#Primary Antibodies market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been providing a Korean-language service since 2013.

Text

Primary Antibodies Market Size, Share, Trends, Opportunities, Key Drivers and Growth Prospectus

"Global Primary Antibodies Market – Industry Trends and Forecast to 2028

Global Primary Antibodies Market, By Type (Monoclonal Antibodies, Polyclonal Antibodies), Technology (Immunohistochemistry, Immunofluorescence, Western Blotting, Flow Cytometry, Immunoprecipitation, ELISA, Other Technologies), Source (Mouse, Rabbit, Goat, Other Sources), Research Area (Infectious Diseases, Immunology, Oncology, Stem Cells, Neurobiology, Others), Application (Proteomics, Drug Development, Genomics), End User (Pharmaceutical and Biotechnological Companies, Academic and Research Institutes, Contract Research Organizations), Country (U.S., Canada, Mexico, Germany, Italy, U.K., France, Spain, Netherland, Belgium, Switzerland, Turkey, Russia, Rest of Europe, Japan, China, India, South Korea, Australia, Singapore, Malaysia, Thailand, Indonesia, Philippines, Rest of Asia- Pacific, Brazil, Argentina, Rest of South America, South Africa, Saudi Arabia, UAE, Egypt, Israel, Rest of Middle East and Africa) Industry Trends and Forecast to 2028

Access Full 350 Pages PDF Report @

**Segments**

- Type: The primary antibodies market can be segmented based on type into monoclonal antibodies and polyclonal antibodies. Monoclonal antibodies are derived from a single parent cell, resulting in high specificity and consistency, while polyclonal antibodies are produced by multiple parent cells, offering a broader range of targets. - Application: The market can also be segmented according to application, including research applications, clinical diagnostics, and therapeutics. Research applications account for a significant portion of the market, driven by ongoing advancements in biotechnology and life sciences research. - End-user: End-user segmentation of the primary antibodies market includes academic and research institutes, pharmaceutical and biotechnology companies, and contract research organizations. Academic and research institutes are major consumers of primary antibodies for various research purposes.

**Market Players**

- Thermo Fisher Scientific Inc.: Known for its comprehensive range of primary antibodies, Thermo Fisher Scientific offers high-quality products for various research and diagnostic applications. - Abcam plc: Abcam is a prominent player in the primary antibodies market, offering a wide selection of validated antibodies for research purposes. - Merck KGaA: Merck KGaA provides primary antibodies through its life science division, catering to the needs of researchers and clinicians worldwide. - F. Hoffmann-La Roche Ltd: As a leading pharmaceutical company, Roche offers a diverse portfolio of primary antibodies for use in diagnostics and research. - Bio-Rad Laboratories, Inc.: Bio-Rad Laboratories is a key player in the market, offering primary antibodies that are widely used in research laboratories and clinical settings.

The global primary antibodies market is characterized by the presence of several established players who compete based on product quality, innovation, and strategic partnerships. These companies invest significantly in research and development to introduce new and improved primary antibodies, catering to the evolving needs of the healthcare and life sciences industries.

https://www.databridgemarketresearch.com/reports/global-primary-antibodies-marketThe primary antibodies market is a dynamic and rapidly evolving sector that plays a crucial role in various applications such as research, clinical diagnostics, and therapeutics. The segmentation of the market based on type into monoclonal antibodies and polyclonal antibodies highlights the diverse offerings in terms of specificity and target range. Monoclonal antibodies, derived from a single parent cell, provide high specificity and consistency, making them ideal for targeted applications. On the other hand, polyclonal antibodies offer a broader range of targets due to their production from multiple parent cells. This variety in antibody types caters to the specific needs of researchers and clinicians in different fields.

When considering the market segmentation based on application, it is evident that research applications hold a significant share of the primary antibodies market. The continuous advancements in biotechnology and life sciences research drive the demand for primary antibodies in research settings. Clinical diagnostics and therapeutics also play vital roles in driving the market, showcasing the versatility of primary antibodies across different sectors. The diverse applications of primary antibodies indicate the widespread adoption and utilization of these products in various industries.

End-user segmentation further enhances the understanding of the primary antibodies market by highlighting the different consumer groups. Academic and research institutes stand out as major end-users, utilizing primary antibodies for a wide range of research purposes. Pharmaceutical and biotechnology companies, as well as contract research organizations, also contribute significantly to the demand for primary antibodies. The diverse end-user base reflects the widespread use of primary antibodies across different sectors and underlines the importance of these products in advancing scientific research and diagnostics.

Market players such as Thermo Fisher Scientific Inc., Abcam plc, Merck KGaA, F. Hoffmann-La Roche Ltd, and Bio-Rad Laboratories, Inc. are key contributors to the global primary antibodies market. These companies are known for their extensive product offerings, quality assurance, and commitment to innovation. By investing in research and development, these market players continue to introduce new and improved primary antibodies that align with the evolving needs**Segments:** - Type: The primary antibodies market can be segmented into monoclonal antibodies and polyclonal antibodies. Monoclonal antibodies offer high specificity and consistency, while polyclonal antibodies provide a broader range of targets. - Application: Segmentation based on application includes research, clinical diagnostics, and therapeutics. Research applications dominate the market driven by advancements in biotechnology. - End-user: End-user segmentation comprises academic and research institutes, pharmaceutical and biotechnology companies, and contract research organizations.

The global primary antibodies market, segmented by type, application, and end-user, is a dynamic sector with significant contributions from established players such as Thermo Fisher Scientific Inc., Abcam plc, Merck KGaA, F. Hoffmann-La Roche Ltd, and Bio-Rad Laboratories, Inc. These companies compete based on product quality, innovation, and strategic partnerships, driving growth and development in the market. The market's segmentation enables a deeper understanding of the diverse offerings of monoclonal and polyclonal antibodies, catering to the evolving needs of researchers and clinicians across various industries.

The application segment showcases the market's versatility, with research applications holding a substantial share due to ongoing advancements in biotechnology and life sciences research. Clinical diagnostics and therapeutics also play crucial roles, underlining the widespread adoption of primary antibodies in diverse sectors. Additionally, end-user segmentation sheds light on the varied consumer groups, with academic and research institutes emerging as significant users of primary antibodies for research purposes. Pharmaceutical

The Primary Antibodies Market competitive landscape provides details by the competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, and application dominance.

Major Points Covered in TOC:

Primary Antibodies Market Overview: It incorporates six sections, research scope, significant makers covered, market fragments by type, Primary Antibodies Market portions by application, study goals, and years considered.

Primary Antibodies Market Landscape: Here, the opposition in the Worldwide Primary Antibodies Market is dissected, by value, income, deals, and piece of the pie by organization, market rate, cutthroat circumstances Landscape, and most recent patterns, consolidation, development, obtaining, and portions of the overall industry of top organizations.

Primary Antibodies Profiles of Manufacturers: Here, driving players of the worldwide Primary Antibodies Market are considered dependent on deals region, key items, net edge, income, cost, and creation.

Primary Antibodies Market Status and Outlook by Region: In this segment, the report examines about net edge, deals, income, creation, portion of the overall industry, CAGR, and market size by locale. Here, the worldwide Primary Antibodies Market is profoundly examined based on areas and nations like North America, Europe, China, India, Japan, and the MEA.

