#Bio Feedstocks Market Trend

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The most popular pages on Tumblr are about Minecraft, GIFs, and David J. Peterson.

Text

Global Bio Feedstocks Market Size Expected To Reach USD 25848 Million With CAGR 23.20% By 2030

The Global Bio Feedstocks Market size was reasonably estimated to be approximately USD 6000 Million in 2023 and is poised to generate revenue over USD 25848 Million by the end of 2030, projecting a CAGR of around 23.20% from 2023 to 2030.

Any material obtained from a biological source and used to produce energy or other goods is referred to as bio-based feedstock. It includes a broad variety of organic elements, including waste from organic processes, crops, forestry byproducts, and agricultural residues. Since these feedstocks come from living things and may be restored by natural processes, they are renewable resources.

Bio-based feedstocks are used in the production of bioenergy, biofuels, biochemicals, and bioplastics. They provide a sustainable substitute for fossil fuels and non-renewable resources in these sectors. We can lessen our reliance on finite resources, cut greenhouse gas emissions, and advance a circular economy that is more ecologically friendly by using bio-based feedstocks.

Biofuels like biodiesel, sustainable diesel, and bioethanol can be produced from bio-based feedstocks like algae, plant-based oils, and animal fats. By replacing fossil fuels in transportation, these fuels lower carbon emissions and lessen reliance on depleting petroleum supplies.

Bio-based feedstocks can be processed to yield a wide range of substances. Biomass can be converted, for instance, into biodegradable packaging materials, biobased polymers, and biocomposites. The synthesis of bio-based compounds, such as bio-based lubricants, solvents, and polymers, can begin with plant oils and sugars.

Leading players involved in the Bio Feedstocks Market include:

"Beta Renewables (Italy), DowDuPont (US), Enerkem (Canada), Fiberight (US), GranBio (Brazil), VIRENT (US), Clariant (Switzerland), Abengoa (Spain), BASF (Germany), INEOS Bio (Switzerland), DSM (Netherlands), Cargill (US), Novozymes (Denmark), DSM (Netherlands), Roquette (France), Total Corbion PLA (Netherlands), Braskem (Brazil), Amyris (US) and Other Major Players".

Get Sample Report: -

Updated Version 2024 is available our Sample Report May Includes the:

Scope For 2024

Brief Introduction to the research report.

Table of Contents (Scope covered as a part of the study)

Top players in the market

Research framework (structure of the report)

Research methodology adopted by Worldwide Market Reports

Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years.

Market Driver:

One major driver propelling the bio feedstocks market is the rising concerns over climate change and the need to reduce carbon footprint. Governments worldwide are implementing strict regulations to limit greenhouse gas emissions, promoting the adoption of sustainable practices across industries. Bio feedstocks offer a viable solution as they are derived from renewable sources and have lower carbon emissions compared to fossil-based alternatives. This regulatory push, coupled with increasing consumer preference for eco-friendly products, is driving the demand for bio feedstocks in various applications.

Market Opportunity:

An emerging opportunity in the bio feedstocks market lies in the development of advanced technologies for efficient production and processing. Innovations in biotechnology, such as genetic engineering and fermentation processes, present opportunities to enhance the yield and quality of bio feedstocks while reducing production costs. Additionally, there is a growing focus on utilizing non-food biomass sources, such as agricultural residues and municipal solid waste, to produce bio-based feedstocks, thereby addressing concerns related to food security and land use. Capitalizing on these technological advancements and diversifying feedstock sources could unlock new growth avenues for market players.

If You Have Any Query Bio Feedstocks Market Report, Visit:

Segmentation of Bio Feedstocks Market:

By Type

Starch

Oils

Cellulose & Lignin

Proteins

Others

By Application

Energy

Pulp & Paper

Food industry

Pharmaceuticals

Chemicals

Others

By Regions: -

North America (US, Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

Effective Points Covered in Bio Feedstocks Market Report: -

Details Competitor analysis with accurate, up-to-date demand-side dynamics information.

Standard performance against major competitors.

Identify the growth segment of your investment.

Understanding most recent innovative development and supply chain pattern.

Establish regional / national strategy based on statistics.

Develop strategies based on future development possibilities.

Purchase This Reports: -

About Us:

We are technocratic market research and consulting company that provides comprehensive and data-driven market insights. We hold the expertise in demand analysis and estimation of multidomain industries with encyclopedic competitive and landscape analysis. Also, our in-depth macro-economic analysis gives a bird's eye view of a market to our esteemed client. Our team at Pristine Intelligence focuses on result-oriented methodologies which are based on historic and present data to produce authentic foretelling about the industry. Pristine Intelligence's extensive studies help our clients to make righteous decisions that make a positive impact on their business. Our customer-oriented business model firmly follows satisfactory service through which our brand name is recognized in the market.

Contact Us:

Office No 101, Saudamini Commercial Complex,

Right Bhusari Colony,

Kothrud, Pune,

Maharashtra, India - 411038 (+1) 773 382 1049 +91 - 81800 - 96367

Email: [email protected]

#Bio Feedstocks#Bio Feedstocks Market#Bio Feedstocks Market Size#Bio Feedstocks Market Share#Bio Feedstocks Market Growth#Bio Feedstocks Market Trend#Bio Feedstocks Market segment#Bio Feedstocks Market Opportunity#Bio Feedstocks Market Analysis 2022#US Bio Feedstocks Market#Bio Feedstocks Market Forecast#Bio Feedstocks Industry#Bio Feedstocks Industry Size#china Bio Feedstocks Market#UK Bio Feedstocks Market

0 notes

Text

https://akvisintelligence.com/reports/bio-feedstocks-market

#Bio Feedstocks Market#Bio Feedstocks Size#Bio Feedstocks Growth#Bio Feedstocks Trend#Bio Feedstocks segment#Bio Feedstocks Opportunity#Bio Feedstocks Analysis 2024#Bio Feedstocks Forecast

0 notes

Text

#Bio Feedstocks Market#Bio Feedstocks Market Size#Bio Feedstocks Market Trends#Bio Feedstocks Market Growth#Bio Feedstocks Market Opportunities#Bio Feedstocks Market Analysis

0 notes

Quote

The Global Bio Feedstocks Market size was reasonably estimated to be approximately USD 6000 Million in 2023 and is poised to generate revenue over USD 25848 Million by the end of 2030, projecting a CAGR of around 23.20% from 2023 to 2030.

