#Automotive Sensor and Camera Technologies Market trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Forty percent of Tumblr users are between the ages of 18 to 25.

Text

Smart Mirrors Market Size, Share & Report Trends 2025

Meticulous Research®—a leading global market research company, published a research report titled, ‘Smart Mirrors Market by Offering (Hardware, Software, Services), Installation Type (Wall Mounted, Free-Styled), Application (Automotive, Healthcare, Residential, Retail, Media & Entertainment, Corporate) and Geography - Global Forecast to 2032.’

The global smart mirrors market is projected to reach $8.85 billion by 2032, at a CAGR of 16.4% from 2025 to 2032. The growth of this market is attributed to smart mirrors being an alternative to convex mirrors for enhanced safety features in the automobile sector, the rising need for home security, and the shift of the retail industry from traditional to digital. However, security breach of confidential and personal data restrains market growth. The growing Industry 4.0 adoption to offer lucrative opportunities and untapped potential in the Asia-Pacific region is expected to create significant opportunities for this market. However, a lack of awareness about smart mirrors and higher cost than ordinary mirrors pose challenges to market growth.

The global smart mirrors market is segmented by offering, installation type, application, and geography. The study also evaluates industry competitors and analyses the regional and country-level markets.

Key Players

The key players profiled in the global smart mirrors market study include Japan Display Inc. (Japan), Gentex Corporation (U.S.), Magna International Inc. (Canada), Harman International Industries, Incorporated (U.S.), Murakami Corporation (Japan), Ficosa Internacional SA (Spain), Mirrocool, Inc. (U.S.), Electric Mirror, Inc. (U.S.), ad notam AG (Germany), Dirror (Germany), Seymour Powell Limited (U.K.), Alke (Italy), HILO Solutions, Inc. (Canada), Evervue USA Inc. (U.S.) and Séura (U.S.).

Based on offering, the global smart mirrors market is segmented into hardware, software, and services. In 2025, the hardware segment is expected to account for the largest share of the global smart mirrors market. The hardware segment includes displays, cameras, and sensors, along with connectivity and audio components, which form a major share of the cost of the complete smart mirror system. The smart mirror offers a platform for shoppers to try on new clothes, check the sizes or varieties of clothes in a store, and share information related to the tried clothes on social media platforms. Smart rear-view mirrors are being increasingly utilized to enhance safety in cars and reduce complications of camera systems. Smart rear-view mirrors for automotive applications can work normally even in the event of poor weather conditions with minimum obstructions to drivers. Unlike conventional mirrors, electric mirrors utilized in vehicles have the features of auto-adjusting their displays under different light intensities and thus provide better assistance to drivers under all weather conditions. These features make mirror technology irreplaceable. As automotive and retail continue to grow, this will create lucrative opportunities for smart mirror hardware in the coming years.

Based on installation type, the global smart mirrors market is segmented into wall-mounted and free-styled. In 2025, the wall-mounted segment is expected to account for the larger share of the global smart mirrors market. The growing consumer preference for wall-mounted smart mirrors over free-standing mirrors is influencing the growth of the segment. Free-standing mirrors are more likely to fall or topple over, whereas wall-mounted mirrors are significantly less likely to do so. Furthermore, as smart mirrors are more expensive than regular mirrors, buyers are more cautious about choosing wall-mounted smart mirrors. These are installed on the wall, saving space by freeing up the floor area and improving the overall appearance of a room. Such mirrors are space-saving alternatives, thereby, demand for wall-mounted smart mirrors is gaining traction.

Based on application, the global smart mirrors market is segmented into automotive, healthcare, residential, hospitality, retail, media & entertainment, corporate, and other applications. In 2025, the retail segment is expected to account for the largest share of the smart mirrors market. The large share of the segment is attributed to their ability to enhance customer experiences, improve engagement, and provide valuable data for businesses. These devices offer various functionalities that cater to different industries, transforming the way businesses interact with customers. In the retail sector, smart mirrors are used in stores to create interactive and immersive shopping experiences, enabling customers to virtually try on clothing, accessories, and makeup. This technology enhances customer convenience, reduces return rates, and boosts sales. Thereby, the potential growth of the retail sector is likely to create lucrative opportunities for the segment in the coming years.

Based on geography, the global smart mirrors market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2025, North America is expected to account for the largest share of the smart mirrors market. The large share of this market is attributed to the customers' awareness of AI developments and its application in smart mirrors. As of present, integrating smart speakers such as Alexa into these mirrors increases their popularity at residencies across North America. Moreover, growing investments, strategic developments, and increasing new entrants in the market space are driving the market growth. As technology advances, smart mirrors are likely to offer even more novel capabilities and become more widespread in people's daily lives.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5747?

Key Questions Answered in the Report:

Which are the high-growth market segments in terms of offering, installation type, application, and geography?

What is the historical market size for smart mirrors across the globe?

What are the market forecasts and estimates for the period 2025–2032?

What are the major drivers, opportunities, and challenges in the global smart mirrors market?

Who are the major players in the market, and what are their market shares?

What is the competitive landscape like for the global smart mirrors market?

What are the recent developments in the global smart mirrors market?

What are the different strategies adopted by the major players in the market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the global smart mirrors market, and how do they compete with other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Smart Mirrors Market#Digital Mirrors#Interative Mirrors#Mirror Hardware#Wall Mounted Mirrors#Smart Mirror Sensors#Mirror Display

1 note

·

View note

Text

Vision Sensor Market Size Accelerating Automation with Intelligent Visual Inspection

The Vision Sensor Market Size is witnessing substantial growth driven by the increasing demand for automation, quality assurance, and precision manufacturing. Vision sensors—integrated systems that combine image capture, processing, and decision-making—are transforming industries by enabling real-time visual inspection and object detection. According to Market Size Research Future, the global Market Size is projected to reach USD 5.8 billion by 2030, growing at a CAGR of 10.2% during the forecast period.

Market Size Overview

Vision sensors are essential in automating manufacturing lines, detecting defects, guiding robotic arms, and ensuring consistent product quality. These sensors outperform traditional photoelectric sensors by analyzing multiple parameters like shape, size, orientation, and texture.

With Industry 4.0 gaining momentum, the need for intelligent inspection systems that can work at high speeds with minimal error has grown dramatically. Vision sensors are now a core component in packaging, automotive, electronics, pharmaceuticals, and logistics industries.

Market Size Segmentation

By Type:

1D Vision Sensor

2D Vision Sensor

3D Vision Sensor

By Application:

Inspection

Measurement

Code Reading

Object Detection

Sorting and Counting

By End-Use Industry:

Automotive

Consumer Electronics

Food & Packaging

Pharmaceutical

Logistics & Warehousing

Semiconductor

Others (Textile, Paper, Glass)

By Component:

Camera

Sensor

Processor

Communication Interface

Software

By Region:

North America

Europe

Asia-Pacific

Rest of the World

Key Market Size Trends

1. Rise of Smart Manufacturing

Vision sensors are central to smart factories, where they perform tasks like real-time defect detection, barcode reading, and robot guidance, reducing reliance on manual labor and enhancing production efficiency.

2. Growth in 3D Vision Technology

3D vision sensors are gaining popularity for complex applications such as volume estimation, bin picking, and precise robotic navigation, especially in automotive and warehouse automation.

3. Integration with AI and Deep Learning

Modern vision sensors utilize artificial intelligence to improve pattern recognition and reduce false positives, enabling adaptive inspection systems that learn over time.

4. Miniaturization and Cost Optimization

Compact, affordable vision sensors are making high-precision inspection feasible for small and medium-sized enterprises (SMEs), expanding Market Size reach across all industry tiers.

Segment Insights

2D Vision Sensors Dominate

2D sensors are widely used due to their cost-effectiveness and ability to handle basic inspection tasks like label verification, presence detection, and part orientation.

