annual rate from 2022 to 2030, or USD 1924.34 million.

The arterial blood collection market focuses on products and devices used to obtain blood samples from arteries for diagnostic testing, particularly for arterial blood gas (ABG) analysis. These tests measure the levels of oxygen, carbon dioxide, and other gases in the blood, providing critical information about a patient's respiratory and metabolic status.

Market growth is driven by the increasing prevalence of respiratory diseases, such as chronic obstructive pulmonary disease (COPD) and acute respiratory distress syndrome (ARDS), and the growing demand for point-of-care testing in emergency departments, intensive care units, and operating rooms. Arterial blood collection devices enable healthcare providers to quickly and accurately obtain blood samples for ABG analysis, facilitating timely diagnosis and treatment of respiratory and metabolic disorders.

Technological advancements and innovations in arterial blood collection devices are shaping the market, offering improved safety, ease of use, and sample quality. From prepackaged arterial blood gas syringes and safety lancets to integrated blood gas analyzers and wireless monitoring systems, these advancements enhance workflow efficiency and patient care in healthcare settings.

The Arterial Blood Collection Devices Market is witnessing substantial growth, primarily fueled by the rising demand for arterial blood collection syringes in healthcare settings. These devices are crucial for accurate blood gas analysis and are extensively used in critical care units and laboratories. Technological advancements and the increasing prevalence of chronic diseases are further driving market expansion.

Moreover, the COVID-19 pandemic has highlighted the importance of arterial blood gas analysis in managing respiratory complications and optimizing mechanical ventilation strategies in critically ill patients. Arterial blood collection devices play a crucial role in monitoring patients' oxygenation status, acid-base balance, and ventilation parameters, contributing to better patient outcomes and reduced mortality rates.

However, challenges such as blood sample variability, operator proficiency, and infection control concerns pose obstacles to market growth. Addressing these challenges requires collaboration between device manufacturers, healthcare providers, and regulatory agencies to develop standardized protocols, training programs, and quality assurance measures for arterial blood collection and analysis.

Overall, the arterial blood collection market presents significant opportunities for innovation and collaboration to improve patient care and outcomes in respiratory and critical care medicine. By investing in research, education, and technology, stakeholders can drive continued growth and advancement in the market and contribute to the development of more effective diagnostic and monitoring tools for patients worldwide.

Segmentation –

A wide range of blood collection devices are available for both venous and arterial blood collection purposes. Arterial blood collection involves obtaining blood samples from arteries to analyze arterial blood gases. The blood collection devices market is categorized into various types, including blood collection tubes, lancets, needles, vacuum blood collection systems, microfluidic systems, and other devices such as arterial cannulae and blood bags.

Arterial blood collection devices play a crucial role in diagnosing and treating diseases. They enable healthcare providers to conduct blood tests, aiding in disease diagnosis and treatment planning. These devices are utilized for arterial blood gas sampling and intraoperative blood salvage. The arterial blood collection market is further segmented based on application into arterial blood gas sampling, which includes disease diagnosis and acid-base status monitoring.

In terms of end users, the blood collection devices market includes hospitals and clinics, laboratories, blood banks, and other facilities like ambulatory surgery centers.

Regional Analysis –

Regional analysis of the Arterial Blood Collection Market provides crucial insights into the distribution and trends of blood collection methods for arterial sampling across diverse geographic regions. Understanding regional dynamics is essential for stakeholders to tailor their strategies effectively, considering factors such as the prevalence of cardiovascular diseases, healthcare infrastructure, and regulatory frameworks.

For instance, regions with a high prevalence of critical care admissions or cardiac surgeries may witness a heightened demand for arterial blood gas testing, thereby driving the adoption of arterial blood collection methods. Developed regions with advanced healthcare systems often have well-established protocols for arterial blood gas analysis, making arterial sampling a routine procedure in intensive care units and operating rooms. Conversely, developing regions may encounter challenges like limited access to arterial blood gas testing facilities, shortages of trained healthcare personnel, and financial constraints.

Factors such as government healthcare expenditure, reimbursement policies, and technological advancements significantly influence regional dynamics in the arterial blood collection market. Conducting a comprehensive regional analysis enables stakeholders to identify growth opportunities, assess competitive landscapes, and tailor strategies to address the specific needs of each region. Furthermore, understanding regional disparities in healthcare delivery and patient demographics facilitates the development of targeted interventions to improve access to arterial blood collection methods and enhance patient care outcomes. Overall, regional analysis serves as a vital tool for optimizing resource allocation, promoting innovation, and advancing healthcare quality in the arterial blood collection market.

Key Players –

The Arterial blood collection devices leading players include Becton, Dickinson and Company, Bio-Rad Laboratories, Inc., NIPRO Medical Corporation, QIAGEN, F. Hoffmann-La Roche Ltd, Terumo Medical Corporation, and Thermo Fisher Scientific, Inc.

