#North America Heating Equipment Market Segmentation

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr.com rank in the US is 25.

Text

Brazed Plate Heat Exchangers Market: Regional Analysis, Competitive Landscape, and Key Players

The global brazed plate heat exchangers market size is expected to reach USD 1.62 billion by 2030, registering a CAGR of 6.3% over the forecast period, according to a new report by Grand View Research, Inc. Rising product demand, particularly on account of cost-effectiveness, lower carbon footprints, and higher energy efficiency is anticipated to drive the industry. According to Centrum Institutional Research, investments in the chemical industry have increased 2.5 times in the last decade, rising to 6,100 crores in FY22. Brazed plate heat exchangers are used in the chemical manufacturing process to cool, heat, and mix chemicals.

The chemical industry’s rapid expansion is projected to be a major driver for market growth. In industrial power generation engines, lubricating oil is required to optimize performance, protect moving parts, and provide optimal operating conditions for internal components. A brazed plate heat exchanger is used for activation units and engines in power generation industrial facilities as it has oil-cooling properties. Rapid industrialization in growing economies and rising investments in commercial, industrial, and residential projects have contributed to a rise in industry growth. Furthermore, increased product demand in the food, oil & gas, and other industries due to lower operational costs will also support market growth.

Brazed plate heat exchangers are utilized in the oil & gas industry for various applications, such as selective gas component extraction, natural gas evaporation, and industrial gas consumption. Brazed plate heat exchangers are now chosen over traditional shell & tube heat exchangers due to their thermal efficiency, compactness, and quicker lead time. Providers of brazed plate heat exchangers are adopting several strategies, including acquisitions, mergers, new product developments, and geographical expansions to enhance their industry presence. For instance, in October 2021, Alfa Laval launched the AC74 to improve energy efficiency and enable the use of refrigerants with a low global warming potential.

Brazed Plate Heat Exchangers Market Report Highlights

The multi-circuit segment is estimated to expand at a steady CAGR over the forecast period owing to advantages, such as a low maintenance cost, smaller footprint, and energy efficiency

The HVAC-R segment accounted for the maximum share in 2022. Due to their lower footprint, brazed plate heat exchangers have become increasingly popular among HVAC equipment manufacturers

The Europe region accounted for the maximum revenue share in 2022. Rising public and private infrastructure investments are expected to drive brazed plate heat exchanger demand in the HVAC & refrigeration industry

Asia Pacific is estimated to advance at the fastest CAGR over the forecast period owing to increased industrial construction and infrastructure activities in emerging nations, such as India, China, Vietnam, and Thailand

In February 2022, Alfa Laval launched AC540 brazed plate heat exchangers, such as ACK540, ACH540, CBP540 and ACP540, which were manufactured in San Bonifacio, Italy

Brazed Plate Heat Exchangers Market Segmentation

Grand View Research has segmented the global brazed plate heat exchangers market on the basis of product, application, and region:

Brazed Plate Heat Exchangers Product Outlook (Revenue, USD Million, 2018 - 2030)

Single-circuit

Multi-circuit

Brazed Plate Heat Exchangers Application Outlook (Revenue, USD Million, 2018 - 2030)

HVAC-R

Chemical & Petrochemical

Food & Beverage

Power Generation

Heavy Industry

Others

Brazed Plate Heat Exchangers Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

France

Germany

Italy

Asia Pacific

China

Japan

India

Central & South America

Brazil

Middle East & Africa

Saudi Arabia

UAE

Key players in the Brazed Plate Heat Exchangers Market

Alfa Laval

Danfoss

Kelvion Holding GmbH

SWEP International AB

Xylem Inc.

API Heat Transfer

AIC

Hisaka Works, Ltd.

Charts Industries, Inc.

Order a free sample PDF of the Brazed Plate Heat Exchangers Market Intelligence Study, published by Grand View Research.

0 notes

Text

IC Substrate Market Size, Analyzing Forecasted Outlook and Growth for 2025-2031

Global Info Research’s report offers key insights into the recent developments in the global IC Substrate market that would help strategic decisions. It also provides a complete analysis of the market size, share, and potential growth prospects. Additionally, an overview of recent major trends, technological advancements, and innovations within the market are also included.Our report further provides readers with comprehensive insights and actionable analysis on the market to help them make informed decisions. Furthermore, the research report includes qualitative and quantitative analysis of the market to facilitate a comprehensive market understanding.This IC Substrate research report will help market players to gain an edge over their competitors and expand their presence in the market.

According to our (Global Info Research) latest study, the global IC Substrate market size was valued at US$ 15160 million in 2024 and is forecast to a readjusted size of USD 27020 million by 2031 with a CAGR of 8.7% during review period.