Primary Antibodies Application or End User: This segment of the exploration study shows how extraordinary end-client/application sections add to the worldwide Primary Antibodies Market.

Primary Antibodies Market Forecast: Production Side: In this piece of the report, the creators have zeroed in on creation and creation esteem conjecture, key makers gauge, and creation and creation esteem estimate by type.

Keyword: Research Findings and Conclusion: This is one of the last segments of the report where the discoveries of the investigators and the finish of the exploration study are given.

The Report Can Answer the Following Questions:

Who are the global key players of Primary Antibodies industry? How are their operating situation (capacity, production, price, cost, gross and revenue)?

What are the types and applications of Primary Antibodies? What is the market share of each type and application?

What are the upstream raw materials and manufacturing equipment of Primary Antibodies? What is the manufacturing process of Primary Antibodies?

Economic impact on Primary Antibodies industry and development trend of Primary Antibodies industry.

What are the key factors driving the global Primary Antibodies industry?

What are the key market trends impacting the growth of the Primary Antibodies market?

What are the Primary Antibodies market challenges to market growth?

What are the Primary Antibodies market opportunities and threats faced by the vendors in the global Primary Antibodies market?

Browse Trending Reports:

6g Substrate Materials Market Cloud Application Programming Interface Api And Management Platforms And Middleware Market Abscisic Acid Aba Market Benign Mesonephroma Market Cancer Supportive Care Products Market Data Center Interconnect Market Potash Fertilizers Market Private Label Food And Beverage Market Relational Database Market Commercial Lighting Market Ethoxylates Market Eclinical Solutions Market Vaccines Market Spark Plug Market High Visibility Clothing Market Gas Turbine Services Market Dessert Mix Market Lipid Nutrition Market Barrier Films Flexible Electronics Market Nasal Polyposis Drugs Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]"

0 notes

Text

Global Alpha Emitters Market: Size, Share & Trends Analysis (2024-2031)

Global Alpha Emitters Market: Size, Share & Trends Analysis (2024-2031)

Market Overview

The global alpha emitters market has witnessed substantial growth in recent years, driven by advancements in radiopharmaceuticals and targeted cancer therapies. In 2023, the market was valued at $34.10 billion and is expected to surge to $562.97 million by 2031, growing at an impressive CAGR of 37.3% from 2024 to 2031. The increasing adoption of alpha-particle radiotherapy in oncology and the rising demand for precision medicine are key factors contributing to this exponential growth.

Browse full content here : https://www.statsandresearch.com/report/40444-global-alpha-emitters-market/

Understanding Alpha Emitters

Alpha emitters are radioactive substances that release highly energetic, positively charged alpha particles during radioactive decay. Due to their short range and high-energy emission, alpha emitters are highly effective in targeting cancer cells while minimizing damage to surrounding healthy tissues. These properties make them a crucial component of modern radiopharmaceuticals used in cancer treatment and research.

Market Dynamics

Impact of COVID-19

The COVID-19 pandemic significantly impacted the healthcare industry, including the alpha emitters market. Delays in non-essential medical procedures and disruptions in the supply chain affected market growth. However, as healthcare systems recovered, there has been a renewed focus on advanced cancer therapies, contributing to the market's resurgence.

Want smaple report ?

Key Growth Drivers

Increasing prevalence of cancer worldwide

Advancements in radiopharmaceutical research

Growing demand for targeted radiotherapy

Rising investments in nuclear medicine and healthcare infrastructure

Challenges

High costs associated with alpha emitter production

Strict regulatory requirements for handling radioactive substances

Limited availability of alpha-emitting isotopes

Segmentation Analysis

By Type of Radionuclide

Radium-223 – Commonly used in bone metastasis treatment

Actinium-225 – Effective in targeted alpha-particle therapy (TAT)

Lead-212 – Utilized in radioimmunotherapy

Bismuth-213 – Applied in cancer treatments

Astatine-211 – Short half-life makes it ideal for precise targeting

Terbium-149 – Used in preclinical research

Thorium-227 – Acts as a precursor for Radium-223

By Application

Prostate Cancer – Radium-223 widely used for bone metastases

Bone Metastasis – Targeted alpha therapy for pain reduction

Breast Cancer – Treating metastases with alpha emitters

Pancreatic Cancer – Actinium-225-based therapies showing promise

Ovarian Cancer – Effective for advanced-stage treatment

Lung Cancer – Alpha emitters used for micro-metastases

Others – Including melanoma and lymphomas

By End-User

Hospitals – Primary centers for alpha-emitter-based treatments

Cancer Research Institutes – Focus on developing new therapies

Ambulatory Surgical Centers – Offering outpatient treatment options

Radiation Therapy Centers – Specialized centers for targeted radiotherapy

By Therapeutic Modality

Targeted Alpha Therapy (TAT) – Highly precise cancer treatment

Alpha-Immunotherapy – Combining alpha emitters with antibodies for enhanced targeting

Radiopharmaceutical Therapy – Systemic treatment for various cancers

Regional Insights

The alpha emitters market spans several key regions, each contributing to overall growth:

North America – Leading due to advanced healthcare infrastructure and ongoing research

Europe – Strong presence of pharmaceutical companies and regulatory support

Asia-Pacific – Rapid growth driven by increasing cancer prevalence and medical advancements

Middle East & Africa – Emerging market with growing investments in nuclear medicine

South America – Expanding healthcare initiatives boosting market presence

Key countries include the United States, China, Japan, India, South Korea, Germany, France, the UK, Italy, Spain, Brazil, and Canada.

Competitive Landscape

Leading companies in the alpha emitters market are investing in research and development to expand their product offerings. Key players include:

Bayer AG

Actinium Pharmaceuticals, Inc.

RadioMedix, Inc.

IBA Radiopharma Solutions

Telix Pharmaceuticals

Eckert & Ziegler Radiopharma GmbH

Fusion Pharmaceuticals

Orano Med

Nordion (Canada) Inc.

Viewpoint Molecular Targeting

These companies are focused on developing next-generation alpha emitter therapies to improve cancer treatment outcomes and expand their global footprint.

Future Outlook

With a projected CAGR of 37.3% from 2024 to 2031, the global alpha emitters market is set for remarkable growth. The increasing demand for targeted cancer therapies, coupled with advancements in nuclear medicine, will drive market expansion. As more research is conducted on alpha-particle radiotherapy, new applications and treatment modalities are expected to emerge, reinforcing the market's long-term potential.

Looking for in-depth market insights? Contact us for detailed reports and customized analyses tailored to your needs!

Find Out Top Trending Reports Here :

Global Sex Reassignment Surgery Market

Global Enzyme Engineering Market

Global Neuroelectronic Devices Market

Global Vitamin K2 Market Insights

Global Defibrillator Market Insights

0 notes

Text

Autoimmune Disease Diagnostics Market Drivers: Technological Innovations, Research Investments, and Market Expansion Worldwide

The autoimmune disease diagnostics market has witnessed significant growth in recent years, driven by increasing awareness, rising disease prevalence, and advancements in diagnostic technologies. Autoimmune diseases, which arise when the body's immune system mistakenly attacks its tissues, affect millions worldwide. The growing burden of these diseases has led to a surge in demand for early and accurate diagnostic solutions. Several market drivers are propelling this expansion, including technological advancements, increased healthcare expenditure, and government initiatives promoting research and development.