Global Bio Feedstocks Market Research Report 2023

0 notes

Text

Future of U.S. Geosynthetics Market: Insights from Industry Experts

The U.S. geosynthetics market size was estimated at USD 3.08 billion in 2023 and is expected to grow at a CAGR of 5.8% from 2024 to 2030. The U.S. is expected to account for a significant market share of the total shale gas consumption in the future on account of increasing drilling activities for shale gas and tight oil supply conditions. This is projected to positively drive the geosynthetics market in the country over the forecast period.

Geosynthetics are used for base reinforcement, separation, and stabilization of roads and pavements. Furthermore, these products also find their application in subsurface drainage systems for dewatering, road base, and structure drainage. Geotextiles are used in the strengthening of industrial units, car parks, and new roadways. The incorporation of geosynthetics entails sustainable development, a small volume of earthwork, low carbon footprint, and an increased rate of construction. The growth of the construction industry around the world, including the U.S., is expected to remain one of the key market drivers for the global geosynthetics market, further boosting the market in the U.S.

Gather more insights about the market drivers, restrains and growth of the U.S. Geosynthetics Market

Key U.S. Geosynthetics Company Insights

The market is majorly run by petrochemical manufacturers across the U.S. The competition in the market is also high due to the presence of a large number of manufacturers. Market players have established strategic partnerships with the distributors to supply their product offerings. Stringent government regulations and depleting petroleum feedstock have contributed to shifting the focus of manufacturers on renewable energy sources and prompted extensive research and development of bio-based raw materials.

Some of the prominent players in the U.S. geosynthetics market are TenCate Geosynthetics Americas; Maccaferri; Concrete Canvas Ltd.; NAUE GmbH & Co. KG; and Propex Operating Company, LLC

• NAUE GmbH & Co. KG, formerly known as Naue Fasertechnik GmbH & Co. KG, was established in 1967. It changed its name to NAUE GmbH & Co. KG in 2005. The company has its headquarters in Germany, with a global presence across North America, Asia, Europe, Australia, South America, and the Middle East & Africa.

• Maccaferri provides advanced solutions for problems related to erosion control, soil reinforcement, stabilization of the soil, and infrastructure development in application areas such as roads, railways, canals, rivers, coastal defenses, and landfills. It owns over 70 subsidiaries in over 100 countries. As of 2018, the company employed over 3,000 individuals globally.

• TENAX Group was established in 1960 and headquartered in Viganò, Italy. The company majorly specializes in extruding thermoplastic polymers. Its product range includes fences, screens, plastic nets, geogrids, and geosynthetics, which find applications in areas such as pipeline, packaging, industrial, geotechnical, gardening, fencing, construction, and agriculture.

U.S. Geosynthetics Market Report Segmentation

This report forecasts market share and revenue growth at country levels and provides an analysis of industry trends in each of the sub-segments from 2018 to 2030. For the purpose of this study, Grand View Research has segmented the U.S. geosynthetics market report based on product:

Product Outlook (Volume, Million Square Meters; Revenue, USD Billion, 2018 - 2030)

• Geotextiles

o By Raw Material

o By Product

o By Application

• Geomembranes

o By Raw Material

o By Application

o By Technology

• Geogrids

o By Raw Material

o By Application

o By Product

• Geonets

o By Raw Material

o By Application

• Geocells

o By Raw Material

o By Application

Order a free sample PDF of the U.S. Geosynthetics Market Intelligence Study, published by Grand View Research.

#U.S. Geosynthetics Market#U.S. Geosynthetics Market Size#U.S. Geosynthetics Market Share#U.S. Geosynthetics Market Analysis#U.S. Geosynthetics Market Growth

0 notes

Text

Butyric Acid: A Growing Market in Health, Animal Feed, and Biotechnology

Butyric acid, a short-chain fatty acid with a distinctive rancid odor, is a key compound used in various industries, including food, pharmaceuticals, animal feed, and chemicals. Its applications range from acting as a flavoring agent and preservative in food products to being utilized in the production of butyrate supplements, which support gut health. The global butyric acid market has been experiencing steady growth, driven by increasing demand for functional food ingredients, animal feed additives, and growing awareness of the health benefits associated with butyric acid. This article explores the current trends, key drivers, challenges, and future outlook for the butyric acid market.

Market Overview and Growth Drivers

The butyric acid market has been steadily expanding as industries increasingly recognize its diverse applications. As a naturally occurring fatty acid in dairy products, butter, and some plant-based oils, butyric acid plays an important role in human health, particularly in gut microbiota regulation. Additionally, butyric acid derivatives, such as butyrate, are gaining popularity as potential dietary supplements to promote digestive health.

The rising demand for healthier, functional food ingredients is one of the key drivers of the butyric acid market. As consumer awareness of gut health and the importance of the microbiome grows, butyric acid has gained traction as a prebiotic that supports the growth of beneficial bacteria in the digestive system. This trend has contributed to the increased use of butyric acid in functional foods, dietary supplements, and even beverages.

Key Trends in the Butyric Acid Market

Growth in Animal Feed Applications: Butyric acid is commonly used as an animal feed additive to promote gut health in livestock, poultry, and pets. As the global demand for meat and poultry products rises, there is an increasing need for efficient animal feed additives that enhance the health and growth of animals. Butyric acid is valued in this segment for its ability to improve nutrient absorption, boost immune systems, and reduce pathogenic bacteria in the gut. These benefits are driving the adoption of butyric acid in animal feed formulations, particularly in emerging economies with growing agricultural industries.

Increased Demand for Butyric Acid in Pharmaceuticals and Healthcare: Butyric acid's potential health benefits are driving its growing presence in the pharmaceutical and healthcare industries. Studies have shown that butyric acid derivatives may have therapeutic effects for conditions such as inflammatory bowel disease (IBD), irritable bowel syndrome (IBS), and even cancer. The expanding pharmaceutical applications of butyric acid are a significant factor driving market growth. Furthermore, with the increasing popularity of gut health supplements, the demand for butyrate-based products is expected to rise.