IC substrate is a type of carry material for integrated circuit with internal circuit to connect the chips and PCBs. Additionally, the IC substrate can protect the circuit, special line, it is designed for heat dissipation and acts standardized module of IC components. It is one of the most key materials of the IC packaging.

The main IC substrate players include Ibiden, Unimicron, Semco, Simmtech, Kinsus, etc. The top 5 players account for approximately 45% of the total global market. Asia-Pacific is the largest consumer market accounting for about 87%, followed by Europe and North America. In terms of type, FC-BGA is the largest segment, with a share about 30%. And in terms of application, the largest application is smart phones, followed by PC (tablet, laptop).

This report is a detailed and comprehensive analysis for global IC Substrate market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2025, are provided.

We have conducted an analysis of the following leading players/manufacturers in the IC Substrate industry: Unimicron、Ibiden、Nan Ya PCB、Shinko Electric Industries、Kinsus Interconnect Technology、AT&S、Semco、Kyocera、TOPPAN、Zhen Ding Technology、Daeduck Electronics、ASE Material、LG InnoTek、Simmtech、Shennan Circuit、Shenzhen Fastprint Circuit Tech、ACCESS、Suntak Technology、National Center for Advanced Packaging (NCAP China)、Huizhou China Eagle Electronic Technology、DSBJ、Shenzhen Kinwong Electronic、AKM Meadville、Victory Giant Technology、KCC (Korea Circuit Company) Market segment by Type: WB CSP、FC BGA、FC CSP、PBGA、SiP、BOC、Other Market segment by Application:Smart Phones、PC (Tablet, Laptop)、Wearable Devices、Others Report analysis: The IC Substrate report encompasses a diverse array of critical facets, comprising feasibility analysis, financial standing, merger and acquisition insights, detailed company profiles, and much more. It offers a comprehensive repository of data regarding marketing channels, raw material expenses, manufacturing facilities, and an exhaustive industry chain analysis. This treasure trove of information equips stakeholders with profound insights into the feasibility and fiscal sustainability of various facets within the market. Illuminates the strategic maneuvers executed by companies, elucidates their corporate profiles, and unravels the intricate dynamics of the industry value chain. In sum, the IC Substrate report delivers a comprehensive and holistic understanding of the markets multifaceted dynamics, empowering stakeholders with the knowledge they need to make informed decisions and navigate the market landscape effectively. Conducts a simultaneous analysis of production capacity, market value, product categories, and diverse applications within the IC Substrate market. It places a spotlight on prime regions while also performing a thorough examination of potential threats and opportunities, coupled with an all-encompassing SWOT analysis. This approach empowers stakeholders with insights into production capabilities, market worth, product diversity, and the markets application prospects. Assesses strengths, weaknesses, opportunities, and threats, offering stakeholders a comprehensive understanding of the IC Substrate markets landscape and the essential information needed to make well-informed decisions. Market Size Estimation & Method Of Prediction

Estimation of historical data based on secondary and primary data.

Anticipating market recast by assigning weightage to market forces (drivers, restraints, opportunities)

Freezing historical and forecast market size estimations based on evolution, trends, outlook, and strategies

Consideration of geography, region-specific product/service demand for region segments

Consideration of product utilization rates, product demand outlook for segments by application or end-user. About Us: Global Info Research is a company that digs deep into Global industry information to IC Substrate enterprises with market strategies and in-depth market development analysis reports. We provide market information consulting services in the Global region to IC Substrate enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Polyamide Market: Key Insights, Growth Drivers, and Future Opportunities

Introduction

The Polyamide Market is projected to reach $40.5 billion by 2028, growing at a CAGR of 5.7% from 2023 to 2028. Polyamides (nylon) are widely used in automotive, electronics, and textile industries due to their high strength, chemical resistance, and versatility. The growing demand for lightweight materials in automotive and electronics is a significant market driver.

Market Overview

Polyamides are available in various forms, including PA6, PA66, and bio-based polyamides. They are used in applications such as automotive parts, electrical components, packaging, and textiles. The shift toward sustainable and bio-based materials is creating new opportunities in the market. Key Applications: Automotive, Electrical & Electronics, Textiles, Packaging, Consumer Goods

Key Market Segments

By Product Type: PA6, PA66, Bio-Based Polyamide

By Application: Automotive, Electronics, Textiles, Packaging, Industrial Equipment

By Region: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Regional Insights

1. Asia-Pacific – Market Leader

Asia-Pacific dominates the market, accounting for over 50% of global consumption, driven by strong growth in automotive and textile manufacturing in China, India, and Japan.

