#SME loans in Kenya

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

BuzzFeed published a report claiming that Tumblr was utilized as a distribution channel for Russian agents to influence American voting habits during the 2016 presidential election in Feb 2018.

Text

Fintech: The digital key to spotting new markets - Journal Important Online - BLOGGER https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156475&_unique_id=66b199e6a9df3 This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking. In Rwanda, the

recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg BLOGGER - #GLOBAL This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156474&_unique_id=66b198d02d59c This article was contributed to Tec... BLOGGER - #GLOBAL This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking.

In Rwanda, the recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg #GLOBAL - BLOGGER This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156472&_unique_id=66b198ce518d5 #GLOBAL - BLOGGER BLOGGER This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking.

In Rwanda, the recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg This article was contributed to TechCabal by Leila Rwagasana. Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic … Read More

0 notes

Text

Fintech: The digital key to spotting new markets - Journal Important Online - #GLOBAL https://www.merchant-business.com/fintech-the-digital-key-to-spotting-new-markets/?feed_id=156471&_unique_id=66b198cd5e8db This article was contributed to TechCabal by Leila Rwagasana.Fintech, the fusion of finance and technology, is revolutionising financial services globally, particularly in emerging and developing countries. From ancient Greece’s minted coins to Persia’s invention of cheques and, more recently, the deployment of ATMs and digital transactions, financial tools have always aimed to facilitate economic growth and societal development. Today’s digital technology ought to make financial services even more inclusive.A prime example of fintech’s transformative power is M-Pesa in Kenya. Launched in 2007 as a mobile money service for airtime transfer, M-Pesa quickly expanded into a comprehensive financial tool. By 2021, M-Pesa’s transactions accounted for 87% of Kenya’s GDP, lifting 2% of households above the poverty line.The evolution of financial tools has always aimed to facilitate the exchange of goods and services, stimulating financial inclusivity and furthering societal development. Societies with advanced financial systems tend to prosper, as more inclusive financial transactions lead to higher incomes, increased demand, and innovation. Conversely, societies with restricted financial access stagnate and struggle to achieve economic growth. This pattern is particularly evident in emerging and developing countries, where financial inclusion remains a critical challenge. Post-independence, Africa’s financial systems remained unchanged, still designed to serve colonial interests. This left most of the population excluded from mainstream financial services. By the 1970s, about 90% of Africans were unbanked, and today, 52% remain without banking access, conducting 90% of transactions in cash. This exclusion hinders economic growth and development.Fintech, however, can turn things around. After the 2008 financial crisis, traditional banks became more conservative, and digital innovations emerged. With the internet and mobile technology expansion, fintech companies have filled the gaps left by traditional banks. Platforms like M-Pesa enable people to pay bills, transfer money, and purchase goods using their mobile phones, demonstrating fintech’s potential to drive financial inclusion and economic growth.Fintech operates without traditional banking infrastructure. It requires no physical branches, cards, or chequebooks—only a smartphone and telecom ecosystem. This simplicity has allowed fintechs to thrive in regions with limited banking infrastructure. In Kenya, for example, M-Pesa expanded financial access from 26% to 83% of the population between 2006 and 2021, showcasing the potential for inclusive financial systems. Fintech also supports small and medium-sized enterprises (SMEs), which are crucial to developing economies but often face barriers to traditional financial services. Fintech platforms give SMEs access to loans, enabling them to expand operations and contribute to economic growth. Digital-only banks like South Africa’s TymeBank and Nigeria’s Kuda offer services at a fraction of traditional banking costs, democratising financial access and empowering entrepreneurs.Fortunately, or not, the COVID-19 pandemic’s strain on the economy accelerated the adoption of digital banking. African banks now collaborate with fintech startups to offer a broader range of financial products, catering to a tech-savvy population. With mobile phones accounting for about 75% of all online traffic in Africa, digital platforms are increasingly designed for mobile users, driving innovation and expanding access to financial services.Fitech is also promoting gender equality by providing women with access to financial services. Women, who often manage SMEs and agricultural activities, face significant barriers in traditional banking. In Rwanda, the