Biotechnology and Renewable Production Methods: Traditional methods of producing butyric acid rely on petrochemical processes, but there is a growing shift toward using renewable resources such as plant-based feedstocks and biotechnology for its production. Advances in microbial fermentation techniques are enabling the production of bio-based butyric acid, which is more sustainable and environmentally friendly than conventional methods. This shift aligns with the growing global emphasis on sustainable and eco-friendly practices, attracting both consumers and manufacturers seeking green alternatives.

Challenges Facing the Butyric Acid Market

Despite its positive growth trajectory, the butyric acid market faces several challenges. The production process of butyric acid remains costly, particularly when utilizing sustainable methods such as fermentation. Moreover, fluctuations in raw material prices, such as the cost of feedstocks for bio-based production, could impact the market's stability. Additionally, the strong odor of butyric acid can limit its acceptance in some consumer markets, particularly in food and beverage applications, where the compound must be carefully incorporated to avoid unpleasant sensory experiences.

Regional Insights

The demand for butyric acid is widespread across regions, but the market is particularly strong in North America and Europe, where there is a high demand for functional foods, animal feed, and pharmaceutical products. The Asia-Pacific region is experiencing rapid growth, driven by expanding agriculture and pharmaceutical sectors, particularly in countries like China and India. The increasing awareness of gut health and digestive wellness in these regions is likely to contribute to continued market growth.

Future Outlook

The global butyric acid market is expected to continue expanding in the coming years, supported by rising demand across various end-use industries. The focus on functional food ingredients, animal feed applications, and the growth of bio-based production methods will likely drive the market forward. Furthermore, ongoing research into the health benefits of butyric acid and its derivatives will continue to open new opportunities in the pharmaceutical and healthcare sectors. While challenges remain, particularly in production costs and odor-related issues, the future of the butyric acid market looks promising as it aligns with evolving consumer preferences and industry trends.

Conclusion

The butyric acid market is poised for significant growth, driven by increasing demand across food, animal feed, pharmaceuticals, and biotechnology industries. As more companies explore the health benefits and sustainable production methods associated with butyric acid, the market is expected to see continued innovation and expansion. With growing consumer awareness around gut health and sustainability, butyric acid is well-positioned to meet the needs of the global market in the years ahead.

0 notes

Text

Polypropylene Filament Yarn (PPFY) Prices: Trends, Drivers, and Market Dynamics

Polypropylene Filament Yarn (PPFY) is a versatile and lightweight material widely used in textiles, packaging, and industrial applications. Its cost-effectiveness, durability, and resistance to chemical and environmental degradation make it a preferred choice in various industries. However, PPFY prices are subject to significant fluctuations, influenced by multiple factors, including raw material costs, global demand-supply dynamics, and geopolitical factors.

Current Trends in PPFY Prices

In recent years, PPFY prices have shown a mixed trend, reflecting the global economic environment and raw material volatility. As of the latest market analysis, PPFY prices have been affected by:

Feedstock Fluctuations: Polypropylene, derived from crude oil or natural gas, is the primary feedstock for PPFY production. Changes in crude oil prices directly impact polypropylene costs, which subsequently affect PPFY prices.

Supply Chain Challenges: Disruptions in the supply chain, such as shipping delays or plant shutdowns, have led to sporadic price spikes.

Regional Demand Variances: The demand for PPFY varies across regions, with Asia-Pacific being the largest consumer due to its robust textile and packaging industries. In contrast, markets in North America and Europe have shown steady but slower growth.

Get Real time Prices for Polypropylene Filament Yarn (PPFY): https://www.chemanalyst.com/Pricing-data/polypropylene-filament-yarn-ppfy-1160

Key Drivers of PPFY Prices

Several factors drive PPFY pricing dynamics:

Raw Material Costs: Polypropylene prices account for a significant portion of the total cost. Fluctuations in crude oil and natural gas prices, driven by geopolitical tensions or changes in production levels, heavily influence PPFY prices.

Manufacturing and Technology: Advances in production technology can lower costs, but investments in new machinery and processes can temporarily increase prices.

Demand from End-Use Industries: The growing demand for lightweight, durable, and cost-effective materials in automotive, construction, and textiles fuels PPFY consumption, impacting prices.

Government Policies: Tariffs, trade regulations, and subsidies for petrochemical industries in major producing countries affect global PPFY pricing.

Environmental Concerns: Increasing pressure to reduce the environmental impact of synthetic fibers has led to investments in recycling and bio-based alternatives. While this can elevate costs in the short term, it may stabilize prices in the long run.

Forecast for PPFY Prices

In the short to medium term, PPFY prices are expected to remain volatile due to global economic uncertainties and fluctuating crude oil prices. However, the rising demand from emerging economies, especially in Asia, is likely to provide a cushion against sharp price declines.

The adoption of sustainable practices and innovations in production methods may also help stabilize prices. Furthermore, the growing interest in circular economy models could lead to an increased supply of recycled polypropylene, which might impact virgin PPFY prices.

Conclusion

The PPFY market is highly dynamic, with prices influenced by an intricate interplay of raw material costs, market demand, and macroeconomic factors. Stakeholders, including manufacturers, traders, and end-users, must stay vigilant and adopt flexible strategies to navigate price fluctuations effectively. Monitoring global trends and investing in sustainable practices could provide a competitive edge in this evolving market.

By understanding these dynamics, businesses can make informed decisions and capitalize on opportunities in the PPFY sector.

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Polypropylene Filament Yarn#Polypropylene Filament Yarn Prices#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Carboxylic Acids Market

Carboxylic Acids Market Size, Share, Trends: BASF SE Leads

Rising Demand: Bio-Based and Pharmaceutical Applications Drive Growth

Market Overview:

The global Carboxylic Acids market is projected to grow at a CAGR of XX% from 2024 to 2031. Asia-Pacific currently dominates the market, accounting for the largest share of global revenue. Key metrics include the growing demand from end-use industries such as food & beverages, pharmaceuticals, and personal care, increasing applications in industrial processes, and rising investments in bio-based carboxylic acids.

The market is steadily expanding due to rising population and urbanisation, increasing demand for processed foods and drinks, growing awareness of personal hygiene and cosmetics, and the expanding pharmaceutical industry. The market is also benefiting from the shift to sustainable and bio-based chemicals in various industrial applications.