Related Reports –

Medical Tourniquets

Forensic Swab

Ascites

Intraoperative Neurophysiological Monitoring

For more information visit at MarketResearchFuture

#Arterial Blood Collection Devices Market#Arterial Blood Collection Devices Market Size#Arterial Blood Collection Devices Market Share#Arterial Blood Collection Devices Market Trends

0 notes

Text

On May 7, 2011, Georgia resident Tonya Brand noticed a pain on the inside of her right thigh. As the pain grew worse in the 4- to 5-inch area of her leg, she headed to a hospital. There, doctors suspected she had a blood clot. But an ultrasound the next day failed to find one. Instead, it revealed a mysterious toothpick-sized object lodged in Brand's leg.

Over the next few weeks, the painful area became a bulge, and on June 17, Brand put pressure on it. Unexpectedly, the protrusion popped, and a 1.5-inch metal wire came poking out of her leg, piercing her skin.

The piece of metal was later determined to be part of a metal filter she had implanted in a vein in her abdomen more than two years earlier, in March 2009, according to a lawsuit Brand filed. The filter was initially placed in her inferior vena cava (IVC), the body's largest vein tasked with bringing deoxygenated blood from the lower body back up to the heart. The filter is intended to catch blood clots, preventing them from getting into the lungs, where they could cause a life-threatening pulmonary embolism. Brand got the IVC filter ahead of a spinal surgery she had in 2009, which could boost her risk of clots.

After the wire burst from her leg, X-rays showed that another metal shard had broken free from the filter and traveled. The second one lodged itself near her spine, which is where it remains—it's too risky to try to remove. Brand underwent surgery in July 2011 to try to remove the rest of the filter in her IVC, but the surgeons failed to collect the remnants after several attempts.

@startorrent02

10 notes

·

View notes

Link

0 notes

Text

Butterfly Needle Sets Market

Butterfly Needle Sets Market Size, Share, Trends: Becton, Dickinson and Company (BD) Leads

Increasing Adoption of Safety-Engineered Butterfly Needle Sets to Prevent Needlestick Injuries Drives Market Growth

Market Overview:

The global butterfly needle sets market is projected to grow at a CAGR of 6.8% from 2024 to 2031, reaching a value of USD YY billion by 2031. North America is expected to dominate the market, driven by advanced healthcare infrastructure and increasing demand for minimally invasive procedures. Key metrics include rising prevalence of chronic diseases requiring frequent blood draws, growing geriatric population, and increasing adoption of home healthcare services.

The Butterfly Needle Sets market is experiencing steady growth due to their ease of use, patient comfort, and versatility in various medical procedures. Factors such as technological advancements in needle design, increasing focus on patient safety, and the rising number of diagnostic tests and blood donations are driving the adoption of butterfly needle sets across various healthcare settings.

DOWNLOAD FREE SAMPLE

Market Trends:

The trend towards safety-engineered butterfly needle sets is gaining momentum as healthcare facilities prioritize the prevention of needlestick injuries and the transmission of bloodborne pathogens. These advanced needle sets incorporate safety features such as automatic retraction mechanisms or protective shields that cover the needle after use. For instance, a major medical device company recently launched a new line of butterfly needles with a passive safety mechanism that automatically activates upon withdrawal from the patient, reducing the risk of accidental needlesticks by up to 90% compared to standard designs.

Market Segmentation:

21G needle gauge dominates the Butterfly Needle Sets market, accounting for the largest share in the needle gauge segment. This gauge offers an optimal balance between flow rate and patient comfort, making it suitable for various blood collection and infusion procedures across different patient populations.

Recent advancements in 21G butterfly needle sets have focused on improving needle sharpness and reducing patient discomfort. For instance, a leading medical device manufacturer recently introduced a new 21G butterfly needle set featuring a proprietary needle coating technology that reduces insertion force by up to 20% compared to standard needles.

Market Key Players:

Becton, Dickinson and Company (BD)

Terumo Corporation

B. Braun Melsungen AG

Nipro Corporation

Cardinal Health

Smiths Medical

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Link

0 notes

Text

Global IoT Medical Devices Market Report and Forecast 2024-2032

The global Internet of Things (IoT) medical devices market size is being driven by the rising prevalence of cardiovascular diseases across the globe. The market value was close to USD 31.40 billion in 2023 and is anticipated to grow at a compound annual growth rate (CAGR) of 25.1% during the forecast period of 2024-2032. The market is anticipated to achieve a value of USD 236.30 billion by 2032. IoT medical devices are revolutionising healthcare by enabling real-time monitoring, remote patient management, and data-driven decision-making. With advancements in technology, healthcare providers can offer more personalised and efficient care, improving patient outcomes while reducing operational costs. This blog post delves into the key factors driving the growth of the IoT medical devices market, the latest trends, market dynamics, and the segmentation driving growth. We will also highlight the impact of COVID-19 and analyse recent developments in the IoT space for medical applications.

Get a Free Sample Report with Table of Contents: https://www.expertmarketresearch.com/reports/iot-medical-devices-market/requestsample

IoT Medical Devices Market Overview

The IoT medical devices market refers to the segment of the healthcare industry that uses interconnected devices and technology to gather, store, and transmit health-related data. These devices leverage the power of the internet to monitor patient health in real-time, enhance diagnostic accuracy, improve patient care, and streamline hospital operations. The devices in this category include wearable sensors, implantable devices, remote monitoring tools, and connected diagnostic equipment.