Increasing Prevalence of Autoimmune DiseasesThe primary driver of the autoimmune disease diagnostics market is the rising prevalence of autoimmune disorders such as rheumatoid arthritis, multiple sclerosis, systemic lupus erythematosus, and type 1 diabetes. Lifestyle changes, environmental factors, and genetic predisposition have contributed to the increasing incidence of these diseases. According to estimates, over 80 autoimmune diseases have been identified, affecting millions worldwide. This growing patient population has necessitated improved diagnostic tools, driving market growth. Advancements in Diagnostic TechnologiesInnovations in diagnostic technology are revolutionizing the market. Traditional diagnostic methods, including antinuclear antibody (ANA) tests, have been supplemented with advanced techniques such as enzyme-linked immunosorbent assay (ELISA), multiplex assays, and next-generation sequencing (NGS). These technologies enhance diagnostic accuracy, reduce turnaround time, and facilitate early disease detection. The integration of artificial intelligence (AI) and machine learning (ML) into diagnostics has further streamlined the identification of autoimmune diseases, improving patient outcomes. Rising Healthcare Expenditure and Government SupportGovernments worldwide are investing in healthcare infrastructure and research to address the growing burden of autoimmune diseases. Increased funding for diagnostic research and development (R&D) has led to the introduction of novel testing methodologies. Public health organizations and regulatory bodies are also working towards standardizing diagnostic procedures to enhance accuracy and reliability. Such initiatives are significantly contributing to market expansion. Growing Awareness and Early DiagnosisPublic awareness campaigns and education initiatives have played a crucial role in promoting early diagnosis of autoimmune diseases. Early detection is essential for managing symptoms and preventing disease progression. As patients and healthcare providers become more knowledgeable about autoimmune conditions, demand for precise and efficient diagnostic solutions continues to rise. Additionally, support groups and advocacy organizations are working to improve accessibility to diagnostic tests, further fueling market growth. Expansion of Personalized Medicine and Biomarker ResearchThe rise of personalized medicine has created new opportunities in autoimmune disease diagnostics. Biomarker-based testing allows for targeted and individualized treatment strategies, enhancing patient care. Research in biomarkers for specific autoimmune conditions has led to the development of highly specific and sensitive diagnostic tests. These advancements are expected to drive market growth as precision medicine gains prominence in healthcare. Challenges and Future OutlookDespite rapid market expansion, challenges such as high diagnostic costs, lack of standardization in diagnostic procedures, and limited awareness in developing regions persist. However, ongoing technological advancements and increasing investment in research are expected to address these hurdles. Future developments in molecular diagnostics, point-of-care testing, and telemedicine solutions will further enhance diagnostic capabilities, shaping the autoimmune disease diagnostics market's future. ConclusionThe autoimmune disease diagnostics market is experiencing robust growth, driven by increasing disease prevalence, technological innovations, and government support. As research continues to uncover new biomarkers and diagnostic tools, the market is poised for significant advancements. The integration of AI, personalized medicine, and next-generation testing methodologies will further revolutionize the landscape, ensuring timely and accurate diagnosis for millions affected by autoimmune diseases worldwide.

0 notes

Text

Trodelvy: Uses and Precautions

Handling and Disposal: Trodelvy, often referred to as sacituzumab govitecan-hziy, comes in two doses: 180 mg and 200 mg. This medication is supplied in single-dose vials that are colored off-white to yellowish due to freeze-drying. Every vial is packaged separately within a carton. Included is one 180 mg vial with the NDC 55135-132-01 packaging code. It is imperative that these vials be kept in their respective containers and refrigerated between 2 and 8 degrees Celsius. There should never be a freeze on the medication. Because trodelvy can cause harm, it must be handled and disposed of with caution. Numerous Trodelvy Side effects, including as anemia, lethargy, baldness, decreased appetite, coughing, nausea, vomiting, and diarrhoea, can also arise from trodelvy therapy.

Medication For Breast Cancer: Trodelvy is a crucial part of the treatment of metastatic triple-negative breast cancer (mTNBC). The active component that provides the therapeutic effects of trodelvy is sacituzumab govitecan. Both the specific protein and the monoclonal antibody that comprise this medication are necessary ingredients. Its primary benefits are for patients who have had at least two previous treatments for metastatic disease. Trodelvy is performed when surgical removal of the cancerous tissue is not feasible. The main medicinal ingredient is sacituzumab govitecan-hziy, which is a mix of a Trop-2-directed antibody and a topoisomerase inhibitor. It is important to keep in mind that Trodelvy can only be prescribed by licensed medical professionals. To buy trodelvy in India and make it accessible to a wider community, get in touch with The Indian Pharma.

Available as lyophilized powder: Trodelvy must be given in accordance with FDA-approved cycles, and the dosage is directly correlated with the patient's body weight. An intravenous dose of 10 mg/kg is given twice a day, on the first and the eighth day of each repeating 21-day cycle. Sacituzumab govitecan-hziy must be dosed accurately based on the patient's weight because it is a lyophilized powder. To create a concentration of 10 mg/mL, the vial is mixed with 20 mL of 0.9% sodium chloride injection, USP.Trodelvy 180mg is a reasonably priced medication that is readily accessible in the market

Use In Chemotherapy: As part of the treatment regimen, a 5-HT3 receptor antagonist or an NK1 receptor antagonist is given as a premedication along with dexamethasone. This premedication approach lessens the chance that infusion reactions and chemotherapy will cause nausea and vomiting. The reason Trodelvy is so reasonably priced in India is its unique blend of a topoisomerase inhibitor and an anti-Trop-2 antibody. In individuals who have not responded well to earlier infusions, corticosteroids should be given. For additional information on the trodelvy cost , get in touch with Indian Pharma, a licensed distributor of this drug.

Potency of The Drug : Trodelvy offers hope to patients with advanced triple-negative breast cancer who have undergone at least two prior therapies. What makes it successful is how it interacts with SN-38, a small molecule that is crucial to its mode of action. The drug's potency is further increased by Trodelvy's monoclonal antibody's ability to bind to the Trop-2 protein present on a range of breast cancer cells. An additional advantage of Trodelvy is its cost-effectiveness, which is made possible by Indian Pharma. For individuals who would like additional information regarding the Trodelvy price. Along with anemia, more than one in five patients undergoing therapy for metastatic triple-negative breast cancer may also experience baldness, decreased appetite, coughing, stomach discomfort, and exhaustion.

Use Under Prescription: One of the potential negative effects of Trodelvy treatment is the emergence of severe or possibly fatal neutropenia. It is necessary to temporarily halt the administration of trodelvy in patients who have neutropenic fever or an absolute neutrophil count below 1500/mm3. It is essential to regularly evaluate blood cell counts during the course of treatment. It makes sense to utilize G-CSF for secondary prevention. In patients with feverish neutropenia, anti-infective treatment ought to be initiated promptly. It's crucial to remember that the cost of Trodelvy injection is reasonably priced and accessible for those who have a valid prescription.

Therapeutic Effects: The active component of Trodelvy that promotes its therapeutic effects is sacituzumab govitecan-hziy. Inactive ingredients in trodelvy include trehalose dihydrate, polysorbate 80, and 2-(N-morpholino) ethane sulfonic acid. 180 mg and 200 mg are the available strengths. Sacituzumab govitecan-hziy has shown promise in treating progesterone- and oestrogen-receptor-negative breast cancer because of its mechanism of action.For those who want to buy Trodelvy from India at a discount, you can get it through The Indian Pharma.