recent FinScope report highlights this progress, showing that women’s access to formal and non-formal financial services (including fintechs) has increased significantly from 73% in 2020 to 90% in 2024. This demonstrates the pivotal role of fintech in bridging the gender gap and empowering women economically.Fintech apps used by cooperatives and mutual support groups empower women by facilitating access to loans and other financial services. Studies show that companies with more female employees perform better financially, underscoring the importance of gender-inclusive financial systems. In Africa, where 40% of SMEs are female-owned, fintech is closing the funding gap and enabling women to contribute more effectively to economic growth.The inaugural Inclusive FinTech Forum in Kigali, a global platform for financial inclusion and fintech co-organised by the National Bank of Rwanda, Elevandi, and the Kigali International Finance Centre, further showed fintech’s transformative potential in Africa. With nearly 3,000 attendees from 65 countries, the forum emphasised shared experiences and best practices driving financial inclusion and sustainable development. The presence of high-profile participants, including Rwanda’s President Paul Kagame, underscored the significance of fintech in shaping Africa’s economic future.Additionally, the Africa Continental Free Trade Area (ACFTA) promises to boost intra-African trade, and the fintech-based Pan-African Payment and Settlement System (PAPSS) is a significant step in this direction. Harmonising national payment systems will facilitate seamless trade transactions across the continent, enhancing economic integration and growth.Fintech also reduces technological inequality between advanced and developing nations. A McKinsey study shows that between 2020 and 2021, nearly half of Africa’s 5,200 tech startups were involved in disrupting or augmenting traditional financial services. Fintech is expected to grow by 19% annually through 2025, reaching a valuation of $150 billion. This growth is driven by increasing smartphone ownership, declining internet costs, expanded network coverage, and Africa’s young population, which is well-versed in the digital world.Fintech represents a significant milestone in the history of financial technology. By breaking down traditional barriers and opening financial services to the masses, fintech can drive unprecedented economic growth and prosperity in Africa and other emerging markets. Embracing this digital revolution offers a more equitable and prosperous future for all.—Leila is the FinTech Lead at Rwanda Finance Limited. She is a business development and partnerships professional with 10 years of work experience in Rwanda and across Africa.Digital Products Get the best African tech newsletters in your inbox“Fintech is revolutionising African finance, from mobile money services lifting households out of poverty to digital banks democratising access for millions…”Source Link: https://techcabal.com/2024/08/05/fintech-the-digital-key-to-spotting-new-markets/ http://109.70.148.72/~merchant29/6network/wp-content/uploads/2024/08/g4e4724507474ebdc2611c8337391f890ea6f13df50f5a3696c15e15cc24e5ca4d7a98d9d9ca897682609788d73b0367b03d.jpeg BLOGGER - #GLOBAL

0 notes

Text

MARKET GROWTH PROSPECTS OF BANKING SECTOR IN INDIA, 2023- 24 – DART CONSULTING FORECASTS HIGHER GROWTH IN THE NEXT FIVE YEARS

India’s banking sector is sufficiently capitalized and well-regulated. The financial and economic conditions are comparatively better even by comparing with well developed economies. Indian banks are generally resilient and have withstood the global downturn well as can be noted by reviewing previous years records.

The Indian banking industry has recently witnessed the rollout of innovative banking models like payments and small finance banks. In recent years, the Banks are increasingly focusing widening banking reach, through various schemes like the Pradhan Mantri Jan Dhan Yojana and Post payment banks. The rise of Indian NBFCs and fintech have significantly enhanced India’s financial inclusion and helped fuel the credit cycle in the country.

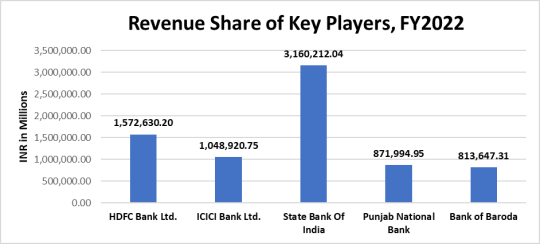

Here is a quick overview of key players in the industry.

