#Polyphenylene Ether Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Hackers stole 65M passwords from Tumblr in 2013.

Text

Polyphenylene Ether Compounds Market: A Deep Dive into Regional Market Trends

Polyphenylene Ether Compounds Market: An Overview

The Polyphenylene Ether Compounds market is a dynamic and evolving segment of the chemical industry. These compounds, often referred to as PPE, are high-performance thermoplastics known for their exceptional thermal and electrical insulating properties. They find widespread use in various applications across industries, making them a critical part of the global market.

Definition: Polyphenylene Ether Compounds, or PPE compounds, are a class of thermoplastic polymers known for their high-temperature resistance, dimensional stability, and excellent electrical insulating properties. They are primarily derived from polyphenylene ether resin and various additives, resulting in a versatile material suitable for a range of applications.

Market Overview & Scope: The Polyphenylene Ether Compounds market has witnessed steady growth in recent years due to their unique combination of properties. These compounds are extensively used in the automotive, electrical and electronics, and industrial sectors. In the automotive industry, PPE compounds are employed in various parts, such as connectors, switches, and motor components, due to their ability to withstand high temperatures and resist electrical arcing. Moreover, the growing demand for lightweight materials in the automotive sector has boosted the adoption of PPE compounds.

In the electrical and electronics industry, PPE compounds find use in the manufacturing of connectors, insulators, and circuit boards. The increasing demand for smaller and more efficient electronic devices further fuels the demand for these compounds. In the industrial sector, PPE compounds are used for applications where heat resistance and electrical insulation are crucial, making them suitable for components like pumps, valves, and filters.

Market Growth: The Polyphenylene Ether Compounds market is expected to witness significant growth in the coming years. This growth is attributed to the expanding application areas, increasing technological advancements, and the growing demand for high-performance materials in various industries. As the world continues to focus on energy efficiency and sustainability, PPE compounds are likely to play a vital role, given their recyclability and potential for reducing environmental impact.

Market Industry: The market for Polyphenylene Ether Compounds is highly competitive, with several key players involved in the manufacturing and distribution of these materials. Companies in this industry are constantly innovating to develop new formulations of PPE compounds to meet the evolving needs of end-users across different sectors. Additionally, strategic partnerships and collaborations are common within the industry to expand market reach and diversify product portfolios.

Trends: The polyphenylene ether compounds market trends is witnessing rise in current market scenario. One of the key trends is the increasing use of these compounds in 3D printing and additive manufacturing. This trend is driven by the desire to create complex, customized parts with high-performance characteristics. Furthermore, the development of PPE compounds with enhanced flame-retardant properties is gaining traction, especially in industries where fire safety is paramount.

In conclusion, the Polyphenylene Ether Compounds market continues to grow and diversify due to its remarkable properties and adaptability to various applications. As technology and industrial needs evolve, this market is expected to play a crucial role in shaping the future of high-performance materials and their applications across industries.

#Polyphenylene Ether Compounds Market#Polyphenylene Ether Compounds Market Growth#Polyphenylene Ether Compounds Market Trends

0 notes

Text

Copper-Clad Laminates Market Research Trends 2025: Insights Driving the Future

At Straits Research, published a new research publication on "Copper-Clad Laminates Market Insights, to 2032" and enriched with self-explained Tables and charts in presentable format. In the Consider you will find new evolving Trends, Drivers, Restraints, Opportunities generated by targeting Market associated stakeholders. The development of the Copper-Clad Laminates Market was primarily driven by the expanding R&D investing over the world.

Copper-clad laminates (CCLs) are composite materials made by bonding a thin layer of copper foil to a reinforcing base material, such as epoxy resin, paper, or glass fabric, under heat and pressure. These laminates serve as a fundamental component in the production of printed circuit boards (PCBs), which are essential for electronic devices and systems. CCLs are widely used in industries like consumer electronics, automotive, telecommunications, aerospace, and healthcare due to their excellent electrical conductivity, thermal stability, and mechanical strength.

Request Sample Report at : https://straitsresearch.com/report/copper-clad-laminates-market/request-sample

Some of the key players profiled in the study are:

Kingboard Holdings Ltd

Shengyi Technology (SYTECH)

ITEQ Corporation

Panasonic Corp

Isola Group

Nan Ya Plastics Corp

FINELINE Ltd

Doosan Corporation Electro-Materials (South Korea)

Grace Electron Corp (Wuxi city and Guangzhou city)

Taiwan Elite Material Co. Ltd

Taiwan TAIFLEX Scientific Co. Ltd

UBE Industries Ltd

Goldenmax International Technology Ltd

Guagndong Chaohua Technology Co

The titled segments and sub-section of the market are illuminated below:

By Product

Paper Board

Composite Substrate

FR-4

Halogen-free Board

Others

By Type

Rigid

Flexible

By Application

Computers

Communication Systems

Consumer Appliances

Vehicle Electronics

Healthcare Devices

Defense Technology

By Reinforcement Fiber

Glass Fiber Base

Paper Base

Composite Base

By Resin

Epoxy

Phenolic

Polyimide

Polyester (PET)

Fluoropolymer/PTFE

Polyphenylene Ether (PPE)

Polyphenylene Oxide (PPO)

Others (Polyethylene Naphthalate [PEN], etc.)

By End Use

Automotive

Aerospace & Defense

Consumer Electronics

Healthcare

Industrial

Others

Browse Complete Summary and Table of Content @ https://straitsresearch.com/report/copper-clad-laminates-market/toc

Global Copper-Clad Laminates Market report highlights information regarding the current and future industry trends, growth patterns, as well as it offers business strategies to makes a difference the partners in making sound choices that may offer assistance to guarantee the benefit direction over the forecast years. Key Discoveries Of The Study: By benefit, the overseen administrations fragment is anticipated to witness most elevated development amid the forecast period. Based on Copper-Clad Laminates Market type, the outdoor Copper-Clad Laminates Market segment accounted for highest market share. Depending on enterprise size, the SMEs segment is anticipated to exhibit biggest growth during the forecast period. In terms of industry vertical segment, telecom & IT segment held the biggest share in Copper-Clad Laminates Market in 2019. Region Included are: Global, North America, Europe, APAC, South America, Middle East & Africa, LATAM. Country Level Break-Up: United States, Canada, Mexico, Brazil, Argentina, Colombia, Chile, South Africa, Nigeria, Tunisia, Morocco, Germany, United Kingdom (UK), the Netherlands, Spain, Italy, Belgium, Austria, Turkey, Russia, France, Poland, Israel, United Arab Emirates, Qatar, Saudi Arabia, China, Japan, Taiwan, South Korea, Singapore, India, Australia and New Zealand etc. At long last, Copper-Clad Laminates Market is a important source of direction for people and companies.

Buy Now & Get Exclusive Report at : https://straitsresearch.com/buy-now/copper-clad-laminates-market

Thanks for reading this article you can also get region wise report version like Global, North America, Europe, APAC, South America, Middle East & Africa, LAMEA) and Forecasts, 2024-2032

About Straits Research

Straits Research is dedicated to providing businesses with the highest quality market research services. With a team of experienced researchers and analysts, we strive to deliver insightful and actionable data that helps our clients make informed decisions about their industry and market. Our customized approach allows us to tailor our research to each client's specific needs and goals, ensuring that they receive the most relevant and valuable insights.