2. North America

North America shows steady growth, supported by demand for high-performance polymers in the automotive and electronics industries.

3. Europe

Europe’s focus on sustainability and lightweight automotive materials is driving the adoption of bio-based polyamides. The region’s strong automotive industry contributes significantly to market demand.

Key Market Drivers

Growing Demand for Lightweight Automotive Components: Polyamides help reduce vehicle weight and improve fuel efficiency, making them essential in automotive manufacturing.

Expansion of the Electronics Industry: The increasing use of polyamides in electronic components for heat resistance and durability is boosting demand.

Shift Toward Sustainable Materials: Bio-based polyamides are gaining popularity due to increasing environmental awareness and stringent regulations.

Challenges

High Production Costs: Polyamide production requires expensive raw materials and processes, which can limit adoption.

Fluctuating Raw Material Prices: The volatility in petroleum-based raw materials affects production costs and pricing.

Future Outlook

The Polyamide Market is set for steady growth, driven by the rising demand for lightweight, durable, and sustainable materials. Companies investing in bio-based polyamides and advanced composites will unlock new growth opportunities in the coming years.

Conclusion

The Polyamide Market presents significant opportunities across various industries, from automotive to electronics and textiles. Businesses focusing on innovation and sustainability will gain a competitive advantage in this evolving market.

Contact Us

Want to stay ahead in the Polyamide Market? Mark & Spark Solutions offers expert market research and insights to help your business thrive. Contact us today!

0 notes

Text

Liquefied Natural Gas (LNG) Liquefaction Equipment Market Analysis & Forecasts 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Liquefied Natural Gas (LNG) Liquefaction Equipment Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Liquefied Natural Gas (LNG) Liquefaction Equipment Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Liquefied Natural Gas (LNG) Liquefaction Equipment Market?

The Liquefied Natural Gas (LNG) liquefaction equipment market size reached US$ 811.2 Million in 2023. Looking forward, Reports and Insights expects the market to reach US$ 1,226.5 Million by 2032, exhibiting a growth rate (CAGR) of 4.7% during 2024-2032.

What are Liquefied Natural Gas (LNG) Liquefaction Equipment?

Liquefied Natural Gas (LNG) liquefaction equipment is utilized to convert natural gas into its liquid state for more convenient transportation and storage. This process involves lowering the temperature of the gas to -162 degrees Celsius, causing it to condense into a clear, colorless, and non-toxic liquid. The primary components of LNG liquefaction equipment include compressors, heat exchangers, and cryogenic storage tanks. Compressors elevate the gas pressure before it enters the heat exchangers, where it is cooled using refrigerants. Once cooled, the gas is stored in cryogenic tanks until it is ready for shipment. This equipment is engineered to function efficiently under extremely low temperatures and high pressures, ensuring the safe and dependable production of LNG.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1765

What are the growth prospects and trends in the Liquefied Natural Gas (LNG) Liquefaction Equipment industry?

The liquefied natural gas (LNG) liquefaction equipment market growth is driven by various factors. The market for Liquefied Natural Gas (LNG) liquefaction equipment is experiencing notable expansion due to the increasing global demand for natural gas as a cleaner energy alternative. This growth is marked by the continual development of more advanced and efficient liquefaction technologies to meet the rising need for LNG. Key drivers include the ongoing expansion of LNG infrastructure, particularly in emerging markets, and the growing adoption of LNG as a fuel in various industries including transportation. Moreover, innovations in liquefaction equipment design, such as modular and space-saving units, are improving operational efficiency and reducing upfront costs. However, challenges such as high initial investments and stringent regulatory standards may pose obstacles to market growth. Hence, all these factors contribute to liquefied natural gas (LNG) liquefaction equipment market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Equipment Type:

Liquefaction Units

Heat Exchangers

Compressors

Storage Tanks

Pumps

Others

By Capacity:

Small-Scale (<0.5 MTPA)

Mid-Scale (0.5-2 MTPA)

Large-Scale (>2 MTPA)

By Process Cycle:

Cascade Process

Mixed Refrigerant Process

Shell-And-Tube Process

Others

By Technology:

Conventional LNG Liquefaction

Floating LNG Liquefaction

Modular LNG Liquefaction

By End-Use Industry:

Power Generation

Transportation

Industrial

Residential & Commercial

By Application:

Export/Import Terminals

Bunkering Facilities

Peak Shaving Plants

Distributed LNG Production Units

Segmentation By Region:

North America:

United States

Canada

Europe:

Germany

The U.K.

