#Automotive Heat Exchanger Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

panelledlightsinahmedabad-blog

Switch Dealer, Decorative Lights, Panel Led lights in Ahmedabad

2 posts

Fun Fact

The Tumblr app for Google Glass was released on May 16, 2013.

Text

Automotive Heat Exchanger Market Size & Share, Growth Trends 2023-2027

Automotive Heat Exchanger Market Size & Share, Growth Trends 2023-2027

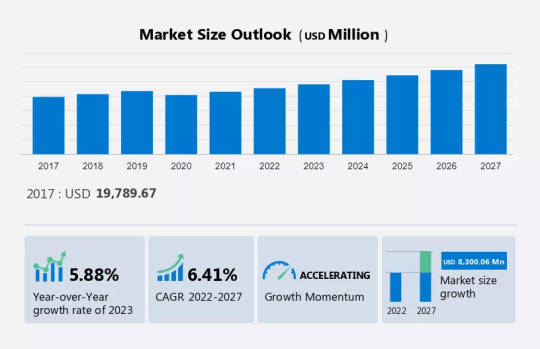

The projected expansion of the Automotive Heat Exchanger Market suggests an estimated growth of USD 8,300.06 million from 2022 to 2027, with an accelerated Compound Annual Growth Rate (CAGR) of 6.41% during the forecast period. This growth is influenced by various factors, notably the substantial reliance on internal combustion (IC) engines for transportation in emerging nations, a surge in passenger car sales, and the mounting government mandates regarding the adoption of efficient Heating, Ventilation, and Air Conditioning (HVAC) systems in vehicles.

To learn more about this report, Request Free Sample

The Automotive Heat Exchanger Market plays a critical role in the functioning of vehicles by regulating temperature and ensuring optimal performance. In this comprehensive analysis, we will explore the dynamics, trends, key players, and future prospects of the automotive heat exchanger market.

Market Overview

The Automotive Heat Exchanger Market has witnessed substantial growth due to several key factors:

Efficiency and Sustainability: The demand for more fuel-efficient and eco-friendly vehicles has led to increased adoption of heat exchangers to manage engine and cabin temperatures.

Technological Advancements: Ongoing research and development efforts have resulted in advanced heat exchanger designs that offer improved performance and durability.

Increasing Vehicle Production: The automotive industry's growth, particularly in emerging markets, has driven the demand for heat exchangers as integral components of vehicles.

Electric and Hybrid Vehicles: With the rise of electric and hybrid vehicles, cooling systems are crucial, further boosting the heat exchanger market.

Market Segmentation

To gain a deeper understanding of the Automotive Heat Exchanger Market, we can segment it in various ways:

Type of Heat Exchangers: Market offerings include air-to-air, air-to-liquid, and liquid-to-liquid heat exchangers, each catering to specific vehicle cooling needs.

Vehicle Types: Heat exchangers are used in a wide range of vehicles, from passenger cars to heavy-duty trucks and buses.

Material and Technology: The market features a variety of materials and technologies, including aluminum, copper, and various heat exchanger designs, reflecting diverse industry needs.

Geographical Regions: Market dynamics can vary by region, with North America, Europe, Asia-Pacific, and other regions exhibiting different growth patterns.

Key Market Players

Several companies have established themselves as leaders in the Automotive Heat Exchanger Market:

Denso Corporation: Denso is a global leader in automotive components, offering a wide range of heat exchangers for various vehicle applications.

Valeo: Valeo specializes in automotive technology and thermal solutions, including heat exchangers for enhanced vehicle performance.

Mahle: Mahle is known for its innovative thermal management solutions, providing heat exchangers designed for efficiency and sustainability.

Modine Manufacturing Company: Modine manufactures heat exchangers for diverse industries, including automotive, with a focus on advanced technology and quality.

Market Trends

Understanding current market trends is crucial for stakeholders in the Automotive Heat Exchanger Market:

Weight Reduction: Lightweight heat exchanger designs, often using aluminum, are gaining traction to reduce the overall weight of vehicles and enhance fuel efficiency.

Compact and Efficient Designs: Heat exchangers are becoming more compact and efficient, optimizing their integration within modern vehicle layouts.

Electric Vehicle (EV) Adaptation: With the growth of EVs, heat exchangers for battery cooling and cabin temperature management are evolving rapidly.

Sustainability: The emphasis on sustainability is driving the development of eco-friendly materials and manufacturing processes in heat exchanger production.

Future Prospects

The Automotive Heat Exchanger Market's future holds several promising opportunities:

Electric Vehicle Growth: The rise of electric vehicles will lead to increased demand for heat exchangers for battery and system cooling.

Advanced Materials: Continued research will lead to the development of advanced materials with improved thermal conductivity and sustainability.

Enhanced Performance: Heat exchangers will continue to evolve to meet the increasing demands of vehicle efficiency and performance.

Global Expansion: Emerging markets will play a significant role in the expansion of the Automotive Heat Exchanger Market, as vehicle production surges in these regions.

In conclusion, the Automotive Heat Exchanger Market is instrumental in ensuring the efficient operation of vehicles, with a focus on sustainability and advanced technology. As the automotive industry continues to evolve, heat exchangers will play a vital role in enhancing vehicle performance and reducing environmental impact.

For more detailed information and insights, Explore the Sample Report PDF

About Technavio

Technavio is a leading global technology research and advisory company. Their research and analysis focus on emerging market trends and provide actionable insights to help businesses identify market opportunities and develop effective strategies to optimize their market positions. With over 500 specialized analysts, Technavio's report library consists of more than 17,000 reports and counting, covering 800 technologies, spanning 50 countries. Their client base consists of enterprises of all sizes, including more than 100 Fortune 500 companies. This growing client base relies on Technavio's comprehensive coverage, extensive research, and actionable market insights to identify opportunities in existing and potential markets and assess their competitive positions within changing market scenarios.

Contacts

Technavio Research Jesse Maida Media & Marketing Executive US: +1 844 364 1100 UK: +44 203 893 3200 Email: [email protected] Website: www.technavio.com

#Automotive Heat Exchanger Market Size#Automotive Heat Exchanger Marketshare#Automotive Heat Exchanger Market growth

0 notes

Text

Green Hydrogen Market — Forecast(2024–2030)

Green Hydrogen market size is forecasted to reach US$2.4 billion by 2027, after growing at a CAGR of 14.1% during the forecast period 2022–2027. Green Hydrogen is produced using low-carbon or renewable energy sources, such as solid oxide electrolysis, alkaline electrolysis and proton exchange membrane electrolysis. When compared to grey hydrogen, which is made by steam reforming natural gas and accounts for the majority of the hydrogen market, green hydrogen has significantly lower carbon emissions. Due to its capacity to lower carbon emissions, green hydrogen has recently been in high demand. Since it is a renewable energy source, its use is anticipated to rise in the coming years. The demand for the green hydrogen industry is expected to grow as public awareness of hydrogen’s potential as an energy source increases. Additionally, because hydrogen fuel is highly combustible, it has the potential to displace fossil fuels as a source of carbon-free or low-carbon energy, which is anticipated to support the growth of the green hydrogen industry during the forecast period. The novel coronavirus pandemic had negative consequences in a variety of green hydrogen end-use industries. The production halt owing to enforced lockdown in various regions resulted in decreased supply, demand and consumption of green hydrogen, which had a direct impact on the Green Hydrogen market size in the year 2020.

Request sample

Green Hydrogen Market Report Coverage

The “Green Hydrogen Market Report — Forecast (2022–2027)” by IndustryARC, covers an in-depth analysis of the following segments in the Green Hydrogen industry.