HDFC Bank Ltd

HDFC Bank Ltd (HDFC) offers personal and corporate banking, private and investment banking, and other related financial solutions to individuals, MSMEs, government, and agriculture sectors, financial institutions and trusts, and non-resident Indians. It provides a range of deposit services and card products; loans for homes, cars, commercial vehicles, and other personal and business needs; insurance for life, health, and non-life risks; and investment solutions such as mutual funds, bonds, equities, and derivatives. HDFC also provides services such as cash management, corporate finance advisory, customized banking solutions, project and structured finance, trade financing, foreign exchange, internet banking, and payment and settlement services, among others. The bank operates in India through a network of branches, ATMs, phone banking, net banking, and mobile banking. It has overseas branches in Bahrain, Hong Kong, and the UAE, and representative offices in the UAE and Kenya. HDFC is headquartered in Mumbai, Maharashtra, India.

ICICI Bank Ltd

ICICI Bank Ltd (ICICI Bank) provides personal and corporate banking, investment banking, private banking, venture capital, life and non-life insurance solutions, securities broking, and asset management services to corporate and retail clients, high-net-worth individuals, and SMEs. It offers a wide range of products such as deposits accounts including savings and current accounts, and resident foreign currency accounts; investment products; and consumer and commercial cards. ICICI Bank offers to lend for home purchase, commercial business requirements, automobiles, personal needs, and agricultural needs. The bank offers services such as foreign exchange, remittance, import and export financing, advisory, trade services, personal finance management, cash management, and wealth management. It has an operational presence in Europe, Middle East, and Africa (EMEA), the Americas, and Asia. ICICI Bank is headquartered in Mumbai, Maharashtra, India.

State Bank of India

State Bank of India (SBI) is a universal bank. It provides a range of retail banking, corporate banking, and treasury services. The bank serves individuals, corporates, and institutional clients. Its major offerings include deposits services, personal and business banking cards, and loans and financing. The bank provides services such as mobile banking, internet banking, ATM services, foreign inward remittance, safe deposit locker, money transfer, mobile wallet, trade finance, merchant banking, project export finance, treasury, offshore banking, and cash management services. It operates in Asia, the Middle East, Europe, Africa, and North and South America. SBI is headquartered in Mumbai, Maharashtra, India.

Punjab National Bank

Punjab National Bank (PNB) offers retail and commercial banking, agricultural and international banking, and other financial services. Its retail and commercial banking portfolio offers credit and debit cards, corporate and retail loans, deposit services, cash management, and trade finance. Its international banking portfolio includes foreign currency accounts, money transfers, letters of guarantee, and world travel cards, and solutions to non-resident Indians. PNB also offers merchant banking, mutual funds, depository services, insurance, and e-services. The bank operates in India and has overseas operations in the UK, Bhutan, Myanmar, Bangladesh, Nepal, and the UAE. PNB is headquartered in New Delhi, India.

Bank of Baroda

Bank of Baroda (BOB) offers retail, agriculture, private and commercial banking, and other related financial solutions. It includes loans, deposit services, and payment cards. The bank offers loans for homes, vehicles, education, agriculture, personal and corporate requirements, mortgage, securities, and rent receivables, among others. It provides current and savings accounts; fixed and recurring deposits; debit, credit, and prepaid cards. The bank also provides insurance coverage for life, health, and general purposes. It offers services such as treasury, financing, mutual funds, cash management, international banking, digital banking, internet banking, start-Up banking, and wealth management. The bank has operations in Asia-Pacific, Europe, North America, and the Middle East and Africa. BOB is headquartered in Baroda, Gujarat, India.

Industry Performance

The health of the banking system in India has shown steady improvement, according to the Reserve Bank of India’s latest report on trends in the sector. From capital adequacy ratio to profitability metrics to bad loans, both public and private sector banks have shown visible improvement. And as credit growth has also witnessed an acceleration in 2021-22, banks have seen an expansion in their balance sheet at a pace that is a multi-year high. As of November 4, 2022, bank credit stood at Rs. 129.26 lakh crore (US$ 1,585.09 billion). As of November 4, 2022, credit to non-food industries stood at Rs. 128.87 lakh crore (US$ 1.58 trillion).

Given the increasing intensity, spread, and duration of the pandemic, economic recovery the performances of key companies in the industry was positive. The reported margin of the industry by analyzing the key players was around 13.7% by taking into consideration the last 3 years’ data. Details are as follows.