DOWNLOAD FREE SAMPLE

Market Trends:

The trend towards bio-based and sustainable chemicals is having a significant impact on the carboxylic acid market. Bio-based carboxylic acids, derived from renewable resources such as corn, sugarcane, and other biomass, are gaining popularity due to their minimal environmental impact and reduced reliance on petrochemical feedstock. Major chemical corporations like BASF and Cargill have made significant investments in bio-based carboxylic acid production plants. The market for bio-based carboxylic acids is predicted to grow at a 7.2% CAGR between 2024 and 2031, outpacing the growth of traditional petrochemical-based acids.

Market Segmentation:

The Acetic Acid segment dominates the Carboxylic Acids market, driven by its versatile applications across multiple industries. This sector has emerged as the leading force in the Carboxylic Acids industry, with the highest market share due to acetic acid's wide range of applications in chemicals, food and beverages, and pharmaceuticals.

According to our analysis, the global acetic acid market reached $YY billion in 2023 and is expected to rise at a CAGR of 4.7% between 2024 and 2031. This expansion is driven by rising demand for vinyl acetate monomer (VAM), an important acetic acid derivative used in adhesives, paints, and coatings. The food and beverage industry has also been a major driver of acetic acid usage, with its use as a food preservative, flavouring ingredient, and acid. Acetic acid's versatility in chemical synthesis has further contributed to its market dominance.

Market Key Players:

BASF SE

Eastman Chemical Company

Perstorp Group

Celanese Corporation

Dow Chemical Company

Alfa Aesar (Thermo Fisher Scientific)

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

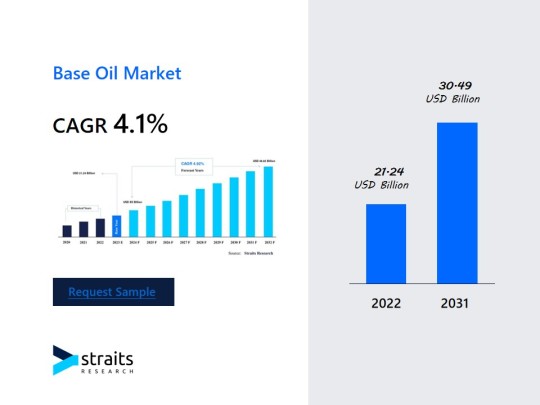

Base Oil Market Key Insights: Global Trends and Growth Forecasts by 2031

The global base oil market was valued at USD 21.24 billion in 2022. It is projected to grow from USD 22.76 billion in 2023 to USD 48.82 billion by 2031, registering a compound annual growth rate (CAGR) of 4.92% during the forecast period (2023–2031).

Overview of the Base Oil Market

The global base oil market is on a robust growth trajectory, driven by increasing demand for high-performance lubricants across various industries. Base oils, the primary ingredients in lubricants, play a crucial role in the formulation of oils used for automotive, industrial, and metalworking applications. As industrial activity ramps up worldwide and the automotive sector continues its evolution, base oils are expected to experience heightened demand in the coming years.

In 2022, the base oil market was valued at USD 21.24 billion and is forecasted to expand to USD 48.82 billion by 2031, growing at a CAGR of 4.92%. This growth is attributed to the increasing industrialization in emerging markets, rising demand for advanced lubricants, and a greater focus on energy-efficient solutions.

Market Definition

Base oils are refined from crude oil and used as the foundation for creating lubricants, oils, and other products, such as hydraulic fluids, metalworking fluids, and automotive oils. The classification of base oils is determined by their performance properties, with each type offering specific benefits based on application requirements. As key raw materials for a range of applications, base oils are essential to maintaining the smooth operation of machinery and vehicles.

Get a Full PDF Sample Copy of the Report @ https://straitsresearch.com/report/base-oil-market/request-sample

Market Dynamics: Key Trends, Drivers, and Opportunities

Key Trends:

Growing Adoption of Synthetic and High-Performance Oils: There is an increasing shift toward synthetic and high-performance base oils, particularly Group III and Group IV oils, which offer better oxidation stability, improved low-temperature performance, and longer-lasting protection for engines and industrial machinery. This trend is expected to accelerate as consumers and industries alike seek more efficient and durable oils.

Integration of Green and Sustainable Technologies: As environmental concerns continue to rise, there is a growing emphasis on the development of eco-friendly and sustainable base oils. The industry is witnessing innovations in bio-based oils and processes that use renewable feedstocks, reducing the overall carbon footprint of oil production and usage. This shift aligns with global sustainability goals and is likely to enhance market prospects.

Key Market Drivers:

Industrial Growth and Expansion in Emerging Markets: The expansion of industrial activities in emerging markets, particularly in Asia-Pacific, is one of the primary drivers for the base oil market. Rapid infrastructure development, increased manufacturing capacity, and growing demand for automotive lubricants are propelling the need for high-quality base oils. As industrial production ramps up, base oils will continue to be in high demand for applications ranging from hydraulic oils to industrial lubricants.

Technological Advancements in Lubricants and Oils: Advancements in lubricant technology, especially the demand for more energy-efficient and high-performance oils in automotive and industrial applications, are significantly driving the base oil market. Group II and Group III base oils, known for their superior properties, are gaining popularity due to their enhanced performance in high-temperature environments and longer service life.

Key Market Opportunities:

Expanding Automotive Sector and Electric Vehicle Production: As the automotive sector continues to grow, especially in emerging economies, the demand for lubricants is increasing. Additionally, the rise of electric vehicles (EVs) presents a unique opportunity for the base oil market. Even though electric vehicles require fewer oils and lubricants, the growing market for hybrid and electric vehicles will necessitate a shift toward specialized lubricants, creating new opportunities for base oil manufacturers.

Rising Demand for Metalworking Fluids and Hydraulic Oils: Base oils used in metalworking fluids, industrial oils, and hydraulic fluids represent a significant opportunity for market growth. As industries such as construction, mining, and manufacturing expand, the demand for high-performance industrial oils and lubricants is rising, offering strong growth prospects for the base oil market.

