#Telemedicine Market Telemedicine Market Growth Telemedicine Market Research Telemedicine Market Share Telemedicine Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. is using 66 technologies for its website.

Text

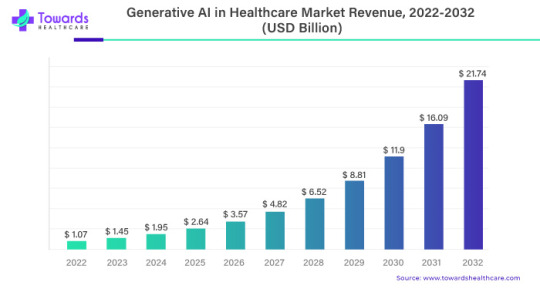

Generative AI in Healthcare Market to Grow at an 35.1% CAGR Till 2032!

The global Generative AI in Healthcare Market worth USD 1.07 billion in 2023 is likely to be USD 21.74 billion by 2032, growing at a 35.1% CAGR between 2023 and 2032.

According to the stats published by World Health Organization (WHO), approximately 1.28 million adults (between 30 and 79 years of age) have hypertension. Of these, as little as 42% of adults are diagnosed and treated correctly and the remaining population is unaware of this condition. The majority of this population resides in low to middle-income countries of the world. Despite this substantial number of untreated cases, the rising awareness among doctors and the general population regarding health illnesses associated with hypertension is expected to drive the demand for the required devices.

Download White Paper@ https://www.towardshealthcare.com/personalized-scope/5069

A recent report provides crucial insights along with application based and forecast information in the Global Generative AI in Healthcare Market. The report provides a comprehensive analysis of key factors that are expected to drive the growth of this Market. This study also provides a detailed overview of the opportunities along with the current trends observed in the Generative AI in Healthcare Market.

A quantitative analysis of the industry is compiled for a period of 10 years in order to assist players to grow in the Market. Insights on specific revenue figures generated are also given in the report, along with projected revenue at the end of the forecast period.

Report Objectives

To define, describe, and forecast the global Generative AI in Healthcare Market based on product, and region

To provide detailed information regarding the major factors influencing the growth of the Market (drivers, opportunities, and industry-specific challenges)

To strategically analyze microMarkets1 with respect to individual growth trends, future prospects, and contributions to the total Market

To analyze opportunities in the Market for stakeholders and provide details of the competitive landscape for Market leaders

To forecast the size of Market segments with respect to four main regions—North America, Europe, Asia Pacific and the Rest of the World (RoW)2

To strategically profile key players and comprehensively analyze their product portfolios, Market shares, and core competencies3

To track and analyze competitive developments such as acquisitions, expansions, new product launches, and partnerships in the Generative AI in Healthcare Market

Companies and Manufacturers Covered

The study covers key players operating in the Market along with prime schemes and strategies implemented by each player to hold high positions in the industry. Such a tough vendor landscape provides a competitive outlook of the industry, consequently existing as a key insight. These insights were thoroughly analysed and prime business strategies and products that offer high revenue generation capacities were identified. Key players of the global Generative AI in Healthcare Market are included as given below:

Generative AI in Healthcare Market Key Players:

Syntegra

NioyaTech

Saxon

IBM Watson

Microsoft Corporation

Google LLC

Tencent Holdings Ltd.

Neuralink Corporation

OpenAI

Oracle

Market Segments :

By Application

Clinical

Cardiovascular

Dermatology

Infectious Disease

Oncology

Others

System

Disease Diagnosis

Telemedicine

Electronic Health Records

Drug Interaction

By Function

AI-Assisted Robotic Surgery

Virtual Nursing Assistants

Aid Clinical Judgment/Diagnosis

Workflow & Administrative Tasks

Image Analysis

By End User

Hospitals & Clinics

Clinical Research

Healthcare Organizations

Diagnostic Centers

Others

By Geography

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

Contact US -

Towards Healthcare

Web: https://www.towardshealthcare.com/

You can place an order or ask any questions, please feel free to contact at

Email: [email protected]

About Us

We are a global strategy consulting firm that assists business leaders in gaining a competitive edge and accelerating growth. We are a provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations.

#seo marketing#seo#market analysis#market share#marketing#ai#artificial intelligence#Generative AI#healthcare

2 notes

·

View notes

Text

Insertable Cardiac Monitors (ICM) Market Trends, Opportunities and Forecast By 2028

The Insertable Cardiac Monitors (ICM) Market sector is undergoing rapid transformation, with significant growth and innovations expected by 2028. In-depth market research offers a thorough analysis of market size, share, and emerging trends, providing essential insights into its expansion potential. The report explores market segmentation and definitions, emphasizing key components and growth drivers. Through the use of SWOT and PESTEL analyses, it evaluates the sector’s strengths, weaknesses, opportunities, and threats, while considering political, economic, social, technological, environmental, and legal influences. Expert evaluations of competitor strategies and recent developments shed light on geographical trends and forecast the market’s future direction, creating a solid framework for strategic planning and investment decisions.

Brief Overview of the Insertable Cardiac Monitors (ICM) Market:

The global Insertable Cardiac Monitors (ICM) Market is expected to experience substantial growth between 2024 and 2031. Starting from a steady growth rate in 2023, the market is anticipated to accelerate due to increasing strategic initiatives by key market players throughout the forecast period.

Get a Sample PDF of Report - https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-insertable-cardiac-monitors-icm-market

Which are the top companies operating in the Insertable Cardiac Monitors (ICM) Market?

The report profiles noticeable organizations working in the water purifier showcase and the triumphant methodologies received by them. It likewise reveals insights about the share held by each organization and their contribution to the market's extension. This Global Insertable Cardiac Monitors (ICM) Market report provides the information of the Top Companies in Insertable Cardiac Monitors (ICM) Market in the market their business strategy, financial situation etc.

Abbott, Medtronic, BioTelemetry, Inc., Siemens, Boston Scientific Corporation, Koninklijke Philips N.V, Shenzhen Mindray Bio-Medical Electronics Co., Ltd, SHL Telemedicine, The ScottCare Corporation, Medicomp Inc., Preventice Solutions, Inc.

Report Scope and Market Segmentation

Which are the driving factors of the Insertable Cardiac Monitors (ICM) Market?

The driving factors of the Insertable Cardiac Monitors (ICM) Market are multifaceted and crucial for its growth and development. Technological advancements play a significant role by enhancing product efficiency, reducing costs, and introducing innovative features that cater to evolving consumer demands. Rising consumer interest and demand for keyword-related products and services further fuel market expansion. Favorable economic conditions, including increased disposable incomes, enable higher consumer spending, which benefits the market. Supportive regulatory environments, with policies that provide incentives and subsidies, also encourage growth, while globalization opens new opportunities by expanding market reach and international trade.

Insertable Cardiac Monitors (ICM) Market - Competitive and Segmentation Analysis:

**Segments**

- By Product Type: Subcutaneous ICM, Transvenous ICM - By Technology: Electrocardiogram (ECG), Optical Fiber, Others - By Indication: Atrial Fibrillation, Bradycardia, Tachycardia, Others - By End-User: Hospitals, Cardiac Clinics, Ambulatory Surgical Centers, Others

The global insertable cardiac monitors (ICM) market is expected to witness significant growth from 2021 to 2028. The increasing prevalence of cardiovascular diseases, coupled with advancements in healthcare technology, is driving the demand for insertable cardiac monitors globally. The market is segmented by product type into subcutaneous ICM and transvenous ICM. Subcutaneous ICMs are non-invasive devices that are implanted just beneath the skin to monitor heart activity, while transvenous ICMs are inserted into the chest wall to monitor heart rhythms more closely. Based on technology, the market is categorized into electrocardiogram (ECG), optical fiber, and others. The ECG segment dominates the market due to its wide usage and effectiveness in detecting cardiac abnormalities. Moreover, the indications for ICMs include atrial fibrillation, bradycardia, tachycardia, among others, with atrial fibrillation holding a significant share owing to its high prevalence globally. Hospitals, cardiac clinics, ambulatory surgical centers, and others are the key end-users of insertable cardiac monitors.