Contact Us

Email: [email protected]

Tel: UK: +44 203 695 0070, USA: +1 646 905 0080

#Copper-Clad Laminates Market Market#Copper-Clad Laminates Market Market Share#Copper-Clad Laminates Market Market Size#Copper-Clad Laminates Market Market Research#Copper-Clad Laminates Market Industry#What is Copper-Clad Laminates Market?

0 notes

Link

0 notes

Text

0 notes

Text

Global Heat Resistant Polymer Market: Growth Drivers and Competitive Landscape

The global heat resistant polymer market size was valued at USD 17.9 billion in 2023 and is anticipated to grow at a CAGR of 9.9% from 2024 to 2030. This growth is driven by the increasing demand from the electronics and electrical industries, where these polymers are essential for manufacturing components that can withstand high temperatures. The shift of the automotive sector towards lightweight and fuel-efficient vehicles has spurred the use of heat-resistant polymers in engine components and under-the-hood applications.

The aerospace industry relies heavily on these materials for their durability and performance in extreme conditions. The advancements in polymer technology and the rising trend of miniaturization in various sectors are propelling market growth. Regulations play a significant role in shaping the global heat resistant polymer market. Stringent environmental policies, such as the European Union’s REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation, mandate using safer and more sustainable materials, driving the demand for eco-friendly heat resistant polymers.

In addition, fire safety standards, such as the U.S. UL 94 flammability rating, require materials to meet specific flame retardancy criteria, influencing the development and adoption of flame-retardant polymers. In the automotive sector, regulations to reduce vehicle emissions and improve fuel efficiency, such as the Corporate Average Fuel Economy (CAFE) standards in the U.S., encourage using lightweight, high-performance polymers. These regulatory frameworks ensure safety and environmental compliance and stimulate innovation and growth within the heat resistant polymer market.

Heat Resistant Polymer Market Report Highlights

The fluoropolymers segment accounted for 31.9% of the market revenue in 2023, attributed to their exceptional heat and chemical resistance. This makes them valuable in demanding industrial applications, especially in the automotive and aerospace sectors.

The automotive segment dominated the market in 2023. Heat resistant polymers are extensively used in various automotive applications, including under-the-hood components such as engine covers, air intake manifolds, and radiator end tanks.

The aerospace and defense segment is expected to grow at the fastest CAGR over the forecast period from 2024 to 2030 driven by the aerospace industry’s stringent requirements for materials that can perform reliably under extreme conditions, including high temperatures, pressure, and exposure to aggressive chemicals.

The UK heat resistant polymer market is experiencing steady growth, driven by the country’s focus on innovation and high-performance materials.

Global Heat Resistant Polymer Market Segmentation

This report forecasts revenue & volume growth of the Heat Resistant Polymer market and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global agrochemicals market report based on application, end use and region:

Product Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

Fluoropolymer

Polyphenylene Sulfide

Polyimides

Polybenzimidazole

Polyether Ether Ketone

Others

End Use Outlook (Volume, Kilo Tons; Revenue, USD Million, 2018 - 2030)

Transportation

Electronics & Electrical

Others

Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Russia

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Thailand

South Korea

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Order a free sample PDF of the Heat Resistant Polymer Market Intelligence Study, published by Grand View Research.

0 notes

Text

Carbon Fiber Reinforced Plastic Market - Forecast(2024 - 2030)

Carbon Fiber Reinforced Plastic Market Overview:

Carbon fiber reinforced plastic market size is forecast to reach $30.5 billion by 2030, after growing at a CAGR of 9.41% during 2024-2030, owing to the increasing adoption of carbon fiber reinforced plastics over conventional metallic alloys in various end-use industries such as automotive, aerospace, wind energy, and others. This is mainly due to the tensile strength carried by CFRP, which falls between 1500 and 3500 MPa, whereas its metallic counterparts such as aluminum and steel only possess tensile strength of 450–600 MPa and 750–1500 MPa, respectively. Growing demand from the aerospace industry and a rising preference for fuel-efficient and lightweight vehicles are the major factors driving the carbon fiber reinforced plastic (CFRP) market during the forecast period

Report Coverage

The report: “Carbon Fiber Reinforced Plastic (CFRP) Market – Forecast (2020-2025)”, by IndustryARC, covers an in-depth analysis of the following segments of the carbon fiber reinforced plastic (CFRP) Industry.

By Type: Thermoplastic (Polyether Ether Ketone (PEEK), Polypropylene, Nylon, Acrylic Resins, Polyamide Resins, PET, Polyphenylene Sulfide (PPS), Polyethylene, Polyurethane, Polyethersulfone, Polyetherimide (PEI), and Others), and Thermosetting (Epoxy Resin, Polyester Resin, Vinyl Ester Resin, Phenolic, Polyimide Resins, and Others)

By Application: Automobiles, Industrial, Aviation & Aerospace, Marine, Defense, Electrical & Electronics, Medical, Sports Equipment, Wind Energy, Civil Engineering, and Others

By Geography: Americas, Europe, Asia Pacific, RoW

Request Sample

Key Takeaways

Europe dominates the carbon fiber reinforced plastic (CFRP) market, owing to the increasing demand and production of lightweight vehicles in the region. According to OICA, in 2018 the production of light commercial vehicles has increased by 2.5 % in Europe.

The carbon fiber reinforced plastics are being widely used to manufacture sport equipment such as golf shafts, bicycles, skis, surfboards, helmets, racquets, hockey sticks, baseball bats and several other products. Its low maintenance cost and corrosion resistance properties are the major factor driving the market in the sports sector.

The properties associated with CFRP such as good conductivity, flame resistance, high strength and vibration damping has facilitated their inclusion in several electrical and electronic products such as household appliances, audio systems, enclosures, electrical installations, interconnects, brushes and EMI shielding.

The X-Ray permeability, biological inertness coupled with high strength has paved the way for CFRP applications in Medical sector. Imaging equipment, orthopedics and surgical outfits are some of the common medical devices that employ CFRP.

Due to the COVID-19 Pandemic most of the countries has gone under lockdown, due to which operations of various industries such as automotive, defense, and aerospace has been negatively affected, which is hampering the carbon fiber reinforced plastic (CFRP) market growth.

By Type – Segment Analysis

The thermosetting segment held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019, owing to the superior characteristics of thermosetting CFRP over thermoplastic CFRP. Unlike thermoplastics, they retain their strength and shape even when heated. This makes thermosetting plastics well-suited to the production of permanent components and large, solid shapes. Furthermore, these components have outstanding high strength-to-weight ratio performance, enhanced dielectric strength, low thermal conductivity. Thus, thermoset CFRP find their use in varied applications owing to their heat resistant characteristics, excellent dimensional and chemical stability properties when exposed to high heat and more.