Market Segmentation

The base oil market is segmented based on type, application, and end-user industry. This segmentation helps understand the market's diverse needs and the opportunities available across various sectors.

By Type:

Group I

Group II

Group III

Group IV

Group V

By Application:

Hydraulic Oil

Automotive Fluid

Metalworking Fluids

Industrial Oil

Other

By End-User:

Industry

Construction

Automobile

Agriculture

Marine

Other

For more detailed segmentation and insights, visit: https://straitsresearch.com/report/base-oil-market/segmentation

Key Players in the Base Oil Market

The base oil market is highly competitive, with several global players leading the way in product innovation, capacity expansion, and market consolidation. The key players in the market include:

Royal Dutch Shell PLC

Exxon Mobil Corporation

H&R Ölwerke Schindler GmbH

Chevron Corporation

BP plc

Saudi Arabian Oil Co.

Petronas Pvt. Ltd.

Evonik Industries AG

Ergon Inc.

Nynas AB

Total S.A.

SK Lubricants Co. Ltd

S-Oil Corporation

Sinopec Group

Repsol S.A.

PetroChina Company Limited

Neste Oil

MOGoil GmbH

Lotos Oil SP. Z O.O.

GS Caltex Corporation

Calumet Specialty Products Partners Lp

Avista Oil AG

These companies are focusing on expanding their production capabilities, enhancing product quality, and exploring new geographic markets to tap into the growing demand for high-performance base oils.

Regional Analysis

Dominated Region: The Asia-Pacific region is the largest market for base oils, driven by the rapid industrialization in countries like China, India, and Japan. The region's booming automotive and manufacturing sectors, along with increasing infrastructure projects, are fueling the demand for base oils in various applications, such as automotive lubricants, industrial oils, and hydraulic fluids.

Fastest Growing Region: North America is expected to be the fastest-growing region for the base oil market. The U.S. and Canada are focusing on sustainable technologies and improving automotive and industrial production. Additionally, the rising demand for high-performance lubricants and oils is driving market growth in this region.

Conclusion

The base oil market is poised for significant growth, driven by industrial expansion, technological advancements, and the increasing need for high-performance lubricants. With a projected CAGR of 4.92%, the market is set to reach USD 48.82 billion by 2031. As demand grows across various industries, particularly in emerging markets, base oil manufacturers are well-positioned to capitalize on the opportunities in the automotive, industrial, and metalworking sectors.

For more information or to customize the report before purchasing, visit: https://straitsresearch.com/buy-now/base-oil-market

About Us:

StraitsResearch.com is a leading market research and market intelligence organization, specializing in research, analytics, and advisory services along with providing business insights & market research reports.

Contact Us:

Email: [email protected] Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.) Website: https://straitsresearch.com/

0 notes

Text

Emerging Trends in the 3D Printing Plastics Market You Need to Know

The global 3D printing plastics market was valued at USD 1.26 billion in 2022. It is projected to grow from USD 1.55 billion in 2023 to USD 7.46 billion by 2030, exhibiting a CAGR of 25.1% during the forecast period.

3D printing technology builds three-dimensional objects by layering material in a digital design or model. The 3D-printed plastic model is digitally divided into horizontal layers using specialized software, creating sets of instructions for the 3D printer. The versatility of 3D-printed plastics increases its use in various applications, such as automotive, consumer products, and healthcare, driving the growth.

Fortune Business Insights™ mentioned this in a report titled, “3D Printing Plastics Market, 2023-2030.”

Get Free Sample Report- https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/3d-printing-plastics-market-108834

Competitive Landscape

Strong Regional Presence of Key Players to Propel Market Growth

The leading market players’ strong geographical presence, product offerings, and distribution channels boosts the market growth. The engagement of the key market players in research and development to provide enhanced features and produce superior quality to drive market expansion.

Key Industry Development

October 2023 – Evonik launched a new grade of 12 Polyamide powders to unbound 3D printing on the bio circular raw materials. The launch is the first Polyamide power material produced for industrial uses that replaces 100 percent of fossil feedstock with bio-circular material.

List of Key Players Present in the Report:

HP Development Company, L.P (U.S.)

Evonik Industries AG. (Germany)

Stratasys (U.S.)

3D Systems, Inc. (U.S.)

Arkema S.A. (France)

Henkel Corporation (Germany)

EOS GmbH Electro Optical Systems (Germany)

Solvay S.A.(Belgium)

Huntsman Corporation (U.S.)

SABIC (Saudi Arabia)

3D Printing Plastics Market Segments

Polylactic Acid Segment to Lead Owing to its Unique Qualities

By type, the market is divided into Polylactic Acid, ABS, Polyamide, Polycarbonate, and others. The Polylactic Acid segment held the largest 3D printing plastics market share in 2022 and is also the fastest-growing segment in the market. The growth is attributed to the use of Polylactic Acid in different applications owing to its unique properties.

Growing Adoption and Utilization of 3D Printing Technologies to Aid Aerospace & Defense Segment Growth

Based on end-use industry, the market is segmented into automotive, aerospace & defense, healthcare, electronics & electrical, consumer goods, and others. The aerospace & defense segment held the largest market share. The growth is attributed to the growing adoption and utilization of 3D printing technologies, especially with different plastic types, owing to customization, precision, and weight-saving capabilities.

Report Coverage

The report offers:

Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

Comprehensive insights into regional developments.

List of major industry players.

Key strategies adopted by the market players.

The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Rising Technological Innovations in 3D Printing to Boost Market Growth

The increasing technological innovations in 3D printing, printer capabilities, and materials boost the 3D printing plastics market growth. The advancements in multi-material capabilities, speed, and precision are expanding the 3D printing applications with plastics.

However, meeting the safety and quality standards of the healthcare and aerospace industries and obtaining certifications for 3D-printed parts can be challenging and may impede market growth.

Get More Info- https://www.fortunebusinessinsights.com/3d-printing-plastics-market-108834

Regional Insights

Rising Demand for Commercial Aerospace Products to Drive Market Growth in North America

North America held the largest 3D printing plastics market share and accounted for USD 0.51 billion in 2022. The growth was attributed to the demand for commercial aerospace products, including passenger aircraft, in the region.