**Market Players**

- Medtronic - Abbott - Biotronik - Boston Scientific Corporation - LivaNova PLC - BIOTRICITY INC. - Medtronic - Koninklijke Philips N.V. - Preventice Solutions, Inc. - Hill-Rom Services Inc.

Leading market players in the global insertable cardiac monitors (ICM) industry are focusing on research and development initiatives to introduce innovative products and strengthen their market presence.The global insertable cardiac monitors (ICM) market is highly competitive, with key players such as Medtronic, Abbott, Biotronik, Boston Scientific Corporation, and LivaNova PLC leading the industry. These companies have a strong focus on research and development to introduce innovative products that cater to the evolving needs of healthcare providers and patients. For instance, Medtronic has been actively involved in developing advanced monitoring solutions to improve the diagnosis and management of cardiac conditions. Abbott, on the other hand, has been instrumental in introducing cutting-edge technologies in the field of cardiac monitoring, enhancing patient outcomes and streamlining healthcare delivery.

In addition to established players, emerging companies like BIOTRICITY INC., Koninklijke Philips N.V., Preventice Solutions, Inc., and Hill-Rom Services Inc. are also making a mark in the insertable cardiac monitor market. These companies are investing in technological advancements to offer novel solutions that address unmet needs in cardiac care. BIOTRICITY INC., for instance, focuses on developing remote monitoring solutions that provide real-time data to healthcare providers, enabling timely interventions and improved patient outcomes. Koninklijke Philips N.V. is known for its expertise in digital health solutions, integrating data analytics and artificial intelligence to enhance diagnostic capabilities in cardiac monitoring.

The market players in the insertable cardiac monitor segment are strategically collaborating with healthcare institutions, research organizations, and regulatory bodies to ensure the successful development and commercialization of their products. By leveraging partnerships and alliances, these companies can access new markets, gain regulatory approvals, and foster innovation in cardiac monitoring technologies. Moreover, mergers and acquisitions are prevalent in the industry as companies look to expand their product portfolios, diversify their customer base, and strengthen their competitive position in the market.

In terms of market dynamics, the growing prevalence of cardiovascular diseases, particularly atrial fibrillation, is a key driver for the insertable cardiac monitor market. As the aging population increases and lifestyle factors contribute to heart-related conditions, the demand for**Market Players**

Abbott, Medtronic, BioTelemetry, Inc., Siemens, Boston Scientific Corporation, Koninklijke Philips N.V, Shenzhen Mindray Bio-Medical Electronics Co., Ltd, SHL Telemedicine, The ScottCare Corporation, Medicomp Inc., Preventice Solutions, Inc.

The global insertable cardiac monitor market is witnessing significant growth due to the rising prevalence of cardiovascular diseases and technological advancements in healthcare. The market is segmented by product type, technology, indication, and end-user, providing a comprehensive overview of the industry landscape. Subcutaneous ICMs and transvenous ICMs offer unique monitoring capabilities, with ECG technology being the dominant choice for cardiac monitoring. Atrial fibrillation, bradycardia, and tachycardia are among the key indications for ICMs, with atrial fibrillation driving a substantial share of the market. Hospitals, cardiac clinics, and ambulatory surgical centers serve as primary end-users for insertable cardiac monitors.

Leading market players such as Medtronic, Abbott, and Boston Scientific Corporation are at the forefront of innovation in the ICM industry. These companies invest heavily in research and development to introduce cutting-edge products that cater to the evolving needs of healthcare providers and patients. Collaborations with healthcare institutions and regulatory bodies are crucial for product development and market expansion. Emerging players like Preventice Solutions, Inc. and Koninklijke Philips N.V. are also making significant strides in the market by focusing

North America, particularly the United States, will continue to exert significant influence that cannot be overlooked. Any shifts in the United States could impact the development trajectory of the Insertable Cardiac Monitors (ICM) Market. The North American market is poised for substantial growth over the forecast period. The region benefits from widespread adoption of advanced technologies and the presence of major industry players, creating abundant growth opportunities.

Similarly, Europe plays a crucial role in the global Insertable Cardiac Monitors (ICM) Market, expected to exhibit impressive growth in CAGR from 2024 to 2028.

Explore Further Details about This Research Insertable Cardiac Monitors (ICM) Market Report https://www.databridgemarketresearch.com/reports/global-insertable-cardiac-monitors-icm-market

Key Benefits for Industry Participants and Stakeholders: –

Industry drivers, trends, restraints, and opportunities are covered in the study.

Neutral perspective on the Insertable Cardiac Monitors (ICM) Market scenario

Recent industry growth and new developments

Competitive landscape and strategies of key companies

The Historical, current, and estimated Insertable Cardiac Monitors (ICM) Market size in terms of value and size

In-depth, comprehensive analysis and forecasting of the Insertable Cardiac Monitors (ICM) Market

Geographically, the detailed analysis of consumption, revenue, market share and growth rate, historical data and forecast (2024-2031) of the following regions are covered in Chapters

The countries covered in the Insertable Cardiac Monitors (ICM) Market report are U.S., Canada and Mexico in North America, Brazil, Argentina and Rest of South America as part of South America, Germany, Italy, U.K., France, Spain, Netherlands, Belgium, Switzerland, Turkey, Russia, Rest of Europe in Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA

Detailed TOC of Insertable Cardiac Monitors (ICM) Market Insights and Forecast to 2028

Part 01: Executive Summary

Part 02: Scope Of The Report

Part 03: Research Methodology

Part 04: Insertable Cardiac Monitors (ICM) Market Landscape

Part 05: Pipeline Analysis

Part 06: Insertable Cardiac Monitors (ICM) Market Sizing

Part 07: Five Forces Analysis

Part 08: Insertable Cardiac Monitors (ICM) Market Segmentation

Part 09: Customer Landscape

Part 10: Regional Landscape

Part 11: Decision Framework

Part 12: Drivers And Challenges

Part 13: Insertable Cardiac Monitors (ICM) Market Trends

Part 14: Vendor Landscape

Part 15: Vendor Analysis

Part 16: Appendix

Browse More Reports:

Japan: https://www.databridgemarketresearch.com/jp/reports/global-insertable-cardiac-monitors-icm-market

China: https://www.databridgemarketresearch.com/zh/reports/global-insertable-cardiac-monitors-icm-market

Arabic: https://www.databridgemarketresearch.com/ar/reports/global-insertable-cardiac-monitors-icm-market

Portuguese: https://www.databridgemarketresearch.com/pt/reports/global-insertable-cardiac-monitors-icm-market

German: https://www.databridgemarketresearch.com/de/reports/global-insertable-cardiac-monitors-icm-market

French: https://www.databridgemarketresearch.com/fr/reports/global-insertable-cardiac-monitors-icm-market

Spanish: https://www.databridgemarketresearch.com/es/reports/global-insertable-cardiac-monitors-icm-market

Korean: https://www.databridgemarketresearch.com/ko/reports/global-insertable-cardiac-monitors-icm-market

Russian: https://www.databridgemarketresearch.com/ru/reports/global-insertable-cardiac-monitors-icm-market

Data Bridge Market Research:

Today's trends are a great way to predict future events!