By Technology: Proton Exchange Membrane Electrolyzer, Alkaline Electrolyzer, Solid Oxide Electrolyzer

By Renewable Source: Wind Energy and Solar Energy

By Application: Energy Storage, Fuels, Fertilizers, Off-grid Power, Heating and Others

By End-Use Industry: Transportation [Automotive (Passenger Vehicles, Light Commercial Vehicles and Heavy Commercial Vehicles), Aerospace, Marine and Locomotive], Power Generation, Steel Industry, Food & Beverages, Chemical & Petrochemical (Ammonia, Methanol, Oil Refining and Others) and Others

By Country: North America (USA, Canada and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Belgium and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile and Rest of South America), Rest of the World (Middle East and Africa)

Key Takeaways

Europe dominates the Green Hydrogen market, owing to the growing base of green hydrogen manufacturing plants in the region. Europe has been taking steps to generate clean energy from green hydrogen to reduce carbon emission, which is the major factor for expanding European green hydrogen manufacturing plants.

The market is expanding due to the rise in environmental concerns, which also emphasizes the need for clean/renewable energy production to lower emission levels. Additionally, the industry for green hydrogen is expanding owing to the increased use of nuclear power and green hydrogen.

However, the primary factors limiting the growth of the green hydrogen market are the initial investment requirements for installing hydrogen infrastructure as well as prohibitive maintenance costs.

Green Hydrogen Market Segment Analysis — By Technology

The alkaline electrolyzer segment held the largest share in the Green Hydrogen market share in 2021 and is forecasted to grow at a CAGR of 13.8% during the forecast period 2022–2027, owing to its higher operating time capacity and low capital cost. Alkaline electrolyzers work by generating hydrogen on the cathode side and transporting hydroxide ions (OH-) through the electrolyte from the cathode to the anode. The alkaline electrolyzer primarily benefits from three factors. As it produces hydrogen with relatively high purity and emits no pollutants during the production process, it is firstly a green and environmentally friendly device. Second, flexibility in production. The production of hydrogen by alkaline water electrolysis has greater advantages in large-scale applications with solar power and wind power converted into hydrogen energy storage. It is available for large-scale distributed generation applications, in particular in the current large-scale productions with alkaline electrolytic water. Thirdly, alkaline electrolyzer electrodes, cells and membranes are comparatively inexpensive with high efficiency and long-term stability. These characteristics and precious metal-free electrodes enable the green hydrogen production by alkaline water electrolysis a promising technology for green hydrogen production, thereby significantly contributing to segment growth.

Green Hydrogen Market Segment Analysis — By End-Use Industry

The chemical & petrochemical segment held a significant share in the Green Hydrogen market share in 2021 and is forecasted to grow at a CAGR of 14.5% during the forecast period 2022–2027. Green hydrogen is often used in the chemical & petrochemical industry to manufacture ammonia, methanol, petroleum products, including gasoline and diesel and more. Integrated refinery and petrochemical operations use huge volumes of green hydrogen to desulfurize the fuels they produce. Using green hydrogen to produce ammonia, methanol, gasoline and diesel, could help countries gain self-sufficiency in a vital chemical manufacturing sector, hence, companies are increasingly using green hydrogen in the industry. The chemical & petrochemical industry is projected to grow in various countries, for instance, according to Invest India, the market size of the Chemicals & Petrochemicals sector in India is around US$178 billion and is expected to grow to US$300 billion by 2025. This is directly supporting the Green Hydrogen market size in the chemical & petrochemical industry.

Green Hydrogen Market Segment Analysis — By Geography

Europe held the largest share in the Green Hydrogen market share in 2021 and is forecasted to grow at a CAGR of 14.3% during the forecast period 2022–2027, owing to the bolstering growth of the chemical & petrochemical sector in Europe. The European chemical & petrochemical industry is growing, for instance, according to the European Chemical Industry Council (Cefic), The 10.7 percent increase in manufacturing output in the EU27 during the first three quarters of 2021 is indicated by the January-Sep 2021 data as a sign that chemical output is returning to the pre-COVID19 pandemic levels. After the COVID-19 outbreak, the EU27’s chemical output increased by 7.0 percent between the first three quarters of 2021 and the same period in 2020. About 3% more chemicals were produced in 2021 than there were before the pandemic (Jan-Sep-2019). In 2022, it is anticipated that EU27 chemical output will increase by +2.5 percent. Over the forecast period, the growth of the green hydrogen industry in Europe is being directly supported by the rising production of chemicals and petrochemicals. Numerous green hydrogen projects are also expected to start in Europe. For instance, a 500MW green hydrogen facility, one of Europe’s largest single-site renewable H2 projects, is planned for construction at the Portuguese port of Sines by 2025. Germany invested $1 billion in a funding plan to support green hydrogen in December 2021 as the new government aims to increase investment in climate protection. such green hydrogen projects in the area are projected to further support the European green hydrogen market size over the coming years.

BUY Now

Green Hydrogen Market Drivers

Increasing Investments in Establishing Green Hydrogen Plants:

Governments from several industrialized nations are stepping up efforts to build green hydrogen infrastructure. Infrastructure growth will enable producers to increase their capacity and reach, which will help them lower the cost of green hydrogen. For the development of an ecosystem that accepts green hydrogen as an alternative fuel, the participation of the governments of the respective countries is extremely important. Oil India Limited (OIL), a major player in exploration and production, officially opened “India’s first 99.999 percent pure” green hydrogen plant in Assam in April 2022. The installed capacity of the solar-powered pump station is 10 kg of hydrogen per day. The UK Government first announced plans to create a hydrogen village by 2025 and a hydrogen neighborhood by 2023 in November 2020 as part of the Ten-Point Plan for a Green Industrial Revolution. The UK government announced in April 2022 that it would establish a hydrogen village by the year 2025, the same day that First Hydrogen unveiled its selection of four English locations for green hydrogen production projects. Berlin’s H2Global initiative, which provides a path to market for sizable renewable hydrogen facilities worldwide, is approved by the European Commission in December 2021. The European Commission has approved a €900 million (US$1 billion) plan to subsidize the production of green hydrogen in non-EU nations for import into Germany under EU state aid regulations. The development of such infrastructure is facilitating the manufacturers to expand their reach and capacity, which will assist them in expanding the manufacturing base, thereby driving the market expansion.

Bolstering Demand for Green Hydrogen from Transportation Sector:

The world is getting ready to change the way it moves as it moves toward net zero-emission goals. Vehicles that use hydrogen directly in fuel cells or internal combustion engines are being developed by the transportation sector. Vehicles powered by hydrogen have already been created and are being used in a few sectors in Europe, Asia and North America. A prime example is the Toyota Mirai, a green hydrogen-based advanced fuel cell electric vehicle (FCEV) that was introduced by Indian Union Minister Nitin Gadkari in March 2022. This project is a first of its kind in India and aims to develop a market for such vehicles. It is one of the best zero-emission options and is powered by hydrogen. In August 2021, Small forklifts powered by hydrogen fuel cells will be developed, according to a plan unveiled by Hyundai Construction Equipment Co. By 2023, the Hyundai Genuine Co. subsidiary and S-Fuelcell Co., a local manufacturer of hydrogen fuel cells, plan to commercialize the 1–3 tonne forklifts. The U.K.-based startup Tevva debuted a hydrogen-electric heavy goods vehicle in July 2022, becoming the most recent business to enter a market where multinational corporations like Daimler Truck and Volvo are showing interest. The hydrogen tanks will need to be refilled in 10 minutes and it will take five to six hours to fully charge the battery. The first hydrogen-electric truck produced by the company weighs 7.5 tonnes, with later versions expected to weigh 12 and 19 tonnes. The countries are planning to more than double the number of such hydrogen-based vehicles in the future, which is anticipated to be a driver for the green hydrogen market during the forecast period.