Inquiry Before Buying

By Application – Segment Analysis

The defense application held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019 and is growing at a CAGR of 9.42%, owing to its ability to reduce a weight of an object to a large extent while providing superior strength. Thus, there is an increasing demand of carbon fiber reinforced plastics from the defense industries to manufacture specialty components for missile systems, radar panels, body armors, helmets, rocket motor casing, artificial limbs, ballistics, nuclear submarine, propulsion systems and many more. Some of the materials used in military composites include Kevlar, fiberglass and carbon fiber. Countries like Russia, India and Japan are increasingly using composites in submarines, jets, sonar domes and truck components. U.S., U.K., India, and China are the major spenders on defense equipment and maintenance of army. M80 Stileto is the largest U.S. naval vessel built using carbon-fiber composites. Armored vehicles have conventionally used steel armor for protection; however, weight of these large trucks creates logistical problems. Therefore, the adoption of CFRP is increasing in these vehicles. U.S. DOD aims to replace UH-60 Black Hawk with Bell Helicopter’s V-280 which incorporates carbon fibers in its wings, fuselage, and tail. The need for agility at the time of sudden attacks and upgrading the defense technologies has led to the shift from conventional materials to fiber reinforced materials, which is anticipated to propel the carbon fiber reinforced plastic market during the forecast period.

By Geography – Segment Analysis

Europe region held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019 up to 34%, owing to the increasing defense, and aerospace sectors in the region. The CFRP are particularly attractive to defense applications because of their exceptional strength, better stiffness-to-density ratios and superior physical properties. Also, CFRP provides relatively stronger and stiffer fibers in a tough resin matrix. According to International Trade Administration (ITA), the Norwegian Government presented a core defense spending budget of USD 6.9 billion in 2019. The Norwegian defense budget accounted for 1.62% of Norway’s GDP in 2018. French civil aerospace industry in 2018 grew to €50.36 billion, out of total non-consolidated aerospace and defense aerospace revenues of €65.4 billion. This is a 1.2% increase over 2017. Also, France has put forth an agreement with the U.K government of $2.1 billion to build a prototype combat drone, which will further boost CFRP market growth. Thus, the increasing aerospace and defense industry in Europe is likely to influence the growth of the carbon fiber reinforced plastic market in Europe.

Drivers – Carbon Fiber Reinforced Plastic (CFRP) Market

Growing Wind Power Sector

As a consequence of drastic increase in energy demand, the conventional sources of energy are depleting very fast. Hence, the need to expand and utilize the renewable energy sources like wind power is growing. The wind power sector is increasing, as use of renewable energy sources results in less emission of greenhouse and other harmful gases such as SO2. The modern wind turbine are being increasingly used in wind power sector as they are cost-effective, more reliable and have scaled up in size to multi-megawatt power ratings. Wind Energy installations in APAC increased by 23.6%. This region is set to witness high growth for wind energy equipment and materials majorly driven by commitments of government of India and China towards green energy. Carbon fiber reinforced plastic is used primarily in the spar, or structural element, of wind blades longer than 45m/148 ft, both for land-based and offshore systems. Carbon fiber has known benefits for reducing wind turbine blade mass due to the significantly improved stiffness, strength, and fatigue resistance per unit mass compared to fiberglass. Due to the increasing adoption of wind power energy source, the demand for the carbon fiber reinforced plastic is also increasing, which acts as a driver for the carbon fiber reinforced plastic market during the forecast period.

Schedule a Call

Stringent Government Regulation on Emission

Carbon fiber reinforced plastics are being extensively used in the automotive industries to reduce fuel consumption as well as emissions and to manufacture lightweight vehicles. Several governments across the world have imposed stringent standard emission and fuel economy regulations for vehicles. These standard regulations have compelled automotive OEMs to increase the use of lightweight materials such as carbon fiber reinforced plastics to assist in increasing the fuel economy of a vehicle while ensuring safety and performance. The emission regulation for light-duty cars such as Corporate Average Fuel Economy (CAFÉ) and Greenhouse Gas Emission standards sets fuel consumption standards for the vehicles. These regulations by the governments have made sure that the car manufacture henceforth might need to be manufacturing much lighter vehicles to obey as per these norms, which acts as a driver for the carbon fiber reinforced plastic market during the forecast period.

Challenges – Carbon Fiber Reinforced Plastic (CFRP) Market

High Cost of Carbon Fiber Reinforced Plastics

The cost of the carbon fiber reinforced plastics is at times supposedly higher. When compared with other traditional materials such as steel and aluminum, lightweight materials such as carbon fiber reinforced plastics (CFRP) and glass fiber reinforced plastics (GFRP) are costly. Composites of carbon fiber cost almost 1.5 to five times more than steel. High cost of fiber production inhibits large volume deployment. Therefore, precursor and processing costs need to be reduced. The high price of carbon fibers in many applications constrains the potential use of composites. Hence, the high cost of carbon fiber reinforced plastics may hinder with the carbon fiber reinforced plastics market growth during the forecast period. However, cost effective production methods coupled with high volume processing, assembly techniques and automation processes will lead to reduction of price in the near future.

Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the carbon fiber reinforced plastic (CFRP) market. In 2019, the market of carbon fiber reinforced plastic (CFRP) has been consolidated by the top five players accounting for 40% of the share. Major players in the carbon fiber reinforced plastic (CFRP) market are SGL Carbon SE, Teijin Ltd., Toray Industries Inc., Cytec Industries Inc., Mitsubishi Rayon Co. Ltd., Farmosa Plastics Corporation, Nippon Carbon Co. Ltd., DowAksa Advanced Composites Holdings BV, Hexcel Corporation, and Hyosung Advanced Materials.

Buy Now

Acquisitions/Technology Launches

In May 2016, Dowaska, Under secretariat of Defense Industries (SSM) and Turkish Aerospace Industries (TAI) have jointly opened The DowAksa Global Composites Center with an objective to advance Turkey’s carbon fiber and other reinforcement composites manufacturing mainly for aerospace applications in both defense and commercial aviation and the infrastructure, marine, wind energy and transportation sector.

In March 2018, Toray Industries, Inc. developed a new fabrication technology for Carbon Fiber Reinforced Plastics that enables both improved dimensional accuracy and energy savings.

In November 2018, Toray Industries, Inc. developed new carbon fibers that realized both higher tensile strength and tensile modulus named “TORAYCA® MX series”.

In September 2019, Teijin Limited acquired Benet Automotive, a leading automotive composite and component supplier in the Czech Republic. The acquisition benefits Teijin’s composite technologies business.

In December 2019, SGL Carbon and Solvay entered into a joint development agreement to develop composite materials based on large-tow intermediate modulus carbon fiber for aerospace primary structures.

In May 2020, Toray Industries, Inc. developed a high tensile modulus carbon fiber and thermoplastic pellets that are ideal for injection molding employing. Toray announced to push ahead with research and development to commercialize the fiber and pellets within the next three years.

#Carbon Fiber Reinforced Plastic Market#Carbon Fiber Reinforced Plastic Market Share#Carbon Fiber Reinforced Plastic Market Size#Carbon Fiber Reinforced Plastic Market Forecast#Carbon Fiber Reinforced Plastic Market Report#Carbon Fiber Reinforced Plastic Market Growth

0 notes

Text

4, 4-Dichlorodiphenyl Sulfone (DCDPS) Market huge Growth in future scope 2024-2030 | GQ Research

The 4, 4-Dichlorodiphenyl Sulfone (DCDPS) market is set to witness remarkable growth, as indicated by recent market analysis conducted by GQ Research. In 2023, the global 4, 4-Dichlorodiphenyl Sulfone (DCDPS) market showcased a significant presence, boasting a valuation of US$ 3.91 Billion. This underscores the substantial demand for 4, 4-Dichlorodiphenyl Sulfone (DCDPS) technology and its widespread adoption across various industries.