Data Bridge Market Research is a market research and consulting company that stands out for its innovative and distinctive approach, as well as its unmatched resilience and integrated methods. We are dedicated to identifying the best market opportunities, and providing insightful information that will help your business thrive in the marketplace. Data Bridge offers tailored solutions to complex business challenges. This facilitates a smooth decision-making process. Data Bridge was founded in Pune in 2015. It is the product of deep wisdom and experience.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 1985

Email:- [email protected]

#Insertable Cardiac Monitors (ICM) Market Size#Insertable Cardiac Monitors (ICM) Market Shares#Insertable Cardiac Monitors (ICM) Market Forecast#Insertable Cardiac Monitors (ICM) Market Growth#Insertable Cardiac Monitors (ICM) Market Demand

0 notes

Text

U.S. Hospice Market: Key Trends and Innovations Driving Industry Growth

The U.S. hospice market size is expected to reach USD 65.0 billion by 2030, growing at a CAGR of 8.07% from 2024 to 2030, according to a new report by Grand View Research, Inc. Growth can be attributed to the growing geriatric population and the increasing prevalence of chronic disorders amid this demographic. The rising demand for end-of-life care for chronic disorders, such as cancer, dementia, and cardiovascular disease, drives the growth of the industry. According to NHPCO statistics, in 2020, 1.72 million Medicare beneficiaries in the U.S. received hospice services for at least one day or more. Enrollment rate increased by around 6.8% from 2019.

The adoption of new technologies among providers is constantly growing. This includes bringing services to rural areas and demonstrating how technology is transforming the approach to care. Many service providers have begun to deploy technology such as telemedicine, predictive analytics, virtual reality, and artificial intelligence. For instance, in March 2023, WorldView partnered with care coordinations to design a solution to transform home health & hospice care delivery by integrating automation and patient engagement.

The COVID-19 pandemic negatively impacted the market by affecting long-term projections and operational goals of the industry in the U.S. providers reported the lowest share of Medicare decedents enrolled for care since 2013, owing to the death rate outpacing the increase in enrollment rate. According to NHPCO data, in 2020, around 47.8% of Medicare decedents received hospice care in the U.S., much lower than around 51.6% in 2019. Currently, these centers are adopting advanced technologies due to patients refusing in-person visits during the COVID-19 pandemic. This is expected to drive market growth post-pandemic.

Gather more insights about the market drivers, restrains and growth of the U.S. Hospice Market

U.S. Hospice Market Report Highlights

• Based on location, hospice center segment dominated the market, with the largest revenue share of around 60% in 2023. This can be attributed to several benefits offered by these centers. In addition, growing awareness regarding various advantages, such as 24/7 availability of professional care and emotional support from family members, is projected to propel market growth

• Based on type, the routine home care (RHC) held the largest market share of around 90% in 2023, owing to the vast majority of Medicare days of care. According to NHPCO statistics, in 2020, around 92.7% of Medicare days of care were at RHC facilities

• Based on diagnosis, the dementia segment dominated the market with a revenue share of around 25% in 2023. This can be attributed to the growing need for care and high prevalence of the condition

U.S. Hospice Market Segmentation

Grand View Research has segmented the U.S. hospice market based on location, type, and diagnosis:

U.S. Hospice Type Outlook (Revenue, USD Billion, 2018 - 2030)

• Routine Home Care

• Continuous Home Care

• Inpatient Respite Care

• General Inpatient Care

U.S. Hospice Location Outlook (Revenue, USD Billion, 2018 - 2030)

• Hospice Center

• Hospital

• Home Hospice Care

• Skilled Nursing Facility

U.S. Hospice Diagnosis Outlook (Revenue, USD Billion, 2018 - 2030)

• Dementia

• Circulatory/Heart

• Cancer

• Respiratory

• Stroke

• Chronic Kidney Disease

• Others

Order a free sample PDF of the U.S. Hospice Market Intelligence Study, published by Grand View Research.

#U.S. Hospice Market#U.S. Hospice Market Size#U.S. Hospice Market Share#U.S. Hospice Market Analysis#U.S. Hospice Market Growth

0 notes

Text

Veterinary Biomarkers Market Report: Opportunities and Challenges in Diagnostics

The global veterinary biomarkers market size is expected to reach USD 2.04 billion by 2030, expanding at 12.61% CAGR from 2023 to 2030, according to a new report by Grand View Research, Inc. The key drivers for the market growth are the increasing prevalence of numerous acute and chronic disorders among animals coupled with the growing demand for better & accurate diagnostic and monitoring technologies. According to the American Veterinary Medical Association, almost half of the dog population is developing cancer at the same rate as humans. This supports the requirement for biomarker-based specific diagnostic kits for timely disease predictions and treatments.

The COVID-19 pandemic created barriers and challenges in the global animal health industry that include decreased marketing & sales activities, low veterinary clinic admission, cancellation of routine pet check-ups, and a low number of disease diagnostic tests performed in veterinary hospitals. However, governments and veterinary organizations of various countries implemented strategies and safety measures to resume veterinary practices and research during the pandemic. According to the American Veterinary Medical Association, telemedicine services were widely incorporated in veterinary clinics and hospitals to curb the impact of lockdowns. Furthermore, the pet parents were given digital training to use certain diagnostic kits.

The increasing animal care expenditure in both developing and developed economies is a significant opportunity for market growth. According to the American Kennel Club (AKC), pet owners in the U.S. were spending more money on their pet’s wellness and related healthcare products. The American Pet Products Association reported that the overall pet industry sale exceeded USD 140 billion by the end of 2022. In addition, the research and development activity in the upcoming fields, such as biomarkers in the veterinary, has been significantly growing over the last decade. These factors are expected to boost the growth of the market.

Veterinary Biomarkers Market Report Highlights

The veterinary biomarkers industry was estimated to be USD 797.3 million in 2022 and is expected to have lucrative growth at a CAGR of 12.61% over the forecast period

The companion animals segment is anticipated to dominate with the highest market share based on animal type during the forecast period. This is owing to the growing adoption rates of dogs and cats in global households coupled with the significant prevalence of diseases and accurate diagnostic requirements among them

Based on the product type, the biomarkers, kits & reagents segment has dominated the market in 2022 with a significant share. This is owing to the growing emergence of post-genomic technologies such as transcriptomics, proteomics, and metabolomics which rises the identification of numerous specific biomarkers for novel point-of-care test kit developments

Based on the application, the disease diagnostics segment has dominated the market in 2022 with the highest share. This is owing to the increasing number of biomarker-based diagnostic test kits launched by key players coupled with the enhanced usage of such kits in veterinary clinics and hospitals

The inflammatory & infectious diseases segment held the largest share of about 35% of the market in 2022 by disease type. This is owing to the high prevalence of inflammatory and infectious diseases among companion and production animals, coupled with a significant number of protein indicators identified for the diseases

By region, North America has dominated the market with a share of over 35% in 2022, while the Asia Pacific market is anticipated to grow the fastest in the coming years. The economic, social, and technological advancements in the North American region are boosting the development of veterinary care in its countries

The market is emerging with the presence of major animal health key players such as Merck & Co., Inc.; Zoetis; Virbac; and IDEXX Laboratories, Inc., among others. The implementation of strategic initiatives by companies, such as acquisitions, collaborations, partnerships, and product launches are, greatly contributing to the growth of the market

Veterinary Biomarkers Market Segmentation

Grand View Research has segmented the global veterinary biomarkers market based on animal type, product type, application, disease type, and region:

Veterinary Biomarkers Animal Type Outlook (Revenue, USD Million, 2018 - 2030)

Companion Animals

Dogs

Cats

Others

Production Animals

Cows

Pigs

Others

Veterinary Biomarkers Product Type Outlook (Revenue, USD Million, 2018 - 2030)

Biomarkers, Kits & Reagents

Biomarker Readers

Veterinary Biomarkers Application Outlook (Revenue, USD Million, 2018 - 2030)

Disease Diagnostics

Preclinical Research

Others

Veterinary Biomarkers Disease Type Outlook (Revenue, USD Million, 2018 - 2030)

Inflammatory & Infectious Diseases

Cardiovascular Diseases

Skeletal Muscle Diseases

Tumor

Others

Veterinary Biomarkers Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Europe

Germany

UK

France

Italy

Spain

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

MEA

South Africa

Saudi Arabia

Order a free sample PDF of the Veterinary biomarkers Market Intelligence Study, published by Grand View Research.