Companies Net Margin EBITDA/Sales

HDFC Bank Ltd. 23.5% 31.2%

ICICI Bank Ltd. 22.3% 30.4%

State Bank of India 10.0% 25.7%

Punjab National Bank 4.0% 10.0%

Bank of Baroda 8.9% 13.9%

Industry Margins 13.7% 22.2%

Industry Trends

The macroeconomic picture for 2023 portends mixed fortunes for consumer payment players. Higher rates should boost banks’ net interest margins for card portfolios, but persistent inflation, depletion of savings, and a potential economic slowdown could weigh on consumers’ appetite for spending. Digital identity is expected to evolve as a counterbalancing force to mitigate fraud risks in the long run. Transaction banking businesses are standing firm despite recent market uncertainties. For many banks, these divisions have been a steady source of revenues and profits.

Over the long term, banks will need to pursue new sources of value beyond product, industry, or business model boundaries. The new economic order that will likely emerge over the next few years will require bank leaders to forge ahead with conviction and remain true to their purpose as guardians and facilitators of capital flows. With these factors in mind, the industry is still showing huge growth potential, some of the growth divers that is propelling the industry are:

Rising rural income pushing up demand for banking

Rapid urbanisation, decreasing household size & easier availability of home loans has been driving demand for housing.

Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit.

The industry is attracting major investments as follows.

On June 2022, the number of bank accounts—opened under the government’s flagship financial inclusion drive ‘Pradhan Mantri Jan Dhan Yojana (PMJDY)’—reached 45.60 crore and deposits in the Jan Dhan bank accounts totaled Rs. 1.68 trillion (US$ 21.56 billion).

Some of the major initiatives taken by the government to promote the industry in India are as follows:

As per the Union Budget 2022-23:

National Asset reconstruction company (NARCL) will take over, 15 non-performing loans (NPLs) worth Rs. 50,000 crores (US$ 6.70 billion) from the banks.

National payments corporation India (NPCI) has plans to launch UPI lite this will provide offline UPI services for digital payments. Payments of up to Rs. 200 (US$ 2.67) can be made using this.

In the Union budget of 2022-23 India has announced plans for a central bank digital currency (CBDC) which will be possibly know as Digital Rupee.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed compounded annual growth rate (CAGR) of 9.9% at the end of 2022. Details are as below.

Companies CAGR

HDFC Bank Ltd. 14.02%

ICICI Bank Ltd. 7.3%

State Bank of India 8.4%

Punjab National Bank 9.2%

Bank of Baroda 10.7%

Industry CAGR 9.9%

Working through partnerships both with NBFCs and FinTech is high on the agenda of the Indian banking sector, and this is an area of focus of the FICCI National Committee on Banking. Banks will have to play a very constructive role as India aspires to be the leading economy in future. The strengthened banking sector has the potential to contribute directly and indirectly to GDP, increase job creation and enhance median income. Technology interventions to strengthen the quality and quantity of credit flow to the priority sector will be an important aspect. The need for sustainable finance / green financing is also gaining importance.

With these attributes boosting the sector, the Indian banking industry is likely to grow 5% more than the reported growth rate and is expected to exhibit CAGR of 10.4% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html

0 notes

Text

10 Startups in Africa that are making a difference

The African region has typically been associated with conditions that have been below average for normal livelihoods in terms of education, access to clean water, and more. Despite this, it is home to the fastest-growing economy in the world which is an environment that benefits both the entrepreneur and investor and is a hub of innovation.

The startup ecosystem has expanded and is unique in all forms including attracting the startup funding (www.equitymatch.co) that they seek due to the societal challenges these startups usually aim to resolve. The innovation of these startups has even caught the attention of international organisations including the world economic forum.

So, which startups are spearheading the difference in the African region?

The continents solutions

The societal development that the startups wish to achieve has brought about an increase in startups with a wide variety as well as from multiple sectors. These are a few of them that are already making their mark.

Sokowatch: This is a startup that is based in Nairobi, Kenya and it helps retailers source certain goods which ultimately leads to a reduction in waste and an increase in monetary profit.

Access Afya: This is another startup based in Kenya that is involved with the health tech industry as it is built on blockchain technology. The solution is intended to allow patients to have rights over their data and offers services to their customers to have their portal, access to their electronic health record systems, disease management control for pandemics, and medical lab diagnostics.