France

Spain

Italy

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Who are the key players operating in the industry?

The report covers the major market players including:

Air Products and Chemicals, Inc.

Linde plc

TechnipFMC plc

Siemens Energy AG

Chart Industries, Inc.

Mitsubishi Heavy Industries, Ltd.

General Electric Company

Bechtel Corporation

McDermott International, Inc.

Baker Hughes Company

Chiyoda Corporation

Saipem S.p.A.

JGC Corporation

Samsung Engineering Co., Ltd.

KBR, Inc.

View Full Report: https://www.reportsandinsights.com/report/Liquefied Natural Gas (LNG) Liquefaction Equipment-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd. 1820 Avenue M, Brooklyn, NY, 11230, United States Contact No: +1-(347)-748-1518 Email: [email protected] Website: https://www.reportsandinsights.com/ Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/ Follow us on twitter: https://twitter.com/ReportsandInsi1

#Liquefied Natural Gas (LNG) Liquefaction Equipment Market share#Liquefied Natural Gas (LNG) Liquefaction Equipment Market size#Liquefied Natural Gas (LNG) Liquefaction Equipment Market trends

0 notes

Text

Temperature Sensor Market Key Trends, New Opportunities, Analysis And Sales Revenue 2025-2032

The temperature sensor market is witnessing robust growth, fueled by increasing demand across various industries such as automotive, healthcare, industrial automation, and consumer electronics. Temperature sensors are essential for monitoring and controlling temperature in critical applications, driving the adoption of advanced technologies and ensuring efficient operations.

According to SkyQuest’s latest market research, Temperature Sensor Market size is poised to grow at a CAGR of 5.6% by 2032, driven by technological advancements, the rise of automation, and the increasing adoption of smart devices.

Request a sample of the report here: https://www.skyquestt.com/sample-request/temperature-sensor-market

Market Overview: The Expanding Role of Temperature Sensors

Temperature sensors are devices that detect and measure temperature changes, playing a pivotal role in a wide range of industries. With applications spanning from manufacturing to healthcare, these sensors help optimize performance, improve safety, and enhance efficiency.

The demand for temperature sensors is increasing as industries continue to prioritize automation, precision, and monitoring of environmental conditions. From industrial machines to consumer electronics, temperature sensors ensure that systems operate within their optimal thermal conditions.

Key Market Drivers

Rising Demand from Automotive & Industrial Automation The automotive industry relies heavily on temperature sensors for engine management, climate control, and battery monitoring in electric vehicles (EVs). Similarly, temperature sensors are critical in industrial automation processes to maintain optimal operating conditions in factories and manufacturing plants.

Healthcare Applications With the rise of wearable medical devices and the need for accurate monitoring of patient temperature, the healthcare sector is increasingly incorporating advanced temperature sensors to improve diagnostics, patient care, and medical equipment performance.

Advancements in IoT and Smart Devices The growing adoption of the Internet of Things (IoT) and smart home devices is driving demand for temperature sensors in applications like smart thermostats, temperature control systems, and HVAC solutions.

Technological Innovations in Sensor Design Advancements in temperature sensor technology, such as miniaturization, wireless communication, and improved accuracy, are boosting the market’s growth by making sensors more versatile, reliable, and cost-effective.

Speak with an analyst for more insights on industry trends: https://www.skyquestt.com/speak-with-analyst/temperature-sensor-market

Market Segmentation

By Sensor Type

Thermocouples – Dominating due to their wide temperature range and versatility across various applications.

RTDs (Resistance Temperature Detectors) – Known for their accuracy and stability, ideal for precision applications.

Thermistors – Common in consumer electronics due to their sensitivity and cost-effectiveness.

Semiconductor-Based Sensors – Gaining popularity in small-scale electronics and integrated circuits.

By Application

Automotive – Used in engine monitoring, battery temperature regulation in EVs, and climate control systems.

Healthcare – Crucial for temperature monitoring in medical devices, wearables, and diagnostic equipment.

Industrial Automation – Integral to manufacturing processes, equipment monitoring, and machine efficiency.

Consumer Electronics – Employed in devices like smartphones, computers, and household appliances.

Food & Beverage – Essential for temperature control in production and storage to ensure product quality and safety.

HVAC Systems – Ensures optimal heating, ventilation, and air conditioning for comfort and energy efficiency.

Regional Insights

North America: Leading the Temperature Sensor Market The United States and Canada are at the forefront, driven by robust industries in automotive, healthcare, and industrial automation. Increased demand for electric vehicles and smart technologies are major factors contributing to the market’s growth in the region.