Object Detection and Code Reading are Key Applications

Automated barcode reading and object detection are fundamental in packaging, logistics, and retail industries where speed and accuracy are essential.

Automotive Industry Leads Adoption

In automotive manufacturing, vision sensors check welding seams, surface finishes, and component placements—ensuring safety-critical components meet strict standards.

End-User Insights

Automotive:

Vision sensors are vital in ensuring component alignment, surface inspection, and robotic guidance in the assembly line, minimizing defects and warranty claims.

Consumer Electronics:

Microscopic component placement, solder inspection, and screen defect detection are common tasks handled by vision sensors in electronics production.

Food & Packaging:

Vision sensors check for proper labeling, seal integrity, and product positioning on packaging lines, ensuring regulatory compliance and reducing recalls.

Pharmaceuticals:

In pharma manufacturing, vision sensors verify dosage forms, blister packaging integrity, and imprint verification—supporting quality control and patient safety.

Logistics & Warehousing:

Used for sorting, scanning, and tracking parcels, vision sensors streamline operations in e-commerce and distribution centers, reducing manual errors.

Key Players in the Vision Sensor Market Size

Leading players are focusing on expanding their product range with features like edge processing, AI integration, and multi-dimensional imaging. Major contributors include:

Cognex Corporation

SICK AG

Omron Corporation

Keyence Corporation

Balluff GmbH

Banner Engineering Corp.

Pepperl+Fuchs

Teledyne Technologies Incorporated

Datalogic S.p.A.

ifm electronic GmbH

These companies are also investing in easy-to-configure vision solutions for SMEs, ensuring a scalable and flexible Market Size footprint.

Conclusion

The vision sensor Market Size is a vital pillar of the automation revolution. From ensuring defect-free products to enabling intelligent logistics, vision sensors are indispensable for modern industry. With ongoing advancements in AI, 3D imaging, and IoT integration, the vision sensor ecosystem is set to deliver smarter, faster, and more precise automation solutions across sectors.

Trending Report Highlights

Explore other technology-driven Market Sizes transforming industrial and consumer innovation:

Proximity Sensor Market Size

Wi-Fi Adapter Card Market Size

5G Processor Market Size

Kids Tablet Market Size

Laser Projector Market Size

Underwater Lighting Market Size

Static Random-Access Memory (SRAM) Market Size

Wafer Fabrication Market Size

Plasma Lighting Market Size

Fluorescent Lighting Market Size

Body Area Network Market Size

0 notes

Text

ADAS Camera Modules Market: Share, Size, Trends, 2025–2032

Global ADAS Camera Modules Market Research Report 2025(Status and Outlook)

The global ADAS Camera Modules market size was valued at US$ 6.74 billion in 2024 and is projected to reach US$ 14.2 billion by 2032, at a CAGR of 11.3% during the forecast period 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=95741

MARKET INSIGHTS

The global ADAS Camera Modules market size was valued at US$ 6.74 billion in 2024 and is projected to reach US$ 14.2 billion by 2032, at a CAGR of 11.3% during the forecast period 2025-2032.

ADAS camera modules are critical components in modern automotive safety systems, enabling features like lane departure warnings, automatic emergency braking, and adaptive cruise control. These modules integrate high-resolution cameras with advanced image processing capabilities to detect objects, pedestrians, and road markings in real-time. Key variants include front-view, rear-view, and surround-view systems, each serving distinct safety applications.

The market growth is driven by stringent government safety regulations, rising consumer demand for vehicle automation, and increasing adoption of electric vehicles with advanced driver assistance systems. However, challenges like high development costs and complex integration requirements may temper growth in price-sensitive markets. Major players including Magna International, Continental AG, and Valeo are investing heavily in developing higher-resolution thermal imaging cameras and AI-powered object recognition systems to maintain competitive advantage.

List of Key ADAS Camera Module Manufacturers

Magna International (Canada)

Phenix (South Korea)

Wuhan HT Optical and Electronic (China)

Cammsys (South Korea)

Wissen (China)

LiteOn (Taiwan)

Jabil Optical (U.S.)

Omnivision Technologies (U.S.)

Continental AG (Germany)

ZF Friedrichshafen AG (Germany)

Recent industry developments highlight intensifying competition, with several major players announcing next-generation camera systems featuring AI-powered object recognition and enhanced low-light performance. Market leaders are also forming strategic alliances with semiconductor companies to secure stable supplies of image sensor components, which remain critical for ADAS camera modules.

Segment Analysis:

By Type

Front Camera Modules Segment Leads Due to Growing Demand for Collision Avoidance Systems

The market is segmented based on type into:

Front cameras

Rear cameras

Side cameras

Interior cameras

Surround view systems

By Application

Passenger Vehicles Segment Dominates with Increased ADAS Adoption in Luxury and Mid-Range Cars

The market is segmented based on application into:

Passenger vehicles

Commercial vehicles

Electric vehicles

By Technology

Stereo Vision Technology Gains Traction for Enhanced Depth Perception Capabilities

The market is segmented based on technology into:

Mono cameras

Stereo vision cameras

Infrared cameras

Thermal cameras

By Level of Autonomy

Level 2 ADAS Systems Show Strong Adoption with Growing Semi-Autonomous Features

The market is segmented based on autonomy level into:

Level 1 (Driver Assistance)

Level 2 (Partial Automation)

Level 3 (Conditional Automation)

Level 4 (High Automation)

Regional Analysis: Global ADAS Camera Modules Market

North America The North American ADAS camera modules market is driven by stringent vehicle safety regulations, technological advancements, and high consumer awareness. NHTSA mandates require advanced driver assistance systems in all new vehicles by 2025, accelerating adoption. Tesla, GM, and Ford lead in integrating multi-camera systems, with front cameras dominating due to collision avoidance requirements. The U.S. accounts for over 80% of regional demand, supported by a robust automotive R&D ecosystem. However, supply chain disruptions and semiconductor shortages intermittently impact production scalability. The region favors high-resolution (8MP+) cameras with advanced image processing, creating opportunities for suppliers like Magna International and Jabil Optical.

Europe Europe’s market is shaped by Euro NCAP safety protocols and the EU’s Vision Zero initiative, pushing automakers to incorporate surround-view camera systems. Germany dominates with BMW and Mercedes-Benz pioneering night vision and AI-powered cameras. Regulatory pressure has made front and rear cameras standard in 92% of new EU vehicles as of 2023. However, pricing pressures persist as Eastern European OEMs prioritize cost-efficient solutions. The region shows growing demand for thermal imaging cameras in premium segments. Valeo and Continental maintain strong market positions through partnerships with European automakers, though Asian suppliers are gaining traction through competitive pricing.

Asia-Pacific As the largest and fastest-growing market, APAC accounts for over 45% of global ADAS camera module installations, driven by China’s booming EV sector and Japan’s safety-first automotive culture. Chinese brands like BYD and NIO prefer locally sourced camera modules from Wuhan HT Optical to avoid import tariffs. India’s market remains price-sensitive, with basic rear-view cameras dominating entry-level vehicles. Southeast Asia shows potential, though adoption lags due to fragmented regulations. Japan leads in camera-LiDAR fusion technologies, with Sony emerging as a key supplier. The region’s growth is tempered by quality consistency issues among local manufacturers and intellectual property concerns.

South America Market development in South America faces challenges including economic instability and low vehicle electrification rates. Brazil and Argentina represent 85% of regional demand, primarily for aftermarket rear-view cameras in commercial vehicles. OEM adoption remains limited to premium models due to cost constraints. However, recent safety regulation updates in Brazil (CONTRAN Resolution 920/2022) are expected to drive front-camera adoption by 2025. Chinese suppliers like Phenix are expanding distribution networks, though currency fluctuations impact pricing strategies. The lack of local manufacturing forces reliance on imports, creating supply chain vulnerabilities during global component shortages.