The integration of the Internet of Things (IoT) into healthcare systems has transformed the way medical data is collected, analyzed, and utilized. By enabling continuous monitoring of patient health, IoT medical devices allow healthcare providers to detect potential issues early, make timely interventions, and track patient progress over time. In doing so, they support the management of chronic diseases like cardiovascular diseases, diabetes, and respiratory disorders.

Read Full Report with Table of Contents: https://www.expertmarketresearch.com/reports/iot-medical-devices-market

Key factors contributing to the growth of the IoT medical devices market include increasing healthcare demands due to an ageing population, advancements in wireless technology, and the growing emphasis on personalized healthcare. The increasing number of patients with chronic diseases, such as hypertension and diabetes, is further driving demand for IoT-enabled monitoring solutions that provide continuous care and improve patient outcomes.

IoT Medical Devices Market Dynamics

Several dynamics are influencing the growth and transformation of the IoT medical devices market. These include both driving forces and challenges that impact the adoption of IoT solutions in healthcare.

1. Rising Prevalence of Chronic Diseases

The increasing prevalence of chronic diseases like cardiovascular diseases, diabetes, and respiratory conditions is a significant factor driving the demand for IoT medical devices. These conditions require continuous monitoring, making remote health management solutions essential for improving patient care. IoT medical devices, such as wearable ECG monitors, glucose sensors, and blood pressure monitors, help manage these conditions by providing real-time data to healthcare professionals.

2. Technological Advancements in IoT

Technological advancements in sensors, data analytics, and wireless communication are key enablers of the IoT medical devices market. Innovations in sensor technology allow for more accurate and reliable health monitoring. Additionally, the growth of 5G networks and other advanced communication technologies enables faster data transfer, real-time monitoring, and improved connectivity, making IoT devices even more effective for healthcare applications.

3. Shift Towards Remote Healthcare and Telemedicine

The shift towards remote healthcare and telemedicine is one of the most significant trends in the healthcare industry. With the advent of IoT medical devices, remote patient monitoring has become increasingly accessible. Devices such as wearable health trackers and connected diagnostic tools enable healthcare providers to remotely monitor patients, reducing the need for in-person visits and improving access to care, especially in rural and underserved areas.

4. Increasing Adoption of Smart Hospitals

The rise of smart hospitals, which integrate advanced technologies such as IoT, AI, and big data analytics, is contributing to the expansion of the IoT medical devices market. Smart hospitals leverage IoT devices to monitor patient vitals, track equipment, manage inventories, and ensure more efficient healthcare delivery. The use of IoT in hospitals improves patient care, reduces operational costs, and enhances the overall healthcare experience.

5. Regulatory and Security Challenges

One of the main challenges facing the IoT medical devices market is the regulatory landscape and security concerns. As IoT devices generate sensitive patient data, ensuring data privacy and compliance with health regulations such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States or GDPR in Europe is critical. Additionally, cybersecurity risks related to the hacking or malfunctioning of IoT devices could lead to data breaches or jeopardise patient safety.

External IoT Medical Devices Market Trends

The IoT medical devices market is experiencing various external trends that are shaping its future growth. These trends are largely driven by the need for improved patient care, efficient healthcare delivery, and advancements in technology.

1. Integration of Artificial Intelligence (AI) and Machine Learning (ML)

The integration of AI and machine learning with IoT medical devices is transforming healthcare. These technologies allow for real-time analysis of patient data collected by IoT devices. AI-powered IoT devices can provide predictive insights, such as detecting early warning signs of health complications, which helps in timely intervention. The ability to analyse large volumes of health data also supports more personalised treatment plans.

2. Wearable Devices and Fitness Trackers

Wearable devices are among the fastest-growing segments within the IoT medical devices market. Devices such as smartwatches, fitness trackers, and wearable ECG monitors are enabling individuals to monitor their health in real time. These wearables collect data related to heart rate, blood oxygen levels, sleep patterns, and activity levels. This data can be shared with healthcare providers for more accurate diagnoses and proactive management of chronic diseases.

3. Development of Implantable IoT Devices

Implantable IoT devices are emerging as a significant trend in the healthcare industry. These devices, such as pacemakers and insulin pumps, continuously monitor patients' health and transmit data to healthcare providers. Implantable devices can also be used to administer treatments autonomously, such as regulating blood sugar levels or controlling heart rate, further improving patient outcomes and reducing hospital visits.

4. Adoption of Blockchain for Data Security

To address concerns about the security and privacy of patient data, the adoption of blockchain technology is becoming increasingly popular in the IoT medical devices market. Blockchain offers a secure, transparent, and tamper-proof method of storing and sharing health data. It ensures that only authorised individuals can access sensitive patient information, addressing concerns about data breaches and cyberattacks.

5. Collaborations and Partnerships for Innovation

Healthcare providers, medical device manufacturers, and technology companies are forming strategic partnerships to drive innovation in the IoT medical devices market. Collaborations between hospitals, device manufacturers, and AI solution providers are enabling the development of more effective IoT-enabled healthcare solutions. These partnerships are also helping accelerate the adoption of IoT technologies in healthcare settings.