Europe: Technological Advancements & Sustainability Focus Europe’s growing emphasis on sustainability and energy-efficient technologies has driven the demand for temperature sensors in renewable energy, HVAC, and automotive applications. Countries like Germany, the UK, and France are key players in this market.

Asia-Pacific: Rapid Growth in Automotive & Industrial Sectors China, Japan, and India are rapidly adopting advanced sensor technologies, especially in automotive, industrial, and consumer electronics sectors. The rise of electric vehicles and automation is accelerating the market in this region.

Latin America & Middle East: Emerging Market Potential Countries in Latin America and the Middle East are witnessing growing demand for temperature sensors in energy, construction, and manufacturing sectors, presenting new market opportunities.

For a detailed market analysis and strategic insights, explore the full SkyQuest report:

Top Companies in the Temperature Sensor Market

Leading companies in the temperature sensor industry are focused on research and development, expanding their product offerings, and advancing manufacturing processes to maintain a competitive edge:

Honeywell International Inc.

Siemens AG

TE Connectivity Ltd.

Texas Instruments Inc.

Emerson Electric Co.

Analog Devices, Inc.

ABB Ltd.

Bosch Sensortec

STMicroelectronics

NXP Semiconductors

Emerging Trends in the Temperature Sensor Market

Wireless and IoT-enabled Sensors The integration of wireless connectivity in temperature sensors is transforming the market, enabling remote monitoring, real-time data collection, and predictive maintenance in industrial and consumer applications.

Miniaturization and Integration with Smart Devices The demand for smaller, more integrated sensors in wearables, portable medical devices, and consumer electronics is growing. Miniaturization allows for easier integration into smaller systems without compromising performance.

Self-Calibration and Enhanced Accuracy Advances in self-calibration technologies are allowing temperature sensors to maintain higher accuracy and reduce manual recalibration, ensuring reliability in critical applications like healthcare and automotive.

AI and Data Analytics in Temperature Monitoring Artificial intelligence and data analytics are being applied to temperature sensor systems to optimize energy consumption, improve predictive maintenance, and enhance system performance.

The temperature sensor market is poised for rapid growth as technological advancements continue to shape the demand for more efficient, accurate, and cost-effective sensors. With industries increasingly prioritizing automation, sustainability, and IoT connectivity, the market for temperature sensors is expanding across various sectors, from automotive to healthcare.

Companies focusing on innovation, miniaturization, wireless integration, and sustainability will find themselves at the forefront of this rapidly evolving market.

#Asia Temperature Sensor Market#Europe Temperature Sensor Market#Middle East Temperature Sensor Market Size#North America Temperature Sensor Market

0 notes

Text

High-Intensity Focused Ultrasound Therapy Market Size, Growth Outlook 2035

the High Intensity Focused Ultrasound Therapy Market Size was estimated at 0.13 (USD Billion) in 2024. The High Intensity Focused Ultrasound Therapy Market Industry size is expected to grow from 0.15 (USD Billion) in 2025 to 0.54 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 15.50% during the forecast period (2025 - 2034).

Executive Summary

The High-Intensity Focused Ultrasound (HIFU) Therapy Market has been experiencing a significant surge due to its non-invasive nature, precision in targeting tissues, and minimal recovery time. HIFU is used in various therapeutic applications, including the treatment of tumors, uterine fibroids, and prostate cancer. The market has witnessed technological advancements and growing demand across regions, fueled by rising healthcare awareness, aging populations, and the increase in chronic diseases.

Market Overview

HIFU therapy uses focused ultrasound waves to generate heat in specific areas of the body, leading to the targeted destruction of tissues. Unlike traditional surgery, it does not require incisions and typically involves outpatient procedures. As per MRFR analysis, the High Intensity Focused Ultrasound Therapy Market Size was estimated at 0.13 (USD Billion) in 2024. The High Intensity Focused Ultrasound Therapy Market Industry size is expected to grow from 0.15 (USD Billion) in 2025 to 0.54 (USD Billion) till 2034, at a CAGR (growth rate) is expected to be around 15.50% during the forecast period (2025 - 2034).

North America, particularly the United States, dominates the HIFU therapy market, followed by Europe and the Asia-Pacific region. The rise in awareness about non-invasive treatments, coupled with advancements in ultrasound technology, are key factors contributing to market growth.

Market Drivers

Non-invasive Treatment Benefits: HIFU's non-invasive nature is one of the primary drivers, as patients seek alternatives to traditional surgery with less pain, minimal recovery time, and reduced hospital stays.

Increasing Prevalence of Cancer: The rising incidence of cancers, particularly prostate, liver, and breast cancers, has led to an increase in demand for non-invasive treatments such as HIFU.