Middle East & Africa This emerging market shows divergent trends – Gulf Cooperation Council (GCC) countries favor luxury vehicles with comprehensive ADAS suites, while Africa’s market concentrates on basic camera systems for fleet safety. The UAE leads adoption due to Dubai’s Autonomous Transportation Strategy targeting 25% of trips via self-driving vehicles by 2030. South Africa serves as a regional hub for aftermarket installations. Political instability in parts of Africa and low new vehicle penetration (under 5% annually) constrain growth. Turkish manufacturers are gaining market share through competitively priced camera modules tailored for harsh climatic conditions, addressing dust and high-temperature performance requirements.

MARKET DYNAMICS

The increasing motorization rates in developing economies represent a significant growth opportunity for ADAS camera module manufacturers. As vehicle ownership expands in regions like Southeast Asia and Latin America, local safety regulations are evolving to match global standards. These markets currently have relatively low ADAS penetration rates compared to mature automotive markets, suggesting substantial room for growth. Local automakers in these regions are beginning to partner with international suppliers to incorporate camera-based safety systems into their vehicles. This trend is expected to accelerate as consumer awareness of vehicle safety increases and regional safety standards become more stringent.

The development of connected vehicle ecosystems presents exciting opportunities for ADAS camera systems. As vehicle-to-infrastructure and vehicle-to-vehicle communication technologies mature, camera systems are positioned to play a pivotal role in these networks. Future ADAS cameras may serve dual purposes – providing both traditional safety functions and acting as data collection points for smart city infrastructure. This convergence could dramatically increase the value proposition of camera modules, creating new revenue streams for manufacturers. Early pilot programs in several smart city initiatives have already demonstrated the potential of camera-equipped vehicles to improve urban traffic management and safety.

The rapid progress in edge computing and neural network processing presents significant opportunities for ADAS camera innovation. New system-on-chip designs are enabling more sophisticated processing to occur within the camera module itself, rather than relying on centralized vehicle computers. This architectural shift improves system responsiveness while reducing wiring complexity and weight. Manufacturers investing in these technologies stand to gain competitive advantage as automakers seek more efficient, scalable ADAS implementations. The ability to perform complex object recognition and predictive analytics directly within the camera module represents the next frontier in automotive safety technology.

The ADAS camera module market faces significant challenges related to the lack of universal standards across the industry. Different automakers employ varying interface protocols, mounting requirements, and performance specifications, creating complexity for suppliers. This fragmentation increases development costs and limits economies of scale. The absence of standardized testing methodologies for camera-based systems also creates uncertainty in performance evaluation. While industry consortia have made progress in developing common frameworks, widespread adoption remains slow, continuing to challenge manufacturers who must maintain multiple product variants to serve different customers.

As ADAS cameras become more sophisticated and connected, they increasingly face cybersecurity threats that challenge market growth. Modern camera modules often incorporate network connectivity for over-the-air updates and data sharing, creating potential vulnerability points. The automotive industry has seen a dramatic increase in cybersecurity incidents in recent years, with safety systems being particularly attractive targets for potential attacks. Developing secure camera systems requires significant additional investment in encryption, authentication protocols, and intrusion detection systems. These requirements add complexity to both product development and ongoing maintenance, potentially slowing time-to-market for new innovations.

The competitive nature of the ADAS market has led to increasingly complex intellectual property landscapes that challenge industry progress. Camera technology development involves numerous patent holders across imaging sensors, processing algorithms, and optical systems. Navigating these IP rights while trying to innovate requires substantial legal resources and can delay product development. Some promising technological collaborations have stalled due to IP disputes, potentially slowing the pace of innovation. As the market continues to grow, finding frameworks for productive IP sharing will become increasingly important for sustaining technological advancement.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=95741

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global ADAS Camera Modules Market?

Which key companies operate in Global ADAS Camera Modules Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/bluetooth-audio-ic-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/dual-in-line-memory-module-dimm-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/single-in-line-memory-module-simm.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/ddr4-register-clock-driver-market_4.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/ddr4-register-clock-driver-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/tft-lcd-billboards-and-signage-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-advanced-video-coding-avc-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-rf-synthesizers-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/ignition-safety-device-isd-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-external-plug-in-adapters-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-display-power-management-ic.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-display-ic-market-opportunities.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/automotive-nox-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-mask-packages-market-size-share.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/global-smart-lighting-market-industry.html

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 [+91 8087992013] [email protected]

0 notes

Text

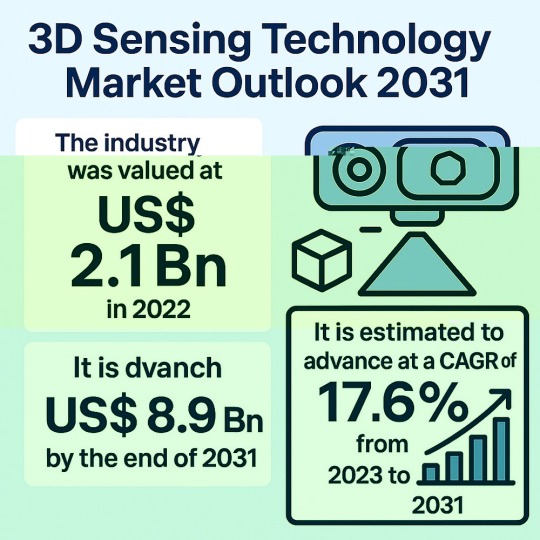

3D Sensing Technology Market to Witness Major Growth as Industries Embrace Digital Transformation

The 3D sensing technology market is witnessing an exciting phase of growth, driven by advancements in several key industries, ranging from consumer electronics to automotive and healthcare. As the global economy increasingly embraces digital transformation, the demand for innovative and immersive technologies is fueling the growth of 3D sensing solutions. The market, valued at US$ 2.1 Bn in 2022, is set to expand at a Compound Annual Growth Rate (CAGR) of 17.6%, reaching US$ 8.9 Bn by 2031, according to the latest market analysis.

Market Overview

3D sensing technology refers to the ability of devices to detect, measure, and interpret spatial information in three dimensions. This technology captures depth and creates detailed three-dimensional representations of objects using methods like structured light, time-of-flight (ToF), and stereoscopic vision. These innovations are increasingly integrated into diverse sectors such as automotive, industrial, healthcare, consumer electronics, and security & surveillance, offering new opportunities for product development and enhancement.

As demand for immersive technologies such as augmented reality (AR), virtual reality (VR), and advanced robotics escalates, 3D sensing technology is becoming a central component in the design of cutting-edge consumer and industrial applications. The future of this market is set to be propelled by the growing adoption of 3D sensing solutions in gaming, smart cities, and autonomous vehicles, with significant advancements anticipated across multiple segments.

Market Drivers & Trends

Several factors are propelling the 3D sensing technology market:

Rising Demand in Consumer Electronics: The proliferation of smartphones, gaming consoles, and wearables is a primary driver of the market. 3D sensing technology enhances the user experience by enabling features such as facial recognition, gesture control, and augmented reality (AR). These advancements are transforming how consumers interact with devices.

Government Initiatives in Smart Cities: The rapid urbanization and industrialization of emerging economies are fueling the demand for smart city infrastructure. 3D sensing technologies, including depth sensing cameras, LiDAR, and time-of-flight (ToF) sensors, are integral to urban planning, waste management, public safety, environmental monitoring, and infrastructure development.

Automotive Advancements: The growing need for autonomous vehicles and advanced driver-assistance systems (ADAS) is boosting demand for 3D sensors. Technologies such as LiDAR and radar systems are being incorporated into navigation systems, offering real-time updates on road traffic, weather conditions, and potential hazards.