Green Hydrogen Market Challenges

High Initial Cost of Green Hydrogen:

The initial costs associated with producing green hydrogen are very high and the inability to transport and store it adds to the material’s cost. Hydrogen energy storage is a pricey process when compared to other fossil fuels. In processes like liquefaction, liquid hydrogen is used as an energy carrier because it has a higher density than gaseous hydrogen. The mechanical plant used in this mode of operation has a very intricate working and functioning system. Thus, this raises overall expenses. While transporting green hydrogen presents additional economic and safety challenges, the fixed cost necessary to set up the production plant is only half the challenge. According to the Columbia Climate School, the issue is that green hydrogen is currently three times more expensive in the United States than natural gas. Additionally, the cost of electrolysis makes producing green hydrogen much more expensive than producing grey or blue hydrogen, even though the cost of electrolyzers is decreasing as production increases. Gray hydrogen currently costs about €1.50 ($1.84) per kilogram, blue hydrogen costs between €2 and €3 and green hydrogen costs between €3.50 and €6 per kilogram. As a result, the high initial cost of green hydrogen is expected to be one of the major factors limiting the Green Hydrogen market growth.

0 notes

Text

Liquid Cooling Systems Market Size, Share, Trends, Opportunities, Key Drivers and Growth Prospectus

"Global Liquid Cooling Systems Market – Industry Trends and Forecast to 2028

Global Liquid Cooling Systems Market, By Type (Liquid Heat Exchanger Systems, Compressor-Based Systems), End-Use Industry (Healthcare, Analytical Equipment, Industrial, Data Centers, Telecommunications, Automotive, Military), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028.

Access Full 350 Pages PDF Report @

**Segments**

- **Type**: The liquid cooling systems market can be segmented based on type into open loop systems and closed loop systems. Open loop systems are more customizable and offer better performance but require more maintenance. On the other hand, closed loop systems are more user-friendly and require less maintenance.

- **End-User**: The market can also be segmented by end-user, with key sectors being data centers, gaming PCs, industrial applications, and servers. Data centers are a major end-user due to the increasing demand for efficient cooling solutions to manage high-density servers. Gaming PCs are another significant segment as gamers look for ways to enhance performance and reduce overheating. Industrial applications and servers also drive the demand for liquid cooling systems for optimal functioning.

- **Region**: Geographically, the market can be segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America and Europe are the leading regions in terms of market share due to the presence of key gaming and data center industries. Asia Pacific is experiencing rapid growth in the liquid cooling systems market, driven by the increasing adoption of advanced cooling technologies in emerging economies like China and India.

**Market Players**

- **Corsair Components, Inc.**: Corsair is a prominent player in the liquid cooling systems market, offering a diverse range of high-performance cooling solutions for gaming PCs and enthusiasts. Their products are known for their reliability and efficiency in managing heat dissipation.

- **Asetek**: Asetek is a leading provider of liquid cooling solutions for data centers and servers. They offer innovative technology that helps in reducing energy consumption and improving overall cooling efficiency in large-scale applications.

- **CoolIT Systems, Inc.**: CoolIT specializes in liquid cooling solutions for high-performance computing and server applications. Their advanced cooling systems are designed to optimize thermal performance and enhance the overall reliability of the systems.

- **NZXT Corporation**: NZXT offers a range of liquid cooling solutions for gaming PCs and enthusiasts. Their products areknown for their sleek design and high-quality performance, catering to the needs of gamers and PC enthusiasts looking for efficient cooling solutions while maintaining aesthetics.

- **Thermaltake Technology Co., Ltd.**: Thermaltake is a well-established player in the liquid cooling systems market, offering a wide range of innovative cooling solutions for gaming PCs and industrial applications. Their products are highly regarded for their durability and advanced features, attracting a loyal customer base globally.

- **Antec Inc.**: Antec is a trusted name in the liquid cooling systems industry, known for its reliable and cost-effective cooling solutions. They cater to a wide range of customers, including gamers, data centers, and industrial sectors, with products that focus on performance and energy efficiency.

- **EVGA Corporation**: EVGA is a key player in the liquid cooling systems market, specializing in high-performance cooling solutions for gaming PCs and enthusiasts. Their products are designed to deliver superior thermal performance and enhance the overall gaming experience for users.

- **Deepcool Industries Ltd.**: Deepcool is a leading manufacturer of liquid cooling systems, offering an extensive range of cooling solutions for various applications. Their products are known for their innovative designs and optimal cooling performance, meeting the demands of both casual users and professionals.

**Market Trends and Growth Drivers**

The liquid cooling systems market is experiencing significant growth worldwide, driven by several key trends and growth drivers. One of the primary factors fueling market expansion is the increasing demand for high-performance cooling solutions in data centers and gaming PCs. With the rising trend of overclocking and high-density computing, there is a growing need for efficient thermal management solutions to prevent overheating and ensure optimal performance.

Another major trend shaping the market is the continuous innovation and technological advancements in liquid cooling systems. Companies are investing in research and development to introduce more advanced cooling solutions with improved efficiency, reliability, and sustainability. This focus on innovation is not only enhancing the performance of liquid cooling systems but also driving customer preference towards more advanced and feature-rich products.

**Segments**

- **Type**: The liquid cooling systems market can be further segmented into liquid heat exchanger systems and compressor-based systems. Liquid heat exchanger systems utilize a heat exchanger to transfer heat from the liquid to another fluid or air, providing efficient cooling solutions. On the other hand, compressor-based systems use a compressor to circulate the cooling liquid, offering effective cooling for various applications.

- **End-Use Industry**: The market can also be segmented by end-use industry, including healthcare, analytical equipment, industrial sector, data centers, telecommunications, automotive industry, and military applications. The healthcare industry requires precise temperature control for medical equipment, while analytical equipment relies on cooling systems for accurate measurements. The industrial sector utilizes liquid cooling for machinery and equipment, and data centers demand efficient cooling solutions for high-density servers. Telecommunications, automotive, and military sectors also rely on liquid cooling for optimal performance.

- **Country**: The global liquid cooling systems market can be analyzed based on country-specific segments, including the U.S., Canada, Mexico, Brazil, Argentina, Germany, Italy, U.K., France, Spain, Japan, China, India, South Korea, Australia, Saudi Arabia, U.A.E, South Africa, and more. Each country segment may have unique market dynamics, regulatory frameworks, and technological advancements influencing the adoption of liquid cooling systems in various industries.

Global Liquid Cooling Systems Market, By Type (Liquid Heat Exchanger Systems, Compressor-Based Systems), End-Use Industry (

Core Objective of Liquid Cooling Systems Market:

Every firm in the Liquid Cooling Systems Market has objectives but this market research report focus on the crucial objectives, so you can analysis about competition, future market, new products, and informative data that can raise your sales volume exponentially.

Size of the Liquid Cooling Systems Market and growth rate factors.

Important changes in the future Liquid Cooling Systems Market.

Top worldwide competitors of the Market.

Scope and product outlook of Liquid Cooling Systems Market.

Developing regions with potential growth in the future.

Tough Challenges and risk faced in Market.

Global Liquid Cooling Systems top manufacturers profile and sales statistics.

Key takeaways from the Liquid Cooling Systems Market report:

Detailed considerate of Liquid Cooling Systems Market-particular drivers, Trends, constraints, Restraints, Opportunities and major micro markets.

Comprehensive valuation of all prospects and threat in the

In depth study of industry strategies for growth of the Liquid Cooling Systems Market-leading players.

Liquid Cooling Systems Market latest innovations and major procedures.

Favorable dip inside Vigorous high-tech and market latest trends remarkable the Market.

Conclusive study about the growth conspiracy of Liquid Cooling Systems Market for forthcoming years.

Frequently Asked Questions

What is the Future Market Value for Liquid Cooling Systems Market?

What is the Growth Rate of the Liquid Cooling Systems Market?

What are the Major Companies Operating in the Liquid Cooling Systems Market?

Which Countries Data is covered in the Liquid Cooling Systems Market?

What are the Main Data Pointers Covered in Liquid Cooling Systems Market Report?

