#Advanced Polymer Composites Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 44% of users from Denmark used Tumblr daily.

Text

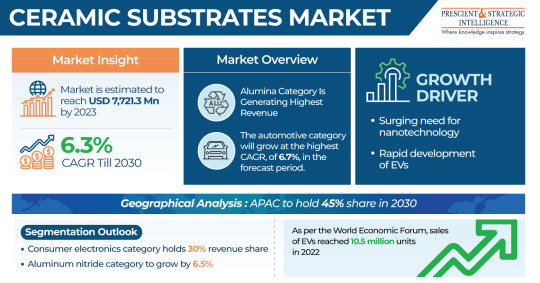

Ceramic Substrates Market Will Reach USD 11,740.8 Million By 2030

In 2023, the ceramic substrates market was valued at USD 7,721.3 million. Forecasts indicate it will grow significantly, reaching USD 11,740.8 million by 2030, with a projected compound annual growth rate (CAGR) of 6.3% between 2024 and 2030. This growth of the industry can be credited to the increasing need for such materials in many sectors and the trend of the reduction of electronic…

View On WordPress

#3D Printing Materials Market#ceramics#Competitive Landscape#composites#growth prospects#innovations#Investors#Key players#Manufacturers#market drivers#metals#polymers#regulatory landscapes#researchers#Technological advancements#Trends

0 notes

Text

How Everyday Chemicals Drive Progress Across Industries

Chemicals play very crucial roles in everyday life-from food to the products one uses; chemicals are in the middle of numerous innovations that integrate new dimensions of convenience, safety, and sustainability. While many of these compounds are taken for granted, knowing about their properties and applications can make one appreciate the science underlying almost every dimension of modern life.

This blog is in a way going to discover some of the most potent chemicals around the world that have changed the industry and daily lives and focus on how they are being made and applied.

Fundamentals of Major Chemical Compounds

Briefly, the beginning part of the blog section is that by the end of reading it, you will know something new about chemicals without even feeling like you read a boring blog. Now we will go deeper into the fundamentals of major chemical compounds.

1. Potassium Tert Amylate

Potassium Tert Amylate is an important reagent that finds enormous application in the chemical industry. It is one of the strong bases used in many organic synthesis processes. The principal applications are:

Alkylation and deprotonation reactions.

The production of pharmaceuticals and agrochemicals.

Increased efficiency of polymer synthesis.

Being a well-known Potassium Tert Amylate Manufacturer, companies have taken to producing pure products with regard to the strict standards of chemical synthesis.

2. Sodium Tert Amylate

Sodium Tert Amylate, like Potassium Tert Amylate, is yet another alkali an integral part of organic synthesis. So distinctively high in its propriety for such reaction conditions, it was discovered a few years back and hence opened up many possible applications. Sodium Tert Amylate reports the following applications:

Preparation of fine chemicals and intermediates.

Used in specialty chemicals developed for the pharmaceutical industry.

Integration for the production of advanced materials.

Sodium Tert Amylate Manufacturers like Suparna Chemicals focus on consistently producing quality products to meet the needs of the world market.

3. Ketonic Resins

Ketonic Resins are versatile chemicals that can be employed in many industries owing to their superlative solubility, adhesion, and gloss-improving properties. Resins manufactured through the condensation of ketones with formaldehyde are compatible with different solvents and pigments. Specific applications of Ketonic Resins are:

Production of coatings and varnishes.

Composition of printing inks and adhesives.

Application in industrial paints to improve durability and beauty.

A Leading Ketonic Resins Manufacturer has put in place measures to ensure all these products meet industrial and environmental standards.

4. Potassium Tert Butoxide

Potassium Tert Butoxide is an exceedingly strong but non-nucleophilic base generally used for organic synthesis. The applications of this base reach beyond the pharmaceutical industry to:

Drug development, especially with respect to the synthesis of active pharmaceutical ingredients.

Agrochemical productions, enhancing the development of more effective pesticides.

Polymerization processes for advanced materials.

With increased complexities in reactions and the development of new constructs in industries, a sustained increase in the demand from Potassium Tert Butoxide Manufacturers is expected to continue.

5. Sodium Tert Butoxide

Sodium Tert Butoxide is one of the most important bases in organic chemistry, which is preferred because of its stability and efficacy in a great number of reactions, including but not limited to the following:

Pharmaceutical applications for selective reactions.

Production of specialty chemicals and intermediates.

High-performance polymer production.

Top a Sodium Tert Butoxide Manufacturer like us, focus on delivering products that ensure consistency, safety, and environmental compliance.

The Role of Chemicals in Everyday Life

Almost all the chemicals discussed above in several diverse aspects enhance our lives significantly in different ways. Here are just a few instances:

Healthcare: Potassium and Sodium-based salts are among the important ones in pharmaceutical development. Pharmaceutical preparations are prepared on the basis of this type of chemistry improvement and use for better health outcomes and improved quality of life.

Agriculture: Such types of agrochemicals based on these chemicals help in enhancing crop yield as well as an increase in resistance to pests, thereby contributing to food security and the sustainable practices of agriculture.

Industrial Applications: Examples of such chemical applications are adhesive production up to high-performance coatings, and Ketonic Resins are necessary chemicals that contribute to the efficiency and durability of industrial products.

Consumer goods: From furniture coatings to the inks used in printing, practically all products from consumer goods to chemical solvents would include these compounds known as Ketonic Resins.

Manufacturing Excellence: Meeting Market Demands

The companies that produce these vital chemicals pour in lots of finances into research and development so that the product quality can be innovated and maintained towards sustainability. This is how the best manufacturers can boast:

Advanced Production Techniques: Beyond technology, high-purity chemicals form the hallmark of any production that is deemed world-class.

Sustainability Practices: Some manufacturers have devoted most of their resources to eco-friendly practices.

Worldwide Presence: These top companies have never-ending varieties of industries that they cater to across the world.

Safety and Sustainability

The safety and sustainability promotion has been at the forefront of the chemical industry. The necessary procedures for chemical handling should be complied with so as to maintain health safety concerning the employees, the consumers, and the environment. The activities undertaken include:

Using suitable PPE while handling chemicals.

Proper storage to prevent degradation and accidental reaction of chemicals.

When possible, development of biodegradable and green alternatives.

Future Trends in the Chemical Industry

According to the latest development of the world towards greener and more sustainable approaches, so is the progress of the chemical industry to newness. The major trends are as follows:

Green Chemistry: To design processes that minimize waste or make use of renewable resources.

Digital Transformation: To adopt analytics and artificial intelligence within production systems for a more efficient method of manufacturing.

Custom Solutions: Providing specific formulations of chemicals for individual industrial requirements.

Final Thoughts

Everyday chemicals are the wonders of science demonstrated by human ingenuity towards the constant endeavor for progress. From Potassium Tert Amylate and Sodium Tert Amylate to Ketonic Resins and advanced bases such as Potassium Tertiary Butoxide and Sodium Tertiary Butoxide and many such innovative compound materials, they drive change and discovery for industries. The better comprehension of the applications of these substances and the hard work of manufacturers let humans understand how necessary and important chemicals are toward our futuristic lives.

Whenever you need to get all these chemicals in the best possible way, call Suparna Chemicals right now. As mentioned above, we are the best in every way and we have also obtained ISO certification. Contact us immediately to get quality service.