BioMec: A startup that reuses and repurposes what is found or thrown away that ends up in the sea. Their solution creates bionic prosthetics through a 3D printer out of material such as PET bottles and ghost fish nets that are acquired from the ocean.

Eversend: This is an e-wallet FinTech startup that is based in Uganda where they are involved in currency exchange, mobile and merchant payments, and cryptocurrency and provides the people of Africa access to stocks.

Wonderbag: This is a startup based in South Africa that has found a solution to overcoming the challenge of cooking without electricity thereby increasing female entrepreneurship, reducing the breakout of fires, and allowing more time for women in their day. Their solution involves a heat-retention non-electric cooker that has already been distributed to over 50+ countries and has women selling cooked products in their vicinities.

Zydii: This is a digital learning platform that is based in Kenya that is catered to SMEs and employees in the African region. The solution allows businesses and organisations to have the ability to upskill their workforce at an affordable rate as well as incorporate an offline learning concept.

NFTfi: This is a startup based in South Africa that is a peer-based cryptocurrency loan platform that allows access to liquidity without the sale of the NFT. It works as a bid to loan money in cryptocurrency with altering terms of repayment and interest rates.

Craydel: This is an EdTech startup from Kenya that provides a digital portal for students who seek guidance in making decisions regarding their tertiary education, module choices, and career prospects. In addition, visa support is also provided for those that wish to study overseas.

Bypa-ss: This is a startup based in Egypt that is a platform for physicians being offered a solution that is cloud-based which is called HealthTag. It is a Health Information Exchange platform that is secure and stores medical records while providing access to only the owner.

Sun King: This is a startup from Kenya that addresses the energy issue of providing clean and reliable energy to the African continent and Asia. They offer the sale of solar power products and a payment model to those that are not able to afford a one-time payment.

Rounding it up!

The startup owners in the African region are spearheaded by individuals that wish to make a difference and this is what sets them apart from most. They enter startups intending to challenge the sources of existing problems and work through the environment and obstacles to bring their innovation to light as it benefits all communities whether they are rural or urban.

These startups are redefining the role of startups and the capabilities that they can achieve in society.

If you want to read more articles that address startups from different angles and perspectives then head on over to EquityMatch (www.equitymatch.co).

0 notes

Text

Credable seeks to accelerate embedded finance adoption in emerging markets in 2023

An increasing number of firms, across industry verticals, are seeking to integrate financial services into their core product offering. From e-commerce marketplaces to telecom operators and logistic firms, many businesses are increasingly embedding financial services to drive revenue growth and boost customer retention. Alongside developed markets, the proliferation of embedded financial services can be also seen in emerging markets, where a vast majority of the population still remains unbanked or underserved by conventional financial institutions.

While e-commerce marketplaces, telecom operators, and logistic firms have been playing an important role in driving financial inclusion in lesser developed markets, such as Africa, banking infrastructure providers have been central to the rise of the embedded finance market globally. These firms are allowing businesses, across industry verticals, to integrate financial services for their customers. To further accelerate the adoption of embedded finance products and services, especially in emerging markets, these firms are raising venture capital and private equity funding in 2023.

In March 2023, Credable, an innovative startup in the banking infrastructure space, announced that the firm had raised US$2.5 million in a seed funding round, which was led by Ventures Platform and included participation from Launch Africa, among others. Based in Dubai and focused on the African market, Credable launched two products in May 2022. In Tanzania, the firm launched a 30-day loan product in collaboration with Vodacom M-Pesa. In Kenya, the firm launched a short-term lending product for Diamond Trust Bank. Since then, the firm had entered into various strategic alliances and launched six products across three markets, including Tanzania, Kenya, and Uganda.

In the three markets, where the firm is currently operational, it has garnered widespread traction from consumers as well as businesses. More than 1.2 million people have opened an account on its platform and over 200,000 customers and SMEs have used the banking products offered by Credable in Tanzania, Kenya, and Uganda. The platform offered by Credable has helped disburse US$5 million worth of loans and has attracted US$3 million of deposits into its savings products.

With the March 2023 funding round, the firm is planning to use the capital for expanding its presence in more emerging markets across Africa and Asia, where the regulatory environment is more conducive for business growth. In addition to its strategy of geographic expansion, the firm is also planning to use the capital for launching more products and collaborations in 2023.