Negative Reactions: Those who have previously experienced a significant negative reaction to trodelvy shouldn't use it. There is a chance of serious hypersensitivity reactions with sacituzumab govitecan-hziy, including potentially lethal anaphylactic reactions. A few of the reactions that could happen are hypotension, wheezing, angioedema, swelling, pneumonitis, and skin reactions. To lessen the effects of the infusion, premedication is recommended. It's also advisable to have an emergency supply of medications and supplies on hand to manage any potential infusion-related complications, such as anaphylaxis, when administering sacituzumab govitecan-hziy. For more information on trodelvy injection price in India.

0 notes

Text

DelveInsight Total Knee Arthroplasty Market Overview

Total Knee Arthroplasty (TKA), or total knee replacement, has significantly improved the quality of life for millions affected by chronic knee pain caused by osteoarthritis, rheumatoid arthritis, and other degenerative joint conditions. The increasing demand for this procedure is driven by advancements in medical technology, an aging population, and a rise in musculoskeletal disorders globally.

DelveInsight’s “Total Knee Arthroplasty Market Insight Report” provides an extensive analysis of market dynamics, key trends, and the competitive landscape, offering valuable insights into emerging opportunities and challenges for industry stakeholders.

Key Drivers of Market Growth for Total Knee Arthroplasty

Several factors are driving the growth of the TKA market:

Technological Advancements: Innovations such as patient-specific implants, robotic-assisted surgeries, and minimally invasive techniques are enhancing patient outcomes and accelerating recovery times.

Increasing Prevalence of Arthritis: As arthritis remains a leading cause of disability, the demand for TKA procedures continues to rise.

Aging Population: With the aging demographic being a primary risk factor for degenerative joint diseases, the market benefits from the growing elderly population in need of TKA surgeries.

Discover how technological advancements are shaping the Total Knee Arthroplasty market by downloading DelveInsight’s detailed report. Access Now! @ Total Knee Arthroplasty Treatment Market

Regional Market Insights

North America: The largest TKA market, driven by high rates of osteoarthritis, advanced healthcare infrastructure, and extensive adoption of innovative technologies.

Europe: Increasing healthcare expenditures and greater awareness of joint replacement procedures are fueling market growth in this region.

Asia-Pacific: This region is experiencing rapid growth due to improving healthcare systems and a growing aging population driving the demand for TKA procedures.

Challenges and Opportunities

While the market presents significant growth potential, challenges such as high costs, postoperative complications, and limited healthcare access in lower-income regions remain. These challenges also provide opportunities for market expansion and innovation in underserved areas.

Download DelveInsight’s comprehensive market report to gain strategic insights into the Total Knee Arthroplasty industry. Get Your Copy Today! @ Total Knee Arthroplasty Drugs Market

Competitive Landscape

The Total Knee Arthroplasty Companies is highly competitive, with major companies focusing on innovation to meet the evolving needs of patients. Key players in the market include:

Zimmer Biomet

DePuy Synthes (Johnson & Johnson)

Stryker Corporation

Smith & Nephew

B. Braun Melsungen AG

These Total Knee Arthroplasty Companies are investing heavily in R&D to enhance implant materials, surgical tools, and patient outcomes.

Market Outlook

The Total Knee Arthroplasty market is expected to grow significantly, driven by continuous technological advancements, greater healthcare awareness, and evolving patient expectations. As the market evolves, improvements in accessibility, outcomes, and cost-effectiveness will likely occur.

Explore Top-Selling Market Research Reports:

Varicose Vein Treatment Devices Market | Vascular Access Devices Market | Indwelling Catheters Market | Healthcare Competitive Benchmarking | Lymphoedema Market | Pacemakers Market | Myeloproliferative Neoplasms Market | Surgical Mask & Respirator Market | NK Cell Therapy Market | Novel Drug Delivery Devices Market | Testicular Neoplasm Market | Phototherapies for Psoriasis Market | Skin Neoplasm Market | Microscopy Device Market | Bone Growth Stimulator Market | Urea Cycle Disorders Market | Antibody Drug Conjugate Market | Penile Cancer Market | Total Knee Arthroplasty Market | Cardiac Implantable Electronic Devices Market | Dyspepsia Market | Lactose Intolerance Market | Medical Marijuana Market | Asperger Syndrome Market | Catheter Stabilization Devices Market

Another Report Offered By Delveinsight

Non Alcoholic Fatty Liver Disease Nafld Market | Xerostomia Market | Adrenal Cortex Neoplasms Market | Arthroscopy Devices Market | Bone Anchored Hearing Systems Market | Cough Assisted Device Market | Neuroblastoma Market | Pharma Licensing Services | Allergic Rhinitis Market | Alpha-mannosidosis Market | Bronchopulmonary Dysplasia Market | Burkitt Lymphoma Market | Chronic Rhinosinusitis Market | Chronic Rhinosinustis Market | Contraceptive Devices Market | Febrile Neutropenia Market | Hepatitis B Virus Market | Minimal Residual Disease Market | Non-st Segment Elevation Acute Coronary Syndromes Market | Nsclc Market | Prefilled Syringes Market | Walking Impairment In Multiple Sclerosis Market | Acute On Liver Failure Market

About DelveInsight

DelveInsight is a leading market research and consulting firm specializing in the life sciences and healthcare industries. By delivering actionable insights, DelveInsight empowers pharmaceutical, biotech, and medical device companies to make informed decisions in rapidly changing markets.

Contact Information Kanishk Email: [email protected]

0 notes

Text

The Leukemia Therapeutics Treatment Market is projected to grow from USD 15296.7 million in 2024 to an estimated USD 26086.71 million by 2032, with a compound annual growth rate (CAGR) of 6.9% from 2024 to 2032.Leukemia, a type of cancer affecting blood and bone marrow, remains a significant global health challenge. With increasing cases worldwide and advancements in medical research, the leukemia therapeutics treatment market is experiencing robust growth.

Browse the full report at https://www.credenceresearch.com/report/leukemia-therapeutics-treatment-market

Market Overview

Leukemia is classified into several types, including acute lymphoblastic leukemia (ALL), acute myeloid leukemia (AML), chronic lymphocytic leukemia (CLL), and chronic myeloid leukemia (CML). The treatment options vary by type and severity, ranging from chemotherapy and radiation therapy to targeted therapy and bone marrow transplantation.

In recent years, the market for leukemia therapeutics has expanded significantly, driven by technological advancements, increased prevalence of the disease, and rising healthcare investments. According to industry reports, the global leukemia treatment market was valued at approximately USD 12 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 7.5% through 2030.

Key Market Drivers

Rising Incidence of Leukemia:

The increasing global burden of leukemia is a primary growth driver. Factors such as aging populations, environmental exposures, and genetic predispositions contribute to the rising incidence rates.

Advancements in Precision Medicine:

Targeted therapies, such as tyrosine kinase inhibitors (TKIs) and monoclonal antibodies, have revolutionized treatment approaches. These therapies offer greater efficacy with fewer side effects compared to traditional chemotherapy.

Development of Immunotherapies:

Immunotherapies, including CAR-T cell therapy and immune checkpoint inhibitors, are at the forefront of innovation. These therapies leverage the body's immune system to fight cancer cells, offering promising outcomes for patients with advanced stages of leukemia.