0 notes

Text

Top 15 Market Players in Global Huntite and Hydromagnesite Market

Top 15 Market Players in Global Huntite and Hydromagnesite Market

The huntite and hydromagnesite market is witnessing significant growth due to increasing demand for flame retardants, fillers, and environmentally friendly materials in various industries, including construction, plastics, and coatings. Here are 15 leading companies that play a crucial role in shaping the global market:

Martin Marietta Materials, Inc. A leading supplier of minerals, Martin Marietta specializes in huntite and hydromagnesite products for industrial and environmental applications.

Omya AG Omya is renowned for its extensive portfolio of mineral fillers, including huntite and hydromagnesite, used in polymers and coatings.

BASF SE BASF offers specialty mineral solutions, integrating huntite and hydromagnesite for fire retardancy and industrial fillers.

IMCD Group A global distributor, IMCD supplies high-purity huntite and hydromagnesite for use in flame retardants and eco-friendly products.

LKAB Minerals LKAB Minerals provides sustainable mineral solutions, focusing on huntite and hydromagnesite for flame-retardant and filler applications.

Huber Engineered Materials Huber is a major producer of specialty chemicals and mineral products, offering huntite and hydromagnesite for polymer and construction applications.

Nabaltec AG Nabaltec is a leader in advanced materials, including huntite and hydromagnesite for halogen-free flame retardants.

Brucite+ This company specializes in magnesium-based products, including hydromagnesite, for industrial and environmental applications.

EuroMinerals GmbH EuroMinerals is a prominent European supplier of high-quality huntite and hydromagnesite for coatings, plastics, and fire-retardant solutions.

Nippon Chemical Industrial Co., Ltd. A leading Japanese chemical company, Nippon Chemical integrates huntite and hydromagnesite into its specialty chemical offerings.

Reade International Corp. Reade specializes in sourcing and distributing mineral fillers, including huntite and hydromagnesite, for diverse industrial uses.

Ziegler Minerals Ziegler focuses on providing tailored mineral solutions, including huntite and hydromagnesite, for advanced material applications.

Mining Ventures Brazil A key supplier from South America, Mining Ventures Brazil offers premium-grade huntite and hydromagnesite for the global market.

NikoMag NikoMag is a leading producer of magnesium-based materials, including hydromagnesite, serving multiple industrial applications.

Specialty Minerals Inc. This company provides innovative mineral solutions, integrating huntite and hydromagnesite for sustainable and performance-enhancing applications.

Request report sample at https://datavagyanik.com/reports/global-huntite-and-hydromagnesite-market-size-production-sales-average-product-price-market-share/

Top Winning Strategies in Huntite and Hydromagnesite Market

Focus on Sustainability With increasing environmental concerns, companies are investing in sustainable mining and processing practices for huntite and hydromagnesite.

Diversification of Applications Expanding the use of huntite and hydromagnesite beyond flame retardants—into paints, coatings, and polymer composites—helps companies tap into new markets.

Investing in R&D Developing advanced formulations and improving product quality ensures better performance in fire resistance and material enhancement.

Geographic Expansion Establishing production facilities and supply chains in high-demand regions, such as Asia-Pacific and North America, allows companies to capture regional opportunities.

Strategic Partnerships Collaborating with end-user industries, including automotive, construction, and electronics, helps secure long-term contracts and co-develop solutions.

Adoption of Halogen-Free Technologies Companies are focusing on producing halogen-free flame retardants using huntite and hydromagnesite to comply with stringent safety and environmental regulations.

Customized Solutions Tailoring products to meet specific customer requirements, such as particle size or enhanced thermal stability, offers a competitive advantage.

Competitive Pricing Streamlining production processes and leveraging economies of scale enables companies to offer competitive pricing, especially in cost-sensitive markets.

Vertical Integration Controlling the supply chain, from mining to final product processing, ensures consistent quality and cost efficiency.

Market Consolidation Mergers and acquisitions among key players allow for improved market reach, technological advancements, and resource optimization.

Digital Transformation Leveraging digital tools for supply chain management, customer engagement, and production monitoring enhances efficiency and responsiveness.

Regulatory Compliance Staying ahead of global safety and environmental regulations ensures continued market access and credibility.

Marketing Eco-Friendly Products Promoting huntite and hydromagnesite as sustainable, non-toxic alternatives to traditional materials appeals to environmentally conscious industries.

Expanding Product Portfolio Offering a variety of huntite and hydromagnesite grades for different industrial applications increases market penetration.

Customer Education and Training Educating end-users on the benefits and proper usage of huntite and hydromagnesite strengthens customer relationships and fosters loyalty.

Request a free sample copy at https://datavagyanik.com/reports/global-huntite-and-hydromagnesite-market-size-production-sales-average-product-price-market-share/

#Huntite and Hydromagnesite Market#Huntite and Hydromagnesite Production#market players#top trends#revenue#average price#market share#market size

0 notes

Text

Microspheres Market Trends, Opportunities and Forecast By 2028

The Microspheres Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2028. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Microspheres Market:

The global Microspheres Market is expected to experience substantial growth between 2024 and 2031. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-microspheres-market

Which are the top companies operating in the Microspheres Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Microspheres Market report provides the information of the Top Companies in Microspheres Market in the market their business strategy, financial situation etc.

Akzo Nobel N.V., 3M, Nouryon, Chase Corp, Luminex Corporation., Matsumoto Yushi-Seiyaku Co.,Ltd, Thermo Fisher Scientific Inc., The Cary Company., Trelleborg AB (publ), Momentive, Chase Corp, Sigmund Lindner GmbH, Mo-Sci Corporation, SINOSTEEL MAANSHAN NEW MATERIAL TECHNOLOGY, Imperial-Microspheres.com, The Kish Company, Inc., PolyMicrospheres, Eko Export, Givaudan

Report Scope and Market Segmentation

Which are the driving factors of the Microspheres Market?

The driving factors of the Microspheres Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Microspheres Market - Competitive and Segmentation Analysis:

**Segments**

- By Type: Hollow Microspheres, Solid Microspheres - By Raw Material: Glass, Ceramic, Fly Ash, Polymer, Metallic. - By End-Use Industry: Construction Composites, Medical Technology, Paints & Coatings, Cosmetics, Automotive, Oil & Gas, Aerospace - By Geography: North America, Europe, Asia-Pacific, South America, Middle East and Africa

The global microspheres market is projected to witness significant growth by 2028. The market is segmented by type into hollow microspheres and solid microspheres. Hollow microspheres are expected to dominate the market due to their wide range of applications in various industries such as construction composites, medical technology, paints & coatings, cosmetics, automotive, oil & gas, and aerospace. Based on raw material, the market is categorized into glass, ceramic, fly ash, polymer, and metallic. Among these, the polymer segment is anticipated to show substantial growth owing to its increasing usage in medical technology and automotive applications. In terms of end-use industry, the market is segmented into construction composites, medical technology, paints & coatings, cosmetics, automotive, oil & gas, and aerospace. The paints & coatings segment is likely to hold a significant market share due to the rising demand for advanced materials in the construction and automotive sectors. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

**Market Players**

- AkzoNobel - Matsumoto Yushi-Seiyaku - Luminex Corporation - Trelleborg AB - Chase Corporation - Momentive - MO SCI Corporation - Potters Industries LLC - Sigmund Lindner GmbH - Polysciences, Inc.