IoT Medical Devices Market Segmentation

The IoT medical devices market can be segmented based on various factors, including device type, application, end-user, and region. This segmentation helps in understanding the diverse applications of IoT technology in healthcare and the specific needs of different market segments.

1. By Device Type

Wearable Medical Devices: This segment includes fitness trackers, smartwatches, and wearable ECG monitors that track a range of health metrics like heart rate, physical activity, and sleep patterns.

Implantable Medical Devices: This category includes devices such as pacemakers, insulin pumps, and implantable defibrillators, which provide continuous monitoring and treatment.

Portable Medical Devices: These devices, such as portable oxygen concentrators and handheld ultrasound machines, allow for easy mobility and use in remote or homecare settings.

In-Home Medical Devices: In-home IoT devices, such as blood glucose monitors, thermometers, and pulse oximeters, enable individuals to monitor their health and manage chronic conditions from the comfort of their homes.

2. By Application

Cardiovascular Monitoring: IoT medical devices are extensively used for monitoring heart conditions. Devices like wearable ECG monitors, blood pressure cuffs, and implantable pacemakers enable real-time monitoring of cardiovascular health, helping to manage conditions like hypertension and arrhythmias.

Diabetes Management: IoT-enabled glucose monitors, insulin pumps, and continuous glucose monitoring systems allow patients with diabetes to track their blood sugar levels and receive insulin automatically, improving their overall health management.

Respiratory Monitoring: Devices like smart inhalers and portable oxygen concentrators are used to monitor and treat respiratory conditions like asthma and chronic obstructive pulmonary disease (COPD).

Remote Patient Monitoring: Remote monitoring devices are used for managing a variety of chronic conditions and monitoring patients outside of clinical settings, ensuring timely interventions and reducing hospital readmissions.

3. By End-User

Hospitals and Healthcare Providers: Hospitals remain the largest end-users of IoT medical devices. These institutions use a wide range of devices to monitor patients in real-time, enhance diagnostic accuracy, and provide more efficient care.

Home Healthcare: With the rise of homecare services, patients can now use IoT medical devices to monitor their health remotely and manage chronic conditions without frequent visits to healthcare facilities.

Ambulatory Care Centers: These centers use IoT devices to monitor patients and manage treatments, particularly for those with chronic illnesses or post-surgical care needs.

Research and Clinical Trials: IoT devices are also used in research settings to monitor patient health during clinical trials, collecting data to assess treatment efficacy and improve medical research.

4. By Region

North America: North America is the largest market for IoT medical devices, driven by high healthcare expenditure, advanced healthcare infrastructure, and a growing adoption of telemedicine and remote monitoring solutions.

Europe: Europe follows closely behind, with increasing government initiatives to improve healthcare through digital health solutions and IoT devices. The region is expected to witness steady growth in the coming years.

Asia-Pacific: The Asia-Pacific region is emerging as a significant market for IoT medical devices due to rising healthcare needs, a growing geriatric population, and increasing healthcare spending in countries like China, India, and Japan.

Latin America and Middle East & Africa: These regions are expected to witness gradual growth, driven by improvements in healthcare infrastructure and increasing awareness about IoT medical devices.

COVID-19 Impact Analysis

The COVID-19 pandemic had a significant impact on the IoT medical devices market. The demand for remote healthcare solutions surged as healthcare providers sought ways to monitor patients without requiring in-person visits. This led to increased adoption of IoT medical devices for telemedicine, homecare, and remote patient monitoring.

The pandemic also accelerated the development and deployment of contactless health monitoring solutions. Wearables, smart thermometers, and remote patient monitoring devices became essential tools for managing the health of individuals and preventing the spread of the virus.

Additionally, the global supply chain disruptions during the pandemic affected the availability of IoT medical devices, causing temporary delays in the delivery of some devices. However, the long-term impact has been positive, with greater investment in healthcare technology and digital transformation of the healthcare sector.

Key Players in the IoT Medical Devices Market

Several leading companies are driving innovation and growth in the IoT medical devices market:

Medtronic (Ireland): Medtronic is a global leader in medical technology, offering a wide range of IoT-enabled medical devices for cardiovascular monitoring, diabetes management, and other healthcare applications.

Cisco Inc (USA): Cisco provides advanced networking and communications solutions that enable the efficient and secure transmission of medical data from IoT devices to healthcare providers, enhancing telemedicine and remote monitoring capabilities.

GENERAL ELECTRIC (USA): GE Healthcare offers IoT-enabled imaging and monitoring devices used in hospitals and healthcare facilities for patient diagnosis, monitoring, and treatment.

FAQ

1. What are IoT medical devices?

IoT medical devices are interconnected devices that collect and transmit patient data in real-time, enabling healthcare providers to monitor and manage patients' health remotely. These devices include wearables, implantables, and remote monitoring tools.

2. How do IoT medical devices improve patient care?

IoT medical devices allow for continuous health monitoring, providing real-time insights that enable timely interventions and improved management of chronic diseases. This leads to better patient outcomes, reduced hospital visits, and more personalised care.

3. What are the benefits of using IoT medical devices in hospitals?

In hospitals, IoT medical devices enhance patient monitoring, reduce the risk of medical errors, improve operational efficiency, and facilitate timely decision-making by healthcare professionals.