Technological Advancements: Developments in ultrasound technology, precision, and imaging systems have significantly improved the effectiveness and safety of HIFU therapy, boosting market growth.

Aging Population: The global aging population is contributing to the rise in conditions like tumors, prostate cancer, and fibroids, increasing the demand for HIFU therapy.

Market Restraints

High Cost of Treatment: One of the major challenges is the high cost of HIFU therapy, which may not be affordable for a large portion of the population, especially in developing regions.

Limited Availability of Equipment: The availability of HIFU equipment is concentrated in developed countries, which may hinder the market's growth in emerging economies.

Lack of Awareness: In certain regions, there is limited awareness regarding the advantages of HIFU therapy, affecting its adoption.

Regional Analysis

North America: The United States holds the largest share of the HIFU market due to high healthcare spending, a robust healthcare infrastructure, and the presence of leading manufacturers. Canada also contributes to market growth with increasing adoption of non-invasive treatments.

Europe: Countries like Germany, the UK, and France have well-established healthcare systems and are witnessing rising demand for HIFU therapies, especially for treating uterine fibroids and prostate cancer.

Asia-Pacific: Countries like China, Japan, and India are showing significant growth potential due to the growing prevalence of cancer and the increasing adoption of advanced therapeutic options. Rising disposable income and healthcare investments in these regions are expected to drive the market.

Segmental Analysis

By Application:

Tumor Treatment (Prostate Cancer, Liver Cancer, Breast Cancer)

Uterine Fibroid Treatment

Pain Management

Aesthetic Treatments (Facial Rejuvenation, Skin Tightening)

By End-User:

Hospitals

Specialized Clinics

Research Institutes

Key Market Players

Guided Therapy

EDAP TMS

SonaCare Medical LLC

heraclion

Chongqing Haifu Medical Technology Co. Ltd

Koninklijke Philips N.V.

Shanghai A&S Co. LTD

Recent Developments

Partnerships and Collaborations: InSightec formed strategic collaborations with leading hospitals and research institutes to expand the clinical use of HIFU therapy, particularly in cancer treatment.

Technological Innovations: Recent advancements include the development of more compact, portable, and cost-effective HIFU devices, making the therapy more accessible to healthcare centers globally.

For more information, please visit @marketresearchfuture

#High-Intensity Focused Ultrasound Therapy Market Size#High-Intensity Focused Ultrasound Therapy Market Share#High-Intensity Focused Ultrasound Therapy Market Growth#High-Intensity Focused Ultrasound Therapy Market Analysis#High-Intensity Focused Ultrasound Therapy Market Trends#High-Intensity Focused Ultrasound Therapy Market Forecast#High-Intensity Focused Ultrasound Therapy Market Segments

0 notes

Text

Ready-To-Drink Market Size Was Projected to Reach USD 4.67 Billion by 2032

Ready-To-Drink Market Size Was Valued at USD 1.67 Billion in 2023 and is Projected to Reach USD 4.67 Billion by 2032, Growing at a CAGR of 12.1 % From 2024-2032.

Ready-To-Drink liquids additionally referred to as RTDs are single-use packaged drinks which can be packaged and bought in a organized form equipped for immediate consumption upon buy. Such Beverages do not need any further processing and can be ate up without delay through the package. Ready-to-drink (RTD) liquids have received a whole lot of popularity due to their functionality, specifically in the summer season. Consumers’ leisure of the fortified drinks and alcohols and the easiness of the product is the precise feature provided by the RTDs.

The Major Players Covered in this Report:

PepsiCo Inc.(US)

Fuze Beverage (US)

Nestle S.A. (Switzerland)

The Coca-Cola Company(US)

Jack Daniel's (US)

Suntory Beverages & Food Ltd. (Japan)

Kirin Brewery Company, Limited (Japan)

Red Bull GmbH (Austria)

Monster Beverage Corporation (US)

NZMP (New Zealand)

Zevia (US)

White Claw Hard Seltzer (US)

Southeast Bottling & Beverage (US)

Gehl Foods LLC (US)

Tropical Bottling Corporation (US) and Other Major Players

Get more Information About the Ready-To-Drink Market here & Take a Sample Copy:

https://introspectivemarketresearch.com/request/16553

"Kindly use your official email ID for all correspondence to ensure seamless engagement and access to exclusive benefits, along with prioritized support from our sales team."

Introspective Market Research specializes in delivering comprehensive market research studies that offer valuable insights and strategic guidance to businesses worldwide. With a focus on reliability and accuracy, our reports empower informed decision-making. An in-depth examination of the overall Ready-To-Drink Market is done to provide this report encompassing all essential market fundamentals.