The global microspheres market is highly competitive with the presence of various key players. Some of the prominent market players include AkzoNobel, Matsumoto Yushi-SeThe global microspheres market is witnessing significant growth driven by the increasing demand for lightweight materials in various industries. Hollow microspheres, in particular, are expected to dominate the market due to their versatility and wide range of applications across industries such as construction composites, medical technology, paints & coatings, cosmetics, automotive, oil & gas, and aerospace. These hollow microspheres offer benefits such as reduced weight, improved strength, and enhanced insulation properties, making them highly sought after in the market. On the other hand, solid microspheres also play a crucial role in specific applications where durability and thermal resistance are key requirements.

In terms of raw materials, the market is segmented into glass, ceramic, fly ash, polymer, and metallic microspheres. The polymer segment is projected to experience substantial growth, driven by the increasing utilization of polymers in medical technology and automotive applications. Polymers offer attributes such as flexibility, chemical resistance, and compatibility with various matrices, making them an ideal choice for a wide range of end-use industries. Additionally, advancements in polymer technology have led to the development of innovative microsphere formulations that cater to specific application needs, further driving the segment's growth.

The end-use industry segment of the microspheres market is diverse, catering to sectors such as construction composites, medical technology, paints & coatings, cosmetics, automotive, oil & gas, and aerospace. Among these, the paints & coatings segment is expected to witness substantial growth due to the increasing demand for high-performance coatings in the construction and automotive sectors. Microspheres are extensively used in coatings to enhance properties such as scratch resistance, durability, and thermal insulation. The aerospace industry is also a significant consumer of microspheres, utilizing them in applications such as syntactic foams and lightweight composites for aircraft components.

Geographically, the global microspheres market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. North America is expected to hold a**Market Players**

- Akzo Nobel N.V. - 3M - Nouryon - Chase Corp - Luminex Corporation. - Matsumoto Yushi-Seiyaku Co.,Ltd - Thermo Fisher Scientific Inc. - The Cary Company. - Trelleborg AB (publ) - Momentive - Chase Corp - Sigmund Lindner GmbH - Mo-Sci Corporation - SINOSTEEL MAANSHAN NEW MATERIAL TECHNOLOGY - Imperial-Microspheres.com - The Kish Company, Inc. - PolyMicrospheres - Eko Export - Givaudan

The global microspheres market is witnessing significant growth driven by the increasing demand for lightweight materials across various industries. Hollow microspheres are leading the market due to their versatility and wide array of applications in sectors such as construction composites, medical technology, paints & coatings, cosmetics, automotive, oil & gas, and aerospace. These hollow microspheres offer advantages like reduced weight, improved strength, and enhanced insulation properties, making them highly valued in the market. Meanwhile, solid microspheres also play a crucial role in applications where durability and thermal resistance are essential.

Regarding raw materials, the market includes glass, ceramic, fly ash, polymer, and metallic microspheres. The polymer segment is expected to see substantial growth due to the increasing use of polymers in medical technology and automotive applications. Polymers provide flexibility,

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Microspheres Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Microspheres Market, expected to exhibit impressive growth in CAGR from 2024 to 2028.

Explore Further Details about This Research Microspheres Market Report https://www.databridgemarketresearch.com/reports/global-microspheres-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Microspheres Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Microspheres Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Microspheres Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2031) of the following regions are covered in Chapters

The countries covered in the Microspheres Market report are U.S., Canada and Mexico in North America, Brazil, Argentina and Rest of South America as part of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe in Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA

Detailed TOC of Microspheres Market Insights and Forecast to 2028

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Microspheres Market Landscape

Part 05: Pipeline Analysis

Part 06: Microspheres Market Sizing

Part 07: Five Forces Analysis

Part 08: Microspheres Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Microspheres Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Japan: https://www.databridgemarketresearch.com/jp/reports/global-microspheres-market

China: https://www.databridgemarketresearch.com/zh/reports/global-microspheres-market

Arabic: https://www.databridgemarketresearch.com/ar/reports/global-microspheres-market

Portuguese: https://www.databridgemarketresearch.com/pt/reports/global-microspheres-market

German: https://www.databridgemarketresearch.com/de/reports/global-microspheres-market

French: https://www.databridgemarketresearch.com/fr/reports/global-microspheres-market

Spanish: https://www.databridgemarketresearch.com/es/reports/global-microspheres-market

Korean: https://www.databridgemarketresearch.com/ko/reports/global-microspheres-market

Russian: https://www.databridgemarketresearch.com/ru/reports/global-microspheres-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 1355

Email:- [email protected]

#Microspheres Market Size#Microspheres Market Shares#Microspheres Market Forecast#Microspheres Market Growth#Microspheres Market Demand

0 notes

Text

Bone Regeneration Market: Recent Developments Shaping the Future of Regenerative Medicine

Bone regeneration market has witnessed significant advancements in recent years, driven by evolving technologies, innovative materials, and growing demand for effective treatments. These recent developments are shaping the future of the industry and offering new opportunities for healthcare providers and patients. Below are the key recent advancements in the market:

Advancements in Biomaterials

Development of synthetic bone grafts with enhanced biocompatibility and mechanical strength.

Innovations in biodegradable scaffolds designed for effective bone tissue regeneration.

Introduction of composite materials combining ceramics and polymers for optimized healing.

Use of bioactive glasses that stimulate natural bone repair and regeneration processes.

Improved surface modification techniques enhancing cell adhesion and integration.

3D Printing Technology

Adoption of 3D printing to create customized bone implants tailored to individual needs.

Use of bioprinting for developing complex bone structures with high precision.

Advances in multi-material printing allowing integration of different regenerative elements.

Creation of anatomically accurate scaffolds supporting efficient bone tissue engineering.

Reduction in production time and costs through innovative 3D printing techniques.

Stem Cell-Based Therapies

Expanded use of mesenchymal stem cells for promoting natural bone growth.

Development of stem cell-laden scaffolds for enhanced tissue regeneration.

Integration of gene editing tools like CRISPR for improving stem cell performance.

Clinical trials exploring the efficacy of stem cell therapies in treating bone defects.

Combination therapies using stem cells and growth factors for superior outcomes.

Growth Factors and Biologics

Increasing applications of bone morphogenetic proteins (BMPs) in clinical settings.

Use of platelet-rich plasma (PRP) to accelerate healing and regeneration.

Advances in delivery systems ensuring sustained release of growth factors.

Exploration of novel biologics targeting faster recovery in complex fractures.

Focus on combining biologics with other regenerative techniques for enhanced efficiency.

Minimally Invasive Techniques

Rising adoption of minimally invasive surgical procedures for bone regeneration.

Integration of robotic-assisted systems for precise implantation of bone grafts.

Use of nanotechnology to enhance the effectiveness of injectable bone substitutes.

Development of non-surgical methods for delivering regenerative materials.

Enhanced imaging technologies aiding accurate placement of regenerative products.

Personalized Medicine

Growth of patient-specific treatments based on genetic profiling and imaging data.

Application of AI and machine learning to design individualized bone regeneration plans.

Use of digital modeling tools for pre-surgical planning and custom implant design.

Advances in tailored scaffolds that match the patient’s specific anatomy and needs.

Increased focus on reducing complications through personalized approaches.

Regenerative Medicine Collaborations

Partnerships between biotech firms and academic institutions to develop cutting-edge solutions.