Browse Trending Reports:

Recreational Cannabis Market Paediatric Gliomas Drugs Market Zinc Glycinates Market Restriction Endonucleases Products Market Food Grade Gases In Meat And Seafood Application Market Temperature Smart Roads Market Automotive Airbag Silicone Market Non Networked Sound Masking System Market Nitrile Butadiene Rubber Br Market Big Data As a Service Bdaas Market Robotically Assisted Surgical Devices Market Transactional Video Demand Market Rice Transplanter Market Bio Based Polyethylene Terephthalate Pet Packaging Market Bath Mats Market Synthetic Iron Oxide Pigments Market Polyvalent Anti Venom Market Managed Siem And Log Management Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Metal Strips Market is valued at USD million and is projected to grow at a compound annual growth rate (CAGR) of 3.99% over the forecast period, reaching approximately USD 221,263.68 million by 2032. The global metal strips market is an integral part of the industrial economy, supplying essential raw materials to sectors like automotive, construction, electronics, aerospace, and packaging. Metal strips, typically produced from steel, copper, aluminum, and other alloys, serve diverse applications due to their excellent mechanical properties, such as durability, malleability, and resistance to wear and corrosion.

Browse the full report at https://www.credenceresearch.com/report/metal-strips-market

Market Overview

Metal strips refer to thin, flat pieces of metal that can be further processed into different forms, such as sheets, coils, or foils. These strips are widely used in various industries for different applications, including:

1. Automotive Industry: Metal strips are critical for manufacturing automotive components, such as body panels, engine parts, and electrical wiring. 2. Construction Sector: In construction, metal strips are used for roofing, structural reinforcements, and electrical wiring. 3. Electronics Industry: Metal strips made from copper and aluminum are widely used for electrical contacts, connectors, and heat sinks in electronic devices. 4. Packaging Industry: Aluminum strips are common in food and beverage packaging due to their lightweight, non-corrosive, and recyclable properties.

Key Growth Drivers

Several factors are driving the demand for metal strips globally:

1. Growing Construction Activities

Rapid urbanization and industrialization across emerging economies, particularly in Asia-Pacific and Latin America, are boosting the demand for metal strips in construction. The need for robust infrastructure, such as bridges, railways, airports, and commercial buildings, has led to increased consumption of steel and aluminum strips for structural purposes.

2. Expanding Automotive Industry

The global automotive industry is a significant consumer of metal strips. With the rising demand for electric vehicles (EVs) and lightweight materials in conventional vehicles, manufacturers are increasingly using aluminum strips to improve vehicle efficiency. Lightweight metals help reduce vehicle weight, enhancing fuel economy and minimizing carbon emissions.

3. Technological Advancements in Electronics

The proliferation of consumer electronics, smart devices, and advancements in communication technology are driving the demand for copper and aluminum strips. These materials play a critical role in electronic circuitry, connectors, and power distribution systems. The shift towards miniaturization of electronic components has also increased the need for high-precision metal strips in semiconductor and microchip production.

4. Sustainability and Recycling Initiatives

As environmental concerns grow, the recycling of metals has become a key focus for industries. Metal strips, particularly aluminum, are highly recyclable, contributing to the circular economy. Recycling metal strips significantly reduces energy consumption and greenhouse gas emissions compared to the production of virgin metals, making it an eco-friendly solution for industries aiming for sustainability.

Challenges Facing the Metal Strips Market

Despite its growth, the global metal strips market faces several challenges:

1. Volatility in Raw Material Prices

The prices of metals such as steel, aluminum, and copper are highly volatile and subject to fluctuations due to factors like geopolitical tensions, changes in supply and demand, and currency exchange rates. This volatility poses a risk to manufacturers, as it affects profit margins and pricing strategies.

2. Trade Regulations and Tariffs

The global metal strips market is affected by trade policies, tariffs, and import-export regulations. Trade wars, such as those between major economies like the US and China, have impacted the metal industry by imposing tariffs on raw materials. These trade barriers can disrupt supply chains and increase production costs for manufacturers.

3. Competition from Alternative Materials

The growing trend of using alternative materials, such as composites and polymers, in sectors like automotive and aerospace, poses a challenge to the metal strips market. These materials offer similar strength and durability but are often lighter and more resistant to corrosion, reducing the demand for traditional metal strips.

Future Outlook

The global metal strips market is poised for steady growth in the coming years, driven by:

- Technological Advancements: Innovations in metallurgy and processing techniques will continue to enhance the quality and performance of metal strips, enabling them to meet the evolving demands of industries. - Sustainability Trends: As industries focus on reducing their carbon footprint, the demand for recyclable and energy-efficient metal strips will increase. - Electric Vehicle (EV) Boom: The rapid adoption of EVs worldwide will drive the demand for lightweight metal strips, particularly aluminum, in battery casings, electrical components, and structural parts.

According to market analysts, the global metal strips market is expected to grow at a **compound annual growth rate (CAGR) of around 5%** during the forecast period (2023-2030), with Asia-Pacific leading the market due to its booming industrial and automotive sectors.

Key Player Analysis:

United States Steel Corporation (United States)

Nucor Corporation (United States)

ThyssenKrupp AG (Germany)

ArcelorMittal S.A. (Luxembourg)

Nippon Steel & Sumitomo Metal Corporation (Japan)

BlueScope Steel Limited (Australia)

JFE Steel Corporation (Japan)

Shandong Iron and Steel Group (China)

JSW Steel Ltd (India)

Hyundai Steel Co., Ltd (South Korea)

Posco Co., Ltd (South Korea)

Tata Steel Ltd (India)

Valin Xiangtan Iron and Steel Co Ltd (China)

Baotou Iron & Steel (Group) Co., Ltd (China)

Segmentation:

Based on Product Type:

Aluminum Strips

Copper Strips

Steel Strips

Brass Strips

Other Metal Strips

Based on Technology:

Cold Rolling

Hot Rolling

Alloying

Coating Technologies

Others

Based on End User:

Automotive

Construction

Electronics

Aerospace

Manufacturing

Other Industries

Based on Region:

North America (United States, Canada, Mexico)

Europe (Germany, France, United Kingdom, Italy, Spain)

Asia-Pacific (China, India, Japan, South Korea, Australia)

Latin America (Brazil, Argentina, Chile)

Middle East and Africa (Saudi Arabia, UAE, South Africa, Egypt)

Browse the full report at https://www.credenceresearch.com/report/metal-strips-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Refrigerant Oil Market - Forecast(2024 - 2030)

Overview

The Refrigerant Oil Market size is forecast to reach USD $1.6 billion by 2030, after growing at a CAGR of 4.3% during the forecast period 2024-2030. Refrigerant Oil is a high-temperature formulation of a mixture of oil and additives devised for usage in cooling systems. It acts as a lubricant in refrigeration compressors, derived from both mineral and synthetic oil in order to lubricate or reduce friction of metal parts and wear on the compressor. The product flows under high pressure to turn from liquid to vapor state to generate a cooling effect due to its special characteristics such as better chemical and thermal stability, low contamination, low pour point, high dielectric strength and viscosity. Global environmental regulations, such as the Montreal Protocol and subsequent amendments like the Kigali Amendment, are driving the phase-out of high-GWP refrigerants like hydrofluorocarbons (HFCs). This shift is propelled by the need to curb greenhouse gas emissions and combat climate change. Low-GWP refrigerants, including hydrocarbons, natural refrigerants (like ammonia and CO2), and hydrofluoroolefins (HFOs), are gaining prominence due to their significantly reduced impact on global warming compared to their predecessors. The HVACR (Heating, Ventilation, Air Conditioning, and Refrigeration) sector is witnessing consistent growth globally, driven by urbanization, industrialization, and an increasing focus on indoor comfort and air quality. HVACR systems, including air conditioning units, heat pumps, and refrigeration equipment, rely on Refrigerant Oils for effective operation and lubrication of components like compressors, motors, and heat exchangers. Commercial buildings, industries, hospitals, and data centers require sophisticated HVACR systems for temperature control, preservation of goods, and maintaining optimal working environments.