4. How does the IoT medical devices market impact the healthcare industry?

The IoT medical devices market is transforming the healthcare industry by enabling remote patient monitoring, improving diagnostic accuracy, enhancing patient outcomes, and reducing healthcare costs.

#health and wellness#healthcare#market research report#market research#Global IoT Medical Devices Market Report and Forecast 2024-2032

0 notes

Text

Empowering Healthcare Providers with Precision Blood Screening Tools

Blood Screening Industry Overview

The global blood screening market size is expected to reach USD 6.62 billion by 2030, registering a CAGR of 11.9% from 2025 to 2030, according to a new report by Grand View Research, Inc. The growth of the market is attributed to the increase in screening of donor and continuous technological advancement by the market players. Demand for blood screening tests is increasing continuously due to increasing donation, rising awareness about transfusion-transmitted diseases, and technological developments in the industry. Furthermore, governments of various countries are in process to mandates testing all donated blood for several viruses.

Thorough screening is necessary for all donated blood to ensure that recipients receive the safest products. As of 2015, such testing consists of screening for red cell antibodies, and the infectious diseases agents: HIV-1, HIV-2, hepatitis virus, West Nile Virus (WNV), Human T-Lymphotropic Virus (HTLV) T. Cruzi, and T. pallidum (syphilis). The result of all these assays must be negative for blood donation.

Gather more insights about the market drivers, restrains and growth of the Blood Screening Market

Technological developments increase the sensitivity and efficiency of the tests. For instance, in 2016, the U.S. FDA approved the Procleix Zika virus assay from Hologic, Inc. and Grifols to screen donated blood. Furthermore, the U.S. FDA approved next-generation sequencing (NGS) technology in 2013. The technology is cheaper and faster than previous DNA analysis methods.

Browse through Grand View Research's Clinical Diagnostics Industry Research Reports.

The global body fluid collection and diagnostics market size was estimated at USD 34.35 billion in 2024 and is projected to grow at a CAGR of 6.6% from 2025 to 2030.

The global genetic testing market size was estimated at USD 11.71 billion in 2024 and is projected to grow at a CAGR of 22.5% from 2025 to 2030.

Blood Screening Market Segmentation

Grand View Research has segmented global blood screening market report based on technology, product, and region:

Blood Screening Technology Outlook (Revenue, USD Million, 2018 - 2030)

Nucleic Acid Amplification Test (NAT)

ELISA

Chemiluminescence Immunoassay (CLIA & EIA )

Next Generation Sequencing (NGS)

Western Blotting (WB)

Blood Screening Product Outlook (Revenue, USD Million, 2018 - 2030)

Reagent

Instrument

Blood Screening Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Norway

Denmark

Sweden

Asia Pacific

India

Japan

China

South Korea

Australia

Thailand

Latin America

Brazil

Argentina

Middle East and Africa (MEA)

Saudi Arabia

South Africa

UAE

Kuwait

Key Companies profiled:

Abbott

Danaher Corporation (Beckman Coulter)

Becton Dickinson and Company

Bio-Rad Laboratories, Inc.

Hoffman-La Roche Ltd.

Grifols, S.A.

Ortho-Clinical Diagnostics, Inc.

Siemens Healthcare GmbH

Thermo Fisher Scientific, Inc.

SOFINA s.a (Biomerieux)

Key Blood Screening Company Insights

Some of the key companies in the market include Bio-Rad Laboratories, Inc., Hoffman-La Roche Ltd., Grifols, S.A., and others. These companies adopt strategies such as strategic collaborations to enhance innovation, mergers, and acquisitions to expand capabilities, and new product launches to address evolving healthcare needs, ensuring competitiveness and a strong market presence.

Abbott manufactures specialized medical equipment that may utilize Blood Screening components for durability and lightweight properties. Beyond blood screening, Abbott operates in various segments, including laboratory diagnostics, cardiovascular devices, diabetes care, and nutrition products, thereby enhancing its portfolio and addressing diverse healthcare needs.

Bio-Rad Laboratories, Inc. develops diagnostic instruments that may incorporate Blood Screening materials for enhanced performance and reliability in relation to Blood Screening. The company also engages in other segments, such as quality control products, gene expression analysis, and protein purification, positioning itself as a leader in both research and clinical settings.

Recent Developments

In May 2023, Siemens Healthineers launched two new analyzers, the Atellica HEMA 570 and Atellica HEMA 580, designed for high-volume hematology testing, crucial for blood screening. These advanced devices can streamline the complete blood count (CBC) process, offering rapid results and improved workflow efficiency. With the ability to process up to 120 tests per hour, these analyzers can address the growing demand for timely diagnostics in critical care settings.

Order a free sample PDF of the Blood Screening Market Intelligence Study, published by Grand View Research.

0 notes

Text

The Disposable Hypodermic Syringes Market is projected to grow significantly, with its market size estimated to increase from USD 4,395 million in 2024 to USD 9,037.53 million by 2032, reflecting a compound annual growth rate (CAGR) of 9.43% during the forecast period. The global disposable hypodermic syringes market is witnessing robust growth, fueled by advancements in healthcare, rising prevalence of chronic diseases, and increasing awareness of safety protocols in medical practices. Disposable syringes, primarily used for administering medications and vaccinations, have become indispensable in modern healthcare due to their convenience, affordability, and ability to reduce the risk of cross-contamination. This article explores the dynamics, drivers, challenges, and future prospects of this essential medical device market.