0 notes

Text

Optometry Equipment Market

Optometry Equipment Market Size, Share, Trends: Carl Zeiss Meditec AG Leads

Integration of AI and Telemedicine in Optometry Equipment Enhances Diagnostic Capabilities

Market Overview:

The Optometry Equipment Market is estimated to grow at a 5.6% CAGR from 2024 to 2031. North America currently dominates the market, accounting for the vast majority of global sales. Key factors include an increase in the prevalence of eye diseases, technological advancements in diagnostic equipment, and increasing awareness of eye health. The industry is quickly developing as the global prevalence of visual issues and eye diseases rises. Technological innovations, such as the introduction of artificial intelligence into diagnostic devices, are propelling the market forward. Furthermore, the growing geriatric population and rising healthcare costs in developing countries are fueling market growth.

DOWNLOAD FREE SAMPLE

Market Trends:

The combination of artificial intelligence (AI) and telemedicine solutions is becoming increasingly common in the optometry equipment business. The increased demand for remote eye care services, as well as the need for more precise and economical diagnostic technology, are driving this development. AI-enabled optometry equipment can evaluate complex eye imaging data, discover minor issues, and provide timely, accurate diagnoses. Telemedicine integration enables remote eye examinations and consultations, improving access to eye care services in underserved areas. Manufacturers are investing heavily in R&D to develop smart optometry equipment that can seamlessly integrate with telemedicine platforms, enhancing patient outcomes and streamlining eye care delivery.

Market Segmentation:

The optical coherence tomography (OCT) systems segment leads the optometry equipment market. OCT technology provides high-resolution cross-sectional imaging of the retina and other eye components, making it a valuable tool for diagnosing and monitoring a wide range of eye problems. Recent developments in OCT technology, such as swept-source OCT and OCT angiography, have expanded these systems' capabilities, enabling more comprehensive imaging of deeper eye structures and blood flow analysis. According to research published in the Journal of Ophthalmology, OCT-based screening found early indications of glaucoma in 15% more cases than traditional techniques, highlighting its clinical value.

Market Key Players:

The optometry equipment sector is highly competitive, with a focus on technological innovation and strategic alliances. Leading companies such as Carl Zeiss Meditec AG, Topcon Corporation, Nidek Co., Ltd., Essilor International S.A., Hoya Corporation, and Alcon, Inc. dominate the market. These firms invest heavily in R&D to diversify their product portfolios and gain a competitive advantage.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

South Korea Smart Healthcare Market Size, Share, Trends, Growth, & Report | 2024-2032

The healthcare industry is undergoing a significant transformation with the advent of smart technologies. South Korea, known for its technological advancements and robust healthcare infrastructure, is at the forefront of this change. The south korea smart healthcare market in South Korea is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.1% from 2024 to 2032. This growth is driven by government initiatives aimed at digitalising the healthcare system and a growing emphasis on research and development.

South Korea’s Smart Healthcare Market

South Korea's healthcare system is widely recognised for its advanced medical technology, high-quality care, and efficient delivery. With the integration of smart technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), and data analytics, the country is poised to revolutionise the healthcare landscape. The government's policies and investments in healthcare innovation are also contributing significantly to the market's growth.

Smart healthcare refers to the use of cutting-edge technologies to enhance healthcare services, making them more efficient, personalised, and accessible. These technologies include remote monitoring systems, telemedicine, health apps, and AI-driven diagnostic tools, which are increasingly being adopted by hospitals, healthcare providers, and consumers alike.

Get a Free Sample Report with Table of Contents : https://www.expertmarketresearch.com/reports/south-korea-smart-healthcare-market/requestsample

Factors Driving the Growth of South Korea’s Smart Healthcare Market

Government Initiatives in Digital HealthcareThe South Korean government has been proactive in promoting digitalisation in healthcare. The government has rolled out several initiatives to integrate smart technologies into the healthcare sector, such as the "Digital Healthcare Master Plan," which aims to make South Korea a global leader in digital healthcare innovation. The government is also encouraging private sector involvement and collaboration in the development and deployment of smart healthcare solutions.

Rising Demand for Healthcare ServicesSouth Korea’s rapidly ageing population is contributing to the growing demand for healthcare services. The country has one of the fastest ageing populations in the world, and this demographic shift is creating a significant need for innovative healthcare solutions. Smart healthcare technologies are helping address the needs of elderly patients by offering remote monitoring, telemedicine consultations, and personalised care plans.

Research and DevelopmentSouth Korea is investing heavily in research and development (R&D) in the healthcare sector. Leading universities and research institutions in South Korea are focusing on innovations in AI, big data analytics, and telemedicine. These advancements are not only improving the quality of healthcare but are also driving the growth of the smart healthcare market by offering new and improved solutions for patients and healthcare providers.

Increasing Prevalence of Chronic DiseasesChronic diseases such as diabetes, hypertension, and cardiovascular conditions are on the rise in South Korea. Managing these diseases requires constant monitoring and intervention, making smart healthcare solutions particularly appealing. Wearable devices, smart monitoring systems, and AI-based diagnostic tools are increasingly being used to manage and prevent chronic diseases, contributing to the growth of the market.

Technological AdvancementsThe continuous development of AI, IoT, and other digital technologies is a major driver of the smart healthcare market. AI-powered diagnostic tools, robotic surgery, and smart devices for monitoring vital signs are transforming the healthcare delivery model in South Korea. These technologies are improving patient outcomes, enhancing operational efficiency, and reducing costs.

Key Technologies in South Korea’s Smart Healthcare Market

TelemedicineTelemedicine allows healthcare providers to offer remote consultations and care, reducing the need for in-person visits. This technology has gained significant traction, especially in rural areas where access to healthcare services may be limited. It enables patients to receive consultations and follow-up care from the comfort of their homes, improving accessibility and convenience.

Wearable Health DevicesWearable health devices such as smartwatches, fitness trackers, and health-monitoring sensors are becoming increasingly popular in South Korea. These devices can track a wide range of health parameters, including heart rate, blood pressure, sleep patterns, and physical activity levels. The data collected from these devices can be used to monitor chronic conditions, alert healthcare providers to potential health issues, and promote preventive care.

AI and Machine LearningArtificial Intelligence (AI) is revolutionising healthcare in South Korea. AI algorithms are being used for early diagnosis, personalised treatment plans, and predictive analytics. AI is also playing a crucial role in medical imaging, where machine learning models can identify anomalies in X-rays, MRIs, and CT scans faster and more accurately than human doctors.