Report Coverage

The report “Refrigerant Oil Market– Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Refrigerant Oil Market. By Type of Oil: Mineral Oil, Synthetic Oil and Others. By Refrigerant Type: Chlorofluorocarbon (CFC), Hydro-chlorofluorocarbon (HCFC), Hydrofluorocarbon (HFC), Ammonia, HFO, Butane and Iso Butane, Propane and Others By Application: Refrigerator & Freezer, Air conditioners, Automotive AC System, Aftermarket and Others By Geography: North America, South America, Europe, APAC, and RoW.

Request Sample

Key Takeaways

Asia Pacific region is expected to maintain its dominance during the forecast period.

The key factor driving the growth of the global Refrigerant Oil market is the increasing consumption of frozen and packaged food products.

Refrigerant Oil exhibits high viscosity, low pour point, and is contamination-free due to which the market is expected to grow during the forecast period.

By Type of Oil - Segment Analysis

Synthetic Oil segment held a significant share in Refrigerant Oil market in 2023. This dominance is attributed to its high performance in extreme conditions, superior viscosity index, high shear stability, and enhanced chemical resistance in comparison to mineral oil. Additionally, synthetic oil lasts longer and is compatible with low GWP and modern refrigerants such as NH3, HFO, and CO2. The growth is attributed to the increasing demand for POE and PGA in ammonia and CO2 refrigeration systems. On the other hand, the mineral oil offers more benefits over the synthetic oil, which leads to its use as a thermal fluid in mechanical and industrial applications.

Inquiry Before Buying

By Application - Segment Analysis

Building Refrigerator & Freezer segment held a significant share in Refrigerant Oil market in 2023 growing at a CAGR of 4.5% during the forecast period. This growth is attributed to the growing demand for perishable food products due to the changing lifestyle of people in developed and developing regions and growth in trade of food products. The rising sales of refrigerators & freezers are anticipated to drive the growth of the market over the forecast period. Compressor Oil is designed to provide long service life in most compressor applications. Moreover, air conditioners segment is expected to have a significant growth during the forecast period due to installation of air conditioners in vehicles, residences, centralized systems in offices and in industries. However, consumer electronics companies plan to increase prices of refrigerators, air-conditioners, microwave ovens and washing machines due to higher component prices amid short supplies from coronavirus-hit China.

By Geography - Segment Analysis

Asia Pacific dominated the Refrigerant Oil market with a share of more than 32%, followed by North America and Europe. The increasing population in the region and the rising demand for refrigerators, freezers, air conditioners, and automobiles in the emerging markets of APAC, such as China and India, are some of the major factors projected to drive the demand for Refrigerant Oil in the region. Furthermore, the improving lifestyle, increasing employment rate, rising disposable income of the people, and mounting foreign investments in various sectors of the economy are some of the other factors that make APAC an attractive market for Refrigerant Oil manufacturers.

Schedule a Call

Drivers – Refrigerant Oil Market

Growing Demand for Environmentally Friendly Oils

Stringent EU Consumer and industry preferences are increasingly inclined towards sustainable and eco-friendly products. This extends to refrigeration systems where there's a growing preference for oils derived from renewable sources or with minimal environmental impact. Manufacturers are responding to this demand by developing Refrigerant Oils derived from bio-based or synthetic sources that offer lower GWP, reduced toxicity, and improved biodegradability. Many industries are incorporating sustainability into their operational strategies. This includes using Refrigerant Oils that align with their sustainability commitments and promote environmentally responsible practices.

Cold chain logistics have sparked an interest in refrigeration equipment and in turn Refrigerant Oil

Changing food habits coupled with spending capacity have resulted in a number of licensed and franchised stores of limited services restaurants such as McDonald’s and Subway, KFC and local services and is driving demand for frozen and chilled food products. Moreover, storage of medical products (such as vaccines, other medical products, etc.) is expected to increase demand for refrigeration systems. Hence, it is expected to increase installation of refrigeration equipment in warehouses as well as in vehicles for distribution.

Challenges – Refrigerant Oil Market

Inadequate Source: Expert Insights & IndustryARC Analysis

Stringent regulations Various government organizations are trying to enforce amendments over the industries to reduce the use of HCFCs and CFCs in refrigeration system until 2030 by A5 countries in order to identify such refrigerants as obsolete. Thus, stringent government regulations are expected to hinder the Refrigerant Oil market. Moreover, ammonia is not compatible with copper, so it cannot be used in any system with copper pipes. Release of ammonia due to excess water within the system freezing, causes broken pipes and equipment.

Buy Now

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Refrigerant Oil market. in 2023, The major players in the Refrigerant Oil market are Exxon Mobil Corporation, Shell PLC, FUCHS, Idemitsu Kosan Co. Ltd, Petronas International Limited, BP p.l.c., Sinopec Group, Johnson Controls, Japan Sun Oil Company, Ltd., Isel Inc. and Others.

Developments:

In August 2023, The Japanese lubricating oil manufacturer Sun Oil Co. launched a mineral Refrigerant Oil that works with most refrigerants.

In September 2022, Tata Motors announced the launch of the 5W30 synthetic engine oil, which is specifically intended to enhance the performance of the BS6 diesel engines.

#refrigerant oil market#refrigerant oil market size#refrigerant oil market share#refrigerant oil market report#refrigerant oil market analysis#refrigerant oil market research#refrigerant oil market forecast#Polyolester oil#Polyalkylene glycol#Polyvinyl Ether Oil

0 notes

Text

Copper Components Suppliers in India

Copper components are widely used in various industries due to their excellent electrical and thermal conductivity, durability, and corrosion resistance. One of the leading suppliers of high-quality copper components in India is Nexim Alloys, a company known for its superior products, exceptional service, and commitment to meeting industry standards.

Why Copper Components Are Essential

Copper’s unique properties make it the material of choice for a wide range of applications. Some of the key benefits of copper include:

Excellent Electrical Conductivity: Copper is second only to silver in electrical conductivity, making it ideal for electrical components like wires, connectors, and busbars.

Thermal Conductivity: Its high thermal conductivity ensures that copper components effectively manage heat, which is vital for cooling systems, heat exchangers, and electronic devices.

Corrosion Resistance: Copper naturally resists corrosion, which extends the life of components in various environments, including marine and industrial settings.

Nexim Alloys: Leading Copper Components Supplier

Nexim Alloys is most renowned manufacturers, stockists, supplier & exporter of Copper Components. These Components consists of features like high ductility, highly durable, wear & tear resistant, long lasting strength, corrosion & abrasion resistant, good conductor of heat & electricity good conductor of thermal energy etc. These Components are manufactured using best quality raw material & do match national & International quality standard and this helps us to have high demand in the market from our customers. The Copper Components are sold to customers at market friendly prices. When it comes to packaging it is done with tremendous care because we know the challenges faced while import & export of product hence we see through it that the products are delivered in good conditions without any harm to it. These Components are manufactured in different size, dimension & thickness and are delivered to customers as per their need & requirement.

Description:

Description:Forged Copper components

Material:Pure copper 99.9%

Process:Hot forging, CNC machining

Finish:Machined surface

Application:High/low voltage electrical conductor components

Conclusion

As one of the leading suppliers of copper components in India, Nexim Alloys has earned the trust of clients across various industries. Whether for electrical applications, construction, automotive, or telecommunications, Nexim provides high-quality copper products that meet the exacting standards of modern industries.

For More Information:

Visit: https://www.neximalloys.com/

Contact: +91- 8082302533

Email-Id: [email protected]

0 notes

Text

Heat Exchanger Market: Growth Trends, Innovations, and Future Outlook

1. Overview of the Global Heat Exchanger Market

Market Size and Growth Forecast: The Heat Exchanger Market is projected to be valued at USD 18.08 billion in 2024, with an expected growth to USD 28.26 billion by 2029, reflecting a robust compound annual growth rate (CAGR) of 9.34% over the forecast period (2024-2029). The rising energy demand and the need for energy-efficient systems are major factors driving this growth.