Healthcare Applications: The adoption of robotics in healthcare is growing, and with it, the use of 3D sensing technologies. Surgeons are using 3D imaging for minimally invasive surgeries, improving diagnostic accuracy and enabling precise drug delivery. The medical sector's shift towards robotic surgeries is creating ample growth opportunities for 3D sensing technology providers.

Increased Popularity of Virtual and Augmented Reality: Virtual reality (VR) and augmented reality (AR) are rapidly evolving sectors, both of which rely heavily on 3D sensing technologies. Whether for gaming, training, or immersive experiences, 3D sensing is essential to providing realistic and interactive environments.

Latest Market Trends

Integration with Artificial Intelligence (AI) and IoT: AI and Internet of Things (IoT) technologies are increasingly being integrated with 3D sensing solutions to provide smarter, more intuitive systems. AI-driven data analysis enables real-time decision-making, while IoT devices are leveraging 3D sensing for applications in smart homes, industrial automation, and healthcare.

Miniaturization of Sensors: The continuous miniaturization of 3D sensors is allowing these devices to be integrated into smaller, more compact applications, especially in mobile devices, wearables, and drones. The ability to offer high-precision measurements in smaller form factors is expanding the potential for 3D sensing technology.

Advancements in Sensor Accuracy: New generations of 3D sensors are becoming more accurate and versatile. With improvements in depth sensing capabilities, these sensors are finding more applications in precision industries such as medical diagnostics, automotive, and manufacturing.

Key Players and Industry Leaders

The 3D sensing technology market is competitive and consists of key players leading the way in innovation and product development. Some of the leading companies in the market include:

ams-OSRAM AG

Infineon Technologies AG

PMD Technologies AG

STMicroelectronics N.V.

Texas Instruments Incorporated

Coherent Corp.

Lumentum Operations LLC

Himax Technologies, Inc.

Intel

Sony Depthsensing Solutions

Recent Developments

In recent months, several key developments have been observed in the 3D sensing technology space:

ams OSRAM AG launched a low-power, small-sized global shutter visible and near-infrared (NIR) image sensor for 2D and 3D sensing systems, making it ideal for applications in VR, drones, and industrial sensors.

Senet, Inc. and Iota Communications, Inc. partnered to offer 3D sensing technologies that support smart infrastructure, paving the way for increased adoption of 3D sensors in IoT-enabled environments.

Market Opportunities and Challenges

As the 3D sensing technology market expands, several opportunities and challenges emerge:

Opportunities:

The growing demand for robotics and automation in healthcare offers substantial growth potential for 3D sensing solutions, particularly in surgical applications.

Government investments in smart cities create new avenues for 3D sensing technologies, which are essential for efficient urban planning and management.

Technological advancements in augmented reality and virtual reality open new market opportunities for 3D sensing in gaming, training, and entertainment.

Challenges:

The high cost of 3D sensors and technology may pose a challenge to widespread adoption, particularly in emerging markets.

Data privacy concerns, especially regarding facial recognition and biometric security, could limit the deployment of 3D sensing solutions in certain sectors.

Integration and compatibility with existing systems across industries may require significant investment in research and development.

Future Outlook

Looking ahead, the global 3D sensing technology market is set to experience robust growth. The increasing adoption of IoT, AI, and automation will drive demand for more precise and innovative 3D sensing solutions. Additionally, the continued push towards autonomous vehicles and smart cities will create new applications for this technology.

The key to sustained growth will lie in the ability of companies to innovate and address challenges such as cost-effectiveness and data privacy while capitalizing on new opportunities in the healthcare, automotive, and consumer electronics sectors.

Market Segmentation

Technology:

Stereoscopic Vision

Structured Light Pattern

Time of Flight (ToF)

Ultrasound

Sensor Type:

Pressure Sensors

Image Sensors

Gyro Sensors

Proximity Sensors

End-user Industries:

Consumer Electronics

Media & Entertainment

Automotive

Security & Surveillance

Industrial

Regional Insights:

North America

Europe

Asia Pacific

South America

Middle East & Africa

Why Buy This Report?

This comprehensive report on the 3D sensing technology market provides:

In-depth market analysis: With segment and regional-level insights, market trends, and forecasts for the period 2023-2031.

Competitive landscape: Profiles of key players, their strategies, financial performance, and recent developments.

Future insights: Detailed analysis of emerging opportunities and challenges, as well as technological innovations in 3D sensing.

For businesses, investors, and professionals looking to understand the dynamic landscape of the 3D sensing technology market, this report offers valuable insights that will inform strategic decisions, product development, and market entry.

0 notes

Text

Automotive DC-DC Converters Market Drivers Fueling Industry Expansion Globally

The global automotive DC-DC converters market is witnessing significant growth, driven by the rising adoption of electric vehicles (EVs), advancements in vehicle electrification, and the growing emphasis on energy efficiency. DC-DC converters play a vital role in modern automotive electrical architectures, enabling efficient voltage conversion between high-voltage batteries and low-voltage subsystems. With automakers investing heavily in EV production and technological innovation, the demand for reliable, compact, and high-performance DC-DC converters is expected to accelerate in the coming years.

Market Drivers

1. Booming Electric Vehicle (EV) Market

One of the primary drivers of the automotive DC-DC converters market is the exponential rise in electric vehicle production and adoption. Governments worldwide are introducing stringent emission regulations and providing incentives for EV purchases, pushing manufacturers to expand their electric fleets. EVs require efficient DC-DC converters to manage voltage levels between high-voltage battery packs and lower-voltage systems such as lighting, infotainment, and electronic control units (ECUs). As EV sales continue to climb, so does the need for advanced DC-DC converter solutions.

2. Increased Vehicle Electrification

The growing trend of vehicle electrification extends beyond EVs to include hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs). Even conventional vehicles are increasingly incorporating electronic systems that demand stable, regulated power supplies. DC-DC converters ensure smooth voltage transitions, improve energy efficiency, and support critical vehicle functions. As automakers prioritize electrification to meet sustainability targets and consumer demands for enhanced safety and comfort features, the market for automotive DC-DC converters is experiencing steady growth.

3. Technological Advancements and Product Innovation

Advancements in semiconductor technology, miniaturization, and power electronics have significantly improved the performance of automotive DC-DC converters. Modern converters offer higher efficiency, reduced weight, compact form factors, and improved thermal management, making them ideal for space-constrained automotive environments. Innovations such as GaN (Gallium Nitride) and SiC (Silicon Carbide) power devices are enhancing power density and overall system efficiency. These technological breakthroughs are fueling the adoption of DC-DC converters across various vehicle platforms.

4. Rising Demand for Advanced Safety and Infotainment Systems

The integration of sophisticated driver assistance systems (ADAS), infotainment, and connected car technologies necessitates a reliable low-voltage power supply within vehicles. DC-DC converters facilitate efficient power delivery to cameras, sensors, navigation units, and entertainment systems, enhancing overall vehicle functionality and user experience. The increasing consumer preference for high-tech, connected vehicles is directly contributing to the expansion of the DC-DC converters market.

5. Supportive Government Regulations and Incentives

Global initiatives to reduce greenhouse gas emissions and promote energy-efficient transportation have created a favorable regulatory environment for the adoption of EVs and hybrid vehicles. Government subsidies, tax benefits, and investments in charging infrastructure are accelerating the electrification of the automotive sector. This regulatory push, combined with environmental awareness among consumers, is driving demand for essential components like DC-DC converters that enable efficient energy management in electric and hybrid vehicles.