Robotic SurgeryRobotic surgery systems, such as the da Vinci Surgical System, are being increasingly adopted in South Korea. These advanced systems offer greater precision, reduce the risk of complications, and shorten recovery times. Robotic surgery allows for minimally invasive procedures that result in fewer scars, less pain, and faster healing.

Big Data AnalyticsBig data analytics is helping healthcare providers in South Korea make more informed decisions. By analysing large volumes of health data, providers can identify trends, predict patient outcomes, and improve overall care. Big data analytics is also being used to optimise hospital management and enhance the efficiency of healthcare delivery.

Challenges Facing the Smart Healthcare Market in South Korea

Privacy and Data Security ConcernsAs the use of digital technologies increases, so does the risk of data breaches and privacy concerns. Patient data is highly sensitive, and ensuring its security is crucial for the success of the smart healthcare market. South Korea’s healthcare sector must invest in robust cybersecurity measures to protect patient information.

Regulatory HurdlesThe regulatory framework for smart healthcare technologies is still evolving. While South Korea is known for its regulatory efficiency, the fast pace of technological advancement means that there is often a gap between the introduction of new technologies and the establishment of regulations governing their use. This can delay the widespread adoption of new innovations.

High Initial CostsImplementing smart healthcare technologies can be costly, especially for small and medium-sized healthcare providers. The high upfront costs of purchasing and integrating new technologies can be a barrier to entry for many organisations, especially in a market that is still developing.

Healthcare Professional TrainingHealthcare professionals need to be trained to effectively use new technologies. The integration of AI, robotics, and telemedicine into everyday healthcare practice requires a significant shift in how healthcare professionals approach their work. Training and upskilling are essential to ensure that these technologies are used effectively and safely.

Key Players in South Korea’s Smart Healthcare Market

Several key players are driving the growth of South Korea's smart healthcare market, ranging from established healthcare providers to technology companies. Here are some of the leading players in this market:

Samsung ElectronicsSamsung Electronics, based in Suwon, South Korea, is a global leader in electronics and smart devices, including healthcare technologies. Samsung has been heavily involved in the development of wearable health devices, such as the Galaxy Watch, which includes health-monitoring features like heart rate tracking and ECG functionality. Samsung’s expertise in IoT and AI positions it as a major player in the smart healthcare market.

LG ElectronicsLG Electronics, also headquartered in South Korea, has been developing healthcare solutions through its wearable devices and health monitoring technologies. LG’s focus on integrating AI with healthcare applications has made it a key player in the growing smart healthcare market. The company is working on innovations that leverage AI to improve patient care, hospital management, and health outcomes.

SK TelecomSK Telecom, a leading telecommunications company in South Korea, is involved in the smart healthcare sector by providing IoT-based solutions for remote patient monitoring, telemedicine, and health data analytics. SK Telecom is focusing on expanding its smart healthcare services and providing hospitals and healthcare providers with advanced digital solutions.

MedtronicMedtronic, a global leader in medical devices, operates in South Korea, offering advanced medical technologies and smart healthcare solutions. The company’s products range from minimally invasive devices to diagnostic and monitoring systems, contributing to the overall growth of the smart healthcare market in South Korea.

Hana HealthcareHana Healthcare, a prominent player in South Korea’s healthcare industry, is known for its innovations in the development of telemedicine and health apps. The company focuses on delivering healthcare services through digital platforms, enabling patients to receive consultations, prescriptions, and health advice remotely.

Kakao HealthcareKakao Healthcare, a subsidiary of the Kakao Corporation, is leveraging its expertise in digital platforms to create healthcare services that are more accessible and efficient. Kakao Healthcare is focused on integrating AI and big data analytics to enhance patient care and health management in South Korea.

FAQs

What is smart healthcare?Smart healthcare refers to the integration of digital technologies such as AI, IoT, and big data into healthcare services. These technologies aim to improve patient care, enhance operational efficiency, and make healthcare more accessible and affordable.

What are the key factors driving the growth of the South Korea smart healthcare market?The key drivers include government initiatives to digitalise healthcare, an ageing population, rising chronic disease prevalence, advancements in technology, and significant investments in research and development.

What are the challenges facing the smart healthcare market in South Korea?The main challenges include privacy and data security concerns, regulatory hurdles, high initial costs, and the need for healthcare professional training to use new technologies effectively.

Which companies are leading the smart healthcare market in South Korea?Key players include Samsung Electronics, LG Electronics, SK Telecom, Medtronic, Hana Healthcare, and Kakao Healthcare, all of which are contributing significantly to the development of smart healthcare technologies in South Korea.

What technologies are driving smart healthcare in South Korea?The main technologies include telemedicine, wearable health devices, AI and machine learning, robotic surgery, and big data analytics.

0 notes

Link

0 notes

Text

Parkinson’s Disease Treatment market Size, Share, Trends & Forecast 2025-2035

Parkinson's Disease Treatment Market Overview

The Parkinson’s Disease Treatment market was valued at USD 6.4 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 10.2%, reaching USD 18.6 billion by 2035. This market includes medications such as dopaminergic drugs (e.g., levodopa), non-dopaminergic therapies, surgical treatments like deep brain stimulation, and supportive therapies. Growth is driven by rising disease prevalence, advancements in treatment technologies, and increased diagnostic rates.

Key Market Insights ·Largest Market: North America leads due to advanced treatments and robust R&D investments. ·Fastest Growing Region: Europe, supported by healthcare spending and aging demographics.

·Major Segments: oTreatment Type: Non-surgical treatments dominate, with oral medications being preferred for their convenience and lower cost.

oRoute of Administration: Oral drugs, such as levodopa, are the most popular. ·Challenges: Despite progress, most treatments focus on symptom management rather than a cure, limiting long-term growth. High treatment costs further strain healthcare systems, particularly in developing countries.

Market Dynamics Drivers: oExpanding healthcare infrastructure and rising awareness of Parkinson’s disease. oIncreased R&D investments in innovative therapies, including neuroprotective agents and personalized medicine. oIntegration of digital health solutions like telemedicine and mobile apps to improve patient care. Opportunities: oBiomarker development enables early diagnosis and personalized treatments, improving patient outcomes. oPatient-centric approaches based on genetic data are driving innovation, enhancing treatment effectiveness and reducing side effects. Restraints: oLack of curative therapies limits market potential. oThe diversity in symptoms and progression rates complicates treatment standardization. Competitive Landscape Leading companies like AbbVie, Teva Pharmaceuticals, and Lundbeck are investing in novel therapies. For instance, AbbVie’s Tavapadon showed promising results in Phase 3 trials as a Parkinson’s monotherapy. Medtronic’s ADAPT-PD clinical trial is setting new benchmarks in neuromodulation research. Collaborations, such as Roche’s partnerships with biotech firms, highlight the industry’s focus on innovation. Regional Trends ·North America: Advanced drug formulations and neuromodulation technologies drive market dominance. ·Europe: Government-backed R&D and increasing adoption of personalized care models propel growth. ·Asia-Pacific: Rising healthcare expenditure and aging populations are boosting demand for treatments. Conclusion The Parkinson’s Disease Treatment market shows promising growth fueled by technological advancements, personalized medicine, and global advocacy for improved care solutions. However, addressing challenges like symptom-focused therapies and high costs will be essential for sustained growth. Get sample report for more detailed insights https://www.metatechinsights.com/request-sample/1176

0 notes

Text

High-Resolution Anoscopy Market 2024 : Industry Analysis, Trends, Segmentation, Regional Overview And Forecast 2033

The high-resolution anoscopy global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

High-Resolution Anoscopy Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The high-resolution anoscopy market size has grown strongly in recent years. It will grow from $13.97 billion in 2023 to $15.03 billion in 2024 at a compound annual growth rate (CAGR) of 7.6%. The growth in the historic period can be attributed to increased prevalence of anal dysplasia, advancements in endoscopy technology, growing awareness and screening, colorectal cancer screening.