Get Sample of this Report at: https://gqresearch.com/request-sample/global-44-dichlorodiphenyl-sulfone-dcdps-market/

Projected Growth: Projections suggest that the 4, 4-Dichlorodiphenyl Sulfone (DCDPS) market will continue its upward trajectory, with a projected value of US$ 5.64 Billion by 2030. This growth is expected to be driven by technological advancements, increasing consumer demand, and expanding application areas.

Compound Annual Growth Rate (CAGR): The forecast period anticipates a Compound Annual Growth Rate (CAGR) of 7%, reflecting a steady and robust growth rate for the 4, 4-Dichlorodiphenyl Sulfone (DCDPS) market over the coming years.

Technology Adoption:

The adoption of 4, 4-Dichlorodiphenyl Sulfone (DCDPS) has seen significant growth across various industries due to its versatile properties. Initially developed for its exceptional thermal and chemical resistance, DCDPS has found applications in diverse sectors such as electronics, aerospace, automotive, and healthcare. Its ability to withstand high temperatures and harsh environments makes it indispensable for manufacturing electronic components, composite materials, medical devices, and specialized coatings.

Consumer Preferences:

Consumer preferences for products incorporating DCDPS are influenced by several factors. Firstly, there's a growing demand for durable and high-performance materials, especially in electronics and automotive sectors, where reliability is paramount. Additionally, consumers increasingly prioritize sustainability and eco-friendliness, favoring products that utilize environmentally responsible materials in their production processes. As DCDPS is non-toxic and resistant to degradation, it aligns with these preferences, driving its adoption in consumer goods.

Technological Advancements:

Technological advancements continue to expand the scope of applications for DCDPS. Innovations in manufacturing processes have enabled the production of DCDPS-based materials with enhanced properties, such as improved strength, flexibility, and conductivity. Furthermore, research into nanotechnology has led to the development of nanostructured DCDPS materials, offering unique functionalities like self-healing and antimicrobial properties. These advancements open up new opportunities for DCDPS across industries and drive further innovation in its utilization.

Market Competition:

The market for DCDPS faces competition from alternative materials with similar properties, such as polyether ether ketone (PEEK) and polyphenylene sulfide (PPS). These materials offer comparable performance characteristics and may be preferred in certain applications due to factors like cost-effectiveness or ease of processing. Additionally, ongoing research into novel materials poses a competitive challenge to DCDPS, as emerging alternatives may offer superior performance or environmental benefits. To maintain its market position, DCDPS manufacturers must focus on innovation, cost-efficiency, and sustainability to meet evolving customer demands.

Environmental Considerations:

Environmental considerations play a crucial role in the DCDPS market, particularly regarding its production and end-of-life disposal. While DCDPS itself is non-toxic and inert, its manufacturing process may involve the use of solvents and reagents that pose environmental risks if not managed properly. Manufacturers are thus under pressure to adopt cleaner production methods and minimize waste generation to reduce their environmental footprint. Additionally, efforts to improve recyclability and biodegradability of DCDPS-based products are underway to address concerns regarding their long-term environmental impact. By embracing sustainable practices throughout the product lifecycle, the DCDPS industry can mitigate its environmental footprint and contribute to a more sustainable future.

Regional Dynamics: Different regions may exhibit varying growth rates and adoption patterns influenced by factors such as consumer preferences, technological infrastructure and regulatory frameworks.

Key players in the industry include:

Solvay SA

Mitsubishi Gas Chemical Company, Inc.

Sigma-Aldrich Corporation (now part of Merck KGaA)

Shandong Luba Chemical Co., Ltd.

Shandong Tianxin Chemical Co., Ltd.

Shangyu Jiehua Chemical Co., Ltd.

Tokyo Chemical Industry Co., Ltd.

Changzhou Koye Chemical Co., Ltd.

Changzhou Shanfeng Chemical Industry Co., Ltd.

Hubei Xinyuan Chemical Industry Co., Ltd.

Hunan Honglian Chemical Industry Co., Ltd.

The research report provides a comprehensive analysis of the 4, 4-Dichlorodiphenyl Sulfone (DCDPS) market, offering insights into current trends, market dynamics and future prospects. It explores key factors driving growth, challenges faced by the industry, and potential opportunities for market players.

For more information and to access a complimentary sample report, visit Link to Sample Report: https://gqresearch.com/request-sample/global-44-dichlorodiphenyl-sulfone-dcdps-market/

About GQ Research:

GQ Research is a company that is creating cutting edge, futuristic and informative reports in many different areas. Some of the most common areas where we generate reports are industry reports, country reports, company reports and everything in between.

Contact:

Jessica Joyal

+1 (614) 602 2897 | +919284395731

Website - https://gqresearch.com/

0 notes

Text

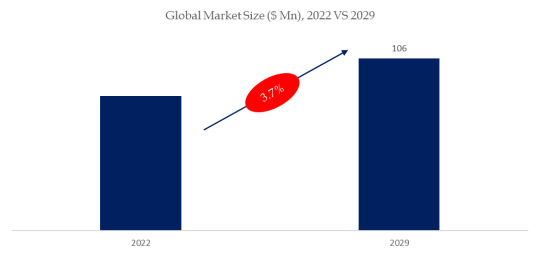

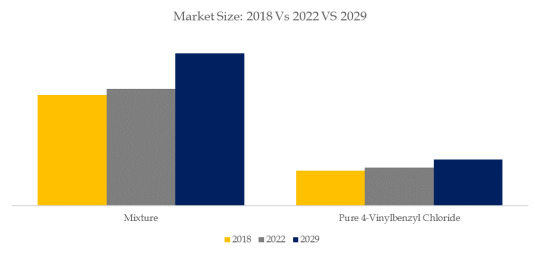

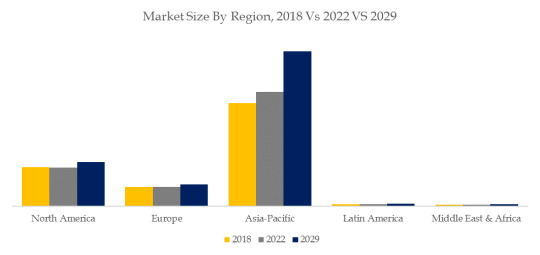

4-Vinylbenzyl Chloride, Global Market Size Forecast, Top 3 Players Rank and Market Share

4-Vinylbenzyl Chloride Market Summary

4-Vinylbenzyl Chloride is a colorless liquid that is typically stored with a stabilizer to suppress polymerization. In combination with styrene, vinylbenzyl chloride can be used as a comonomer in the production of chloromethylated polystyrene.

According to the new market research report “Global 4-Vinylbenzyl Chloride Market Report 2023-2029”, published by QYResearch, the global 4-Vinylbenzyl Chloride market size is projected to reach USD 106.1 million by 2029, at a CAGR of 3.7% during the forecast period.