Asia Pacific accounted for a significant market share. The growth is attributed to the fast-growing manufacturing industries, including automotive and consumer goods in the region.

0 notes

Text

#Bio Feedstocks Market#Bio Feedstocks Market Size#Bio Feedstocks Market Trends.#Bio Feedstocks Market Growth#Bio Feedstocks Market Analysis 2023

0 notes

Text

Aromatic Solvents Market

Aromatic Solvents Market Size, Share, Trends: ExxonMobil Corporation Leads

Increasing Demand for High-Performance Solvents Driving Market Growth

Market Overview:

The global aromatic solvents market is expected to grow at a CAGR of X.X% during the forecast period of 2024-2031, reaching a market size of USD YY billion by 2031 from USD XX billion in 2024. The Asia-Pacific region is projected to dominate the market, driven by the rapid industrialization, growing demand from end-use industries, and increasing investments in infrastructure development. The growth of the aromatic solvents market is fueled by factors such as the rising demand for high-performance solvents in various applications, increasing adoption of environmentally friendly solvents, and growing focus on product innovation. However, stringent regulations regarding the use of certain aromatic solvents may restrain the market growth to some extent.

The increased demand for high-performance solvents in a variety of applications, including paints and coatings, adhesives, and printing inks, is a major trend driving the aromatic solvents market. Aromatic solvents, particularly xylene and toluene, have high solvency, rapid evaporation rates, and are compatible with a wide range of resins and polymers. These characteristics make them excellent for use in high-performance compositions that demand exceptional quality and endurance. The growing need for high-quality paints, coatings, and adhesives in the automotive, construction, and packaging industries is likely to drive up consumption of aromatic solvents in the coming years.

DOWNLOAD FREE SAMPLE

Market Trends:

The rising use of ecologically friendly solvents is a major driver of the aromatic solvents industry. Growing worries about the environmental and health consequences of traditional solvents have prompted the development of cleaner, more sustainable alternatives. Bio-based and low-VOC (volatile organic compound) aromatic solvents are gaining popularity due to their lower environmental impact and adherence to strict requirements. Major market participants are investing in the development of green solvents, such as those generated from renewable feedstocks, to address the growing need for environmentally friendly solutions.

Despite the favourable prognosis, tight rules governing the use of some aromatic solvents may stifle market growth. Some aromatic solvents, such as benzene, have been classified as carcinogenic and are subject to stringent laws in several countries. The European Union, for example, has enacted the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) legislation, which limits the use of some hazardous compounds, such as certain aromatic solvents. Compliance with these laws may raise production costs and reduce the availability of some aromatic solvents, hurting market growth. However, the development of safer and more compliant alternatives is projected to reduce the impact of regulatory challenges to some degree.

Market Segmentation:

The toluene segment is estimated to account for the majority of the aromatic solvents market throughout the forecast period. Toluene is widely utilised as a solvent in a variety of applications, including paints & coatings, adhesives, printing inks, and pharmaceuticals, due to its high solvency, rapid evaporation rate, and low toxicity when compared to other aromatic solvents. This segment's expansion is being driven by rising demand for toluene in the manufacture of high-performance coatings, adhesives, and inks, particularly in the automotive and construction industries.

Major aromatic solvent producers, like ExxonMobil Corporation and Royal Dutch Shell plc, are focussing on increasing toluene production capacity to meet rising demand from end-use industries. For example, in 2023, ExxonMobil announced intentions to enhance toluene production capacity at its Singapore refinery in response to rising demand in Asia-Pacific.

Market Key Players:

ExxonMobil Corporation

Royal Dutch Shell plc

BASF SE

Lyondellbasell Industries Holdings B.V.

Chevron Phillips Chemical Company LLC

Ineos Group AG

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Ethylbenzene Market Progress: Exploring Digital Transformation and Circular Economy Initiatives in 2024

The global ethylbenzene market is undergoing a significant transformation, driven by evolving consumer preferences, technological advancements, and regulatory changes. As a key intermediate in the production of styrene, which is a building block for numerous plastics and resins, ethylbenzene plays a vital role in the modern industrial economy. Here, we delve into the emerging trends that are shaping the future of this dynamic market.

Growing Demand for Styrene-Based Products-

Ethylbenzene’s primary use lies in the production of styrene monomer, which is integral to manufacturing polystyrene and acrylonitrile butadiene styrene (ABS). These materials find extensive applications in packaging, automotive components, electronics, and construction. With rapid industrialization in developing countries, the demand for styrene-based products is expected to see sustained growth. This, in turn, propels the ethylbenzene market forward.

Technological Advancements in Production Processes

The production of ethylbenzene has seen a marked improvement with the advent of innovative technologies. Catalytic processes are becoming more efficient, reducing operational costs and environmental impact. Companies are also exploring bio-based feedstocks as sustainable alternatives to conventional petroleum-based processes, addressing the growing demand for green chemistry in the industry.

Regulatory Impact on the Market

Stringent environmental regulations have a dual impact on the ethylbenzene market. On one hand, they drive innovation as manufacturers seek compliance through eco-friendly practices. On the other, they present challenges by increasing operational costs. For instance, regulations related to volatile organic compounds (VOCs) and emissions require manufacturers to adopt advanced mitigation technologies, adding to their capital expenditure.

Regional Market Dynamics-

The ethylbenzene market exhibits significant regional disparities. Asia-Pacific remains the dominant region, driven by China and India’s expanding manufacturing and construction sectors. Meanwhile, North America and Europe are focusing on sustainability and advanced materials, creating opportunities for high-performance styrene derivatives. Emerging markets in Latin America and Africa are also showing promise, with growing industrial activities and investment in infrastructure.

Sustainability and Circular Economy Initiatives-

Sustainability has emerged as a pivotal trend in the ethylbenzene market. Companies are investing in recycling technologies to recover styrene from post-consumer waste, reducing the reliance on virgin ethylbenzene. Such circular economy initiatives not only align with global environmental goals but also offer cost advantages in the long term.

Challenges in Raw Material Supply-

The availability and cost of raw materials, particularly benzene and ethylene, are critical factors influencing ethylbenzene production. Geopolitical tensions, trade restrictions, and fluctuating crude oil prices contribute to market volatility. Companies are increasingly diversifying their supply chains and exploring alternative sources to mitigate these risks.