Joint ventures for scaling production of innovative bone graft materials.

Integration of interdisciplinary research for advancing bone regeneration techniques.

Collaborations focusing on expanding the clinical application of regenerative products.

Investment in start-ups driving disruptive innovations in the bone regeneration market.

Global Market Expansion

Growing presence of regenerative medicine technologies in emerging economies.

Increased healthcare funding and infrastructure development in Asia-Pacific regions.

Focus on addressing unmet needs in bone repair across underserved populations.

Regulatory advancements supporting faster approval and commercialization of products.

Rising awareness campaigns promoting bone health and regenerative solutions globally.

Nanotechnology Innovations

Development of nanostructured materials that mimic the natural bone environment.

Application of nanocoatings to enhance the performance of implants and scaffolds.

Advances in nanoparticle delivery systems for targeted regeneration therapies.

Use of nanosensors to monitor the progress of bone healing in real-time.

Exploration of nanomaterials combined with growth factors for superior outcomes.

Focus on Sustainability

Emphasis on eco-friendly and sustainable production of bone graft materials.

Reduction of waste and environmental impact through advanced manufacturing processes.

Exploration of renewable materials for creating regenerative products.

Commitment to ethical sourcing and production practices in the bone regeneration market.

Adoption of green technologies to improve the overall sustainability of regenerative solutions.

These recent developments in the bone regeneration market are paving the way for transformative changes in how bone defects and disorders are treated, ensuring better outcomes for patients worldwide.

0 notes

Text

The Ballistic Protection Materials Market is projected to grow from USD 16120.3 million in 2024 to an estimated USD 25500.03 million by 2032, with a compound annual growth rate (CAGR) of 5.9% from 2024 to 2032. The ballistic protection materials market has witnessed robust growth in recent years, driven by the escalating demand for advanced protective solutions in military, law enforcement, and civilian applications. With the increasing prevalence of conflicts, rising concerns about security, and advancements in material science, this market is poised for significant expansion in the coming years.

Browse the full report at https://www.credenceresearch.com/report/ballistic-protection-materials-market

Market Size and Growth Dynamics

The global ballistic protection materials market is projected to grow steadily, driven by increasing defense budgets worldwide and a rising emphasis on personal protection equipment. This market encompasses a wide range of products, including body armor, helmets, shields, and vehicle armoring solutions. Governments and private organizations are investing heavily in research and development to enhance the performance, durability, and versatility of ballistic protection materials, ensuring their application across diverse environments.

The market's growth is further supported by the proliferation of advanced threats, including high-velocity ammunition and improvised explosive devices (IEDs), which necessitate the use of innovative materials capable of providing superior protection. Lightweight yet durable materials such as aramid fibers, ultra-high-molecular-weight polyethylene (UHMWPE), and ceramics have gained prominence, as they offer enhanced mobility without compromising safety.

Key Market Drivers

One of the primary drivers of the ballistic protection materials market is the increasing demand for personal protective equipment (PPE) among military personnel and law enforcement agencies. The global rise in terrorism and regional conflicts has heightened the need for advanced protective gear to ensure the safety of those on the front lines. Ballistic-resistant vests and helmets are now standard equipment for military and police forces in many countries, further propelling market demand.

Additionally, advancements in material science have led to the development of next-generation ballistic protection materials that are lighter, stronger, and more efficient. Innovations in nanotechnology and composite materials are enabling manufacturers to produce gear that not only meets rigorous safety standards but also enhances user comfort and operational efficiency. These technological advancements are particularly crucial in modern warfare and urban policing, where agility and endurance are paramount.

Emerging Trends and Opportunities

The growing focus on sustainability and environmental impact is influencing the development of ballistic protection materials. Manufacturers are increasingly exploring eco-friendly production processes and recyclable materials to align with global sustainability goals. For example, research into bio-based polymers and renewable fiber technologies is gaining traction, offering a potential pathway for reducing the ecological footprint of ballistic protection products.

The civilian segment of the market is also emerging as a significant growth area. With rising crime rates and increasing awareness about personal safety, there is a growing demand for ballistic-resistant products such as backpacks, clothing, and home security solutions. This trend is particularly evident in regions with high urbanization rates and socio-political instability, where civilians seek additional layers of protection.

Challenges and Restraints

Despite its promising growth prospects, the ballistic protection materials market faces several challenges. High production costs and the complex manufacturing processes involved in developing advanced materials pose significant barriers to entry for smaller players. Additionally, stringent regulatory requirements and certification standards can delay product launches and increase operational costs.

Future Outlook

The ballistic protection materials market is set to evolve rapidly, with technological advancements and shifting consumer needs shaping its trajectory. As global security concerns continue to rise, the demand for innovative, lightweight, and eco-friendly ballistic protection solutions will remain robust. Collaboration between governments, private enterprises, and research institutions will be crucial in driving innovation and ensuring the market's sustainable growth.

Key Player Analysis:

ArmorSource LLC

Avient Corporation

BAE Systems

Bally Ribbon Mills

Beijing Tongyizhong New Material Technology Corporation

DuPont

Final Advanced Materials

FY-Composites Oy

Honeywell International Inc.

HUVIS Corp

Hyosung Corporation

Kolon Industries Inc.

Kordsa

Morgan Advanced Materials Plc.

Rheinmetall AG

Rochling Group

Saint-Gobain S.A.

TEIJIN Ltd.

TenCate Protective Fabrics

Toyobo Co., Ltd.

Segmentation:

By Material Type:

Aramid Fibers (e.g., Kevlar)

Ultra-High Molecular Weight Polyethylene (UHMWPE)

Glass Fiber

Ceramic Materials

Metals and Alloys

Composites

Others (e.g., Carbon Fiber, Hybrid Materials)

By Application:

Personal Protective Equipment (PPE):

Body Armor (Vests, Plates)

Helmets

Shields

Vehicle Protection:

Armored Vehicles

Aircraft

Naval Vessels

Infrastructure Protection:

Military Bases

Government Buildings

Embassies

Others (e.g., Border Security Structures)

By End-Use Industry:

Defense and Military

Homeland Security

Law Enforcement

Civilian Applications

Industrial Applications (e.g., Mining, Energy)

By Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/ballistic-protection-materials-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

3D Printing Materials Market Valued at USD 2,836.6 Million in 2025

Exploring the Dynamic World of 3D Printing Materials Market 2034

The world of 3D Printing Materials Market has come a long way since its inception, evolving from a niche technology to a mainstream manufacturing process. At the heart of this transformation is the ever-expanding universe of 3D printing materials. These materials are not just a means to an end; they are pivotal in defining what can be created, how it can be produced, and what industries can benefit from this cutting-edge technology. In this blog, we will delve into the key aspects of the 3D printing materials market, exploring the types, applications, and future trends shaping this exciting field.

Sample copy report:

https://wemarketresearch.com/reports/request-free-sample-pdf/3d-printing-materials-market/1338

Types of 3D Printing Materials

Thermoplastics: Thermoplastics are among the most widely used materials in 3D printing. They are known for their ease of use, affordability, and versatility. Popular thermoplastics include:

PLA (Polylactic Acid): Known for its eco-friendly nature and ease of printing, PLA is a favorite among hobbyists and beginners.

ABS (Acrylonitrile Butadiene Styrene): This material offers greater strength and durability, making it ideal for functional prototypes and end-use parts.