Figure. Global 4-Vinylbenzyl Chloride Market Size (US$ Million), 2022-2029

Based on or includes research from QYResearch: Global 4-Vinylbenzyl Chloride Market Report 2023-2029.

Market Drivers:

Demand from anion ion exchange membrane market keep growing.

Hyperbranched polymers are used as polymeric additives in many linear commercial polymers as compatibilising agents, process and strength improvers. In recent years, the growing interest in Polyphenylene ether graft monomer has brought more attention to VBC.

Restraint:

4-Vinylbenzyl Chloride is produced through a batch reaction, and the production process is complicated, which means that it is difficult to supply this product in large quantities.

The transportation and storage of 4-Vinylbenzyl Chloride requires a low-temperature environment, which poses challenges to downstream enterprise applications.

Opportunity:

4-Vinylbenzyl Chloride is a niche market with limited suppliers. The demand mainly comes high molecular modifiers such as rubber and resin, photographic materials, coupling agents, and various other treatment agents. The market of 4-Vinylbenzyl Chloride would keep stable in the coming years.

4-Vinylbenzyl Chloride is a highly responsive monomer having vinyl and chloromethyl groups in molecules. Possibility of a new 4-Vinylbenzyl Chloride derivative is infinitely expanding in various fields.

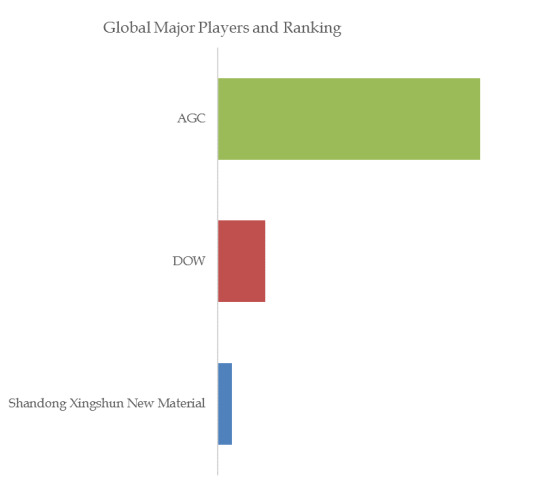

Figure. 4-Vinylbenzyl Chloride, Global Market Size, The Top 3 Players Hold 95% of Overall Market

Based on or includes research from QYResearch: Global 4-Vinylbenzyl Chloride Market Report 2023-2029.

This report profiles key players of 4-Vinylbenzyl Chloride such as AGC, DOW, Shandong Xingshun New Material. In 2022, the global top 3 4-Vinylbenzyl Chloride players account for 95% of market share in terms of revenue. Above figure shows the key players ranked by revenue in 4-Vinylbenzyl Chloride.

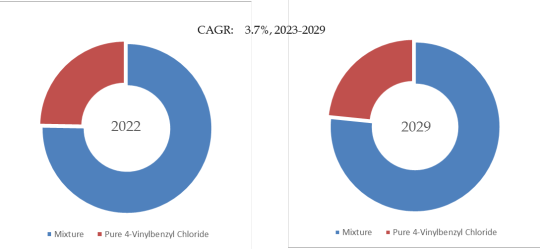

Figure. 4-Vinylbenzyl Chloride, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global 4-Vinylbenzyl Chloride Market Report 2023-2029.

In terms of product type, Mixture is the largest segment, hold a share of 75.3%.

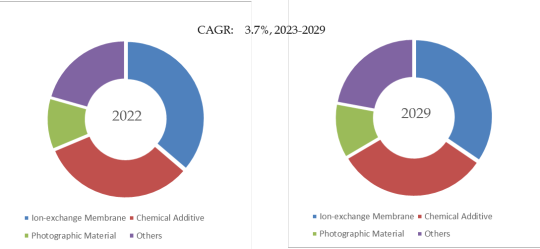

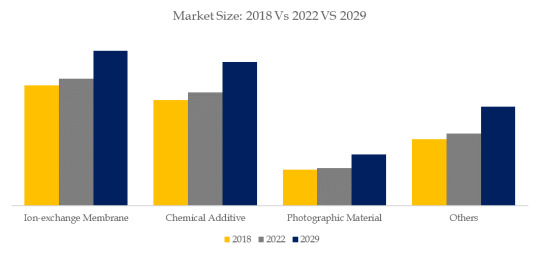

Figure. 4-Vinylbenzyl Chloride, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global 4-Vinylbenzyl Chloride Market Report 2023-2029.

In terms of product application, Ion-exchange Membrane is the largest application, hold a share of 36.2%.

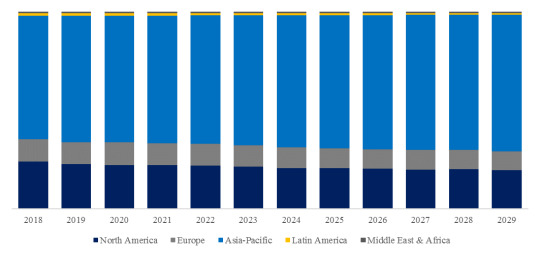

Figure. 4-Vinylbenzyl Chloride, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global 4-Vinylbenzyl Chloride Market Report 2023-2029.

About The Authors

Lu Jing - Lead Author

Email: [email protected]

Lu Jing is a technology & market senior analyst specializing in chemical, advanced material, and component. Lu has 9 years’ experience in chemical and focuses on catalyst and additive, metal and plastic materials, waste recycling, daily chemicals. She is engaged in the development of technology and market reports and is also involved in custom projects.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

0 notes

Text

Masterbatch Prices, Price, Pricing, Trend and Forecast | ChemAnalyst

Masterbatch prices play a crucial role in various industries, especially in the manufacturing sector where colorants and additives are essential for achieving desired product specifications. Understanding the factors influencing masterbatch prices is vital for businesses aiming to optimize their budget and production processes effectively.

One significant determinant of masterbatch prices is the type of polymer used as the carrier resin. Different polymers have distinct characteristics and costs associated with their production. For instance, masterbatches based on high-performance engineering polymers like polyether ether ketone (PEEK) or polyphenylene sulfide (PPS) tend to be more expensive compared to those using commodity plastics such as polyethylene (PE) or polypropylene (PP). The choice of polymer not only affects the material cost but also impacts the processing requirements and final product performance, thus influencing the overall pricing.

Another critical factor influencing masterbatch prices is the quality and concentration of pigments, additives, or fillers incorporated into the masterbatch formulation. High-quality pigments or specialized additives designed for specific applications often command a premium price. Additionally, the concentration of these components can vary depending on the desired color intensity, functional properties, or regulatory compliance requirements. Masterbatches with higher pigment loadings or complex formulations may incur higher production costs, resulting in elevated prices.

Get Real Time Prices of Masterbatch: https://www.chemanalyst.com/Pricing-data/masterbatch-1117

Market dynamics and supply chain factors also play a significant role in determining masterbatch prices. Fluctuations in raw material prices, currency exchange rates, and energy costs can directly impact the overall production expenses for masterbatch manufacturers. Furthermore, availability and demand-supply dynamics of raw materials, particularly specialty chemicals used in masterbatch formulations, can influence pricing trends. Economic conditions, geopolitical factors, and trade policies may also contribute to price volatility within the masterbatch industry.