Browse the full report at https://www.credenceresearch.com/report/disposable-hypodermic-syringes-market

Market Overview

Disposable hypodermic syringes are single-use medical devices designed for various healthcare applications, such as drug administration, blood collection, and therapeutic injections. Unlike reusable syringes, they are designed to be discarded after a single use, ensuring hygienic and safe practices.

Globally, the market is experiencing significant growth, with projections indicating a compound annual growth rate (CAGR) of around 5-7% from 2023 to 2030. Key factors contributing to this growth include the rising demand for vaccinations, especially following the COVID-19 pandemic, and increased government initiatives promoting safe injection practices.

Key Market Drivers

Increased Demand for Vaccination Programs Vaccination programs, particularly in response to global health crises like COVID-19, have driven the mass production and use of disposable syringes. The rollout of immunization programs for diseases such as measles, influenza, and polio has further fueled market demand.

Rising Prevalence of Chronic Diseases Chronic conditions such as diabetes, cardiovascular diseases, and cancer require frequent administration of injectable medications. The rising incidence of these diseases globally has boosted the demand for disposable syringes.

Enhanced Safety and Infection Control Measures The use of disposable syringes eliminates the risk of needle-sharing and cross-contamination. Governments and health organizations, such as the World Health Organization (WHO), advocate for the use of auto-disable syringes, which render them unusable after a single use.

Technological Advancements Innovations such as syringes with built-in safety features (e.g., retractable needles) and eco-friendly materials are enhancing product appeal and compliance with safety standards.

Challenges

Environmental Concerns The disposal of single-use plastic syringes poses a significant environmental challenge. Regulatory agencies and manufacturers are exploring biodegradable and recyclable materials to address this issue.

Price Sensitivity in Developing Markets While safety syringes are gaining popularity, their higher costs remain a barrier in low- and middle-income countries.

Counterfeit Products The market faces challenges from counterfeit syringes, which can compromise patient safety and tarnish brand reputations.

Future Prospects

The disposable hypodermic syringes market is poised for sustained growth, driven by the following:

Regulatory Push: Governments mandating the use of safety syringes and banning reusable options in healthcare facilities.

R&D Investments: Manufacturers investing in innovative products that balance safety, cost-effectiveness, and environmental sustainability.

Global Health Initiatives: Programs by organizations like UNICEF and Gavi to vaccinate underserved populations.

Key Player Analysis:

Becton, Dickinson and Company (BD)

Terumo Corporation

Nipro Corporation

Braun Melsungen AG

Smiths Medical

Cardinal Health

Hindustan Syringes & Medical Devices Ltd. (HMD)

Gerresheimer AG

Retractable Technologies, Inc.

Teleflex Incorporated

Segmentations:

By Material Type:

Polymer Syringes

Cyclic Olefin Polymers (COP)

Cyclic Olefin Copolymers (COC)

Polypropylene and Other Polymers

Glass Syringes

By Sales Channel:

Manufacturers

Distributors

Retailers

By End User:

Hospital

Diabetic Care Centers

Blood Collection Centers

Veterinary Care Centers

Clinics

By Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/disposable-hypodermic-syringes-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Blood Collection Market to Grow with a High CAGR- Global Industry Analysis, Key Manufacturers, Trends, Size

Analysis of Blood Collection Market Size by Research Nester Reveals the Market to grow with a CAGR of 7.2% During 2025-2037 and Attain USD 28.8 billion by 2037

Research Nester assesses the growth and market size of the global blood collection market, which is anticipated to be driven by the increasing prevalence of chronic disorders.

Research Nester’s recent market research analysis on “Blood Collection Market: Global Demand Analysis & Opportunity Outlook 2037” delivers a detailed competitors analysis and a detailed overview of the global blood collectionmarket in terms of market segmentation by product type, method, application, end user, and by region.

Automated Blood Collection Systems Gaining Widespread Adoption

The integration of automation and robotics in blood collection is anticipated to transform the medical device landscape both in terms of efficiency and accuracy. Automated blood collection systems are gaining traction owing to their accuracy and effectiveness with minimal human intervention. Several manufacturers are developing easy-to-use automated blood collection kits particularly targeting at-home patients. Easy portability and on-site blood tests and results are driving the demand for automated blood collection systems in various settings such as emergency rooms and outpatient clinics.

Growth Drivers:

Rising population of senior citizens who are more prone to chronic disorders

Increasing number of surgical procedures and growing awareness regarding blood donation

Challenges

The technological advancements in the blood collection systems have the potential to improve patient care but their high costs may limit their access in poor economies. Advanced blood collection systems such as automated devices require a high upfront investment in research and development activities, which drives up the overall production costs.

High-tech blood collection devices may require regular maintenance, which can be quite expensive. Furthermore, for handling such innovative products the availability of experienced staff or technicians is a must, which again increases the operational cost.