PETG (Polyethylene Terephthalate Glycol): Combining the ease of printing with durability, PETG is commonly used in applications requiring resistance to impact and moisture.

Resins: Resins are liquid materials that solidify under UV light and are used primarily in SLA (Stereolithography) and DLP (Digital Light Processing) printers. They offer high resolution and detail, making them suitable for applications such as jewelry and dental products. Key types include:

Standard Resins: Ideal for detailed models and prototypes.

Tough Resins: Engineered for increased durability and impact resistance.

Flexible Resins: Designed to produce parts with rubber-like properties.

Metals: Metal 3D printing is used for high-performance applications in industries such as aerospace, automotive, and medical. Metal powders, such as titanium, aluminum, and stainless steel, are used in processes like SLM (Selective Laser Melting) and EBM (Electron Beam Melting). Metal 3D printing offers:

High Strength-to-Weight Ratio: Essential for aerospace and automotive components.

Complex Geometries: Allows for the creation of intricate designs that are difficult to achieve with traditional manufacturing methods.

Composites: Composite materials combine thermoplastics with reinforcing fibers, such as carbon fiber or glass fiber, to enhance strength and rigidity. These materials are used in applications where lightweight and high strength are critical, including in the automotive and sports equipment industries.

Innovations Driving the 3D Printing Materials Market

The 3D printing materials market is experiencing rapid innovation, driven by advancements in technology and changing industry needs. Here’s a closer look at some of the latest innovations that are transforming the landscape of 3D printing materials:

Nanomaterials: Nanotechnology is making waves in the 3D printing industry by enabling the creation of materials with enhanced properties at the nanoscale. Nanomaterials can improve strength, durability, and thermal resistance, making them ideal for high-performance applications. For example, incorporating nanoparticles into polymers can enhance their mechanical properties, leading to more robust and reliable printed parts.

Bio-inks and Bioprinting: Bioprinting is revolutionizing the medical and research fields by enabling the creation of living tissues and organs. Bio-inks, which are made from natural and synthetic biopolymers, are used in this process to print cellular structures. These materials can be tailored to support cell growth and tissue development, opening up new possibilities for regenerative medicine and personalized healthcare.

Applications of 3D Printing Materials Market

The versatility of 3D printing materials market has led to their adoption across various sectors:

Aerospace: Lightweight and durable materials are used to manufacture complex parts and components, reducing overall weight and fuel consumption.

Healthcare: Custom prosthetics, implants, and dental products are tailored to individual patients using biocompatible materials.

Automotive: 3D printing enables rapid prototyping and production of lightweight parts, enhancing vehicle performance and reducing time-to-market.

Consumer Goods: Customized products, from eyewear to home decor, benefit from the flexibility and personalization offered by 3D printing.

Future Trends in 3D Printing Materials Market

As the 3D printing industry continues to evolve, several trends are likely to shape the future of 3D printing materials:

Biodegradable and Sustainable Materials: There is a growing focus on developing eco-friendly materials that reduce environmental impact. Innovations in biodegradable plastics and recycling processes are set to make 3D printing more sustainable.

Advanced Metal Alloys: The development of new metal alloys with enhanced properties will open up new possibilities for high-performance applications in industries such as aerospace and defense.

Multi-Material Printing: Advances in multi-material printing technologies will allow for the creation of complex objects with varying properties in a single print, expanding the range of applications and functionalities.

Smart Materials: The integration of materials that respond to environmental changes (such as temperature or pressure) will lead to the development of "smart" products with adaptive capabilities.

Benefits of 3D Printing Materials Market Report:

Analyst Support: Get your query resolved by our expert analysts before and after purchasing the report.

Customer Satisfaction: Our expert team will assist with all your research needs and customize the report.

Inimitable Expertise: Analysts will provide deep insights into the reports.

Assured Quality: We focus on the quality and accuracy of the report.

Conclusion

The 3D printing materials market is a dynamic and rapidly evolving field, driven by continuous innovation and Technological Advancements. From thermoplastics and resins to metals and composites, the variety of materials available today provides limitless possibilities for creators and manufacturers alike. As we look to the future, emerging trends and new material developments promise to further revolutionize the industry, offering exciting opportunities for growth and transformation across various sectors. Whether you're a hobbyist, a designer, or an industry professional, staying informed about these advancements will be key to leveraging the full potential of 3D printing technology.

#3D Printing Materials Analysis#3D Printing Materials Demand#Market Insights 3D Printing#3D Printing Materials Future

0 notes

Text

Advanced Polymer Matrix Composites Market

Advanced Polymer Matrix Composites (APMC) market is experiencing significant growth due to their high strength-to-weight ratio, corrosion resistance, and thermal stability, making them ideal for industries like aerospace, automotive, and defense. APMCs, which combine polymers with reinforcing fibers like carbon or aramid, are increasingly used in lightweight, high-performance applications. The market benefits from advancements in manufacturing technologies and rising demand for energy-efficient solutions. Key factors driving growth include the need for fuel-efficient vehicles, reduction in carbon emissions, and increased automation. Challenges such as high production costs and material complexity are being addressed through innovation and research.

For More : https://www.industryarc.com/Research/advanced-polymer-matrix-composites-market-research-501462?utm_source=SBMs&utm_medium=Tumblr&utm_campaign=Sarath

1 note

·

View note

Text

Automotive Thermoplastic Polymer Composite Market: Lightweighting Solutions for the Future up to 2033

Market Definition

The automotive thermoplastic polymer composite market involves the use of advanced thermoplastic materials reinforced with fibers such as glass or carbon, engineered for automotive applications. These composites are lightweight, durable, and capable of withstanding high stresses, making them ideal for components like body panels, interiors, and structural reinforcements in vehicles. Their recyclability and design flexibility further enhance their appeal in modern automotive manufacturing.

To Know More @ https://www.globalinsightservices.com/reports/automotive-thermoplastic-polymer-composite-market

The automotive thermoplastic polymer composite market is anticipated to expand from $9.2 billion in 2023 to $16.8 billion by 2033, with a CAGR of 6.2%.

Market Outlook

The adoption of thermoplastic polymer composites in the automotive sector is driven by the industry’s focus on weight reduction, fuel efficiency, and compliance with stringent environmental regulations. Lightweight materials are crucial for enhancing vehicle performance while reducing emissions, making thermoplastic composites a preferred choice for automakers.

The increasing demand for electric vehicles (EVs) has further propelled the need for advanced lightweight materials to offset battery weight and optimize energy consumption. Thermoplastic polymer composites offer significant advantages, including faster processing times, superior impact resistance, and cost-effective manufacturing compared to traditional materials.

Challenges include the high cost of raw materials and the need for specialized manufacturing technologies, which can limit adoption among small-scale manufacturers. Additionally, concerns about the thermal and mechanical performance of certain thermoplastics under extreme conditions pose barriers. However, ongoing research and innovation in composite formulations and processing techniques are expected to overcome these challenges.

The growing integration of automation in composite manufacturing and the expansion of EV production present lucrative opportunities for market growth. As regulatory bodies emphasize sustainability, the recyclability of thermoplastic composites is likely to play a pivotal role in shaping market dynamics.