The high-resolution anoscopy market size is expected to see strong growth in the next few years. It will grow to $19.38 billion in 2028 at a compound annual growth rate (CAGR) of 6.6%. The growth in the forecast period can be attributed to global health initiatives, expanded access to specialized care, personalized medicine, telemedicine and remote consultations. Major trends in the forecast period include ai-assisted diagnostics, portable hra devices, digital records and telehealth, home-based hra kits.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/high-resolution-anoscopy-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers - The increasing prevalence of cancer is expected to propel the growth of the high resolution anoscopy market. Cancer is a complex group of diseases characterized by the uncontrolled growth and division of abnormal cells. High-resolution anoscopy can provide high-quality imaging using a colposcope or operating microscope, allowing for more precise observations and evaluation of the anal canal. This medical equipment aids in detecting cancerous lesions or abnormalities within the anal tract. For instance, according to the Cancer Facts and Figures 2023 report published by the American Cancer Society, a US-based professional organization, the number of new anal cancer cases reported in the United States is 9,760, compared to 9,440 cases in 2022. Additionally, the number of deaths attributed to anal cancer rose to 1,870, a rise from the 1,670 deaths recorded in 2022. Therefore, the increasing prevalence of cancer is driving the growth of the disposable endoscopes market.

Market Trends - Major Companies operating in the high-resolution anoscopy market are adopting new technologies, such as computer-aided cervical mapping technology, to provide treatment-related services to their customers and sustain their position in the market. Computer-aided colposcopy combined with cervical mapping is an innovative device that generates data to assist healthcare workers in quickly detecting cervical abnormalities. For instance, in July 2021, DYSIS Medical Inc., a US-based medical technology company specializing in developing colposcopy devices, launched DYSIS View colposcope. It is an out-of-the-box ready, compact and portable colposcope that offers a convenient solution for healthcare professionals performing colposcopy exams. It includes the company's innovative computer-aided cervical mapping technology that generates data to help healthcare professionals detect and assess cervical lesions. DYSIS View has a camera to capture high-resolution videos and photos and quick playback of colposcopy tests. It has DYSIS SMARTtrack to compare a patient's DYSIS View colposcopy exams and a patient database for safe records.

The high-resolution anoscopy market covered in this report is segmented –

1) By Product Type: Colposcopes; Portable Colposcope; Hand-Held Colposcope; Anoscopes; Disposable Anoscope; Reusable Anoscope 2) By Patient Population: Adults; Pediatrics 3) By End Use: Hospitals; Diagnostic Laboratories; Specialty Clinics

Get an inside scoop of the high-resolution anoscopy market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=13011&type=smp

Regional Insights - North America was the largest region in the high-resolution anoscopy market in 2023. The regions covered in high-resolution anoscopy market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

Key Companies - Major players in the high-resolution anoscopy market are Philips Medical Systems Technologies Ltd., Olympus Corporation, Hoya Corporation, Steris PLC, Allegheny Health Network, Karl Storz SE & Co. KG, CooperSurgical, Ecleris S.R.L, Pentax Medical, Fujifilm Medical Systems, Given Imaging, Carl Zeiss Meditec AG, Bovie Medical Corporation, Hill-Rom Holdings Inc., Optomic, Narang Medical Limited, Medorah Meditek Pvt Ltd., Welch Allyn, Leisegang Feinmechanik Optik GmbH, Medimar S.A., DYSIS Medical, Gynius Plus AB, Lutech Medical, Ottomed Endoscopy, Seiler Garepa Pvt. Ltd.

Table of Contents 1. Executive Summary 2. High-Resolution Anoscopy Market Report Structure 3. High-Resolution Anoscopy Market Trends And Strategies 4. High-Resolution Anoscopy Market – Macro Economic Scenario 5. High-Resolution Anoscopy Market Size And Growth ….. 27. High-Resolution Anoscopy Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Progressive Pulmonary Fibrosis (PPF) represents a subset of interstitial lung diseases (ILDs) characterized by chronic and progressive scarring of lung tissue, leading to respiratory decline. As the condition progresses, patients experience increasing breathlessness and reduced quality of life. The growing awareness of PPF, coupled with advancements in diagnostics and treatment, has fueled significant growth in the PPF treatment market. This article explores the market landscape, emerging trends, and future opportunities within this domain.

Browse the full report at https://www.credenceresearch.com/report/progressive-pulmonary-fibrosis-ppf-treatment-market

Market Overview

The PPF treatment market is poised for substantial growth, driven by the rising prevalence of fibrotic lung diseases. According to recent data, idiopathic pulmonary fibrosis (IPF) affects approximately 3 million people worldwide, with a significant portion progressing to PPF. Additionally, other forms of ILD, such as chronic hypersensitivity pneumonitis and connective tissue disease-associated ILD, contribute to the disease burden.

The introduction of antifibrotic therapies has transformed the treatment landscape. Medications like pirfenidone and nintedanib, originally developed for IPF, are now being repurposed and studied for their efficacy in treating other forms of PPF. These drugs aim to slow disease progression and improve patient outcomes, though they do not cure the condition.

Key Market Drivers

Rising Disease Awareness: Improved diagnostic capabilities and awareness campaigns have led to earlier identification of PPF, enabling timely intervention. This has driven demand for effective treatments.

Advancements in Research: Significant investment in understanding the underlying mechanisms of fibrosis has accelerated the development of targeted therapies. Research into biomarkers and personalized medicine holds promise for more effective and tailored treatments.

Regulatory Approvals and Guidelines: Regulatory bodies like the FDA and EMA have recognized the need for effective PPF treatments, facilitating faster approval pathways for promising therapies. Updated guidelines emphasizing the role of antifibrotics in PPF management have further supported market growth.

Aging Population: The global aging population is at increased risk of developing ILDs, including PPF, due to cumulative environmental exposures and age-related changes in lung function.

Challenges

Despite its growth potential, the PPF treatment market faces several challenges:

High Cost of Treatment: Antifibrotic drugs are expensive, limiting accessibility for patients in low- and middle-income countries.

Side Effects: The adverse effects associated with current therapies, such as gastrointestinal disturbances and liver toxicity, can impact patient adherence.

Diagnostic Complexity: Differentiating PPF from other lung diseases remains challenging, often delaying treatment initiation.

Emerging Trends

Combination Therapies: Researchers are exploring the potential of combining antifibrotic drugs with immunomodulators or anti-inflammatory agents to enhance efficacy.

Biologics and Gene Therapy: The use of biologics targeting specific pathways involved in fibrosis, such as TGF-beta signaling, is gaining traction. Additionally, gene therapy approaches offer hope for halting or reversing disease progression.

Digital Health Tools: Wearable devices and telemedicine platforms are being integrated into PPF management to monitor disease progression and improve patient outcomes.

Clinical Trials and Collaboration: Pharmaceutical companies are increasingly collaborating with academic institutions and biotech firms to expedite drug discovery and clinical trials.

Future Outlook

The PPF treatment market is on the cusp of transformative growth, underpinned by innovations in drug development and a deeper understanding of disease mechanisms. Strategic partnerships between stakeholders, coupled with supportive regulatory frameworks, are expected to further accelerate market expansion. However, addressing barriers such as high treatment costs and diagnostic delays will be critical to unlocking the full potential of this market.