The level of customization and technical support offered by masterbatch suppliers can affect pricing structures. Customized masterbatch solutions tailored to meet specific customer requirements often involve additional R&D efforts, formulation adjustments, and technical support services, which may result in higher prices compared to standard off-the-shelf products. However, these tailored solutions can provide significant value by optimizing processing efficiency, enhancing product performance, and ensuring regulatory compliance.

Geographical factors such as regional market dynamics, transportation costs, and regulatory requirements can also impact masterbatch prices. Localized production facilities or sourcing strategies may offer cost advantages in certain regions, while transportation expenses and trade barriers can add to the overall cost structure. Moreover, varying regulatory standards for product safety, environmental compliance, and labeling requirements across different jurisdictions can influence the selection of raw materials and manufacturing processes, consequently affecting pricing considerations.

Innovation and technological advancements in masterbatch manufacturing techniques can influence pricing dynamics. Continuous improvement in processing technologies, equipment efficiency, and formulation techniques may lead to cost savings in production, which can be reflected in competitive pricing strategies. Additionally, the introduction of novel additives, colorants, or functional masterbatch solutions with enhanced performance attributes may justify premium pricing based on the value proposition they offer to customers.

Competition within the masterbatch industry also exerts pressure on pricing strategies. The presence of multiple suppliers competing for market share can lead to price competition, especially in commoditized segments. Price differentiation strategies based on product quality, technical expertise, service offerings, or brand reputation can help suppliers maintain profitability amidst competitive pressures. However, pricing decisions must balance the need for profitability with market demand dynamics and customer expectations to ensure long-term sustainability.

In conclusion, masterbatch prices are influenced by a complex interplay of factors including raw material costs, formulation complexity, market dynamics, customization requirements, geographical considerations, technological innovations, and competitive forces. Businesses must carefully evaluate these factors and collaborate closely with trusted suppliers to optimize their masterbatch procurement strategies and achieve cost-effective solutions without compromising on quality or performance.

Get Real Time Prices of Masterbatch: https://www.chemanalyst.com/Pricing-data/masterbatch-1117

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

0 notes

Text

Polyphenylene Ether Compounds Market Dynamics: Emerging Applications and Future Prospects

The Polyphenylene Ether Compounds market is a dynamic and evolving sector within the chemical industry. Polyphenylene Ether Compounds, also known as PPE compounds, are a group of high-performance thermoplastic materials with a wide range of applications. These compounds are known for their exceptional thermal and electrical properties, making them suitable for various industries. This article provides a comprehensive overview of the Polyphenylene Ether Compounds market, including its definition, market growth, industry trends, and more.

Definition

Polyphenylene Ether Compounds, often abbreviated as PPE compounds, are a class of engineering thermoplastics characterized by their high-temperature resistance, dimensional stability, and excellent electrical insulating properties. They are typically composed of polyphenylene ether resin blended with other materials, such as polystyrene, to enhance specific properties like impact resistance or flame retardancy. PPE compounds find applications in diverse industries, including automotive, electronics, aerospace, and consumer goods.

Market Overview

The Polyphenylene Ether Compounds market has witnessed steady growth in recent years, driven by the increasing demand for high-performance plastics in various end-use industries. Factors such as the need for lightweight and durable materials in automotive manufacturing, the growth of the electronics sector, and a focus on sustainable materials have contributed to the market's expansion. Additionally, the versatility of PPE compounds and their ability to replace traditional materials like metals and ceramics in certain applications have further fueled market growth.

Market Growth

The market for Polyphenylene Ether Compounds has experienced robust growth, with a substantial increase in both production and consumption. This growth is attributed to the material's unique properties, which cater to the evolving needs of modern industries. As industries seek to improve efficiency, reduce energy consumption, and meet stringent regulatory requirements, the demand for PPE compounds continues to rise. Moreover, the ongoing research and development efforts in the field of polymer science have led to the development of new formulations and grades of PPE compounds, expanding their applicability.

Market Industry Trends

Several key polyphenylene ether compounds market industry & trends are shaping the Polyphenylene Ether Compounds market. One prominent trend is the growing focus on sustainability. Manufacturers and end-users are increasingly adopting PPE compounds due to their recyclability and potential to reduce carbon emissions compared to traditional materials. Furthermore, the demand for flame-retardant PPE compounds is on the rise, particularly in the electronics and electrical sectors, as safety and regulatory compliance become paramount.

Another notable trend is the customization of PPE compounds to meet specific industry requirements. Manufacturers are offering tailored formulations with enhanced properties, such as improved heat resistance or greater chemical resistance, to address the diverse needs of different applications. This customization is fostering innovation and driving the adoption of PPE compounds across various industries.

In conclusion, the Polyphenylene Ether Compounds market is experiencing substantial growth due to its unique properties, versatility, and alignment with industry trends. As industries continue to seek advanced materials that offer superior performance and sustainability, PPE compounds are poised to play a significant role in shaping the future of the global polymer industry.

#Polyphenylene Ether Compounds Market#Polyphenylene Ether Compounds Market Growth#Polyphenylene Ether Compounds Market Trends

0 notes

Text

Polyether Ether Ketone Market is estimated to Witness Strong Growth Owing to Increasing Demand from Aerospace and Automotive Industries

Polyether ether ketone (PEEK) is a semi-crystalline thermoplastic polymer belonging to the polyaryletherketone (PAEK) family. It has excellent mechanical properties such as high tensile strength, impact resistance, and strong chemical resistance. PEEK is widely used in aerospace, electronics, medical, automotive and other industrial applications. In the aerospace industry, PEEK finds application in components for both commercial and military aircraft due to its lightweight as well as heat and chemical resistant properties. PEEK polymers offer greater durability and strength than metals, allowing them to replace heavier metallic components and reduce aircraft weight. The global Polyether Ether Ketone Market is estimated to be valued at US$ 840.2 Bn in 2024 and is expected to exhibit a CAGR of 8.5% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights. Market Dynamics: One of the major drivers for the growth of the global Polyether Ether Ketone market size is increasing demand from the aerospace and automotive industries. PEEK offers properties like heat and chemical resistance, strength and durability which makes it an ideal material for components in aircraft and electric/hybrid vehicles. PEEK components are increasingly replacing metals in aircraft brake lines, engine cowlings and undercarriage components as they are lightweight and corrosion-resistant. In automotive, PEEK find applications in fuel cell components, connectors, seals and bearings due to its toughness and strength. This is expected to significantly drive the demand for PEEK over the forecast period. Additionally, excellent corrosion and chemical resistance properties of PEEK also drive its adoption in industrial applications in chemical processing equipment, semiconductor fabrication and electrical components. However, high material and manufacturing costs associated with PEEK limit its adoption in mass applications. Continuous research & development activities focused on reducing costs through novel manufacturing processes can help overcome this challenge and further contribute to the market growth. SWOT Analysis Strength: Polyether ether ketone (PEEK) is known for its high strength, durability, and corrosion resistance compared to metals. It can withstand high temperatures up to 260°C without suffering deformation. PEEK also has good mechanical strength and offers machining versatility. Ease of molding and shaping makes PEEK suitable for a wide range of applications. Weakness: PEEK resin is more expensive than other engineering thermoplastics such as nylon and polycarbonate. PEEK is difficult to color and susceptible to stress cracking. Processing PEEK also requires investments in specialized manufacturing equipment. Opportunity: Growing demand from the aerospace and defense, medical, automotive, and electrical industries is expected to boost the PEEK market. PEEK's biocompatibility makes it suitable for medical implants. Use of PEEK in 3D printing offers new opportunities. Increasing R&D for developing novel grades of PEEK with enhanced properties will expand the material's applications. Threats: Availability of cheaper substitutes such as liquid crystal polymers and polyphenylene sulfide can replace PEEK in some non-critical applications. Macroeconomic uncertainties and supply chain disruptions affect the businesses of end-use industries adopting PEEK. Key Takeaways The global Polyether ether ketone market is expected to witness high growth over the forecast period of 2024 to 2031. The global Polyether Ether Ketone Market is estimated to be valued at US$ 840.2 Bn in 2024 and is expected to exhibit a CAGR of 8.5% over the forecast period 2024 to 2031.