Increased Funding and Research:

Governments and private entities are investing heavily in cancer research and drug development. For instance, initiatives like the Cancer Moonshot in the United States aim to accelerate the discovery of new therapies.

Favorable Regulatory Landscape:

Expedited drug approvals and orphan drug designations by regulatory bodies like the FDA and EMA encourage the development of novel leukemia treatments.

Challenges in the Market

Despite significant progress, the leukemia therapeutics market faces several challenges:

High Treatment Costs:

Advanced therapies like CAR-T can cost hundreds of thousands of dollars, making them inaccessible to many patients, especially in low- and middle-income countries.

Side Effects and Resistance:

While targeted therapies have improved outcomes, issues like drug resistance and adverse effects remain critical concerns.

Complexity of Clinical Trials:

Developing leukemia drugs often involves complex and lengthy clinical trials, delaying time-to-market for new treatments.

Disparities in Access:

Geographic and economic disparities limit access to cutting-edge treatments, with patients in developing regions particularly disadvantaged.

Emerging Trends

Gene and Cell Therapy:

Gene-editing technologies like CRISPR and advancements in cell therapy are paving the way for personalized treatments that address the genetic basis of leukemia.

Artificial Intelligence in Drug Development:

AI and machine learning are being leveraged to accelerate drug discovery, optimize clinical trial design, and identify patient-specific treatment strategies.

Combination Therapies:

Researchers are exploring the potential of combining multiple therapeutic approaches, such as targeted therapy with immunotherapy, to improve treatment outcomes.

Biosimilars:

As patents for blockbuster drugs expire, biosimilars are entering the market, offering cost-effective alternatives and increasing patient accessibility.

Future Outlook

The leukemia therapeutics treatment market is poised for transformative growth, fueled by continuous innovation and an increasing focus on precision medicine. Collaboration among pharmaceutical companies, academic institutions, and governments will be crucial in overcoming existing challenges and ensuring equitable access to life-saving treatments.

Key Player Analysis:

AbbVie (North Chicago, U.S.)

Amgen Inc. (Thousand Oaks, U.S.)

Bristol-Myers Squibb (New York, USA)

Hoffmann-La Roche (Basel, Switzerland)

Johnson & Johnson Services, Inc. (New Brunswick, U.S.)

Lupin Ltd. (India, Mumbai)

Novartis (Basel, Switzerland)

Pfizer Inc. (New York, U.S.)

Sanofi/ Genzyme Corporation (Paris, France)

Takeda Pharmaceutical Co Ltd (Tokyo, Japan)

Segmentation:

By Type of Leukemia

Acute lymphocytic leukemia (ALL)

Chronic lymphocytic leukemia (CLL)

Acute myeloid leukemia (AML)

Chronic myeloid leukemia (CML)

By Treatment Type

Targeted drugs & immunotherapy

Chemotherapy

By Molecule Type

Small Molecules

Biologics

By Mode of Administration

Injectable

Oral

By Gender

Male

Female

By Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/leukemia-therapeutics-treatment-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Introduction to Biopharmaceuticals: Advancing Modern Medicine

The global biopharmaceutical market size was USD 411.4 Billion in 2022 and is expected to register a rapid revenue CAGR of 15.2% during the forecast period. Rising investments in Research & Development (R&D) and technological advancements in biopharmaceuticals are key factors driving market revenue growth.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/2693

Competitive Terrain:

The global Biopharmaceutical industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

BIONIK Inc., Ectron Limited, Rehabtronics, Abbott, Medtronic, Hocoma, Biometrics Ltd, BIONIK Inc., Ekso Bionics, and Kinestica

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Biopharmaceutical market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Biopharmaceutical market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Biopharmaceutical market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/2693

Market Segmentations of the Biopharmaceutical Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Biopharmaceutical market on the basis of product, application, and region:

Segments Covered in this report are:

Product Type Outlook (Revenue, USD Billion; 2019-2032)

Monoclonal Antibodies

Recombinant Growth factor

Vaccine

Recombinant Hormone

Purified Protein

Others

Application Outlook (Revenue, USD Billion; 2019-2032)

Oncology

Inflammatory

Autoimmune

Infectious

Metabolic Disorder

Cardiovascular Diseases (CVDs)

End-Use Outlook (Revenue, USD Billion; 2019-2032)

Big-biopharma Companies

Small Biopharma Companies

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/biopharmaceutical-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/2693

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

mRNA Synthesis & Manufacturing Market worth $738.3 million by 2029

The mRNA synthesis and manufacturing market is projected to reach USD 738.3 million in 2029 from USD 624.4 million in 2024. This market is projected to grow at a CAGR of 3.4% over the forecast period. The primary drivers behind the expansion of this industry are the Growing focus on mRNA-based vaccine development, expanding therapeutic applications of mRNA technology, advancements in mRNA synthesis technology, increased outsourcing for mRNA synthesis and modification, and collaborations among industry players. However, stability, storage, and manufacturing scalability present a challenge to this industry. This is further amplified by the slow patient adoption rate and the complexity of the development of mRNA-based therapy.

In many important respects, artificial intelligence (AI) is transforming the mRNA synthesis and manufacturing sector. First, by scanning large databases to find suitable mRNA sequences for therapeutic usage, artificial intelligence speeds up drug research and development greatly. Developed tools like the LinearDesign AI aim to maximize mRNA sequences, therefore producing vaccines with more antibody responses than conventional techniques. From raw material acquisition to final product packaging, artificial intelligence maximizes several manufacturing steps, thereby lowering costs and raising efficiency. AI-powered predictive maintenance reduces downtime and guarantees manufacturing equipment's seamless running.

Download PDF Brochure:

Browse in-depth TOC on "mRNA Synthesis & Manufacturing Market"

250 - Tables

50 - Figures

250 - Pages

The market is expanding rapidly due to factors such as the development of mRNA-based vaccines and expanded applications such as cancer immunotherapies. Furthermore, improvements in mRNA synthesis technology, a rise in mRNA synthesis and modification outsourcing, and industry players working together to create mRNA therapies all contribute to the growth of the mRNA synthesis and manufacturing market. Additionally, factors such as advancements in drug delivery technologies, growth in the regenerative medicines market, and increasing government funding and private investments in the mRNA therapeutics market will further provide revenue growth opportunities for the players operating in mRNA synthesis & manufacturing.

Based on product type, the mRNA synthesis and manufacturing products market is divided into two broad categories, consumables and instruments. The consumables segment of the market held the largest market share in 2023, due to the sustained use of consumables such as nucleotides, RNA polymerase, reverse transcriptase, buffer, and reagents that also require frequent repurchases. The consumables segment will be experiencing high growth due to several factors, including an increase in the mRNA therapeutics pipeline and growing investments made to develop mRNA-based therapeutics, advancement in mRNA synthesis technologies, increase in demand for consumables among contract service providers with the growing trend of outsourcing.

Based on service type, the global mRNA synthesis and manufacturing services market has been categorized into four service types: mRNA synthesis, modification, and related activities; purification of mRNA; analytical and characterization services; and scale-up and manufacture activities. In 2023, the mRNA synthesis and modification services captured the highest market share because of the demand for custom and modified mRNA sequences, which are intended to enhance therapeutic candidates for the molecules market. Given the expanding uses of the mRNA technology, researchers and developers are looking for mRNA sequences that can incorporate protein expression enhancement or immune response improvement.