Access our detailed report at: https://www.researchnester.com/reports/blood-collection-market/6474

By end user, the hospitals and clinics segment is estimated to capture 40.5% [SG1] of the revenue share through 2037. Hospitals and clinics have a high patient intake as they prefer them as the first choice of option for medical care. These high patient visits to hospitals and clinics are driving the sales of blood collection solutions. The presence of advanced diagnostic facilities in hospitals is also contributing to the overall market growth.

Based on region, North America is projected to hold a market share of 45.5% [SG2] through 2037. The presence of key market players and cutting-edge healthcare infrastructure is driving the blood collection market growth in North America. The rising prevalence of chronic disorders such as diabetes, cardiovascular diseases, and cancer, which necessitates regular blood testing is boosting the sales of blood collection solutions in the region.

Customized report@ https://www.researchnester.com/customized-reports-6474

This report also provides the existing competitive scenario of some of the key players of the global blood collection market which includes company profiling of Becton, Dickinson and Company, Thermo Fisher Scientific Inc., Cardinal Health, Inc., F. Hoffmann-La Roche Ltd., FL MEDICAL s.r.l., Fresenius SE & Co. KGaA, Medtronic Plc, QIAGEN N.V., Haemonetics Corporation, Greiner AG, Sarstedt AG & Co. KG, and Siemens Healthineers AG.

Request Report Sample@ https://www.researchnester.com/sample-request-6474

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates and executives to take wise decisions for their future marketing strategy, expansion and investment etc. We believe every business can expand to its new horizon, provided a right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decision in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

0 notes

Link

#market research future#venous blood collection#venous blood collection device#blood collection device market#venous blood size

0 notes

Text

Continuous Renal Replacement Therapy Market 2030 - In-Depth Analysis on Size, Trends & Prominent Key Players

The global continuous renal replacement therapy market was valued at USD 1,356.7 million in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 8.6% from 2023 to 2030. Factors contributing to this growth include the rising incidence of acute kidney injury (AKI), an increase in sepsis cases, the rapid expansion of hospitals and urgent care centers, growing hospital admission rates, and continuous product innovations by leading companies. The American Kidney Fund reports that 37 million Americans are living with kidney disease, and around 807,000 individuals in the U.S. have been diagnosed with kidney failure.

Demand for advanced CRRT devices is a major driver in the market due to improved patient outcomes. The latest CRRT technology allows for comprehensive analysis and response to technical data, significantly enhancing quality assurance. These technological advancements have led to a more precise evaluation of prescription and delivery patterns, positively impacting clinical results. Modern CRRT devices enable automated data collection and use standardized language, facilitating comparisons across institutions. Leading manufacturers have introduced sophisticated CRRT machines incorporating these capabilities, which is expected to further accelerate market growth.

Gather more insights about the market drivers, restrains and growth of the Continuous Renal Replacement Therapy Market

Additionally, the development of specialized CRRT products for pediatric patients is anticipated to boost the market. Traditionally, pediatric CRRT cases have relied on systems designed for adults, which are not specifically licensed for pediatric use, posing potential clinical challenges, especially for neonates. To address these issues, several manufacturers now provide a range of renal care solutions to improve access, outcomes, and quality of life for pediatric patients with severe renal conditions, driving market expansion globally.

According to the American Hospital Association, in 2023, the U.S. had 5,157 community hospitals, 206 federal government hospitals, and 107 other hospitals. An increase in hospital admissions for AKI and a growing elderly population are fueling the demand for CRRT systems. Moreover, the Centers for Disease Control and Prevention (CDC) reported that, as of 2021, approximately 786,000 Americans had end-stage renal disease (ESRD), also known as end-stage kidney disease (ESKD), with 71% on dialysis and 29% with a kidney transplant. In 2020, there were around 7,500 dialysis clinics in the U.S., underscoring the need for CRRT solutions.

Modality Segmentation Insights:

The CRRT market can be segmented into different modalities: slow continuous ultrafiltration (SCUF), continuous venovenous hemofiltration (CVVH), continuous venovenous hemodialysis (CVVHD), and continuous venovenous hemodiafiltration (CVVHDF). In 2022, the CVVH segment led the market with a revenue share of 31.6%, driven by the high prevalence of fluid overload among AKI patients in critical care settings. Fluid overload, often seen in congestive heart failure cases, significantly impacts dialysis patients. According to an article in Elsevier, congestive heart failure accounted for roughly 5% of all-cause mortality among dialysis patients, a condition closely related to fluid overload. This association is expected to increase demand for CVVH treatment.

The CVVHDF segment is anticipated to grow at the fastest CAGR of 9.2% over the forecast period. CVVHDF, which utilizes a highly effective hemodiafilter, enables the combined removal of fluid and solutes, merging both hemodialysis and hemofiltration techniques. This treatment involves comprehensive fluid and solute clearance from the blood and has become the most commonly used CRRT modality for AKI in various countries. CVVH was the primary CRRT modality until CVVHDF was introduced in 2008, which quickly became the dominant CRRT approach. CVVHDF’s association with higher survival rates relative to other CRRT options is expected to contribute to its rapid market growth in the coming years.

Order a free sample PDF of the Continuous Renal Replacement Therapy Market Intelligence Study, published by Grand View Research.