The Asia Pacific region currently dominates the PEEK market and is anticipated to grow at a faster pace due to rapid industrialization and the growing manufacturing industry in China, India, Japan and other Southeast Asian countries. Key players operating in the Polyether ether ketone market include Victrex plc, Solvay S.A., Evonik Industries AG, Panjin Zhongrun High Performance Polymers Co. Ltd., Zyex Ltd., Quadrant EPP S.A., Prototype & Plastic Mold Company Inc., Jida Evatane, Stern Companies, Caledonian Ferguson Timpson Ltd., Darter Plastics Inc., J K Overseas, Prodas, and others. Get more insights on this topic:https://www.newswirestats.com/polyether-ether-ketone-market-size-and-outlook/

#Polyether Ether Ketone#Polyether Ether Ketone Market#Polyether Ether Ketone Market size#Polyether Ether Ketone Market share#Coherent Market Insights

0 notes

Text

Carbon Fiber Reinforced Plastic Market - Forecast (2023 - 2028)

Carbon fiber reinforced plastic market size is forecast to reach $22.50 billion by 2025, after growing at a CAGR of 9.41% during 2020-2025, owing to the increasing adoption of carbon fiber reinforced plastics over conventional metallic alloys in various end use industries such as automotive, aerospace, wind energy, and others. This is mainly due to tensile strength carried by CFRP, which falls between 1500 and 3500 MPa, whereas its metallic counterparts such as aluminum and steel only possess tensile strength of 450–600 MPa and 750–1500 MPa, respectively. Growing demand from the aerospace industry and a rising preference for fuel efficient and light-weight vehicles are the major factors driving the carbon fiber reinforced plastic (CFRP) market during the forecast period.

Report Coverage

The report: “Carbon Fiber Reinforced Plastic (CFRP) Market – Forecast (2020-2025)”, by IndustryARC, covers an in-depth analysis of the following segments of the carbon fiber reinforced plastic (CFRP) Industry.

By Type: Thermoplastic (Polyether Ether Ketone (PEEK), Polypropylene, Nylon, Acrylic Resins, Polyamide Resins, PET, Polyphenylene Sulfide (PPS), Polyethylene, Polyurethane, Polyethersulfone, Polyetherimide (PEI), and Others), and Thermosetting (Epoxy Resin, Polyester Resin, Vinyl Ester Resin, Phenolic, Polyimide Resins, and Others)

By Application: Automobiles, Industrial, Aviation & Aerospace, Marine, Defense, Electrical & Electronics, Medical, Sports Equipment, Wind Energy, Civil Engineering, and Others

By Geography: Americas, Europe, Asia Pacific, RoW

Key Takeaways

Europe dominates the carbon fiber reinforced plastic (CFRP) market, owing to the increasing demand and production of lightweight vehicles in the region. According to OICA, in 2018 the production of light commercial vehicles has increased by 2.5 % in Europe.

The carbon fiber reinforced plastics are being widely used to manufacture sport equipment such as golf shafts, bicycles, skis, surfboards, helmets, racquets, hockey sticks, baseball bats and several other products. Its low maintenance cost and corrosion resistance properties are the major factor driving the market in the sports sector.

The properties associated with CFRP such as good conductivity, flame resistance, high strength and vibration damping has facilitated their inclusion in several electrical and electronic products such as household appliances, audio systems, enclosures, electrical installations, interconnects, brushes and EMI shielding.

The X-Ray permeability, biological inertness coupled with high strength has paved the way for CFRP applications in Medical sector. Imaging equipment, orthopedics and surgical outfits are some of the common medical devices that employ CFRP.

Due to the COVID-19 Pandemic most of the countries has gone under lockdown, due to which operations of various industries such as automotive, defense, and aerospace has been negatively affected, which is hampering the carbon fiber reinforced plastic (CFRP) market growth.

By Type – Segment Analysis

The thermosetting segment held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019, owing to the superior characteristics of thermosetting CFRP over thermoplastic CFRP. Unlike thermoplastics, they retain their strength and shape even when heated. This makes thermosetting plastics well-suited to the production of permanent components and large, solid shapes. Furthermore, these components have outstanding high strength-to-weight ratio performance, enhanced dielectric strength, low thermal conductivity. Thus, thermoset CFRP find their use in varied applications owing to their heat resistant characteristics, excellent dimensional and chemical stability properties when exposed to high heat and more.

By Application – Segment Analysis

The defense application held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019 and is growing at a CAGR of 9.42%, owing to its ability to reduce a weight of an object to a large extent while providing superior strength. Thus, there is an increasing demand of carbon fiber reinforced plastics from the defense industries to manufacture specialty components for missile systems, radar panels, body armors, helmets, rocket motor casing, artificial limbs, ballistics, nuclear submarine, propulsion systems and many more. Some of the materials used in military composites include Kevlar, fiberglass and carbon fiber. Countries like Russia, India and Japan are increasingly using composites in submarines, jets, sonar domes and truck components. U.S., U.K., India, and China are the major spenders on defense equipment and maintenance of army. M80 Stileto is the largest U.S. naval vessel built using carbon-fiber composites. Armored vehicles have conventionally used steel armor for protection; however, weight of these large trucks creates logistical problems. Therefore, the adoption of CFRP is increasing in these vehicles. U.S. DOD aims to replace UH-60 Black Hawk with Bell Helicopter’s V-280 which incorporates carbon fibers in its wings, fuselage, and tail. The need for agility at the time of sudden attacks and upgrading the defense technologies has led to the shift from conventional materials to fiber reinforced materials, which is anticipated to propel the carbon fiber reinforced plastic market during the forecast period.

By Geography – Segment Analysis

Europe region held the largest share in the carbon fiber reinforced plastic (CFRP) market in 2019 up to 34%, owing to the increasing defense, and aerospace sectors in the region. The CFRP are particularly attractive to defense applications because of their exceptional strength, better stiffness-to-density ratios and superior physical properties. Also, CFRP provides relatively stronger and stiffer fibers in a tough resin matrix. According to International Trade Administration (ITA), the Norwegian Government presented a core defense spending budget of USD 6.9 billion in 2019. The Norwegian defense budget accounted for 1.62% of Norway’s GDP in 2018. French civil aerospace industry in 2018 grew to €50.36 billion, out of total non-consolidated aerospace and defense aerospace revenues of €65.4 billion. This is a 1.2% increase over 2017. Also, France has put forth an agreement with the U.K government of $2.1 billion to build a prototype combat drone, which will further boost CFRP market growth. Thus, the increasing aerospace and defense industry in Europe is likely to influence the growth of the carbon fiber reinforced plastic market in Europe.