Increasing Focus on R&D and Innovation-

Research and development (R&D) efforts are driving the discovery of novel applications and improved production methods for ethylbenzene. From advanced catalysts to process optimization, these innovations promise to enhance efficiency and broaden the application scope of ethylbenzene and its derivatives.

Competitive Landscape and Strategic Collaborations-

The ethylbenzene market is characterized by intense competition, with major players focusing on mergers, acquisitions, and partnerships to strengthen their market presence. Collaborations between petrochemical giants and research institutions are fostering innovation and expanding market opportunities.

Digital Transformation in Operations-

Digital tools, including artificial intelligence (AI) and big data analytics, are being leveraged to optimize production processes and supply chain management. Real-time monitoring and predictive maintenance are enabling manufacturers to reduce downtime and improve overall operational efficiency.

Future Outlook-

The future of the ethylbenzene market appears promising, with robust demand across various end-use industries and a strong focus on sustainability and technological innovation. While challenges persist, such as regulatory pressures and raw material volatility, the industry’s adaptability and commitment to progress ensure its continued growth.

0 notes

Text

Exploring the Methanol Market: Growth, Trends, and Opportunities

The methanol market has gained immense prominence across various industries due to its versatile applications, ranging from fuel production to the manufacturing of chemicals. According to the comprehensive research by SkyQuest Technology, the global methanol market is projected to reach a market size of USD 46.29 billion by 2030, expanding at a CAGR of 5.37% from 2023 to 2030. This robust growth trajectory is driven by rising demand across multiple end-use industries, coupled with an increased emphasis on sustainable and eco-friendly solutions.

Key Drivers of Methanol Market Growth

The methanol market’s expansion is fueled by a variety of factors:

Rising Demand for Alternative Fuels Methanol’s potential as a clean and efficient alternative to conventional fuels has led to its adoption in transportation and energy applications. As governments worldwide push for reduced carbon footprints, methanol-blended fuels are being recognized for their environmental benefits.

Growth in Petrochemical and Construction Industries Methanol serves as a feedstock for manufacturing essential chemicals such as formaldehyde, acetic acid, and olefins. Its use in producing resins, adhesives, and plastics is essential for the construction and automotive industries, further boosting its demand.

Sustainability Initiatives The global shift toward renewable energy and bio-based chemicals is propelling methanol’s usage in biofuels and green methanol production. This trend aligns with global sustainability goals, positioning methanol as a key player in the green economy.

Request a Sample Report - https://www.skyquestt.com/sample-request/methanol-market

Market Segmentation: Insights by Application and Source

The methanol market is segmented into various categories based on its application and source of production.

By Application

Fuel: Methanol’s use as a fuel or fuel additive is rapidly expanding, particularly in automotive and marine sectors.

Chemicals: As a primary feedstock for the production of formaldehyde, acetic acid, and olefins, this segment dominates the methanol market.

Others: Applications in pharmaceuticals, paints, and adhesives add to the growing demand for methanol.

By Source

Natural Gas-Based Methanol: The most common production method due to the abundant availability of natural gas.

Bio-Methanol: Gaining traction as an eco-friendly alternative, produced from renewable resources like biomass and waste.

Speak to an Analyst for Customization - https://www.skyquestt.com/speak-with-analyst/methanol-market

Regional Insights: Methanol Demand Across the Globe

The global methanol market is shaped by diverse regional trends and growth patterns:

Asia-Pacific (APAC): As the largest and fastest-growing market, APAC accounts for a significant share of global methanol consumption. Countries like China, India, and Japan lead the demand due to their expanding chemical, construction, and automotive industries.

North America: The region benefits from an abundance of natural gas, which is a key raw material for methanol production. The United States and Canada are significant contributors to the regional growth.

Europe: Stricter environmental regulations and sustainability initiatives are driving methanol adoption in biofuels and green chemicals across countries like Germany, the UK, and France.

Latin America & Middle East: These regions are witnessing growth due to increased industrialization and investments in methanol-based applications.

Industry Leaders: Top Companies in the Methanol Market

The global methanol market is highly competitive, with leading companies driving innovation and market expansion. Key players include:

Methanex Corporation

Celanese Corporation

BASF SE

SABIC

Mitsubishi Gas Chemical Company, Inc.

LyondellBasell Industries Holdings B.V.

Zagros Petrochemical Company

Yanzhou Coal Mining Company Limited

China XLX Fertilizer Ltd.

Proman AG

These companies are investing in technological advancements and sustainable production methods to strengthen their foothold in the global market.

Make a Purchase Inquiry - https://www.skyquestt.com/buy-now/methanol-market

Emerging Trends in the Methanol Market

Development of Green Methanol Innovations in green methanol production using renewable resources are set to transform the industry. Green methanol is gaining popularity as an alternative fuel with lower carbon emissions.

Expansion of Methanol-to-Olefins (MTO) Technology The advancement of MTO technology, which converts methanol into high-value olefins like ethylene and propylene, is driving growth in the petrochemical sector.

Increased Investments in Bio-Methanol Bio-methanol production is receiving significant investment as companies strive to meet global sustainability goals and address environmental concerns.

Growing Marine Fuel Applications With the International Maritime Organization (IMO) enforcing stringent emissions regulations, methanol is gaining traction as a cleaner and cost-effective marine fuel.

The Methanol Market’s Promising Future

As industries pivot towards sustainability and cleaner energy alternatives, the methanol market is poised for substantial growth. Emerging applications in biofuels, green chemicals, and advanced manufacturing processes will continue to redefine the market landscape.With regions like Asia-Pacific leading the charge and companies investing heavily in innovation, the methanol market presents abundant opportunities for growth and expansion in the coming years.

#Methanol Market#Methanol Market Size#Methanol Market Share#Methanol Market Trends#Methanol Market Growth#Methanol Market Outlook#Methanol Market Key Players#Methanol Market Overview#Methanol Market Competitor#Methanol Market Insights#Methanol Market Forecast#Methanol Market Analysis#Methanol Market Statistics#Methanol Market Data#Methanol Market PDF#Methanol Market Excel#Methanol Market Strategy#Methanol Market Innovations

0 notes

Text

Polyethylene Terephthalate (PET) Prices: Trends, Drivers, and Forecast

Polyethylene Terephthalate (PET), a widely used thermoplastic polymer, plays a critical role in industries such as packaging, textiles, and consumer goods. Its popularity stems from its lightweight, durability, and excellent recyclability. However, the price of PET is influenced by various factors, making it a dynamic and closely monitored market.