6. Growing Aftermarket Demand for DC-DC Converters

The aftermarket for automotive DC-DC converters is expanding due to the rising need for replacement parts and system upgrades, particularly in aging vehicles equipped with modern electrical components. As consumers retrofit vehicles with enhanced electronics, infotainment, or energy-efficient systems, the demand for reliable DC-DC converters increases, creating new revenue streams for market players.

Conclusion

The automotive DC-DC converters market is poised for substantial growth, fueled by the surging electric vehicle industry, technological advancements, vehicle electrification trends, and rising demand for advanced in-vehicle systems. With supportive government policies and consumer preferences shifting toward energy-efficient and connected vehicles, manufacturers and suppliers of DC-DC converters have significant opportunities for innovation and market expansion. As the automotive landscape evolves, the importance of reliable, high-performance DC-DC converters will only intensify, shaping the future of sustainable and technologically advanced mobility solutions.

0 notes

Text

Edge AI Hardware Market Is Set to Garner Staggering Revenues By 2030

Allied Market Research, titled, “Edge AI Hardware Market By Component, Device Type, Process, and End User: Global Opportunity Analysis and Industry Forecast, 2021–2030”, the global edge AI hardware market size was valued at $6.88 billion in 2020, and is projected to reach $38.87 billion by 2030, registering a CAGR of 18.8%. Asia-Pacific is expected to be the leading contributor toward the edge AI hardware market during the forecast period, followed by LAMEA and Europe.

Edge AI hardware is a device that can take decisions & process data independently without any external connection. These edge AI hardware does not have any issue of bandwidth and latency of real-time data, which influence application execution. Real time operations are very crucial in robots and self-driving cars among other applications.

Global edge AI hardware market growth is anticipated to be driven by factors such as emergence of AI coprocessors for edge computing and rise in IoT applications by various end user industries such as automotive and consumer electronics. In addition, increase in real-time low latency on edge devices, boosts the overall market growth. However, power consumption & size constraint acts as a major restraint for the global edge AI hardware industry. On the contrary, rise in demand and adoption of artificial intelligence products & services is expected to create lucrative opportunities for the market.

Moreover, developing nations tend to witness high penetration of edge AI hardware products, especially in the automotive sector, which is anticipated to augment the market growth. Factors such as growing driverless vehicles accelerate the market growth.

The global edge AI hardware market is segmented on the basis of component, device type, process, end user, and region. By component, the market is classified into processor, memory, sensor, and others. Depending on device type, it is categorized into smartphones, cameras, robots, wearables, smart speaker, and others. The process covered in the study include training and inference. On the basis of end user, it is classified into consumer electronics, smart home, automotive, government, aerospace & defense, healthcare, industrial, construction, and others.

Region wise, the edge AI hardware market trend is analyzed across North America (U.S., Canada, and Mexico), Europe (UK, Germany, France, Russia, and rest of Europe), Asia-Pacific (China, Japan, India, Australia, and rest of Asia-Pacific), and LAMEA (Latin America, Middle East, and Africa). The edge AI hardware market size have been analyzed across North America, Europe, Asia-Pacific, and LAMEA. North America contributed maximum revenue in 2020.

However, in between 2020 and 2030, the edge AI hardware market in Asia-Pacific is expected to grow at a faster rate as compared to other regions. This is attributed to increase in demand from emerging economical countries such as India, China, Japan, Taiwan, and South Korea.

Key Findings of the Study

The consumer electronics sector is projected to be the major application, followed by industrial.

Asia-Pacific and North America collectively accounted for more than 61% of the edge AI hardware market share in 2020.

India is anticipated to witness highest growth rate during the forecast period.

U.S. was the major shareholder in the North America edge AI hardware market, accounting for approximately 55% share in 2020.

Depending on component, the processor segment generated the highest revenue in 2020. Also, the processor segment is expected to witness the highest growth rate in the near future.

Region wise, the edge AI hardware market was dominated by North America. However, Asia-Pacific is expected to witness significant growth in the coming years.

The key players profiled in the report include Apple Inc., Google LLC (Alphabet Inc.), Huawei Technologies Co., Ltd., Intel Corporation, International Business Machines Corporation (IBM), MediaTek Inc., Microsoft Corporation, NVIDIA Corporation, Qualcomm Technologies, Inc., and Samsung Electronics Co. Ltd. (Samsung). These players have adopted various strategies such as acquisition and product launch to strengthen their foothold in the industry

0 notes

Text

Self-driving Cars Sensors Market - Trends, Growth, including COVID19 Impact, Forecast

Global Self-driving Cars Sensors Market Research Report 2025(Status and Outlook)

The global Self-driving Cars Sensors Market size was valued at US$ 4.78 billion in 2024 and is projected to reach US$ 17.94 billion by 2032, at a CAGR of 17.98% during the forecast period 2025-2032.

Self-driving car sensors are critical components enabling autonomous vehicles to perceive their surroundings. These include camera sensors for visual recognition, radar sensors for object detection and distance measurement, and lidar sensors for high-resolution 3D mapping. Advanced sensor fusion technologies combine these inputs to create comprehensive environmental awareness essential for autonomous navigation.

The market growth is driven by increasing investments in autonomous vehicle technology from major automotive manufacturers and tech companies. Regulatory approvals for Level 3 autonomous vehicles in key markets, along with declining sensor costs (lidar prices have fallen by approximately 60% since 2018), are accelerating adoption. However, challenges remain in achieving full redundancy and reliability across diverse driving conditions. Key players like Bosch, Continental AG, and Denso Corporation are actively expanding their sensor portfolios through strategic partnerships and R&D investments to capitalize on this high-growth market.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis.https://semiconductorinsight.com/download-sample-report/?product_id=95899

Segment Analysis:

By Type

Lidar Sensors Segment Dominates Due to High Precision in Object Detection and Mapping

The market is segmented based on type into:

Camera Sensors

Radar Sensors

Lidar Sensors

Ultrasonic Sensors

Others

By Application

Passenger Vehicles Segment Leads Owing to Rising Consumer Demand for Autonomous Features

The market is segmented based on application into:

Passenger Vehicles

Commercial Vehicles

Transportation-as-a-Service (TaaS)

Others

By Automation Level

Level 3 Automation Segment Shows Strong Growth Potential with Conditional Driving Automation

The market is segmented based on automation level into:

Level 1 (Driver Assistance)

Level 2 (Partial Automation)

Level 3 (Conditional Automation)

Level 4 (High Automation)

Level 5 (Full Automation)

By Vehicle Type

Electric Vehicles Segment Gains Traction Due to Integration with Self-Driving Technology

The market is segmented based on vehicle type into:

Internal Combustion Engine (ICE) Vehicles

Hybrid Electric Vehicles

Battery Electric Vehicles

Regional Analysis: Global Self-driving Cars Sensors Market

North America The North American self-driving car sensors market is currently the most advanced globally, driven by strong technological innovation and regulatory support. The U.S. leads with significant investments from automotive OEMs and tech companies like Waymo, Tesla, and GM’s Cruise. Stringent safety standards from NHTSA and emerging federal AV policy frameworks create a structured environment for sensor deployment. Lidar adoption is particularly strong here, with market leaders like Luminar and Velodyne gaining traction. However, high sensor costs and unresolved liability issues surrounding autonomous vehicle accidents remain key challenges. The market is expected to grow at a CAGR of over 12% through 2030, with passenger vehicles accounting for nearly 70% of sensor demand.

Europe Europe’s sensor market prioritizes safety and compliance, with strict EU regulations on autonomous driving systems pushing manufacturers toward multi-sensor fusion approaches. Companies like Bosch and Continental dominate the radar and camera sensor segments, while local players are making strides in solid-state lidar development. The region shows strong demand for commercial vehicle applications, particularly in Germany and France where truck platooning trials are underway. Data privacy concerns under GDPR and high consumer skepticism about autonomous technology present growth barriers. That said, substantial EU funding for connected mobility projects (over €1 billion allocated through Horizon Europe) continues to drive R&D investment in advanced sensor technologies.