The Report Will Include A Major Chapter

Patent Analysis

Regulatory Framework

Technology Roadmap

BCG Matrix

Heat Map Analysis

Price Trend Analysis

Investment Analysis

Grab your exclusive discount here before the offer ends:

https://introspectivemarketresearch.com/discount/16553

The Ready-To-Drink Market Trend Analysis

Introduction of Creative New Flavors and New Packaging Options

Consumer motivation to buy the product is the number one component that acts efficiently at the back of the sales of RTD Beverages. Many manufacturers today are transferring toward greater natural, botanical, and natural flavors that create the taste of herbal substances at the side of a few health blessings. Such Creative New Flavors with colorful geared up-to-drink drinks are becoming perfect to satisfy the desire that is widespread in the adventure society for brand spanking new and interesting flavor reports.

Creation of Innovative RTD Beverages With New Flavors and Ingredients

The RTD beverage category for the previous few years is developing very fast. To make the most out of the fashion the manufacturers are going to want to paintings successfully on their improvement and marketing to stand out of others and establish a robust experience of Meaningful to gain big profits.

Segmentation of The Ready-To-Drink Market

By Type

Tea & Coffee

Sports & Energy Drinks

Dairy-Based Beverages

Juices & Nectars

Fortified Water

Alcopops

Others

By Packaging Type

Bottles

Cans

Cartons

Other

By Sales Channel

Supermarkets & Hypermarkets

Specialty Stores

Convenience Stores

Online Stores

By Region

North America (U.S., Canada, Mexico)

Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC)

Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

South America (Brazil, Argentina, Rest of SA)

Through meticulous segmentation analysis and extensive geographical coverage, we offer a deep understanding of regional trends. A key aspect of our Accounting Software report is the thorough examination of company profiles and competitive landscapes. This provides detailed insights into market players' roles, overviews, operating business segments, products, and financial performance. By meticulously evaluating critical metrics like production volume, sales volume, and sales margin, we offer a comprehensive understanding of their market position.

Inquiry of this Research Report:

https://introspectivemarketresearch.com/inquiry/16553

The following points were extensively researched:

Key Players: Here, the Travel and Expense Ready-To-Drink Market research focuses on mergers and acquisitions, expansions, analyses of important players, company founding dates, markets served, manufacturing infrastructure, and revenue of key players.

Breakdown by Product and Application: Information on market size by product and application is provided in this section.

Regional Analysis: The report examines each area and nation based on market size by product and application, major players, and market forecast.

Profiles of International Players: On the basis of their gross margin, pricing, sales, revenue, business, products, and other firm information, participants are rated in this game.

Market Dynamics: It includes supply chain analysis, analysis of regional marketing, challenges, opportunities, and drivers analysed in the report.

Key Findings of the Research Study. Appendix: It includes information about the research methodology, data sources, and authors of the study, as well as a disclaimer.

The latest research on the Ready-To-Drink Market provides a comprehensive overview of the market for the years 2024 to 2032. It gives a comprehensive picture of the global Automotive Wrap Films industry, considering all significant industry trends, market dynamics, competitive landscape, and market analysis tools such as Porter's five forces analysis, Industry Value chain analysis, and PESTEL analysis of the Automotive Damper Market. Moreover, the report includes significant chapters such as Patent Analysis, Regulatory Framework, Technology Roadmap, BCG Matrix, Heat Map Analysis, Price Trend Analysis, and Investment Analysis which help to understand the market direction and movement in the current and upcoming years. The report is designed to help readers find information and make decisions that will help them grow their businesses.

Unlock Insights and Make Informed Decisions – Purchase Our Research Report

https://introspectivemarketresearch.com/checkout/?user=1&_sid=16553

About us:

At Introspective Market Research Private Limited, we are a forward-thinking research consulting firm committed to driving our clients' growth and market dominance. Leveraging cutting-edge technology, big data, and advanced analytics, we provide deep insights and strategic solutions that enable our clients to stay ahead in a competitive landscape. Our expertise spans across comprehensive Market Research Reports, Holistic Market Insights, Macro-Economic Analysis, and tailored Go-to-Market (GTM) Strategies. Through our Consulting Services and AI-Driven Solutions, we empower businesses to navigate challenges and achieve their objectives. Additionally, we offer Product Design and Prototyping support and Flexible Staffing Solutions to meet evolving industry demands. Our IMR Knowledge Cluster ensures continuous learning and innovation, guiding our clients toward sustainable success.