#Continuous Renal Replacement Therapy Market Analysis#Continuous Renal Replacement Therapy Market Trends

0 notes

Text

Global Medical Kiosk Market Insights: Innovations and Forecast

The global medical kiosk market has seen considerable growth in recent years, driven by the increasing adoption of digital health technologies, rising demand for accessible healthcare solutions, and improvements in patient engagement. Medical kiosks, which can provide a variety of healthcare services, play a crucial role in meeting these needs. From patient check-ins and diagnostics to telehealth services, these kiosks help streamline healthcare operations and improve patient experiences. The medical kiosk market overview highlights the growing demand for these devices in hospitals, clinics, pharmacies, and even non-traditional healthcare settings, such as retail stores and airports, where convenient access to basic healthcare services is highly valued.

The Medical Kiosk Market Size was projected to reach 2.28 billion USD in 2022, according to MRFR analysis. By 2032, the medical kiosk market is projected to have grown from 2.52 billion USD in 2023 to 6.1 billion USD. It is anticipated that the Medical Kiosk Market would develop at a CAGR of approximately 10.33% between 2024 and 2032.

Medical Kiosk Market Size

As the healthcare industry continues to innovate and expand its technological footprint, the medical kiosk market size is expected to grow significantly over the forecast period. Recent studies indicate that the market size is poised for robust growth due to the escalating adoption of self-service technologies and the increased need for contactless healthcare solutions, especially in light of the COVID-19 pandemic. Many healthcare providers and facilities are investing in medical kiosks to streamline services and reduce waiting times, providing an efficient solution that saves resources. The medical kiosk market size growth is also driven by advancements in artificial intelligence (AI) and Internet of Things (IoT) technologies, which enhance kiosk functionalities and create a more seamless healthcare experience.

Medical Kiosk Market Share

When analyzing the medical kiosk market share, North America has historically dominated due to high technology adoption rates, established healthcare infrastructure, and increasing investments in healthcare IT. However, other regions such as Asia-Pacific and Europe are catching up, with a notable rise in installations in emerging economies due to government initiatives to improve healthcare access. The medical kiosk market share is also segmented by type, including diagnostic kiosks, telemedicine kiosks, and self-service kiosks. Diagnostic kiosks have gained a significant share due to their ability to perform basic health assessments and diagnostics, which are particularly valuable in remote or underserved areas.

Medical Kiosk Market Analysis

A comprehensive medical kiosk market analysis shows that the demand for medical kiosks is fueled by factors like the growing emphasis on patient-centric care, cost reduction, and the need for efficient healthcare management solutions. The analysis also reveals that medical kiosks are widely adopted in emergency departments and outpatient settings, where they assist with check-in, data collection, and other administrative functions, freeing up healthcare staff to focus on critical care tasks. Additionally, technological advancements, such as integration with electronic health records (EHRs) and secure data handling capabilities, contribute to the rising demand for medical kiosks.

Medical Kiosk Market Trends

One of the major medical kiosk market trends is the integration of telehealth capabilities within kiosks. This trend addresses the growing demand for virtual healthcare, allowing patients to connect with healthcare professionals remotely for consultations. Another trend is the use of biometric and AI-based diagnostic tools, enabling kiosks to perform various health checks, such as temperature measurement, blood pressure monitoring, and symptom checking, without the need for direct patient-provider interaction. Furthermore, the rise of multifunctional kiosks capable of handling multiple healthcare services is reshaping the market, as healthcare facilities prefer all-in-one solutions to meet diverse patient needs.

Reasons to Buy the Reports

In-depth Market Insights: Reports provide a detailed medical kiosk market overview, including current trends, market size, and competitive landscape, which aids businesses in understanding the market's dynamics.

Strategic Planning: Reports offer data-driven insights that help companies make informed decisions and formulate effective strategies for entering or expanding within the medical kiosk market.

Forecast and Growth Opportunities: Access to accurate market forecasts allows stakeholders to identify and capitalize on growth opportunities in the medical kiosk market size.

Competitive Analysis: Reports include analysis of key players and their market share, assisting businesses in evaluating the competitive landscape and identifying potential collaborators or competitors.

Technological Advancements: Insights into recent advancements, such as AI integration and telehealth capabilities in medical kiosks, help companies stay updated on innovations shaping the medical kiosk market.

Recent Developments

Recent developments in the medical kiosk market include the adoption of AI-powered diagnostic tools, which improve the accuracy and range of self-service health assessments. Telemedicine integration has also become a major feature, especially post-COVID-19, enabling remote consultations from kiosks. Furthermore, partnerships between tech companies and healthcare providers are growing, aiming to expand the functionality of medical kiosks in terms of software and hardware. Additionally, regulatory approvals and government funding initiatives in countries focused on digital healthcare are accelerating kiosk installations in public spaces, contributing to increased accessibility and convenience in healthcare services.

Overall, the medical kiosk market shows strong potential for growth and innovation, supported by trends in digital healthcare, AI, and IoT technologies, which are set to redefine healthcare access and service delivery across the globe.

Related reports:

snp genotyping and analysis market

soft tissue allograft market

spinal surgery device market

sterile injectable market

Top of Form

Bottom of Form

0 notes

Link

0 notes