Asia-Pacific Asia-Pacific is emerging as the fastest-growing market, projected to surpass North America in sensor unit shipments by 2026. China’s aggressive push for AV leadership, backed by government initiatives like the New Generation AI Development Plan, has created a thriving ecosystem. Local manufacturers like Hesai Tech and Leishen compete effectively on lidar pricing, while Japanese firms lead in camera-based ADAS solutions. India and Southeast Asia show growing demand, though infrastructure limitations and cost sensitivity favor radar over more expensive lidar systems. The region also sees unique applications emerging, such as autonomous fleets for last-mile delivery in dense urban environments where sensor redundancy is prioritized.

South America South America’s market remains in early development stages, focusing primarily on basic ADAS sensor adoption rather than full autonomy. Brazil and Argentina lead with gradual integration of radar and camera systems in premium passenger vehicles, though overall penetration remains below 15%. Economic instability,缺乏 of charging infrastructure for electric autonomous vehicles, and minimal local manufacturing capacity hinder growth. However, mining and agricultural applications in Chile and Peru present niche opportunities for robust sensor systems designed for harsh environments. Regulatory frameworks are still evolving, creating uncertainty for long-term investments in the region.

List of Key Self-driving Car Sensor Companies Profiled

Robert Bosch GmbH (Germany)

Continental AG (Germany)

Denso Corporation (Japan)

Veoneer (Sweden)

Valeo (France)

Hella GmbH & Co. KGaA (Germany)

Aptiv PLC (Ireland)

Panasonic Corporation (Japan)

ZF Friedrichshafen AG (Germany)

Hitachi Ltd. (Japan)

Velodyne Lidar (USA)

Luminar Technologies (USA)

The global autonomous vehicle market is projected to expand at an impressive CAGR of approximately 40% over the next five years, directly fueling demand for advanced sensor technologies. Modern self-driving cars require a sophisticated sensor fusion approach combining LiDAR, radar, and cameras to achieve SAE Level 4/5 autonomy. Major automotive manufacturers have announced plans to integrate autonomous features in over 50% of new vehicle models by 2030, creating sustained demand for reliable sensing solutions. Industry leaders are investing heavily in sensor development, with recent advances in solid-state LiDAR and 4D radar offering improved performance at decreasing costs.

Stringent vehicle safety regulations across major automotive markets are accelerating sensor deployment. Regulatory bodies in North America and Europe now mandate advanced driver assistance systems (ADAS) in all new vehicles, directly benefiting sensor manufacturers. Recent legislation in several countries provides subsidies for autonomous vehicle development, with funding exceeding $15 billion globally for smart transportation initiatives. Such government support not only validates the technology but also reduces adoption risks for automotive OEMs and tier-1 suppliers.

Breakthroughs in artificial intelligence and edge computing are enabling more sophisticated sensor fusion capabilities critical for autonomous driving. Modern autonomous systems process over 5TB of sensor data per hour, requiring innovative solutions for real-time data interpretation. Recent product launches demonstrate significant progress, with some new sensors offering 300-meter detection range at centimeter-level accuracy while consuming 40% less power than previous generations. These technological improvements are making autonomous systems more reliable and commercially viable for mass-market vehicles.

The transition from mechanical to solid-state sensor designs represents a major technological leap, enabling smaller form factors, improved reliability, and lower production costs. Analysts project that solid-state LiDAR solutions could achieve price points below $500 per unit within three years compared to current $5,000+ systems. Such cost reductions would dramatically improve the business case for autonomous vehicles while enabling broader sensor deployment across vehicle segments. Several startups have recently demonstrated production-ready solid-state designs that maintain performance while eliminating moving parts.

While passenger vehicles dominate current attention, commercial applications including logistics, mining, and agriculture present substantial opportunities with potentially faster adoption timelines. Autonomous trucks alone could represent a $30 billion sensor market by 2030, as operational efficiencies justify earlier investment in these applications. Industrial environments often present more controlled operating conditions than public roads, allowing for faster commercialization of autonomous solutions with appropriate sensor configurations.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=95899

Key Questions Answered by the Outsourced Self-driving Cars Sensors Market Report:

What is the current market size of Global Self-driving Cars Sensors Market?

Which key companies operate in this market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Browse More Reports:

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

0 notes

Text

U.S. Pillow Market : Key Drivers, Significant Analysis

Global U.S. Pillow Market valued at USD X.X Billion in 2024 and is projected to reach USD X.X Billion by 2032, growing at a CAGR of X.X% from 2025 to 2032. Market Report U.S. Pillow Market: Significant Analysis The U.S. pillow market is experiencing steady growth driven by rising consumer awareness of sleep health and comfort. Increasing disposable incomes and evolving lifestyle trends contribute to greater demand for innovative and ergonomic pillow designs. The market is projected to expand at a consistent rate over the next five years, fueled by advancements in material technology and customization options. Consumers are increasingly opting for memory foam, latex, and cooling pillows, which provide enhanced support and comfort. Moreover, online retail channels are making these products more accessible, widening the customer base. The market’s growth is also supported by a surge in wellness-focused products and an aging population seeking better sleep solutions. Overall, the market outlook remains positive with ongoing innovation and diversification expected to drive future expansion. Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs) @ https://www.verifiedmarketresearch.com/download-sample/?rid=369964&utm_source=Glob-VMR&utm_medium=265 U.S. Pillow Market Key Drivers Several key drivers propel the U.S. pillow market forward. Increasing awareness about the importance of sleep and its impact on health has led consumers to invest in high-quality pillows. Innovations in pillow materials such as memory foam, gel-infused foams, and hypoallergenic fabrics offer better comfort and hygiene, attracting a broad customer base. The rise of e-commerce platforms simplifies product discovery and purchase, boosting market accessibility. Additionally, growing concerns about neck pain and posture correction encourage consumers to seek ergonomic solutions, further enhancing demand. Urbanization and hectic lifestyles increase the focus on restorative sleep, which in turn stimulates pillow sales. The influence of social media and endorsements by health professionals also educate and motivate consumers to prioritize better sleep products. U.S. Pillow Market: Future Scope The future scope of the U.S. pillow market is promising with significant opportunities for expansion. Emerging trends emphasize smart pillows embedded with sensors that monitor sleep patterns and offer personalized recommendations. Growing consumer preference for eco-friendly and sustainable materials is expected to shape product development. Additionally, collaborations between manufacturers and wellness brands may introduce holistic sleep solutions combining pillows with other health technologies. Regional penetration in untapped markets and customization options tailored to individual needs will also drive growth. Continuous R&D efforts aimed at improving durability, comfort, and cooling features position the market for sustained progress. As consumers increasingly prioritize wellness and quality of life, the pillow market stands to benefit substantially from these evolving demands. Refractive Optical Element Market Regional Analysis""""""" The Asia Pacific refractive optical element market shows robust regional growth influenced by increasing demand in electronics, automotive, and healthcare sectors. Rapid industrialization and technological advancements in countries like China, Japan, and South Korea fuel the expansion of this market. Growing investments in research and development activities enhance the production capabilities and innovation of optical elements. The rise of consumer electronics, including cameras, smartphones, and augmented reality devices, creates substantial demand for precision optical components. Additionally, government initiatives supporting optical manufacturing and exports contribute to market growth. Increasing applications in medical imaging and defense sectors further bolster the market’s regional significance.