Based on application, the market for mRNA synthesis and manufacturing has been divided into segments including vaccines and cell & gene therapy. The vaccine segment has the dominant share in the market in 2023. The large share of this segment can be supported by the large number of clinical trials of mRNA vaccines for various diseases infectious diseases, cancer and rare genetic disorders. The remarkable success of mRNA-based COVID-19 vaccines has not only proven the efficacy & scalability of mRNA technology but also catalysed interest in targeting other therapy areas, such as cancer and rare diseases.

Based on end user, the mRNA synthesis and manufacturing market has been categorized into pharmaceutical and biotechnology companies, academic and research institutes, and CROs and CDMOs. In 2023, pharmaceutical and biotechnology companies dominated the market for mRNA synthesis and manufacturing. According to the market's emerging needs, companies are investing to develop next-generation biologics such as mRNA therapeutics. Higher research and development activities of companies to develop mRNA therapeutics and cell and gene therapies have resulted in rising needs for specialized consumables and instruments as well as synthesis, modification, purification, analysis, and characterization services.

Request Sample Pages:

The global mRNA synthesis and manufacturing market is consolidated with the top five players— Thermo Fisher Scientific Inc. (US), Aldevron, LLC. (Danaher Corporation) (US), TriLink BioTechnologies (US), GenScript (US), and Merck KGaA (Germany). Other prominent market players include, New England Biolabs (US), Promega Corporation (US), Sartorius AG (Germany), WuXi Biologics (China), Takara Bio Inc. (Japan), GENEWIZ (Azenta US, Inc.) (US), Lonza (Switzerland), Telesis Bio Inc. (US), Aurigene Pharmaceutical Services Ltd. (Dr. Reddy's Laboratories Ltd.) (India), ST Pharm (South Korea), AGC Biologics (US).

Thermo Fisher Scientific Inc. (US):

Thermo Fisher Scientific Inc., headquartered in Waltham, Massachusetts, is a leading player in mRNA synthesis and manufacturing, offering a broad range of products and services tailored to this field. The company provides advanced solutions for mRNA synthesis, including custom RNA synthesis services and reagents through its GeneArt platform, which supports the development of mRNA constructs for research, therapeutic, and vaccine applications. Thermo Fisher's technologies enable efficient in vitro transcription (IVT) and include automated solutions that enhance scalability and production efficiency. Their extensive expertise, quality assurance measures, and global reach position them as a key player in advancing mRNA technology and supporting the development of next-generation therapeutics and vaccines.

Aldevron, LLC. (Danaher Corporation) (US):

Aldevron, established in 1998 and based in Fargo, North Dakota, is a key player in the nucleic acid synthesis industry, particularly known for its expertise in mRNA synthesis and manufacturing. The company is highly regarded for producing high-quality mRNA and plasmid DNA, essential for cutting-edge applications in vaccine development, gene therapy, and other biotechnological innovations. Aldevron's offerings include custom RNA synthesis and cGMP-compliant mRNA production, ensuring that their products meet the stringent standards required for clinical use. Aldevron's robust quality control and assurance processes further guarantee the reliability and efficacy of their products. As a global leader in the field, Aldevron has expanded its facilities and technological infrastructure to meet growing demand, establishing a significant presence in the biopharmaceutical sector. Their collaborations with biotechnology firms, pharmaceutical companies, and research institutions underscore their pivotal role in advancing mRNA technology and supporting the development of next-generation therapies and vaccines.

TriLink BioTechnologies (US):

TriLink BioTechnologies, a subsidiary of Maravai LifeSciences based in San Diego, California, is a key player in mRNA synthesis and manufacturing. The company excels in providing high-quality nucleic acid products and services, with a strong focus on mRNA technology. TriLink offers comprehensive mRNA synthesis services, including the production of custom mRNA and chemically modified mRNA, which enhances stability and translation efficiency—crucial for effective therapeutic and vaccine development. Utilizing advanced in vitro transcription technologies, TriLink ensures high yield and purity in their mRNA products.

For more information, Inquire Now!

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America's best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact:

Mr. Rohan Salgarkar

MarketsandMarkets Inc.

1615 South Congress Ave.

Suite 103, Delray Beach, FL 33445

USA : 1-888-600-6441

UK +44-800-368-9399

Email: [email protected]

Visit Our Website: https://www.marketsandmarkets.com/

0 notes

Text

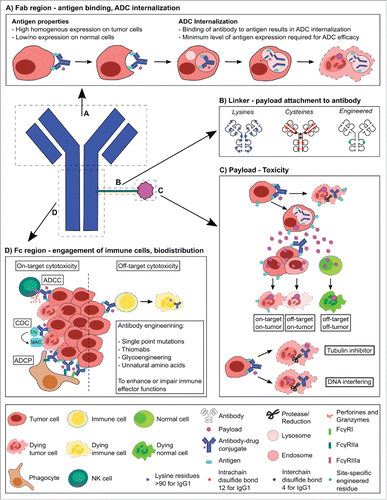

🌟 𝐓𝐫𝐚𝐧𝐬𝐟𝐨𝐫𝐦𝐢𝐧𝐠 𝐂𝐚𝐧𝐜𝐞𝐫 𝐓𝐫𝐞𝐚𝐭𝐦𝐞𝐧𝐭: 𝐓𝐡𝐞 𝐑𝐢𝐬𝐞 𝐨𝐟 𝐀𝐧𝐭𝐢𝐛𝐨𝐝𝐲 𝐃𝐫𝐮𝐠 𝐂𝐨𝐧𝐣𝐮𝐠𝐚𝐭𝐞𝐬 (𝐀𝐃𝐂𝐬) 🌟-IndustryARC™

The Antibody Drug Conjugate Market size is estimated to reach $15275 million by 2030, growing at a CAGR of 14.20% during the forecast period 2024-2030.

👉 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞

𝐇𝐞𝐫𝐞 𝐚𝐫𝐞 ��𝐨𝐦𝐞 𝐤𝐞𝐲 𝐟𝐢𝐧𝐝𝐢𝐧𝐠𝐬 𝐟𝐫𝐨𝐦 𝐭𝐡𝐞 𝐫𝐞𝐩𝐨𝐫𝐭

𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬 𝐢𝐧 𝐓𝐚𝐫𝐠𝐞𝐭𝐞𝐝 𝐓𝐡𝐞𝐫𝐚𝐩𝐲: ADCs represent a targeted approach to cancer therapy, allowing for selective delivery of cytotoxic drugs to cancer cells, reducing damage to healthy cells and enhancing treatment effectiveness. This shift towards targeted therapies is a major trend in oncology.

𝐆𝐫𝐨𝐰𝐢𝐧𝐠 𝐏𝐢𝐩𝐞𝐥𝐢𝐧𝐞 𝐨𝐟 𝐀𝐃𝐂𝐬: Pharmaceutical companies are actively developing ADCs, with a growing number of ADC candidates in clinical trials. Increased R&D investments and strategic collaborations are fueling the expansion of ADC pipelines, particularly for solid tumors and hematologic cancers.