Request the sample copy of report @ https://www.globalinsightservices.com/request-sample/GIS26953

0 notes

Text

Additive Manufacturing Market Analysis, Growth Factors and Competitive Strategies by Forecast 2034

Additive manufacturing (AM), commonly known as 3D printing, is a transformative approach to industrial production that enables the creation of lightweight, complex designs directly from digital models. It is increasingly used across industries like aerospace, automotive, healthcare, and consumer goods due to its ability to reduce waste, lower production costs, and shorten manufacturing times.

According to projections, the additive manufacturing market would grow linearly and reach a valuation of USD 17.23 billion by 2023. With a compound annual growth rate (CAGR) of 21.65% from 2024 to 2033, it is anticipated to have increased to USD 84.87 billion by that time.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/additive-manufacturing-market/1376

Key Drivers

Technological Advancements: Innovations in 3D printing materials and techniques, such as metal and bio-based printing, are fueling growth.

Adoption Across Industries: Applications in aerospace, healthcare, automotive, and consumer goods are expanding rapidly.

Sustainability Goals: Additive manufacturing reduces waste and optimizes material usage, aligning with global sustainability efforts.

Challenges

High initial investment costs for equipment and training.

Limitations in material properties and product size for certain applications.

Regulatory hurdles in industries like healthcare and aerospace.

Applications Across Industries

Aerospace and Defense Additive manufacturing is extensively used to produce lightweight and complex parts, reducing fuel consumption and improving performance.

Healthcare Customized medical devices, implants, and prosthetics are transforming patient care. Bio-printing for tissues and organs is an emerging field.

Automotive Automotive manufacturers leverage 3D printing for prototyping, tooling, and even end-use parts, reducing lead times and costs.

Consumer Goods The ability to personalize products such as footwear, jewelry, and electronics is driving adoption in the consumer market.

Construction Large-scale 3D printing is being utilized to construct buildings and infrastructure more efficiently and sustainably.

Key companies profiled in this research study are,

Stratasys, Ltd.;

Materialise NV;

EnvisionTec, Inc.;

3D Systems, Inc.;

GE Additive;

Autodesk Inc.;

Made In Space;

Canon Inc.;

Voxeljet AG.

Additive Manufacturing Market Segmentation,

By Technology:

Stereolithography (SLA)

Fused Deposition Modeling (FDM)

Selective Laser Sintering (SLS)

Direct Metal Laser Sintering (DMLS)

Others (Binder Jetting, Electron Beam Melting, etc.)

By Material:

Polymers

Metals

Ceramics

Others (Composites, Biomaterials, etc.)

By Application:

Prototyping

Production

Tooling

By Industry:

Aerospace

Automotive

Healthcare (particularly for dental and orthopedic implants)

Consumer Goods

Defense

Additive Manufacturing Market Regional Analysis:

North America: Dominates the market due to high adoption of AM technologies in industries like aerospace and healthcare.

Europe: Strong growth due to government initiatives and industrial adoption.

Asia-Pacific: Emerging as a significant market with increased investment in industrial 3D printing in countries like China, Japan, and South Korea.

Conclusion:

The additive manufacturing market is poised for transformative growth, offering unparalleled opportunities across industries. As technology evolves and adoption increases, this sector is expected to redefine traditional manufacturing processes, paving the way for a more sustainable and efficient industrial future.

0 notes

Text

Automotive Lightweight Materials Market Growth: The Impact of Electrification and Eco-Friendly Vehicle Trends

The automotive industry is undergoing a significant transformation as manufacturers prioritize sustainability, fuel efficiency, and regulatory compliance. One of the key trends driving this transformation is the adoption of lightweight materials, which offer substantial benefits such as improved fuel efficiency, reduced emissions, and enhanced performance. The automotive lightweight materials market is experiencing rapid growth due to various factors, including technological advancements, stringent government regulations, and increasing consumer demand for eco-friendly vehicles. In this article, we will explore the key drivers propelling the growth of the automotive lightweight materials market.

1. Stringent Environmental Regulations

Governments worldwide have implemented strict regulations to combat climate change and reduce automotive carbon footprints. In particular, emissions standards and fuel efficiency regulations are becoming more stringent, particularly in regions like Europe, North America, and Asia-Pacific. Lightweight materials help automakers meet these requirements by reducing the overall weight of vehicles, which leads to improved fuel efficiency and lower emissions. As automakers seek to comply with these regulations, the demand for lightweight materials such as aluminum, magnesium, and high-strength steel has surged.

2. Fuel Efficiency and Performance Enhancements

Fuel efficiency is a top priority for automakers, particularly as fuel prices continue to rise and environmental concerns escalate. Lightweight materials are key to enhancing fuel efficiency, as reducing vehicle weight directly contributes to lower fuel consumption. Lighter vehicles require less energy to move, leading to better miles per gallon (MPG) ratings. Moreover, lightweight materials also improve vehicle performance by enabling better acceleration, handling, and overall driving dynamics. As a result, automakers are increasingly incorporating advanced materials like carbon fiber-reinforced polymers (CFRP) and aluminum alloys into vehicle designs to improve both fuel efficiency and performance.

3. Consumer Demand for Eco-Friendly Vehicles

Consumer preference for environmentally friendly and fuel-efficient vehicles is on the rise. Electric vehicles (EVs), hybrid cars, and fuel-efficient internal combustion engine (ICE) vehicles are gaining popularity as more consumers become aware of the environmental impact of their choices. Lightweight materials play a crucial role in the production of these vehicles by reducing their weight, thereby improving range (for EVs), fuel efficiency (for hybrids and ICE vehicles), and overall environmental footprint. The growing demand for sustainable transportation options is a key driver of the automotive lightweight materials market, as manufacturers seek to meet the needs of eco-conscious consumers.

4. Technological Advancements in Material Science

Technological innovations in material science have led to the development of advanced lightweight materials that are not only lighter but also stronger, more durable, and cost-effective. For example, the development of high-strength steel alloys and the growing use of aluminum in automotive production have significantly improved the safety and structural integrity of vehicles without adding extra weight. Additionally, carbon fiber composites are being used more widely due to their exceptional strength-to-weight ratio. These advancements in material science have made it easier for automakers to adopt lightweight materials without compromising safety or performance, driving the growth of the automotive lightweight materials market.

5. Automotive Industry’s Shift Towards Electrification

The ongoing shift towards electrification in the automotive industry is another major driver of the lightweight materials market. Electric vehicles (EVs) require lightweight materials to enhance their range and efficiency, as every kilogram saved can significantly improve battery life and overall performance. As automakers ramp up their production of electric vehicles to meet growing consumer demand, the need for lightweight materials like aluminum, magnesium, and carbon fiber has increased. These materials help reduce the weight of the vehicle, allowing EVs to travel longer distances on a single charge while also improving acceleration and handling.

6. Cost-Effectiveness and Long-Term Savings

While lightweight materials may have higher upfront costs, they offer significant long-term savings due to improved fuel efficiency and reduced maintenance costs. Lighter vehicles experience less wear and tear on components like tires, brakes, and suspension systems, which leads to lower maintenance costs over time. Additionally, the increased fuel efficiency and reduced emissions result in long-term savings for both consumers and manufacturers. As automakers recognize the cost-effectiveness of lightweight materials, their adoption in vehicle manufacturing has accelerated.