The Asia Pacific region is expected to maintain a leading position globally due to its strong manufacturing base and expanding end-use industries. Download Full PDF Sample Copy of U.S. Pillow Market Report @ https://www.verifiedmarketresearch.com/download-sample/?rid=369964&utm_source=Glob-VMR&utm_medium=265 Key Competitors in the U.S. Pillow Market These companies are renowned for their broad product offerings, sophisticated technologies, strategic efforts, and robust market presence. Each competitor's primary advantages, market share, current events, and competitive tactics—such as collaborations, mergers, acquisitions, and the introduction of new products—are highlighted in the study. Key Player 1 Key Player 2 Key Player 3 Key Player 4 Key Player 5 Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount/?rid=369964&utm_source=Glob-VMR&utm_medium=265 U.S. Pillow Market Trends Insights U.S. Pillow Market Trend Insights offers a thorough examination of the market's current and developing trends, providing insightful data-driven viewpoints to assist companies in making wise decisions. This study explores the major consumer trends, market forces, and technology developments influencing the sector. U.S. Pillow Market Size By Outer Material Type •Linen•Chenille•Velvet By Application •Home use and Commercial use By Sales Channel •Wholesalers and Retailers By Product •Decorative pillows•Sleeping pillows By Inner Material Type •Foam•Cotton•Feather By Pillow Size •18″X18″•24″X24″•20″X20″ By End Use •Indoor and Outdoor By Color •Monochrome and Color And Forecast By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa For More Information or Query, Visit @ https://www.verifiedmarketresearch.com/product/us-pillow-market/ Detailed TOC of U.S. Pillow Market Research Report, 2026-2032 1. Introduction of the U.S. Pillow Market Overview of the Market Scope of Report Assumptions 2. Executive Summary 3. Research Methodology of Verified Market Reports Data Mining Validation Primary Interviews List of Data Sources 4. U.S. Pillow Market Outlook Overview Market Dynamics Drivers Restraints Opportunities Porters Five Force Model Value Chain Analysis 5. U.S. Pillow Market, By Geography North America Europe Asia Pacific Latin America Rest of the World 6. U.S. Pillow Market Competitive Landscape Overview Company Market Ranking Key Development Strategies 7. Company Profiles 8. Appendix About Us: Verified Market Research®Verified Market Research® is a leading Global Research and Consulting firm that has been providing advanced analytical research solutions, custom consulting and in-depth data analysis for 10+ years to individuals and companies alike that are looking for accurate, reliable and up to date research data and technical consulting. We offer insights into strategic and growth analyses, Data necessary to achieve corporate goals and help make critical revenue decisions.Our research studies help our clients make superior data-driven decisions, understand market forecast, capitalize on future opportunities and optimize efficiency by working as their partner to deliver accurate and valuable information. The industries we cover span over a large spectrum including Technology, Chemicals, Manufacturing, Energy, Food and Beverages, Automotive, Robotics, Packaging, Construction, Mining & Gas. Etc.Having serviced over 5000+ clients, we have provided reliable market research services to more than 100 Global Fortune 500 companies such as Amazon, Dell, IBM, Shell, Exxon Mobil, General Electric, Siemens, Microsoft, Sony and Hitachi. We have co-consulted with some of the world's leading consulting firms like McKinsey & Company, Boston Consulting Group, Bain and Company for custom research and consulting projects for businesses worldwide. Contact us:Mr. Edwyne FernandesVerified Market Research®US: +1 (650)-781-4080UK: +44 (753)-715-0008APAC: +61 (488)-85-9400US Toll-Free: +1 (800)-782-1768Email: sales@verifiedmarketresearch.

comWebsite:- https://www.verifiedmarketresearch.com/ Global Pineapple Powder Market

0 notes

Text

Driver and Occupant Monitoring Systems Market : Size, Trends, and Growth Analysis 2032

In the age of intelligent transportation, Driver and Occupant Monitoring Systems (DOMS) are revolutionizing the automotive industry by prioritizing in-cabin safety, real-time monitoring, and proactive response. These systems, driven by a fusion of artificial intelligence (AI), sensors, and biometric analytics, are no longer futuristic concepts—they're becoming essential features in modern vehicles.

With a market valuation of US$ 8,209.32 million in 2024 and a projected CAGR of 15.90% from 2025 to 2032, the DOMS market is poised for rapid expansion. Detailed segmentation by Type (Driver Monitoring Systems, Occupant Monitoring Systems), Components, Vehicle Type, Sales Channel, Country, and Region provides a comprehensive view of industry dynamics. To explore key insights, visit the full Driver and Occupant Monitoring Systems Market Report.

What are Driver and Occupant Monitoring Systems?

DOMS are advanced technologies integrated into vehicles to monitor driver attention and passenger behavior. These systems use AI-based algorithms along with cameras, infrared sensors, and facial recognition tools to gather and analyze data in real time.

Driver Monitoring Systems (DMS) typically assess:

Eye-tracking to gauge focus

Facial recognition to detect fatigue or distraction

Head position monitoring to identify lack of attention

Drowsiness and distraction detection to issue timely alerts

On the other hand, Occupant Monitoring Systems (OMS) focus on:

Occupant presence detection (for automatic airbag deployment)

Seat belt monitoring

Child detection (particularly in rear seats)

Passenger behavior analysis for comfort, entertainment, or safety intervention

These systems work in unison to elevate both driver performance and passenger protection, especially in semi-autonomous and autonomous vehicles.

Market Drivers Fueling Growth

Several macro and microeconomic factors are accelerating the adoption of DOMS across global markets:

1. Rise in Road Accidents Linked to Human Error

Over 90% of traffic accidents are caused by human factors such as distraction, fatigue, or substance use. DOMS can act as early warning systems to prevent these mishaps by actively assessing a driver’s state and intervening when necessary.

2. Integration with Advanced Driver Assistance Systems (ADAS)

Driver and occupant monitoring systems are increasingly being integrated into larger ADAS frameworks, working in harmony with lane-keeping assist, emergency braking, and adaptive cruise control systems.

3. Regulatory Push for In-Cabin Monitoring

The European Union’s General Safety Regulation (GSR) mandates that all new vehicles be equipped with DMS starting in 2024. Other countries, including the U.S., China, and Japan, are also expected to introduce or tighten regulations around in-cabin safety, especially with the rise of autonomous driving.

4. Growing Demand for Premium and Connected Vehicles

Consumers now expect smart features in vehicles—not just externally with sensors and cameras, but internally. Automakers are responding by embedding DOMS into mid-range and high-end models to enhance the driving experience and differentiate their offerings.

Competitive Landscape: Leaders in the DOMS Market

The global market for DOMS is witnessing fierce competition among tech giants and automotive innovators:

Aptiv Plc – A leader in advanced safety systems, offering DMS solutions with deep learning capabilities.

Continental AG – Integrates driver and occupant analytics with cloud-based data for predictive safety.

Denso Corporation – Focuses on combining biometric sensing with thermal and comfort management systems.

Magna International Inc. – Provides flexible camera-based DMS platforms for diverse vehicle types.

Robert Bosch GmbH – A pioneer in in-cabin monitoring, known for combining AI with real-time threat detection.

Valeo SA – Innovates in infrared camera and AI processing for high-accuracy driver assessments.

These companies are investing heavily in research and development, strategic partnerships, and AI-powered innovations to maintain competitive advantage in this rapidly evolving landscape.

Challenges and Future Opportunities

Although the market outlook is promising, some challenges persist:

Privacy concerns related to biometric data collection

Cost barriers in entry-level vehicles

System calibration issues in different lighting or driving conditions

However, opportunities abound:

AI-enhanced personalization: DOMS could adapt cabin settings based on mood and passenger behavior.

Fleet management and insurance integration: Fleet operators and insurers can use real-time DMS data for driver scoring, liability assessment, and predictive maintenance.

Expansion into ride-sharing and autonomous mobility: As ride-sharing grows, monitoring multiple occupants simultaneously becomes crucial for safety and behavior analytics.