𝐈𝐧𝐜𝐫𝐞𝐚𝐬𝐢𝐧𝐠 𝐅𝐃𝐀 𝐀𝐩𝐩𝐫𝐨𝐯𝐚𝐥𝐬 𝐚𝐧𝐝 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐒𝐮𝐩𝐩𝐨𝐫𝐭: Regulatory bodies are accelerating approvals for ADCs due to their effectiveness and safety profile in cancer treatment. Recent approvals of ADCs, such as those targeting breast and bladder cancers, have driven further interest and investment.

𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐈𝐦𝐩𝐫𝐨𝐯𝐞𝐦𝐞𝐧𝐭𝐬 𝐢𝐧 𝐋𝐢𝐧𝐤𝐞𝐫 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐲: Innovations in linker technology, which attaches the antibody to the drug payload, are enhancing ADC stability and precision. Advanced linkers improve the therapeutic index, enabling more controlled drug release and minimizing off-target effects.

𝐅𝐨𝐜𝐮𝐬 𝐨𝐧 𝐍𝐨𝐯𝐞𝐥 𝐏𝐚𝐲𝐥𝐨𝐚𝐝𝐬: ADCs are moving beyond traditional cytotoxic agents, incorporating novel payloads such as immune modulators and DNA-damaging agents. These novel payloads expand ADC applications and offer enhanced potency against resistant cancer cells.

𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐢𝐧𝐭𝐨 𝐍𝐨𝐧-𝐎𝐧𝐜𝐨𝐥𝐨𝐠𝐲 𝐀𝐩𝐩𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬: While oncology remains the primary focus, ADCs are increasingly being explored for autoimmune and infectious diseases. This diversification presents new opportunities and broadens the market’s scope beyond cancer.

#antibodydrugconjugates#oncology#cancertherapy#targetedtherapy#precisionmedicine#cancerresearch#biotechnology#drugdevelopment#pharma#cancerimmunotherapy#biopharma#noveltherapeutics#tumortargeting#personalizedmedicine

0 notes

Text

Mononucleosis Diagnostic Market

Mononucleosis Diagnostic Market Size, Share, Trends: Abbott Laboratories Lead

Integration of Artificial Intelligence and Machine Learning in Diagnostic Platforms

Market Overview:

The global Mononucleosis Diagnostic Market is projected to grow at a CAGR of 5.8% from 2024 to 2031. The market size is expected to reach XX in 2024 and YY by 2031. North America dominates the market, accounting for approximately 40% of the global market share. Key metrics include increasing incidence of Epstein-Barr virus infections, advancements in diagnostic technologies, and growing awareness about early disease detection.

The mononucleosis diagnostic market is steadily growing, owing to the increasing prevalence of infectious mononucleosis, particularly among teenagers and young adults. Demand for accurate and quick diagnostic tests is driving market growth, aided by technological advances in immunoassays and molecular diagnostics.

DOWNLOAD FREE SAMPLE

Market Trends:

The mononucleosis diagnostic market is undergoing a considerable change towards the integration of artificial intelligence (AI) and machine learning (ML) into diagnostic systems. This development is driven by the demand for higher accuracy, faster turnaround times, and better data interpretation in mononucleosis tests.

Recent research has yielded encouraging findings for AI-assisted diagnosis in infectious diseases. A pilot study of 500 mononucleosis cases found that using AI algorithms to analyze EBV antibody test results improved diagnostic accuracy by 20% compared to conventional approaches. Industry experts expect that by 2026, more than 30% of high-volume diagnostic laboratories will have integrated AI-powered technologies into their mononucleosis testing workflows, potentially lowering false-negative rates and enhancing overall diagnostic efficiency.

Market Segmentation:

The EBV Antibody Test segment dominates the mononucleosis diagnostic market, accounting for over 45% of the market share.

EBV antibody tests, which include VCA IgM, VCA IgG, and EBNA IgG antibodies, have established as the gold standard for accurately diagnosing mononucleosis. This segment's dominance is due to its high specificity and capacity to identify the stage of infection, which is critical for optimal patient care.

Market statistics supports the expansion of the EBV Antibody Test segment. A survey of 1,000 infectious disease doctors found that 80% choose EBV serology as the primary diagnostic method for probable mononucleosis cases. The segment is likely to maintain its dominance until 2031, driven by advances in multiplex serology platforms and the incorporation of automated interpretation algorithms.

Market Key Players:

Abbott Laboratories

Beckman Coulter, Inc. (Danaher Corporation)

Bio-Rad Laboratories, Inc.

DiaSorin S.p.A.

Meridian Bioscience, Inc.

Quidel Corporation

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Antibody Drug Conjugates Market: Overview, Target Demographics, Competitive Analysis, and Forecast to 2034

Antibody-drug conjugates (ADCs) are a cutting-edge advancement in cancer therapy, combining monoclonal antibodies with powerful cytotoxic agents for targeted treatment. This approach enhances therapeutic effectiveness while reducing systemic side effects, positioning ADCs as a transformative solution in oncology. With cancer rates rising globally, the ADC market is set to experience significant growth in the coming years.

Market Size and Target Demographics

The antibody-drug conjugate market is forecasted to grow at a strong compound annual growth rate (CAGR) from 2024 to 2034. The growth is fueled by the increasing prevalence of cancers such as breast, lung, and hematological malignancies, which are key indications for ADCs.

Innovative technologies, including site-specific conjugation and improved linker designs, are enhancing ADCs’ safety and efficacy. The primary target group for these therapies consists of patients with relapsed or refractory cancers, where traditional treatments often fall short. Additionally, the growing number of FDA-approved ADCs with expanded therapeutic applications is broadening the potential patient base and further driving market growth.

Competitive Landscape

The ADC Comapnies is highly competitive, with established pharmaceutical companies and emerging biotech firms heavily investing in research and development. Major players include:

Seagen Inc.

AstraZeneca

Pfizer

Daiichi Sankyo

Roche

Gilead Sciences

Takeda Pharmaceutical Company

These organizations are advancing ADC technology through the development of more potent payloads, refined linker systems, and enhanced antibody specificity. Collaborations between biotech innovators and large pharmaceutical firms are expediting the development of next-generation ADCs, further shaping the competitive landscape.

Market Forecast

By 2034, the ADC market is expected to expand substantially, driven by increasing regulatory approvals and a growing pipeline of clinical trials. The introduction of novel ADCs targeting a broader spectrum of cancers, alongside advancements in precision medicine, is anticipated to fuel this growth.

Conclusion

The antibody-drug conjugate market is poised for exceptional growth through 2034. With continuous innovation and an expanding range of therapeutic applications, ADCs are revolutionizing cancer treatment and providing new hope for patients with limited treatment options.

Related Reports by DelveInsight

Primary Progressive Multiple Sclerosis Market

Vascular Graft Devices Market

Vascular Stents Market

Extracorporeal Membrane Oxygenation Devices Market

Fallopian Tube Cancer Market

Physiotherapy Equipment Market

Postoperative Nausea and Vomiting Market

Relapsing Multiple Sclerosis Market

Respiratory Distress Syndrome Market

Interspinous Spacers Market

Resorbable Vascular Scaffold Market

Smart Inhalers Market

Diverticulosis Market

Fenebrutinib Market

Indolent Lymphoma Market

Optic Neuropathy Market

About DelveInsight

DelveInsight is a premier market research and consulting firm specializing in the life sciences and healthcare industries. By offering actionable insights, DelveInsight supports pharmaceutical, biotech, and medical device companies in making informed strategic decisions in dynamic and competitive markets.