Key Types of Heat Exchangers: The market is categorized into several key types of heat exchangers, including shell and tube, plate and frame, air-cooled, double pipe, and others, each serving different industrial needs based on efficiency, cost, and operational requirements.

2. Key Market Drivers in the Heat Exchanger Industry

Energy Efficiency and Sustainability: Increasing emphasis on energy efficiency and sustainability, particularly in the HVAC, power generation, and petrochemical sectors, is driving the demand for advanced heat exchanger systems that reduce energy consumption and enhance operational efficiency.

Industrial Expansion: The growing industrialization in emerging economies such as India, China, and Brazil is fueling the demand for heat exchangers across sectors like oil & gas, power generation, and chemical processing. These industries rely heavily on heat exchangers to maintain optimal thermal performance and reduce operational costs.

Regulatory Pressures: Stringent environmental regulations are pushing industries to adopt heat exchangers that minimize emissions and waste heat. This has accelerated the development of green technologies and high-performance heat exchangers.

Technological Advancements: The advent of new materials, designs, and manufacturing technologies, such as additive manufacturing and corrosion-resistant alloys, is creating opportunities for more durable and efficient heat exchangers. These advancements help reduce maintenance costs and improve longevity, making them attractive to industries with high operational demands.

3. Emerging Trends in the Heat Exchanger Market

Compact Heat Exchangers: There is a growing demand for compact and modular heat exchangers, particularly in industries like automotive and HVAC. These exchangers offer higher efficiency in smaller spaces, making them ideal for applications where space is a constraint.

Integration of Advanced Materials: The use of corrosion-resistant materials such as titanium, stainless steel, and nickel alloys is increasing, particularly in industries dealing with harsh environments like offshore oil & gas and chemical processing. These materials enhance heat exchanger performance and durability.

Renewable Energy Integration: The integration of heat exchangers in renewable energy systems, such as solar power plants and geothermal energy, is a growing trend. Heat exchangers are essential in converting thermal energy from renewable sources into usable electricity, helping the world transition toward cleaner energy.

Smart Heat Exchangers: With the rise of Industry 4.0, there is an increasing focus on smart heat exchangers equipped with IoT and AI-based predictive maintenance systems. These technologies allow for real-time monitoring of exchanger performance, reducing the likelihood of failures and optimizing energy efficiency.

4. Industry-Specific Applications of Heat Exchangers

Power Generation: Heat exchangers are vital in thermal power plants, nuclear power plants, and renewable energy systems. The growing demand for energy globally is pushing for more efficient thermal management solutions in power generation.

Chemical Processing: In the chemical and petrochemical industries, heat exchangers play a key role in controlling temperatures during chemical reactions and maintaining the safety and efficiency of processes.

Oil & Gas: The oil & gas industry uses heat exchangers in various processes, such as liquefied natural gas (LNG) production, refining, and transportation. As oil companies aim to reduce operational costs and environmental impact, there is a growing need for energy-efficient heat exchangers.

HVAC & Refrigeration: The heating, ventilation, and air conditioning (HVAC) sector relies on heat exchangers to regulate indoor temperatures efficiently. The growing demand for energy-efficient buildings and sustainable solutions is driving innovation in this segment.

Automotive: The automotive industry is increasingly relying on lightweight, high-performance heat exchangers to manage engine temperatures, cool electric vehicle batteries, and improve fuel efficiency.

5. Regional Market Analysis

North America: The North American heat exchanger market is driven by rising energy demands and environmental regulations. The region is also a hub for technological innovation, with a strong focus on developing next-generation heat exchanger designs.

Europe: Europe is seeing a surge in demand for heat exchangers due to its focus on energy efficiency and renewable energy adoption. Countries like Germany, the UK, and France are at the forefront of integrating advanced heat exchanger technologies into their energy and manufacturing sectors.

Asia-Pacific: The Asia-Pacific region is expected to witness the highest growth in the heat exchanger market, driven by rapid industrialization, urbanization, and the increasing need for energy-efficient solutions in countries like China, India, and Japan.

Middle East & Africa: In the Middle East, the demand for heat exchangers is growing, particularly in the oil & gas and chemical sectors, due to ongoing investments in large-scale industrial projects. Similarly, Africa is seeing growth in the energy and mining sectors, spurring demand for efficient heat exchangers.

6. Challenges Facing the Heat Exchanger Industry

High Initial Costs: The initial costs of designing and installing advanced heat exchangers can be high, which can be a barrier for small and medium-sized enterprises (SMEs). However, long-term energy savings and operational efficiency often justify these investments.

Material Challenges: Despite advancements, the challenge of finding cost-effective materials that can withstand extreme temperatures and corrosive environments remains. Continuous R&D is needed to overcome this.

Maintenance and Downtime: Heat exchangers require regular maintenance to prevent fouling and scaling, which can reduce their efficiency. Innovations in self-cleaning or fouling-resistant designs are helping address these issues, but maintenance costs can still be significant for some industries.

7. Competitive Landscape

Key Players: The global heat exchanger market is highly competitive, with major players such as Alfa Laval, Danfoss, SPX Flow, Kelvion, Hisaka Works, and Xylem leading the industry. These companies are focusing on expanding their product portfolios, enhancing energy efficiency, and incorporating smart technologies to remain competitive.

Mergers & Acquisitions: Many leading players are engaging in strategic mergers and acquisitions to strengthen their market positions and expand their presence in emerging markets.

Innovation in Design: The heat exchanger industry is witnessing innovations in design, such as compact, plate-type heat exchangers and modular designs that offer higher efficiency, easier installation, and reduced maintenance requirements.

8. Future Outlook and Opportunities

Growing Demand for Green Technologies: As industries strive to reduce their carbon footprints, the demand for green technologies such as waste heat recovery systems and energy-efficient exchangers is expected to rise.

Expansion in Emerging Markets: Emerging economies in Asia-Pacific, Latin America, and Africa offer significant growth opportunities for the heat exchanger market, especially in sectors like power generation, HVAC, and industrial processing.

Focus on Innovation: Continuous R&D into new materials, compact designs, and smart technologies is expected to drive future growth, helping industries meet rising energy efficiency standards and environmental regulations.

Conclusion: The Heat Exchanger Market on the Rise

The heat exchanger market is at a critical juncture of growth, fueled by advancements in technology, the push for energy efficiency, and the need for better thermal management across industries. As the world increasingly focuses on sustainability and energy conservation, heat exchangers will continue to play a vital role in meeting industrial and environmental demands.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence.

#heat exchanger market size#heat exchanger market share#heat exchanger market analysis#heat exchanger market growth

0 notes

Link

0 notes

Text

0 notes

Text

Laser Cutting Machines Market - Changing Supply and Demand Scenarios By 2030

Laser Cutting Machines Industry Overview

The global laser cutting machines market size was valued at USD 6,832.8 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 5.5% from 2023 to 2030.

Over the forecast period, it is anticipated that the growing trend of automation in the manufacturing sector and the rising demand for the end-use industry will increase demand for laser cutting to support the laser cutting machine industry’s growth.

End-use industries such as automotive, electronics, packing, pharmaceuticals, HVAC, and others are increasingly using automated laser cutting machines. Additionally, the end-use sectors widely utilize these machines to produce high-quality goods efficiently. Manufacturers are now able to automate a variety of processes, including laser cutting, owing to the growing trend of automation. These tools produce and cut pieces and patterns precisely; the machines deliver uniform outcomes, due to reduced downtime and the need for energy efficiency, manufacturers are investing in the automation of laser cutting, thus driving the market growth.