The Road Ahead

As we transition into an era of autonomous mobility and connected vehicles, driver and occupant monitoring systems will be non-negotiable elements of automotive safety architecture. These systems are not just about compliance or tech novelty—they’re about saving lives, enhancing comfort, and building trust in autonomous systems.

The DOMS market represents more than a trend; it's a transformation that’s reshaping how vehicles interact with the people inside them.

🔗 Discover the full industry outlook and projections in the Driver and Occupant Monitoring Systems Market Report.

Browse more Report:

Cold Storage Transportation Market

Cement Electrostatic Precipitator Market

BOPET Films Market

Bioprocess Analyzers Market

Autonomous Beyond Visual Line of Sight (BVLOS) Drone Market

0 notes

Text

3D and 4D Technology Market - Global Drivers, Opportunities, Trends, and Forecasts to 2031

The 3D and 4D Technology Market size is expected to reach US$ 1100.92 billion by 2031 from US$ 341.84 billion in 2024. The market is estimated to record a CAGR of 18.5% from 2025 to 2031.

Adding the temporal dimension through 4D simulations allows for the modeling of real-time urban dynamics such as traffic flow, pedestrian movement, and environmental conditions. These simulations aid in evaluating the impact of various scenarios, enabling better decision-making regarding construction timelines, resource allocation, and infrastructure resilience. The combination of 3D and 4D technologies offers scalable solutions for urban growth, traffic management, and environmental sustainability, making them indispensable tools for future-ready city planning. The product landscape of the 3D and 4D technology market includes components such as printing, displays, cameras, sensors, and other hardware. Among these, 3D printing holds a significant share due to its wide-ranging applications in fields like automotive, aerospace, healthcare, and consumer goods. It facilitates the production of complex, customized, and functional items at lower costs and faster speeds. The emergence of 4D printing introduces smart materials capable of altering their structure in response to environmental stimuli such as temperature or pressure.

The 3D and 4D Technology Market is rapidly transforming various industries by introducing immersive and interactive experiences. From entertainment and healthcare to automotive and construction, the adoption of 3D and 4D technologies is reshaping business landscapes and consumer expectations. The 3D and 4D Technology Market continues to thrive due to advancements in imaging, sensing, and simulation technologies that provide depth, realism, and spatial awareness to digital content.

A major factor driving the growth of the 3D and 4D Technology Market is the increasing demand for 3D content across entertainment and media platforms. The use of 3D modeling and animation in movies, games, and virtual reality experiences has become mainstream, pushing developers and producers to invest heavily in these technologies. Moreover, 4D technology adds a time-based dimension, enhancing realism with effects like motion, temperature, and scent, thus offering consumers a more lifelike interaction.

In the healthcare sector, the 3D and 4D Technology Market is revolutionizing diagnostic and surgical procedures. Technologies such as 3D imaging and 4D ultrasound allow medical professionals to view organs and tissues in high detail, improving accuracy in diagnosis and treatment planning. The integration of 3D printing within the 3D and 4D Technology Market also supports the development of customized prosthetics and implants, further advancing patient care and personalization.

Another significant application of the 3D and 4D Technology Market is in the automotive and aerospace sectors. Engineers and designers rely on 3D visualization and prototyping to optimize designs, reduce production costs, and improve product safety. The use of 4D simulations in these industries allows for real-time testing and scenario analysis, providing insights into the performance and durability of components over time.

The construction and architecture fields are also experiencing the benefits of the 3D and 4D Technology Market. Architects now use 3D modeling tools to create highly detailed building plans, while 4D BIM (Building Information Modeling) integrates time as a factor to enable construction teams to visualize project phases and timelines. This leads to better planning, resource allocation, and risk mitigation on complex projects.

Geographically, North America holds a dominant position in the 3D and 4D Technology Market, supported by technological innovation, robust research infrastructure, and high consumer adoption rates. However, the Asia-Pacific region is expected to witness the fastest growth due to rising investments in technology, expanding consumer electronics markets, and increased demand for digital solutions across industries.

The future of the 3D and 4D Technology Market is bright, with opportunities driven by advancements in AI, machine learning, and IoT. These complementary technologies enhance the functionality and usability of 3D and 4D solutions, enabling smarter simulations and more responsive systems. As industries continue to embrace digital transformation, the 3D and 4D Technology Market will remain at the forefront of innovation, enabling richer, more immersive experiences.

In conclusion, the 3D and 4D Technology Market is not just a technological trend—it is a transformative force across diverse sectors. With continuous innovation and expanding applications, the 3D and 4D Technology Market is poised for sustained growth, offering limitless possibilities for the future.

The List of Companies.

3D Systems Corp

Autodesk Inc

Dassault Systemes SE

Dolby Laboratories Inc

Panasonic Holdings Corp

Materialise NV

Hexagon AB

BASLER AG

Samsung Electronics Co Ltd

Stratasys Ltd.

Executive Summary and Global Market Analysis:

The 3D and 4D technology market have experienced robust growth in recent years, driven by advancements in technology and increased consumer demand for immersive experiences. The growing popularity of 3D-enabled TVs, smartphones, and VR headsets has spurred the demand for 3D and 4D content. Consumer interest in enhanced visual experiences drives the adoption of technologies like 3D projection and AR/VR gaming. The film and gaming sectors are major consumers of 3D and 4D technologies. 3D films have become mainstream, while 4D cinemas provide an enhanced experience by combining physical motion, environmental effects (such as wind, water, or scents), and 3D visuals. Improvements in display technologies, such as OLED and 8K resolution, contribute to sharper, more dynamic visuals, driving the demand for 3D content. Applications in gaming, education, healthcare, and training are major contributors to the rise of VR and AR, which depend on 3D and 4D technologies to provide immersive experiences. The demand for interactive, real-time experiences has driven advancements in haptic feedback, touch technology, and motion-sensing, essential elements in 4D environments.

3D and 4D Technology Market Size and Share Analysis

In terms of end users, the market is segmented into automotive, consumer electronics, aerospace and defense, healthcare, construction and architecture, media and entertainment, and others. The aerospace and defense segment held the largest share of the market in 2024. 3D and 4D technologies play a vital role in enhancing the capabilities of the military and defense sectors. In military applications, 3D modeling, simulation, and printing are used to design and prototype complex weapons, vehicles, and equipment with high precision. 3D printing, in particular, enables the creation of rapid prototypes, custom parts, and even field repairs for defense systems, reducing downtime and cost. 4D technologies can also be applied in military training simulations, where real-time environmental effects (weather, terrain changes, and motion) are synchronized with the virtual environment to improve realism in mission training.

The geographic scope of the 3D and 4D technology market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The 3D and 4D technology market in Asia Pacific is expected to grow significantly during the forecast period.

Asia Pacific has become one of the largest markets for 3D printing, with China at the forefront. The China government has heavily invested in 3D printing research and development, seeing it as a key part of its "Made in China 2025" initiative to modernize its manufacturing sector. 3D modeling is revolutionizing the construction and architecture industries in Asia. In countries such as China and India, the large-scale development of cities and infrastructure projects has led to the widespread use of 3D modeling software such as AutoCAD and Rhino. These tools allow architects to visualize complex building designs and optimize their structures before actual construction begins. For example, China has been using 3D printing technologies to construct entire buildings, reducing both the time and cost of construction. In healthcare, countries such as Japan and South Korea are using 3D printing to produce customized prosthetics and implants. For instance, Japan-based Mitsubishi Heavy Industries has been using 3D printing to develop advanced medical devices and tools. In India, 3D printing is being used to produce affordable, patient-specific medical implants, such as titanium knee and hip replacements, making healthcare more accessible.

About Us-

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

0 notes

Text

Interaction Sensor Market Size Redefining Human-Machine Interfaces by 2030