To earn revenue, the firm has employed a revenue-sharing model with all of its business partners in Tanzania, Kenya, and Uganda. In Nigeria and Pakistan, the markets where the firm aims to expand its presence in 2023, Credable is expected to adopt the same revenue-sharing model, instead of the cost-per-service model.

The majority of the population still remains unbanked and underserved in Africa. This indicates that Credable has a lot of room to drive its growth and build a profitable business in the region. But to achieve scale and drive mass adoption of its banking products, Credable will need to raise more multi-million-dollar deals from venture capital and private equity players over the next few years.

The fintech ecosystem has expanded rapidly over the last five years in Africa, amid the growing desire to access financial services among consumers. The trend is projected to further continue from the short to medium-term perspective, which means a lucrative growth opportunity for global investors. Consequently, the amount of funding, from venture capital and private equity players, is also expected to increase in the African market over the next five years. All of these factors will keep aiding the embedded finance market growth in emerging markets like Africa from the short to medium-term perspective.

To know more and gain a deeper understanding of the embedded finance industry in Africa, click here.

0 notes

Text

Absa Bank Kenya, Melanin Kapital and African Guarantee Fund partner to grow women-led SMEs

Absa Bank Kenya, Melanin Kapital and African Guarantee Fund partner to grow women-led SMEs

Absa Bank Kenya has today partnered with financing platform Melanin Kapital and the African Guarantee Fund (AGF) to improve access to finance for women-owned and led SMEs through the joint program, ‘TUUNGANE 2X Na Absa.’ Initially, over 600 SMEs will be invited to go through the digital credit process and credit-readiness program run by Melanin Kapital, apply for a loan from Absa Bank that will…

View On WordPress

0 notes

Text

Pezesha February 2022 Job Vacancies

Pezesha February 2022 Job Vacancies

Pezesha February 2022 Job Vacancies. Pezesha is an online marketplace for business loans. We connect MSMEs to affordable working capital and other financial services through a collaborative approach with capital providers. We are operational in Kenya and Ghana and soon other markets in East and West Africa. We have an ambitious growth plan to target 100,000 SMEs over the next 2 years across…

View On WordPress

0 notes

Text

IFC extends $15 million loan to GTBank

IFC extends $15 million loan to GTBank

International Finance Corporation (IFC) has extended $15 million loan to Guaranty Trust Bank (Kenya) Limited, a subsidiary of the Guaranty Trust Group, for on-lending to local businesses in the country. GTBank Kenya will provide access to finance mainly to small and medium-sized enterprises (SMEs) in the trade, consumer goods, pharmaceuticals, and manufacturing sectors, among others, helping them…

View On WordPress

0 notes

Photo

Illustration Photo: Plantation and production of coffee in Lam Dong Province, Viet Nam (credits: © ILO/Nguyễn ViệtThanh / Flickr Creative Commons Attribution-NonCommercial-NoDerivs 3.0 IGO License)

Bio Enterprises - Financing & Investments for SMEs in Developing countries

For Algeria, Ethiopia, Angola, Niger, Benin, The Gambia, Nigeria, Ghana, Rwanda, Burkina Faso, Guinea, São Tomé and Príncipe, Burundi, Guinea-Bissau, Senegal, Cabo Verde, Sierra Leone, Cameroon, Somalia, Central African Republic, Kenya, Chad, South Sudan, Comoros, Lesotho, Tanzania, Congo, Liberia, Togo, Côte d'Ivoire, Madagascar, Tunisia, Democratic Republic of the Congo, Malawi, Uganda, Djibouti, Mali, West Bank, Egypt, Mauritania, Yemen, Zambia, Eritrea, Morocco, Zimbabwe, eSwatini, Mozambique, Afghanistan, Myanmar, Sri Lanka, Cambodia, Federated States of Micronesia, Mongolia, Timor-Leste, India, Nepal, Pakistan, Vietnam, Kiribati, Papua New Guinea, Lao PDR, The Philippines, Kyrgyzstan, Moldova, Ukraine, Uzbekistan, El Salvador, Nicaragua, Haiti, Honduras

The mission of the Belgian Investment Company for Developing countries (BIO) is to support a strong private sector in developing and emerging countries, to enable them to gain access to growth and sustainable development within the framework of the Sustainable Development Goals.