Drivers – Carbon Fiber Reinforced Plastic (CFRP) Market

Growing Wind Power Sector

As a consequence of drastic increase in energy demand, the conventional sources of energy are depleting very fast. Hence, the need to expand and utilize the renewable energy sources like wind power is growing. The wind power sector is increasing, as use of renewable energy sources results in less emission of greenhouse and other harmful gases such as SO2. The modern wind turbine are being increasingly used in wind power sector as they are cost-effective, more reliable and have scaled up in size to multi-megawatt power ratings. Wind Energy installations in APAC increased by 23.6%. This region is set to witness high growth for wind energy equipment and materials majorly driven by commitments of government of India and China towards green energy. Carbon fiber reinforced plastic is used primarily in the spar, or structural element, of wind blades longer than 45m/148 ft, both for land-based and offshore systems. Carbon fiber has known benefits for reducing wind turbine blade mass due to the significantly improved stiffness, strength, and fatigue resistance per unit mass compared to fiberglass. Due to the increasing adoption of wind power energy source, the demand for the carbon fiber reinforced plastic is also increasing, which acts as a driver for the carbon fiber reinforced plastic market during the forecast period.

Stringent Government Regulation on Emission

Carbon fiber reinforced plastics are being extensively used in the automotive industries to reduce fuel consumption as well as emissions and to manufacture lightweight vehicles. Several governments across the world have imposed stringent standard emission and fuel economy regulations for vehicles. These standard regulations have compelled automotive OEMs to increase the use of lightweight materials such as carbon fiber reinforced plastics to assist in increasing the fuel economy of a vehicle while ensuring safety and performance. The emission regulation for light-duty cars such as Corporate Average Fuel Economy (CAFÉ) and Greenhouse Gas Emission standards sets fuel consumption standards for the vehicles. These regulations by the governments have made sure that the car manufacture henceforth might need to be manufacturing much lighter vehicles to obey as per these norms, which acts as a driver for the carbon fiber reinforced plastic market during the forecast period.

Challenges – Carbon Fiber Reinforced Plastic (CFRP) Market

High Cost of Carbon Fiber Reinforced Plastics

The cost of the carbon fiber reinforced plastics is at times supposedly higher. When compared with other traditional materials such as steel and aluminum, lightweight materials such as carbon fiber reinforced plastics (CFRP) and glass fiber reinforced plastics (GFRP) are costly. Composites of carbon fiber cost almost 1.5 to five times more than steel. High cost of fiber production inhibits large volume deployment. Therefore, precursor and processing costs need to be reduced. The high price of carbon fibers in many applications constrains the potential use of composites. Hence, the high cost of carbon fiber reinforced plastics may hinder with the carbon fiber reinforced plastics market growth during the forecast period. However, cost effective production methods coupled with high volume processing, assembly techniques and automation processes will lead to reduction of price in the near future.

#Carbon Fiber Reinforced Plastic Market#Carbon Fiber Reinforced Plastic Market Size#Carbon Fiber Reinforced Plastic Market Trends#Carbon Fiber Reinforced Plastic Market Forecast#Carbon Fiber Reinforced Plastic Market Growth

0 notes

Link

0 notes

Text

0 notes

Text

Engineering Plastics Market Trends: 2023, Growth Prospects, Future Demand, Size and Forecast Estimation by 2030

The engineering plastics market is a segment of the overall plastics industry that focuses on the production and utilization of high-performance plastics with enhanced mechanical, thermal, chemical, and electrical properties. Engineering plastics are designed to withstand demanding applications and provide superior performance compared to traditional plastics.

Here is a comprehensive overview of the engineering plastics market:

Types of Engineering Plastics:

Polyamide (PA, Nylon) Polycarbonate (PC) Polyoxymethylene (POM, Acetal) Polybutylene Terephthalate (PBT) Polyethylene Terephthalate (PET) Polyphenylene Sulfide (PPS) Polyether Ether Ketone (PEEK) Polyimide (PI) Polysulfone (PSU) Polyetherimide (PEI)

Properties and Applications:

•Polyamide (PA): Excellent strength, toughness, and chemical resistance. Used in automotive, electrical, and consumer goods industries. • Polycarbonate (PC): High impact resistance, transparency, and heat resistance. Applications include automotive components, electronic devices, and construction. • Polyoxymethylene (POM): Low friction, high stiffness, and dimensional stability. Used in gears, bearings, and electrical connectors. • Polybutylene Terephthalate (PBT): Good electrical insulation and resistance to chemicals. Commonly found in automotive parts, electrical connectors, and appliances. • Polyethylene Terephthalate (PET): High strength, chemical resistance, and clarity. Used in beverage bottles, food packaging, and textiles. • Polyphenylene Sulfide (PPS): Excellent thermal and chemical resistance. Applications include electrical components, automotive parts, and filters. • Polyether Ether Ketone (PEEK): Exceptional mechanical and thermal properties. Used in aerospace, medical, and electrical industries. • Polyimide (PI): Excellent heat resistance, electrical insulation, and chemical stability. Commonly used in electronics, aerospace, and automotive applications. • Polysulfone (PSU): High temperature resistance, transparency, and chemical resistance. Used in medical equipment, plumbing, and automotive parts. • Polyetherimide (PEI): Good heat resistance, flame retardancy, and electrical properties. Applications include electrical connectors, aerospace components, and automotive parts.

Market Drivers:

Increasing demand from automotive, electrical and electronics, and aerospace industries for lightweight and high-performance materials. Growing focus on sustainable and environmentally friendly plastics. Advancements in technology leading to improved engineering plastic formulations. Expansion of end-use industries in emerging economies.

Market Challenges:

High material costs compared to traditional plastics. Limited recycling options for certain engineering plastics. Stringent regulations on plastic waste management and disposal.

Market Trends:

Increasing research and development activities to develop new engineering plastic materials with enhanced properties. Rising adoption of engineering plastics in 3D printing applications. Growing demand for bio-based and biodegradable engineering plastics. Shift towards lightweight materials to improve fuel efficiency in automotive and aerospace sectors.

Regional Analysis:

Asia-Pacific: Dominates the engineering plastics market due to rapid industrialization, urbanization, and manufacturing activities in countries like China, India, and Japan.

North America: Significant market share, driven by the automotive, aerospace, and electrical industries.

Europe: Strong presence of automotive and electrical manufacturers contributing to the market growth.

Rest of the World: Increasing demand for engineering plastics in developing regions like Latin America and the Middle East.

Key Players:

BASF SE DowDuPont Inc. Covestro AG Solvay SA Mitsubishi Engineering-Plastics Corporation SABIC Evonik Industries AG Celanese Corporation LANXESS AG Arkema SA

The engineering plastics market is expected to continue growing as industries seek materials that offer superior performance, durability, and sustainability. Technological advancements and increasing investment in research and development activities will likely drive the development of innovative engineering plastic materials in the future.

0 notes