Current Price Trends

In recent years, PET prices have demonstrated significant volatility due to shifting supply and demand dynamics. The post-pandemic recovery spurred a surge in demand for packaging materials, especially for beverages and personal care products, driving PET prices upward. However, the market has also faced challenges such as fluctuating crude oil prices, disruptions in raw material supply chains, and regional trade policies.

Get Real time Prices for Polyethylene Terephthalate (PET) : https://www.chemanalyst.com/Pricing-data/polyethylene-terephthalate-72

Key Price Drivers

Raw Material Costs: PET is derived from purified terephthalic acid (PTA) and monoethylene glycol (MEG), both of which are petrochemical derivatives. Fluctuations in crude oil prices directly impact the costs of these raw materials, subsequently influencing PET prices.

Supply Chain Dynamics: Disruptions in global supply chains, such as port congestion and transportation bottlenecks, have affected the availability of PET and its feedstocks. This has occasionally led to short-term price spikes.

Demand Growth: The packaging sector, especially for beverages and food products, continues to be the largest consumer of PET. The rise in e-commerce and takeaway culture has further boosted demand, supporting price increases.

Recycling Initiatives: With increasing emphasis on sustainability, the demand for recycled PET (rPET) has grown. This has created a dual market for virgin and recycled PET, with prices for rPET often being higher due to processing costs and limited supply.

Regulatory Environment: Policies promoting circular economies and reducing plastic waste have impacted the PET market. Regulations favoring biodegradable or recyclable materials may influence the production and pricing strategies of PET manufacturers.

Future Outlook

The PET market is expected to experience steady growth over the next five years, driven by increasing urbanization, changing consumer lifestyles, and the expansion of industries like food and beverage packaging. Analysts predict that PET prices will remain sensitive to crude oil trends and geopolitical factors affecting raw material availability.

Investments in recycling technologies and infrastructure are likely to play a pivotal role in shaping the PET market. The production of rPET is expected to rise, potentially narrowing the price gap between recycled and virgin PET. However, achieving scalability in recycling processes remains a challenge.

Additionally, advancements in bio-based PET alternatives could provide a sustainable option, potentially influencing long-term price dynamics. While still in nascent stages, such innovations may mitigate the environmental concerns associated with traditional PET.

In conclusion, the PET market is poised for growth but will remain susceptible to external pressures. Stakeholders should monitor raw material costs, regulatory changes, and sustainability trends to navigate this dynamic landscape effectively.

Get Real time Prices for Polyethylene Terephthalate (PET) : https://www.chemanalyst.com/Pricing-data/polyethylene-terephthalate-72

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Polyethylene Terephthalate#Polyethylene Terephthalate Price#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

How the Middle East Crisis is Reshaping the Global Resin Market

Geopolitical Crisis and Oil Distribution

In October 2024, heightened tensions between Iran and Israel escalated into missile attacks and counteroffensives, sparking concerns over oil supply disruptions. Though direct impacts on oil production were minimal, crude oil prices surged over 8%, influencing resin production costs.

Red Sea Shipping Bottlenecks

The Red Sea, a critical trade route, has experienced military activity that has delayed shipments and increased transportation costs. This has restricted resin exports from the Middle East, leading to supply shortages in major markets.

Production Disruptions

Several petrochemical facilities in the region halted operations for planned maintenance, compounding supply constraints. The resulting shortages have pushed resin prices higher, amplifying global market instability.

Impact on Resin Prices

The resin market has faced volatility in 2024, with geopolitical tensions driving price surges. Key impacts include:

Oil Price Volatility:

Following the October crisis, Brent crude oil prices spiked by 7%, leading to a 5% increase in PE and PP prices.

Logistical Challenges:

Shipping delays in the Persian Gulf have caused a 3% rise in resin prices due to increased transportation costs.

Market Speculation:

Investor sentiment and speculative trading further fueled a 2% increase in resin prices, reflecting broader market uncertainties.

Resin Price Trends

Polyethylene (PE)

Price Growth: LLDPE prices in Asia rose from $1,171/MT in January 2024 to $1,182/MT by March, while European prices saw a 13% increase.

Demand and Supply: High demand, coupled with constrained supplies from the Middle East, continues to push prices upward.

Polypropylene (PP)

Rising Costs: PP prices in North America rose 3.6% in two months, while European prices climbed from EUR 1,313/MT to EUR 1,362/MT.

Market Dynamics: Middle Eastern supply shortages and increased domestic demand in India drove prices up by 6% month-over-month in early 2024.

Polyethylene Terephthalate (PET)

Global Fluctuations: PET prices surged 2.5% within three weeks of January 2024, driven by rising production costs and disrupted logistics.

Regional Pressures: European PET prices rose by 6%, fueled by demand from the beverage and packaging industries.

Long-Term Implications

The ongoing geopolitical instability is reshaping the resin market, with several potential long-term outcomes:

Strategic Reserves: Companies may increase reserves of petrochemical feedstocks, potentially driving short-term price spikes.

Supply Chain Diversification: Manufacturers could reduce reliance on Middle Eastern supplies by sourcing feedstocks from other regions or adopting alternatives like bio-based resins.

Technological Innovations: Advances in recycling and bio-resin technologies could mitigate dependence on volatile petrochemical markets.

Conclusion

The Middle East crisis has exposed the resin market's vulnerability to geopolitical instability. Rising oil prices, logistical challenges, and production disruptions have collectively created an environment of heightened costs and uncertainty. Businesses reliant on resins must adopt agile strategies, including diversifying supply chains and exploring sustainable alternatives, to navigate these turbulent times.

At SpendEdge, we specialize in helping companies mitigate supply chain risks and optimize procurement strategies. Our insights and data-driven solutions enable businesses to thrive in dynamic markets. Reach out to us to learn how we can assist your organization in overcoming challenges in the resin market and beyond.

For more information please contact

0 notes