Gather more insights about the market drivers, restrains and growth of the Laser Cutting Machines Market

The growth of the laser cutting machines market is driven by the rising adoption of industry 4.0 technologies such as automation, data analytics, and the Internet of Things (IoT) are assisting in maximizing the efficiency of laser cutting machinery due to the real-time information exchange that enables optimum output by enabling operators to monitor and manage their production processes. Manufacturers aim to improve operating cost-efficiency, decrease downtime, and enhance production.

Another factor supporting the market growth of laser cutting machines is expanding due to the increased human-machine connection provided by industry 4.0 solutions, which is enhancing quality, productivity, and energy efficiency. Additionally, the early notification of the machine operation status provided by predictive analysis is promoting manufacturers to invest in industry 4.0 solutions by significantly lowering maintenance and replacement costs. This is expected to propel the market growth.

The emergence of fiber laser cutting is further expected to support the market growth of laser-cutting machinery. Fiber laser cutting devices are frequently employed in macro-processing applications with millimeter-level precision, such as cutting and welding industrial metals. Given the high demand for laser equipment, the market potential for macro processing is greater than that for micro processing. Fiber lasers are frequently employed in macro processing, which is the processing of objects whose size and shape have a laser beam influence range of millimeters, due to their high output power.

Fiber laser cutting boosts advantages such as precise, high-quality cuts, improved process for micro cutting, and shaping structural steel, positioning them as the preferred choice among the manufacturers. Additionally, the traction of fiber laser cutting equipment is fueled by several key features, including their ergonomics, quick operation, and high power safety. Most of these machines employ pre-focused optical systems with suitable deflection lenses, improving focus accuracy, laser light transmission, and machine performance. Thus, the emergence of new cutting technologies is driving the market growth.

The high cost of laser-cutting machinery coupled with high power consumption is a major restraint hindering the market growth. The high cost of the machinery components, such as water tubes, laser generators, and laser lenses, and their overall maintenance cost is another factor that affects the growth. Furthermore, when heated at high temperatures, cutting polymers such as Polytetrafluoroethylene and other metals releases harmful gases such as phosgene gas. This is another disadvantage restraining the industry’s growth.

Browse through Grand View Research's Electronic Devices Industry Research Reports.

• The global laser printer market size was estimated at USD 9.62 billion in 2023 and is projected to grow at a CAGR of 5.1% from 2024 to 2030.

• The global power electronics market size was valued at USD 38.12 billion in 2023 and is projected to grow at a CAGR of 5.2% from 2024 to 2030.

Key Laser Cutting Machines Company Insights

The key market players include Alpha Laser GmbH; Amada Miyachi Co. Ltd; Bystronic Inc.; Coherent Inc.; and DPSS Laser Inc. Manufacturers are concentrating on implementing tactics like acquisitions, collaborations, and expansions in order to increase their position in the worldwide market.

Participants in the market are focusing on bolstering their position through a range of strategic initiatives, including the development of new products, joint ventures, partnerships, and mergers and acquisitions. R&D efforts are heavily prioritized by major market participants in order to develop cutting-edge products and expand their product portfolios. These players are also focusing on developing laser equipment that uses less power and is more effective.Some prominent players in the global laser cutting machines market include.

Alpha Laser GmbH

Amada Miyachi Co. Ltd

Bystronic Inc.

Coherent Inc.

DPSS Laser Inc.

Epilog Lasers Inc.

Fanuc Corporation

IPG Photonics Corporation

Jenoptik Laser GmbH

Kern Lasers System

Rofin-Sinar Technologies Inc.

Trumpf Laser GmbH + Co. Kg

Avid Identification Systems, Inc

Order a free sample PDF of the Laser Cutting Machines Market Intelligence Study, published by Grand View Research.

0 notes

Text

Steel Square Pipe Manufacturers In Mumbai

Stainless Steel Square Pipe Manufacturers In Mumbai,play a crucial role in the city's industrial landscape. These manufacturers are integral to supplying high-quality stainless steel square pipes that find extensive use in construction, architecture, and various industrial applications. Stainless steel is preferred for its durability, corrosion resistance, and aesthetic appeal, making it a versatile choice across industries.

316Ti Stainless Steel Pipe Manufacturers in Mumbai specialize in producing pipes made from 316Ti stainless steel, which is a titanium-stabilized version known for its enhanced resistance to corrosion, especially in aggressive environments. These manufacturers adhere to stringent quality standards to ensure their pipes meet the demanding requirements of industries such as pharmaceuticals, food processing, and chemical processing.

Additionally, Alloy Steel Pipe Manufacturers In Mumbai who cater to the growing demand for alloy steel pipes. Alloy steel offers superior mechanical properties, including strength and hardness, making it ideal for applications in oil and gas, power generation, and automotive sectors. These manufacturers leverage advanced metallurgical techniques to produce alloy steel pipes that withstand high temperatures, pressure, and corrosive substances.

The manufacturing processes employed by these companies in Mumbai incorporate cutting-edge technology and strict adherence to industry norms, ensuring consistent product quality. They offer a wide range of sizes, dimensions, and customizations to meet specific project requirements. Whether for structural frameworks, fluid transport systems, or heat exchangers, these manufacturers play a pivotal role in Mumbai's industrial ecosystem.

Moreover, Mumbai serves as a hub for stainless steel and alloy steel industries due to its strategic location, skilled workforce, and access to raw materials. The presence of these specialized manufacturers not only supports local infrastructure development but also contributes to India's position in the global steel market.

In conclusion, Stainless Steel Square Pipe Manufacturers in Mumbai, 316Ti Stainless Steel Pipe Manufacturers in Mumbai, and Alloy Steel Pipe Manufacturers in Mumbai collectively drive innovation and reliability in the production of steel pipes. Their commitment to quality and versatility underscores their importance in meeting diverse industrial needs both domestically and internationally.

0 notes

Text

Liquid Cooling Systems Market Size, Share, Trends, Growth Opportunities and Competitive Outlook

"Global Liquid Cooling Systems Market – Industry Trends and Forecast to 2028

Global Liquid Cooling Systems Market, By Type (Liquid Heat Exchanger Systems, Compressor-Based Systems), End-Use Industry (Healthcare, Analytical Equipment, Industrial, Data Centers, Telecommunications, Automotive, Military), Country (U.S., Canada, Mexico, Brazil, Argentina, Rest of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028.

Access Full 350 Pages PDF Report @

**Segments**

- On the basis of Type, the Liquid Cooling Systems Market is segmented into Closed Loop Systems and Open Loop Systems. Closed loop systems are efficient and easy to install, making them a popular choice for consumers. On the other hand, open-loop systems offer more customization options but may require more maintenance. - Based on Application, the market can be classified into Data Centers, Gaming PCs, Automotive, Healthcare, and Industrial. Data centers are the largest consumer of liquid cooling systems due to the need for efficient heat management in high-performance computing environments. The gaming PC segment is also witnessing significant growth as gamers look for ways to enhance the performance of their rigs. - According to Cooling Method, the market is divided into Liquid-to-Liquid Cooling and Direct-to-Chip Cooling. Liquid-to-liquid cooling involves transferring heat from one liquid to another, providing efficient cooling for high-power systems. Direct-to-chip cooling, on the other hand, involves circulating coolant inside the chip package to manage heat at the source.

**Market Players**

- Some of the key players in the Liquid Cooling Systems Market include Asetek, Cooler Master Technology, CORSAIR, EVGA Corporation, NZXT, Inc., Rittal GmbH & Co. KG, Schneider Electric, Thermaltake Technology Co., Ltd., and Zalman Tech Co. These companies focus on product innovation, strategic partnerships, and acquisitions to stay competitive in the market. - Other prominent players in the market are Alfa Laval, Antec Inc., BORSCHE (ZHUHAI) ELECTRONICS CO. LTD., China Mobile Limited, Deepcool Industries Limited, EKWB d.o.o., and Frigadon. These players offer a wide range of liquid cooling solutions catering to various industries and applications.

https://www.databridgemarketresearch.com/reports/global-liquid-cooling-systems-marketThe liquid cooling systems market continues to witness significant growth and innovation driven by the increasing demand for efficient heat management solutions across various applications. The segment differentiation based on type, application, and cooling method provides a clear understanding of the market dynamics and consumer preferences. Closed loop systems are preferred for their efficiency and ease of installation, catering to consumers looking for hassle-free cooling solutions. In contrast, open-loop systems offer customization options, appealing to users seeking more control over their cooling configurations despite the potential need for additional maintenance.