Conclusion

The automotive lightweight materials market is growing at a rapid pace, driven by a combination of regulatory pressures, consumer demand for eco-friendly vehicles, advancements in material science, and the ongoing shift towards electrification. As automakers continue to prioritize fuel efficiency, performance, and sustainability, the demand for lightweight materials such as aluminum, magnesium, and carbon fiber will continue to rise. These materials offer significant benefits in terms of fuel efficiency, performance, and safety, making them essential to the future of the automotive industry.

0 notes

Text

Carbon Nanotubes Market

Carbon Nanotubes Market Size, Share, Trends: Nanocyl SA Leads

Growing Acceptance in Uses Related to Energy Storage

Market Overview:

The global Carbon Nanotubes Market is anticipated to grow at a CAGR of 14.8% between 2024 and 2031. The market size in 2022 is estimated to be USD 876.4 million; by 2031, it is expected to have increased to USD 3,252.7 million. It is anticipated that Asia-Pacific will dominate the market throughout the forecast period. The market for carbon nanotubes is expanding quickly due to rising demand in a number of industries, including electronics, aerospace, automotive, and healthcare. Carbon nanotubes' exceptional strength, exceptional electrical and thermal conductivity, and lightweight nature are what motivate their advanced applications. Expanding research and development endeavours contribute to expanding the potential uses of carbon nanotubes, hence bolstering market expansion.

DOWNLOAD FREE SAMPLE

Market Trends:

The remarkable qualities of carbon nanotubes are driving their increasing popularity in energy storage technologies. To improve their performance, carbon nanotubes are being included into supercapacitors, lithium-ion batteries, and other energy storage technologies. In these devices, carbon nanotubes' large surface area, great electrical conductivity, and mechanical strength help to increase energy density, accelerate charge-discharge rates, and extend cycle life. Growing demand for portable devices, renewable energy systems, and electric cars—all of which depend on effective energy storage—drives this trend. The importance of carbon nanotubes in energy storage uses is predicted to rise greatly as the globe moves toward greener energy sources and electrification fuels industry expansion.

Market Segmentation:

Currently holding the most market share in the carbon nanotubes sector are Multi-Walled Carbon Nanotubes (MWCNTs), thanks to their adaptability and somewhat lower manufacturing costs than Single-Walled Carbon Nanotubes (SWCNTs). Multiple layers of graphene cylinders nested inside one another make MWCNTs strong, conductive, and thermally compatible for a variety of uses. Their numerous walls and bigger diameter allow them to be produced in quantity more easily, which helps to explain their cost-effectiveness and general acceptance in many sectors. Polymer composites, conductive coatings, energy storage systems, and structural materials all find use for MWCNTs.

Market Key Players:

The carbon nanotubes market is highly competitive, with major players focusing on research and development to improve product quality, lower manufacturing costs, and increase application areas. Key companies such as Nanocyl SA, Arkema SA, Showa Denko K.K., Toray Industries Inc., Hanwha Chemical Corporation, Carbon Solutions Inc., Arry International Group Limited, Cheap Tubes Inc., OCSiAl, and Hyperion Catalysis International dominate the market.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

3D Bioprinting Organoids Market Expected to Witness a Sustainable Growth Over 2033

Market Definition

The 3D bioprinting organoids market focuses on developing miniaturized, three-dimensional tissue models using advanced bioprinting technologies. These organoids mimic the complex structure and functionality of human organs, supporting breakthroughs in drug discovery, personalized medicine, and disease modeling. The market encompasses bioprinting technologies, bioinks, and specialized research services, driving significant progress in biomedical research and therapeutic innovation.

Market Segmentation

Type Hydrogels, Extrusion-based, Inkjet-based, Laser-assisted, Microvalve Product Organoids, Bioprinters, Biomaterials, Scaffolds, Bioinks Services Custom Bioprinting, Consultation, Maintenance, Training Technology 3D Bioprinting, 4D Bioprinting, Stereolithography, Digital Light Processing Application Drug Discovery, Regenerative Medicine, Cancer Research, Toxicology Testing, Personalized Medicine, Tissue Engineering Material Type Synthetic Polymers, Natural Polymers, Ceramics, Metals, Composites End User Pharmaceutical Companies, Research Institutes, Healthcare Providers, Biotechnology Firms, Academic Institutions Process Cell Culturing, Pre-processing, Post-processing, Bioassembly Component Printer Head, Nozzle, Cartridge, Control System

Request Sample: https://www.globalinsightservices.com/request-sample/?id=GIS32584

Research Objectives

Estimates and forecast the overall market size for the total market, across product, service type, type, end-user, and region Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling Identify factors influencing market growth and challenges, opportunities, drivers and restraints Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities Thoroughly analyze smaller market segments strategically, focusing on their potential, individual patterns of growth, and impact on the overall market To thoroughly outline the competitive landscape within the market, including an assessment of business and corporate strategies, aimed at monitoring and dissecting competitive advancements. Identify the primary market participants, based on their business objectives, regional footprint, product offerings, and strategic initiatives

Market Outlook

The 3D bioprinting organoids market is projected to grow from $1.2 billion in 2023 to $6.9 billion by 2033, with a CAGR of 18.4%. In 2023, the market volume reached approximately 320 million units, with expectations to grow to 560 million units by 2033. The drug testing segment leads with a 45% market share, followed by organoid transplantation at 30%, and disease modeling at 25%. Growth is driven by advancements in regenerative medicine and personalized healthcare. Leading players such as Organovo Holdings, CELLINK, and Aspect Biosystems are leveraging cutting-edge technologies to strengthen their market positions.

The competitive landscape is shaped by strategic partnerships, innovation, and evolving regulatory frameworks like the FDA's guidance on bioprinting, which influence compliance and approval processes. Future projections highlight a 15% increase in R&D investment by 2033, underscoring the importance of technological advancements for competitive advantage. While the outlook is positive with opportunities in personalized medicine and regenerative therapies, challenges such as regulatory complexities and high production costs remain, necessitating strategic investments in technology and compliance solutions.

Major Players

Organovo Cellink Aspect Biosystems Allevi Cyfuse Biomedical Regen HU Rokit Healthcare 3D Bioprinting Solutions Prellis Biologics Pandorum Technologies Poietis Volumetric Biogelx Advanced Solutions Life Sciences Nano 3D Biosciences Vivax Bio Brinter Modern Meadow Tiss Use Mat Tek

The 3D bioprinting organoids market is undergoing rapid evolution, driven by advancements in precision bioprinting technology that are reducing production costs and broadening accessibility for research and pharmaceutical applications. Demand for organoids is increasing due to their effectiveness as alternatives to animal testing and traditional cell cultures, especially in drug discovery and personalized medicine.

Regulatory landscapes are adapting, with agencies like the FDA establishing guidelines for bioprinted products. Compliance is critical, influencing both market entry and operational costs. Strategic collaborations between biotech companies and academic institutions are accelerating innovation and commercialization. Additionally, rising venture capital investments in bioprinting startups highlight strong market confidence, fueling further technological progress.

Emerging trends include the miniaturization of bioprinters for laboratory use and a focus on ethical sourcing of biomaterials, aligning with sustainability goals. Intellectual property rights are also gaining importance as companies seek to protect innovations in this competitive sector. With growing interest from emerging economies, the market is poised for significant expansion in healthcare and research applications.