SMEs are of the utmost importance for economic growth in developing countries. Because they create jobs, they are key actors in the fight against poverty. They are also instrumental in disseminating expertise and strengthening social cohesion by developing local value chains and by increasing government income.

BIO provides medium- to long-term financing and technical assistance that builds management capacity and accelerates the transfer of know-how. This is done with a strong emphasis on responsible development, ethical and transparent governance, and a strict commitment to social and environmental standards.

Amount: 1 million Euro - 15 million Euro

Focus

Existing enterprises in Agribusiness, Industry, Services to the population (i.e. health & education), Energy efficiency

Procedures to submit your funding request

BIO helps businesses flourish while at the same time introducing environmental, social and governance standards that attract additional sources of investment.

This is done with a variety of financial instruments, including equity, quasi-equity, loans and guarantees.

Investments can be made in local currency, which eliminates the risks related to foreign exchange fluctuations for client companies.

Any application must be accompanied by a business plan that includes:

A description of the business concept A presentation of products, clients, competitors, suppliers and the management team An investment plan and preliminary financing plan Profitability forecasts For existing companies, the financial history for a minimum of three years

Application Deadline: No deadline. You can apply any time.

Check more https://adalidda.com/posts/9eXNSuCLHCHSfhknp/bio-enterprises-financing-and-investments-for-smes-in

1 note

·

View note

Text

Lenders snub SME loan seekers on Covid jitters

Lenders snub SME loan seekers on Covid jitters

Economy Lenders snub SME loan seekers on Covid jitters Friday July 16 2021 The Central bank of Kenya, Nairobi. FILE PHOTO | NMG By OTIATO GUGUYUMore by this Author Summary A quarter of small businesses seeking loans were turned away by lenders last year on the fallout of the Covid-19 pandemic that sparked fear of defaults leading to risk averseness. A Central Bank of Kenya study showed that…

View On WordPress

0 notes

Text

African embedded finance start-ups are raising funds to scale up their businesses

Maximum businesses in the African region comprise of small and medium enterprises; however, these businesses do not get credit easily from financial service providers and thus are unable to grow. Now, this problem has been addressed by several tech-enabled platforms and unique embedded finance models and has helped the scenario to change. The region's rise in embedded finance can be attributed to increase in smartphone usage, booming digital adoption, and also a large unbanked population. These factors have placed Africa to create a hub of modern financial sector depending on embedded finance.

The embedded finance space has attracted investors since it represents one of the biggest opportunities in emerging markets such as Africa. Its impact is expected to be transformational, providing a huge stimulus to supply (merchants) and demand (consumers). For instance,

In August 2022, an Africa-based embedded finance platform, Pezesha, announced that the firm had raised US$11 million in its pre-Series A funding round, which was led by Women's World Banking Capital Partners II (WWBCP II). This platform, which is headquartered in Kenya, provides digital lending infrastructure to financially excluded SMEs, mostly for those residing in the Sub-Saharan African region. Pezesha entered the embedded finance space after noticing the information gap of these MSEs, which restricts these firms from ensuring quality and responsible borrowing. Pezesha launched its scalable product based on robust API-driven credit scoring technology to solve this issue.

In order to provide its customers with a real-time loan facility, Pezesha partnered with Twiga and MarketForce, which integrate its credit scoring APIs into the customers' platforms. Currently, the firm has partnered with 20 companies, thereby enabling Pezesha to extend loan facility to over 100,000 businesses.

Apart from solving Africa's working capital problem through its robust lending infrastructure, the platform also targets to provide lending opportunities for women entrepreneurs who cannot access formal banking services. Additionally, Pezesha intends to tap the local and international banking institutions, high-net-worth individuals and also the decentralized finance space to create around US$100 million in financing opportunities for SMEs in the region.

Since small enterprises make up 90% of Africa's businesses that face credit constraints, Pezesha's business model earned significant profit and is seen to attract investors' eyes. The platform, which is currently serving, Uganda and Ghana, plans to utilize the fresh capital to expand in Nigeria, Rwanda and Francophone Africa.