In terms of application segmentation, data centers stand out as the primary consumer of liquid cooling systems due to the critical need for effective heat dissipation in high-performance computing environments. The gaming PC segment is also experiencing rapid growth as gamers prioritize system performance and seek ways to optimize cooling for enhanced gameplay experiences. Other sectors such as automotive, healthcare, and industrial applications are also adopting liquid cooling solutions to address specific heat management challenges and improve overall system efficiency.

Furthermore, the cooling method classification into liquid-to-liquid cooling and direct-to-chip cooling highlights the diverse approaches to managing heat in different systems. Liquid-to-liquid cooling offers efficient heat transfer between liquids, making it ideal for high-power applications that require robust cooling capabilities. On the other hand, direct-to-chip cooling focuses on circulating coolant within the chip package itself to address heat generation at the source, ensuring effective thermal management for optimized performance.

The competitive landscape of the liquid cooling systems market is characterized by key players such as Asetek, Cooler Master Technology, CORSAIR, and Thermaltake Technology Co., who prioritize innovation, strategic partnerships, and acquisitions to maintain their market position. These companies leverage their expertise in product development to meet evolving consumer demands and offer advanced cooling solutions tailored to specific applications and industries. Additionally, other notable players like Alfa Laval, Antec Inc., and EKWB d.o.o. bring a diverse range of liquid cooling products to the market, catering to a wide spectrum of customer needs and preferences.

Overall**Global Liquid Cooling Systems Market**

- The liquid cooling systems market is poised for significant growth and innovation, driven by the rising demand for efficient heat management solutions across a variety of applications. - Key segments in the market include Closed Loop Systems and Open Loop Systems based on Type, with closed loop systems being favored for their efficiency and ease of installation. - Application segmentation highlights Data Centers as the leading consumer due to the critical need for effective heat dissipation, while the Gaming PCs segment is experiencing rapid growth driven by the quest for enhanced performance. - Cooling methods are categorized into Liquid-to-Liquid Cooling and Direct-to-Chip Cooling, offering distinct approaches to managing heat in different systems.

The market continues to evolve with players like Asetek, Cooler Master Technology, and CORSAIR leading the way through innovation, strategic partnerships, and acquisitions. These companies prioritize product development to meet changing consumer demands and offer advanced cooling solutions customized for various applications and industries. Alongside them, players such as Alfa Laval and EKWB d.o.o. are also contributing diverse liquid cooling products to cater to a wide range of customer needs and preferences. The competitive landscape is dynamic, with companies striving to differentiate themselves by delivering cutting-edge solutions that address the evolving requirements of the market.

**Global Liquid Cooling Systems Market, By Type (Liquid Heat Exchanger Systems, Compressor-Based Systems), End-Use Industry (Healthcare, Analytical Equipment, Industrial, Data Centers, Telecommunications, Automotive, Military), Country (

Core Objective of Liquid Cooling Systems Market:

Every firm in the Liquid Cooling Systems Market has objectives but this market research report focus on the crucial objectives, so you can analysis about competition, future market, new products, and informative data that can raise your sales volume exponentially.

Size of the Liquid Cooling Systems Market and growth rate factors.

Important changes in the future Liquid Cooling Systems Market.

Top worldwide competitors of the Market.

Scope and product outlook of Liquid Cooling Systems Market.

Developing regions with potential growth in the future.

Tough Challenges and risk faced in Market.

Global Liquid Cooling Systems top manufacturers profile and sales statistics.

Key takeaways from the Liquid Cooling Systems Market report:

Detailed considerate of Liquid Cooling Systems Market-particular drivers, Trends, constraints, Restraints, Opportunities and major micro markets.

Comprehensive valuation of all prospects and threat in the

In depth study of industry strategies for growth of the Liquid Cooling Systems Market-leading players.

Liquid Cooling Systems Market latest innovations and major procedures.

Favorable dip inside Vigorous high-tech and market latest trends remarkable the Market.

Conclusive study about the growth conspiracy of Liquid Cooling Systems Market for forthcoming years.

Frequently Asked Questions

What is the Future Market Value for Liquid Cooling Systems Market?

What is the Growth Rate of the Liquid Cooling Systems Market?

What are the Major Companies Operating in the Liquid Cooling Systems Market?

Which Countries Data is covered in the Liquid Cooling Systems Market?

What are the Main Data Pointers Covered in Liquid Cooling Systems Market Report?

Browse Trending Reports:

Recreational Cannabis Market Paediatric Gliomas Drugs Market Zinc Glycinates Market Restriction Endonucleases Products Market Food Grade Gases In Meat And Seafood Application Market Temperature Smart Roads Market Automotive Airbag Silicone Market Non Networked Sound Masking System Market Nitrile Butadiene Rubber Br Market Big Data As a Service Bdaas Market Robotically Assisted Surgical Devices Market Transactional Video Demand Market Rice Transplanter Market Bio Based Polyethylene Terephthalate Pet Packaging Market Bath Mats Market Synthetic Iron Oxide Pigments Market Polyvalent Anti Venom Market Managed Siem And Log Management Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

The global demand for Petrochemical Processing Equipments was USD xx Billion in 2022 and is estimated to reach USD xx Billion in 2030, expanding at a CAGR of 7.50% between 2023 and 2030. The petrochemical processing equipment market is a critical component of the global industrial landscape, driving the production of essential chemicals that form the backbone of modern economies. This market encompasses a wide array of equipment used in the processing of raw materials such as natural gas and crude oil into valuable petrochemical products. With the growing demand for petrochemical products across various sectors, including automotive, construction, and consumer goods, the petrochemical processing equipment market is poised for significant growth. This article provides an overview of the market, highlighting its key drivers, challenges, trends, and future outlook.

Browse the full report at https://www.credenceresearch.com/report/petrochemical-processing-equipment-market

Market Drivers

1. Rising Demand for Petrochemical Products: The increasing demand for petrochemical products, such as ethylene, propylene, and benzene, is a primary driver of the petrochemical processing equipment market. These products are essential in the manufacture of plastics, synthetic rubber, fertilizers, and other chemicals, which are integral to industries like automotive, construction, packaging, and textiles. As global economies expand, the demand for these products continues to rise, fueling the need for advanced processing equipment.

2. Technological Advancements: Technological innovations in petrochemical processing equipment are significantly contributing to market growth. The development of more efficient, reliable, and environmentally friendly equipment is enabling petrochemical companies to optimize their production processes, reduce operational costs, and meet stringent environmental regulations. Innovations such as modularization, digitalization, and automation are also enhancing the performance and scalability of petrochemical plants.

3. Expansion of Petrochemical Production Capacity: To meet the growing demand for petrochemical products, companies are expanding their production capacities by investing in new plants and upgrading existing facilities. This expansion drives the demand for a wide range of processing equipment, including reactors, distillation columns, heat exchangers, and separation units. Additionally, the increasing focus on producing bio-based and sustainable petrochemicals is leading to investments in new types of processing equipment.

Market Challenges

1. High Capital and Operational Costs: The petrochemical processing equipment market is capital-intensive, requiring significant investment in machinery, infrastructure, and technology. High operational costs, including maintenance, energy consumption, and labor, further add to the financial burden on companies. These factors can act as a deterrent for smaller players and new entrants, limiting market competition.