Research Scope

Scope - Highlights, Trends, Insights. Attractiveness, Forecast Market Sizing - Product Type, End User, Offering Type, Technology, Region, Country, Others Market Dynamics - Market Segmentation, Demand and Supply, Bargaining Power of Buyers and Sellers, Drivers, Restraints, Opportunities, Threat Analysis, Impact Analysis, Porters 5 Forces, Ansoff Analysis, Supply Chain Business Framework - Case Studies, Regulatory Landscape, Pricing, Policies and Regulations, New Product Launches. M&As, Recent Developments Competitive Landscape - Market Share Analysis, Market Leaders, Emerging Players, Vendor Benchmarking, Developmental Strategy Benchmarking, PESTLE Analysis, Value Chain Analysis Company Profiles - Overview, Business Segments, Business Performance, Product Offering, Key Developmental Strategies, SWOT Analysis

With Global Insight Services, you receive:

10-year forecast to help you make strategic decisions In-depth segmentation which can be customized as per your requirements Free consultation with lead analyst of the report Infographic excel data pack, easy to analyze big data Robust and transparent research methodology Unmatched data quality and after sales service

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1-833-761-1700 Website: https://www.globalinsightservices.com/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

0 notes

Text

The Global Polyacrylonitrile Fiber Market is projected to grow from USD 9,150.00 million in 2023 to an estimated USD 13,147.80 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.11% from 2024 to 2032.Polyacrylonitrile (PAN) fibers, known for their superior strength, thermal stability, and chemical resistance, have become an integral component in various industries, including textiles, automotive, and aerospace. As global industries demand lightweight, durable, and cost-effective materials, the polyacrylonitrile fiber market is poised for significant growth. This article explores the current trends, market drivers, challenges, and future opportunities in the polyacrylonitrile fiber sector.

Browse the full report at https://www.credenceresearch.com/report/polyacrylonitrile-fiber-market

Market Overview

Polyacrylonitrile fibers are synthetic fibers derived from acrylonitrile, often used in the production of carbon fiber, which is renowned for its high tensile strength and lightweight properties. These fibers serve as precursors for carbon fiber manufacturing, making them essential in high-performance applications. With a growing focus on renewable energy, green technologies, and sustainability, the demand for PAN fibers is increasing in industries such as wind energy, automotive, and construction.

Key Drivers of Market Growth

Rising Demand for Carbon Fiber Carbon fiber, derived from PAN, has become a material of choice in industries that prioritize lightweight and high-strength materials. Its extensive use in aerospace for building fuel-efficient aircraft and in the automotive industry for lightweight vehicles to improve fuel efficiency has propelled the demand for PAN fibers.

Growth in the Textile Industry Polyacrylonitrile fibers are also used in textiles for manufacturing synthetic wool, thermal insulation fabrics, and outdoor wear. The increasing popularity of functional and performance-driven clothing is driving market expansion in this segment.

Sustainability Initiatives The global emphasis on reducing greenhouse gas emissions has led to increased adoption of carbon-neutral technologies, where PAN-based carbon fibers are instrumental. Renewable energy sectors, particularly wind power, rely on carbon fiber for manufacturing durable and lightweight turbine blades.

Technological Advancements Continuous advancements in polymer processing and fiber production have improved the cost-efficiency and performance of PAN fibers. Emerging methods of recycling and reusing PAN fibers are also gaining traction, aligning with global sustainability goals.

Challenges in the Market

Despite its promising growth prospects, the polyacrylonitrile fiber market faces several challenges:

High Production Costs The manufacturing process of PAN fibers, particularly for carbon fiber production, is energy-intensive and costly. This limits its affordability for some applications, particularly in developing markets.

Environmental Concerns The production of PAN fibers involves the use of toxic chemicals, raising concerns about its environmental impact. Strict environmental regulations may hinder production capabilities in certain regions.

Competition from Alternative Materials Advances in materials science have led to the development of alternative fibers and composites. These alternatives often offer similar or superior properties at lower costs, challenging PAN's market share.

Future Opportunities

The future of the polyacrylonitrile fiber market lies in innovation and sustainability. Companies investing in research to develop low-cost and eco-friendly PAN fibers are likely to gain a competitive edge. Additionally, the growing demand for electric vehicles, which rely on lightweight materials, presents a lucrative opportunity for market players. Emerging markets in Africa and the Middle East also offer untapped potential for PAN fiber applications in construction and energy sectors.

Key players

Shandong Haili

Jilin Chemical Fiber

Sateri

Fibrant

Jiangsu Sailboat Petrochemical

Xinjiang Tianye

Mitsubishi Chemical

Yantai Taihe

Tongkun Group

Samyang Corporation

Segments

Based on Type

Standard PAN

High Modulus PAN

Medium Modulus PAN

Carbon Fiber Precursor PAN

Based on Application

Apparel & Clothing

Automotive & Transportation

Construction

Industrial

Medical

Based on End User

Textiles

Automotive Parts

Construction Material

Industrial Composites

Medical Devices

Based on Yarn Type

Filament Yarn

Staple Fibre

Based on Region

North America

U.S.

Canada

Mexico

Europe

UK

France

Germany

Italy

Spain

Russia

Belgium

Netherlands

Austria

Sweden

Poland

Denmark

Switzerland

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Thailand

Indonesia

Vietnam

Malaysia

Philippines

Taiwan

Rest of Asia Pacific

Latin America

Brazil

Argentina

Peru

Chile

Colombia

Rest of Latin America

Middle East

UAE

KSA

Israel

Turkey

Iran

Rest of Middle East

Africa

Egypt

Nigeria

Algeria

Morocco

Rest of Africa

Browse the full report at https://www.credenceresearch.com/report/polyacrylonitrile-fiber-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Unmanned Composites Market Report

Unmanned Composites Market Report Outlook, Statistical Data & Forecast Analysis by 2031

According to Straits Research, the global Unmanned Composites Market is set for substantial growth, projected to reach USD 5.49 Billion by 2031 at a robust CAGR of 15.51%. This growth is driven by advancements in technology and regional expansions that are reshaping the industry landscape. The report captures this momentum and explores the impact of these developments on global and regional markets specifically.

Market Definition

The Unmanned Composites Market refers to the global market for composite materials used in the manufacture of unmanned systems, including unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), unmanned surface vehicles (USVs), autonomous underwater vehicles (AUVs), remotely operated vehicles (ROVs), autonomous ships, and passenger drones. These composite materials offer exceptional strength-to-weight ratios, corrosion resistance, and durability, making them ideal for use in unmanned systems.

Request a Free Sample (Free Executive Summary at Full Report Starting from USD 1850): https://straitsresearch.com/report/unmanned-composites-market/request-sample

Latest Trends

The Unmanned Composites Market is driven by the increasing demand for lightweight, high-performance materials in unmanned systems. Some of the latest trends in the market include:

Increasing use of carbon fiber reinforced polymers (CFRP): CFRP is widely used in unmanned systems due to its exceptional strength-to-weight ratio, corrosion resistance, and durability.

Growing demand for glass fiber reinforced polymers (GFRP): GFRP is a cost-effective alternative to CFRP and is widely used in unmanned systems that require high strength and durability.

Rising adoption of aramid fiber reinforced polymers (AFRP): AFRP is a high-performance material that offers exceptional strength, stiffness, and resistance to impact and fatigue.

Advancements in manufacturing technologies: Advancements in manufacturing technologies, such as 3D printing and automated fiber placement, are enabling the production of complex composite structures with high accuracy and precision.

Market Insights