Key Player Analysis

Bristol-Myers Squibb

FibroGen

Pliant Therapeutics, Inc.

Boehringer Ingelheim

Hoffmann-La Roche Ltd

Merck & Co., Inc.

United Therapeutics Corporation

Novartis AG

Galapagos

Prometic Life Sciences Inc.

Segments:

Based on Treatment Type:

MAPK Inhibitor

Tyrosine Inhibitor

Autotaxin Inhibitors

Based on Distribution Channel:

Hospital Pharmacies

Online Pharmacies

Based on Treatment:

Self-Care

Medicines

Pirfenidone

Nintedanib

Others

Lung Transplant

Palliative Care

Based on the Geography:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/progressive-pulmonary-fibrosis-ppf-treatment-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Global Premature Ejaculation Treatment Market Analysis 2024: Size Forecast and Growth Prospects

The premature ejaculation treatment global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Premature Ejaculation Treatment Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The premature ejaculation treatment market size has grown strongly in recent years. It will grow from $3.53 billion in 2023 to $3.88 billion in 2024 at a compound annual growth rate (CAGR) of 10.0%. The growth in the historic period can be attributed to increasing prevalence of premature ejaculation, growing awareness and reduced stigma, physician and patient education, changing societal attitudes toward sexual health, expansion of telemedicine services, pharmaceutical industry initiatives..

The premature ejaculation treatment market size is expected to see strong growth in the next few years. It will grow to $5.62 billion in 2028 at a compound annual growth rate (CAGR) of 9.7%. The growth in the forecast period can be attributed to continued focus on sexual health, individualized treatment approaches, global efforts to address sexual dysfunction, online health platforms and apps, increased openness in healthcare discussions.. Major trends in the forecast period include rise in behavioral and psychosexual therapies, development of novel topical therapies, advancements in pharmacological treatments, integration of telemedicine and online platforms, focus on patient education and counseling, research on novel mechanisms of action..

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/premature-ejaculation-treatment-global-market-report

Scope Of Premature Ejaculation Treatment Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Premature Ejaculation Treatment Market Overview

Market Drivers - The increasing prevalence of sexual disorders is expected to propel the growth of the premature ejaculation treatment market going forward. Sexual disorder or dysfunction refers to the difficulty faced by both men and women during any phase of regular intimate activity. Premature ejaculation is a sexual disorder where premature ejaculation treatment involving medications or therapeutic approaches addresses and controls this condition. For instance, in November 2021, according to a survey of 2,000 UK adults conducted by Pharmacy Direct GB, a UK-based online pharmacy, around 48% of UK residents reported experiencing erectile dysfunction, representing about 16.5 million individuals. The National Health Service spent over $17,9 million (£13 million) for Erectile Dysfunction treatment prescriptions in 2021. Further, in July 2022, according to a survey of 1,000 men across the UK by Click2Pharmacy, a UK-based provider of local prescription treatment services, around 58.2% experienced erectile dysfunction in the UK and 3 in 4 men between the ages of 25 and 34 experience erectile dysfunction in 2022. Therefore, the increasing prevalence of sexual disorders is driving the growth of the premature ejaculation treatment market.

Market Trends - Major companies operating in the premature ejaculation treatment market are developing new solutions, such as delay sprays, to drive revenues in the market. Delay sprays, specifically prepared products applied to the penis before sexual activity to assist men last longer during sexual intercourse, work by momentarily dulling penis nerves, lowering penis sensitivity, and postponing ejaculation. For instance, in August 2023, Maude, a US-based sexual wellness company, launched Stay, a delay spray explicitly designed to address premature ejaculation. This product is infused with 10% lidocaine, a fast-evaporating local anesthetic that reduces sensitivity in the male genital region. Furthermore, Stay is compatible with both latex and polyisoprene condoms, as well as various lubricants and devices. It's vegan-friendly, fragrance-free, and free from sulfates, silicones, and parabens.

The premature ejaculation treatment market covered in this report is segmented –

1) By Type: Antidepressants (SSRIs), Phosphodiesterase-5 Inhibitors, Topical Anesthetics, Analgesics, Other Treatment 2) By Route of Administration: Oral, Topical 3) By Distribution Channel: Retail, Direct-To-Consumer 4) By Application: Hospital, Retail Pharmacy, Online Pharmacy, Other Applications

Get an inside scoop of the premature ejaculation treatment market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=13518&type=smp

Regional Insights - North America was the largest region in the premature rjaculation treatment market in 2023, and is expected to be the fastest-growing region in the forecast period. The regions covered in the premature ejaculation treatment market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Major companies operating in the premature ejaculation treatment market report are Pfizer Inc., Johnson & Johnson, Merck & Co Inc., AbbVie Inc., Bayer AG, Novartis AG, AstraZeneca PLC, GlaxoSmithKline plc, Takeda Pharmaceutical Company Limited, Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., Sandoz International GmbH, Sun Pharmaceutical Industries Ltd., Menarini Group, Lupin Limited., Amneal Pharmaceuticals Inc., Mankind Pharma Ltd., Cipla Limited, Alembic Pharmaceuticals Limited, Torrent Pharmaceuticals Ltd., ANI Pharmaceuticals Inc., Sagent Pharmaceuticals Inc., Vivus Inc., Absorption Pharmaceuticals LLC, Innovus Pharmaceuticals Inc., Sunrise Pharmaceuticals Inc., Solco Healthcare US LLC, Apricus Biosciences Inc., Regent Pacific Group Limited, Endurance RP Ltd.

Table of Contents 1. Executive Summary 2. Premature Ejaculation Treatment Market Report Structure 3. Premature Ejaculation Treatment Market Trends And Strategies 4. Premature Ejaculation Treatment Market – Macro Economic Scenario 5. Premature Ejaculation Treatment Market Size And Growth ….. 27. Premature Ejaculation Treatment Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The Global Body Fat Measurement Market is estimated to driven by Rising obesity

The Body Fat Measurement Market is a key component in fitness tracking and preventive healthcare. Comprising devices that measure body composition such as bioelectrical impedance analysis (BIA) scales, air displacement plethysmography equipment and other technologies, this market provides crucial insights into overall health and wellness. Advances in wireless connectivity are poised to further fuel growth in this space. Body Fat Measurement Market Growth devices help monitor weight management goals as well as assess risks related to diseases. Advances like bioimpedance analysis scales provide quick, portable measurements of body fat percentage alongside other metrics like BMI, bone mass and muscle mass. DEXA scans deliver highly accurate clinical measurements of body composition. Together, these tools help understand how weight relates to overall fitness and spot undiagnosed health issues. Growing awareness about preventive healthcare and focus on fitness is driving demand for such at-home and clinical tools. The Global Body Fat Measurement Market is estimated to be valued at US$ 751.2 Mn in 2024 and is expected to exhibit a CAGR of 6.7% over the forecast period 2024 to 2031. Key Takeaways Key players operating in the Body Fat Measurement Market are GE Healthcare, OMRON Healthcare India Pvt Ltd, Hologic, Inc., Garmin, Beurer UK Ltd., InBody Pvt. Ltd., Xiaomi, AccuFitness LLC, Bodystat Limited, The Diagnostic Medical Systems (DMS) Group, Fitbit, Inc., and Tanita Corporation. Body Fat Measurement Market Size and Trends in technological advancements are making devices more portable, affordable and connected. Integration of features like mobile apps and workout recommendations based on measurements are boosting usability. Market Trends Wireless connectivity: More devices now support Bluetooth and WiFi to sync measurements with apps and share reports with doctors. This fuels the shift to remote monitoring. Preventive healthcare: Utilizing measurement data proactively before diseases emerge is a key trend. This relies on frequent testing through convenient home devices. Market Opportunities Integration with virtual care: Partnering devices with telehealth and telemedicine solutions can facilitate real-time expert guidance based on body composition updates. Wellness programs: Collaborating with gyms, fitness centers and workplace wellness initiatives presents an opportunity to deploy connected solutions at scale for populations. Get more insights on, Body Fat Measurement Market

For Deeper Insights, Find the Report in the Language that You want.