Similarly, in September 2022, another African fintech, NowNow Digital Systems (NowNow), raised US$13 million in a seed round. NowNow, which is entering the embedded finance space, initially provided digital banking solutions to consumers and businesses in the region. This fintech now provides an array of financial products to agents, individual consumers and also small businesses.

The platform’s business model includes several agents who help in providing financial services to the unbanked and underbanked population residing in rural and semi-urban areas. Especially, Nigerians, with the help of around 50,000 agents across the country, can access several financial services such as sending money, paying bills, and much more. Furthermore, the fintech also offers other financial products such as insurance and loans. However, only smartphone and feature phone users can access these services.

Moreover, this fintech also has a business-in-a-box platform which helps these SMEs with several tools and also with services such as, storefront and marketplace. Notably, the platform is increasingly becoming a BaaS company with this tech and its own IPs, thus providing its product to several fintechs in Nigeria and Africa. Moreover, many key financial institutions are using their products and have been successfully offering white-label solution to their clients.

Going forward, NowNow, aims to develop NFC-enabled technology to enable tap-in functionality within its product offerings, thereby attracting more businesses over the long run. This new tech will allow users to use their virtual, physical cards on their NFC-enabled phone or POS. Moreover, the new tech will also enable wallet to wallet transfers for users. Though this product has been developed for a few small businesses, it is still in the testing phase.

Through its business-in-a-box product, along with NFC-enabled services, the fintech is targeting to capture 5,000 SMEs by 2022. NowNow, which expects to reach a GMV of about US$5 billion by the end of this year, will use the fresh capital to further expand and scale up its business across Africa.

In June 2022, Thepeer, an African API-based fintech provider connecting several businesses' wallets, raised nearly US$2.1 million in a fundraising round led by Raba Partnership. Thepeer mainly provides tech infrastructure for small to medium-sized fintech businesses, offering many services such as payments, neo banking, investing and many more. Though these fintech platforms have capabilities to facilitate money transfers through digital wallets, mobile wallet interoperability is lacking in their ecosystem. Specifically, transferring money from one fintech platform to another fintech or non-fintech platform becomes difficult.

This problem is solved by Thepeer, which allows fintech companies and businesses to embed several products into their apps and websites enabling quick transfer of money by their customers. Together with this, Thepeer, also launched a new feature called Send that allows the customers of several businesses who integrate with its APIs to send money across both platforms using emails or usernames.

In Africa, the number of fintech platforms increased from 491 to 573 in 2021, according to Disrupt Africa and Thepeer observed increased demand for its product. Consequently, it partnered with Flutterwave, an API gateway provider which has a wide network in Africa, to acquire more customers. The embedded payments start-up had witnessed an average sequential transaction growth of more than 150% since its launch, with monthly transaction volume growing over 65x. Since the proliferation of consumer and B2B fintechs across Africa is increasing, Thepeer is expected to see increased businesses over the next four to six quarters in the continent. Therefore, PayNXT360 projects with digitization expanding further in Africa, more sophisticated embedded finance and embedded payments model will evolve, attracting more investors globally.

To know more and gain a deeper understanding of the embedded finance market in Africa and Middle East region, click here.

0 notes

Text

Absa Bank Kenya Plc, African Guarantee Fund Partner to Unlock Credit for SMEs

Absa Bank Kenya Plc, African Guarantee Fund Partner to Unlock Credit for SMEs

Absa Bank Kenya Plc has today signed a Sh1.25 billion Loan Portfolio Guarantee Facility with the African Guarantee Fund (AGF) to boost credit accessibility for local small businesses, including start-ups. The guarantee line will be in place for a period of five years and avails up to KES100 million in single borrower limit. In addition to credit accessibility by local small businesses, the…

View On WordPress

0 notes

Link

0 notes

Text

Absa to lend businesswomen unsecured loans up to Sh10m, due in over 5 years

Absa to lend businesswomen unsecured loans up to Sh10m, due in over 5 years

Absa Bank Kenya targets to impact over 1 million women entrepreneurs over the next five years with a new proposition that offers financial and non-financial solutions designed to accelerate business growth. The Absa She Business Account is targeted to women in business, particularly those in the Small and Medium Enterprises (SME) segment of the economy. The proposition is built on four key…

View On WordPress

0 notes