Contact Information: Kanishk Email: [email protected]

0 notes

Text

The Glioblastoma Treatment Drugs Market is projected to grow from USD 2665 million in 2024 to an estimated USD 5589.2 million by 2032, with a compound annual growth rate (CAGR) of 9.7% from 2024 to 2032. Glioblastoma multiforme (GBM) is the most aggressive and common type of primary brain tumor in adults. Known for its rapid progression and resistance to standard therapies, GBM presents a significant challenge to healthcare professionals and researchers worldwide. The growing prevalence of glioblastoma, coupled with advancements in oncology, has spurred significant developments in the glioblastoma treatment drugs market.

Browse the full report at https://www.credenceresearch.com/report/glioblastoma-treatment-drugs-market

Market Overview

The glioblastoma treatment drugs market is experiencing steady growth, driven by the increasing incidence of GBM and rising investments in cancer research. According to recent statistics, the global glioblastoma treatment market was valued at approximately USD 2.1 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of around 8% during the forecast period of 2023–2030.

Current Treatment Options

The primary treatment for glioblastoma typically involves surgical resection, followed by radiation therapy and chemotherapy. Temozolomide (TMZ), an oral alkylating agent, remains the gold standard chemotherapy drug for GBM treatment. However, the recurrence of glioblastoma post-treatment remains a critical concern.

To address these challenges, several new drugs and therapeutic approaches are entering the market, including:

Targeted Therapies Drugs targeting specific molecular pathways, such as EGFR (epidermal growth factor receptor) inhibitors, have shown promise. Agents like bevacizumab, an anti-VEGF (vascular endothelial growth factor) monoclonal antibody, are being used to control tumor angiogenesis and prolong progression-free survival.

Immunotherapies Immunotherapy has emerged as a game-changer in oncology. Immune checkpoint inhibitors, cancer vaccines, and adoptive T-cell therapies are being explored to harness the body’s immune system to fight glioblastoma. Clinical trials of drugs like nivolumab are underway, aiming to improve patient outcomes.

Gene and Cell-Based Therapies Advances in gene editing and cell-based therapies have paved the way for personalized medicine in glioblastoma treatment. Oncolytic viral therapies, which use genetically modified viruses to target cancer cells, are gaining traction in research and development pipelines.

Challenges in the Market

Despite significant progress, the glioblastoma treatment drugs market faces several hurdles:

High Costs: Advanced therapies often come with a hefty price tag, limiting access for many patients.

Complex Biology of GBM: The heterogeneity and adaptability of glioblastoma tumors make them highly resistant to treatment.

Regulatory Barriers: Stringent approval processes for new drugs can delay market entry.

Future Outlook

The future of the glioblastoma treatment drugs market looks promising, driven by ongoing research and technological advancements. The integration of artificial intelligence and big data analytics in drug discovery is expected to expedite the development of effective treatments. Additionally, combination therapies that incorporate multiple approaches—such as chemotherapy, immunotherapy, and gene therapy—are likely to emerge as the new standard of care.

Government initiatives to support cancer research and increasing funding from private organizations further bolster the market’s growth potential. However, addressing the affordability and accessibility of these advanced treatments remains crucial to ensuring better outcomes for patients worldwide.

Key Player Analysis:

Amgen, Inc.

Amneal Pharmaceuticals

Arbor Pharmaceuticals, LLC

AstraZeneca PLC

Hoffmann-La Roche Ltd.

Gene Therapy

GlaxoSmithKline plc (GSK)

Glioma Steam Cell Targeting

Johnson & Johnson

Karyopharm Therapeutics, Inc.

Kinase Inhibitor

Merck & Co., Inc.

MiRNA Targeting

Novartis AG

Pfizer Inc.

Roche Holding AG

Sanofi S.A.

Sun Pharmaceutical Industries Ltd.

Teva Pharmaceutical Industries Ltd.

Segmentation:

By Treatment

Surgery

Radiation Therapy

Chemotherapy

Targeted Therapy

Tumor Treating Field (TTF) Therapy

Immunotherapy

By Drug Class:

Antineoplastic

VEGF/VEGFR Inhibitors

Alkylating Agents

Miscellaneous Antineoplastic

By Distribution Channel:

Hospitals

Cancer Research Organizations

Long Term Care Centers

Diagnostic Centers

By Region:

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/glioblastoma-treatment-drugs-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Text

Introduction to Monoclonal Antibodies: Basics and Mechanisms of Action

The global monoclonal antibodies market size was USD 204.42 billion in 2022 and is expected to register a revenue CAGR of 10.8% during the forecast period. Rising adoption in personalized medicine and precision therapies, expanding regulatory approvals of monoclonal antibodies by regulatory agencies across the globe, and increasing technological advancements in biotechnology and immunology are some of the factors expected to drive market revenue growth.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/2533

Competitive Terrain:

The global Monoclonal Antibodies industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

Novartis AG; Pfizer Inc; GlaxoSmithKline plc; Amgen Inc.; Merck & Co., Inc.; Daiichi Sankyo Company, Limited; Abbott Laboratories; AstraZeneca plc; Eli Lilly And Company; Johnson & Johnson Services, Inc.; Bayer AG; Bristol Myers Squibb; F. Hoffman-La Roche Ltd.; Viatris Inc.; Biogen Inc.; Thermo Fisher Scientific, Inc.; Novo Nordisk A/S; Sanofi S.A., and Teva Pharmaceutical Industries Ltd

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Monoclonal Antibodies market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Monoclonal Antibodies market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Monoclonal Antibodies market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/2533

Market Segmentations of the Monoclonal Antibodies Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Monoclonal Antibodies market on the basis of product, application, and region:

Segments Covered in this report are:

Source Outlook (Revenue, USD Billion; 2019-2032)

Humanized mAb

Human mAb

Murine mAb

Chimeric mAb

Indication Outlook (Revenue, USD Billion; 2019-2032)

Cancer

Breast cancer

Colorectal cancer

Lung cancer

Ovarian cancer

Others

Autoimmune Diseases

Inflammatory Diseases

Infectious Diseases

Others

Production Type Outlook (Revenue, USD Billion; 2019-2032)

In Vivo

In Vitro

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/monoclonal-antibodies-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/2533

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: www.emergenresearch.com

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Visit for More Insights: https://www.emergenresearch.com/insights

Explore Our Custom Intelligence services | Growth Consulting Services

Trending Titles: Geocell Market | Pancreatic Cancer Treatment Market

Latest Report: Ceramic Tiles Market | Life Science Analytics Market

0 notes

Text

Global Gastrointestinal Drugs Market Size, Share, Growth and Forecast 2031

Global gastrointestinal drugs market is projected to witness a CAGR of 4.23% during the forecast period 2024-2031, growing from USD 45.20 billion in 2023 to USD 62.96 billion in 2031. The market’s growth is boosted by the rising cases of gastrointestinal diseases, novel product launches by the market players, and increasing emphasis on ensuring the availability of gastrointestinal drugs in different regions across the globe.

Technological advancements in drug delivery mechanisms and formulations are enhancing the efficacy of gastrointestinal drugs. The advancements include the development of extended-release and delayed-release formulations that aid in improving the bioavailability and absorption of the drugs, resulting in improved patient outcomes. Such developments are revolutionizing the treatment of ulcerative colitis and Crohn’s disease, among others, providing lucrative growth opportunities for the market.