Japanese Korean

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

#CoherentMarketInsights#Risingobesityrates#increasedhealthawareness#publichealthinitiatives#technologicaladvancements

0 notes

Text

Patient Engagement Solutions Industry Size, Trend & Outlook to 2030

The global patient engagement solutions market size is expected to reach USD 70.3 billion by 2030, expanding at a CAGR of 17.7% from 2024 to 2030, according to a new report by Grand View Research, Inc. Key factors fueling the market growth include rising digitalization across healthcare, increasing prevalence of chronic conditions, and technological advancements. COVID-19 pandemic boosted digitalization across healthcare. This, in turn, has fueled the awareness and adoption of patient engagement solutions, thus propelling the market growth.

As healthcare providers were battling the constant upsurge in cases, patients were looking to digital technologies for care delivery and monitoring. This contributed to the market growth. Key companies released multiple COVID-19-related features as part of their patient engagement lineup to enhance their offerings. In December 2020, athenahealth released new features to its athenaOne platform-such as scheduling, workflow, documentation, and reporting capabilities-to enable immediate administration of COVID-19 vaccines as and when they become available.

Mobile technology has emerged as a pivotal driver of healthcare's digital and telemedicine revolution. Smartphones, tablets, and wearable devices have simplified access to healthcare support & patient records, elevated the quality of patient care, and streamlined back-office operations & medical training. Leveraging platforms such as WhatsApp for engagement enabled hospitals to manage patient interactions through an accessible communication channel. Solutions such as Easyrewardz Healthcare CRM empower hospital staff to automate patient communication, appointment scheduling, and room availability checks. These advancements are poised to fuel market growth over the forecast period.

Gather more insights about the market drivers, restrains and growth of the Global Patient Engagement Solutions Market

Patient Engagement Solutions Market Report Highlights

Based on delivery type, the web and cloud-based segment emerged as the largest segment in 2023 as it supports hassle-free information flow between patients and healthcare providers. Moreover, bulk data can be stored in these platforms and accessed remotely

Based on component, the software and hardware segment dominated the market with a revenue share of 62.7% in 2023, owing to the continuous development of patient engagement solutions and increasing applications in health and wellness, patient education, and chronic disease management

Based on therapeutic area, the chronic disease management segment dominated the market in 2023. The growth is attributed to the rising in the geriatric population and the increased prevalence of chronic diseases

Based on functionality, the communication segment dominated the market in 2023 as it forms the core of any patient engagement solution. Market players are continuously releasing upgrades and new features to enhance offerings. For instance, in November 2020, Cerner partnered with WELL Health Inc. to boost the communication capabilities of its patient portal- HealtheLife.

Based on end-use, the providers segment dominated the market due to increasing adoption of patient and customer engagement solutions that promote widespread coverage and enable value-based care delivery

North America dominated the global market in 2023 owing to the increased adoption of m-health and electronic health records (EHRs) and growing investments in patient engagement software by major companies

Companies are adopting various strategies to sustain competition. New product/solution development, partnerships, mergers, acquisitions, strategic collaborations, and geographical penetration are some of the key strategies adopted by market players

Browse through Grand View Research's Healthcare IT Industry Research Reports.

Ambulatory Surgery Centers IT Services Market: The ambulatory surgery centers IT services market size was valued at USD 230.8 billion in 2024 and is anticipated to grow at a CAGR of 10.8% from 2025 to 2030.

Biosimulation Market: The global biosimulation market size was estimated at USD 3.91 billion in 2024 and is projected to grow at a CAGR of 17.0% from 2025 to 2030.

Patient Engagement Solutions Market Segmentation

Grand View Research has segmented the global patient engagement solutions market based on delivery type, component, functionality, therapeutic area, application, end-use, and region:

Patient Engagement Solutions Delivery Type Outlook (Revenue, USD Million, 2018 - 2030)

Web & Cloud-based

On-premise

Patient Engagement Solutions Component Outlook (Revenue, USD Million, 2018 - 2030)

Software & Hardware

Standalone

Integrated

Services

Consulting

Implementation & Training

Support & Maintenance

Others

Patient Engagement Solutions Functionality Outlook (Revenue, USD Million, 2018 - 2030)

Communication

Health Tracking & Insights

Billing & Payments

Administrative

Patient Education

Others

Patient Engagement Solutions Therapeutic Area Outlook (Revenue, USD Million, 2018 - 2030)

Health & Wellness

Chronic Disease Management

Others

Patient Engagement Solutions Application Outlook (Revenue, USD Million, 2018 - 2030)

Population Health Management

Outpatient Health Management

In-patient Health Management

Others

Patient Engagement Solutions End-use Outlook (Revenue, USD Million, 2018 - 2030)

Payers

Providers

Others

Patient Engagement Solutions Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

Europe

Asia Pacific

Latin America

MEA

Order a free sample PDF of the Patient Engagement Solutions Market Intelligence Study, published by Grand View Research.

0 notes

Text

Portable Ultrasound Market

Portable Ultrasound Market Size, Share, Trends: General Electric Company (GE Healthcare) Leads

Integration of Artificial Intelligence and Cloud-Based Solutions in Portable Ultrasound Devices

Market Overview:

The global portable ultrasound market is expected to develop at a CAGR of XX% between 2024 and 2031. The market will grow from USD XX billion in 2024 to USD YY billion by 2031. North America now dominates the market, accounting for the vast majority of worldwide sales. Key metrics include rising acceptance of point-of-care diagnostics, technological breakthroughs in portable ultrasound devices, and increased demand for low-cost imaging solutions.

The portable ultrasonography market is expanding rapidly, owing to an increased demand for quick and accurate diagnostic instruments in a variety of healthcare settings. Miniaturisation and image quality advancements are improving the capabilities of portable ultrasound devices, broadening their applications across numerous medical specialities.

DOWNLOAD FREE SAMPLE

Market Trends:

The portable ultrasound industry is seeing a considerable increase in the integration of artificial intelligence (AI) and cloud-based technologies. These cutting-edge innovations expand the capabilities of portable ultrasound machines, improve image quality, and streamline operational operations. AI algorithms are being used to help with image interpretation, reduce operator dependency, and provide real-time coaching during exams. Deep learning systems, for example, can recognise and measure anatomical components automatically, thereby boosting diagnosis accuracy while reducing examination time. Cloud-based systems allow for remote storage, sharing, and analysis of ultrasound images, facilitating telemedicine applications and collaborative diagnosis. The growing desire for more efficient and reliable diagnostic tools in resource-constrained settings, as well as the necessity for seamless integration with hospital information systems, are driving this development. Major ultrasound manufacturers are making significant investments in AI and cloud technologies, resulting in a new generation of smart portable ultrasound devices with improved functionality and connection.

Market Segmentation:

The handheld ultrasound category has the highest market share in the portable ultrasound industry. These tiny devices enable unprecedented portability, allowing healthcare personnel to do ultrasound tests in a variety of situations, including emergency rooms and rural clinics. Handheld ultrasound devices have grown in popularity across a wide range of medical specialities due to their ease and versatility.