Contact us:

Canada Office

Introspective Market Research Private Limited, 138 Downes Street Unit 6203- M5E 0E4, Toronto, Canada.

APAC Office

Introspective Market Research Private Limited, Office No. 401, Saudamini Commercial Complex, Chandani Chowk, Kothrud, Pune India 411038

Ph no: + +91-81800-96367 / +91-7410103736

Email: [email protected]

#Global Ready-To-Drink Market#Ready-To-Drink Market Size#Ready-To-Drink Market Share#Ready-To-Drink Market Growth#Ready-To-Drink Market Trend#Ready-To-Drink Market segment#Ready-To-Drink Market Opportunity#Ready-To-Drink Market Analysis 2024#Global Ready-To-Drink Market Industry Size

0 notes

Text

Occupancy Sensor Companies - Legrand (France) and Johnson Controls Inc (US) are the Key Players

The global occupancy sensor market is expected to reach USD 5.20 billion in 2030 from USD 2.75 billion in 2024, at a CAGR of 11.2% during the forecast period. The demand for occupancy sensors is increasing due to the need for high energy efficiency, new releases of smart home technologies, and growing interest in sustainability. It activates lighting systems, heating, ventilation, cooling, and other appliances in a room according to its occupancy to help reduce energy consumption. In addition, the development of smart buildings and independent homes embracing automation systems and increasing demand for energy-efficient solutions is enabling the demand for occupancy sensors in residential, commercial, and industrial spaces.

The key players operating in the occupancy sensor market — Legrand (France), Johnson Controls Inc (US), Eaton (Ireland), Honeywell International Inc (US), Schneider Electric (France), Acuity Brands Inc (US), Signify Holding (Netherland), Hubbell (US), Leviton Manufacturing Co., Ltd., (US), Lutron Electronics Co Ltd (US), Siemens (Germany), Alan Manufacturing Inc (US), Enerlites Inc (US), Functional Devices Inc (US), Pyrotech Electronics Pvt Ltd (India), B.E.G Bruck Electronic GmbH (Germany), Hager Group (Germany), Crestron Electronics Inc (US), Opex Co Ltd (Japan), Pressac Communications Limited (UK), Avuity (US), Enocean GmbH (Germany), IR-TEC International Ltd (Taiwan), Wipro Lighting (India), and Intermatic Incorporated (US). These players have adopted various growth strategies to strengthen their occupancy sensor market position. The methods include product launches, expansions, partnerships, collaborations, and mergers and acquisitions.

Major Occupancy Sensor companies include:

Legrand (France)

Johnson Controls Inc. (US)

Eaton (Ireland)

Honeywell International Inc. (US)

Schneider Electric (France)

Acuity Brands Inc. (US)

Signify Holding (Netherlands)

Hubbell (US)

Leviton Manufacturing Co., Ltd. (US)

Lutron Electronics Co. Ltd. (US)

Legrand (France)

Legrand designs and manufactures low-voltage electrical installation and data network systems for residential, commercial, hospitality, and industrial buildings. The company offers protection, lighting control, and connectivity solutions in its product portfolio as well as home and building automation, communication systems, and industrial products. Its portfolio includes energy distribution, door phones, cable management, home automation systems, wiring accessories, passive networking, and lighting management systems. Legrand offers occupancy sensors under its brand in lighting solutions.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=3859894

Johnson Controls Inc (US)

Johnson Controls empowers companies to build smarter, safer, healthier, and more sustainable environments. Products offered by Johnson Controls include solutions that might help improve energy and building operations, lead-acid and high-performance batteries for hybrid and electric vehicles, and automotive interior systems for passengers. These are procured through four main business segments: Building Solutions North America, Building Solutions EME/LA, Building Solutions Asia Pacific, and Other Products. The Building Solutions unit designs, sells, installs, and services heating, ventilation, and air conditioning systems, controls, building management systems, refrigeration, integrated electronic security, and fire detection and suppression systems. Its Global Products segment designs, manufactures, and sells HVAC equipment, controls, software, and services for residential and commercial markets.

Eaton (Ireland)

Eaton Corporation plc is the intelligent power management company committed for improving the quality of life and protecting the environment. The company has five business segments: Electrical Americas, Electrical Systems and Services, Hydraulics, Aerospace and Vehicle. This makes Eaton offer an extensive variety of products used by different industries in several countries, including data centers, utilities, industrial, commercial, machine building, residential, aerospace, and mobility markets. Eaton is well-positioned to take advantage of the fundamental global megatrends of electrification, the energy transition, and digitalization. Growth is further fueled by the reindustrialization of North America and Europe, a rise in infrastructure investments in clean energy, and the growth of major projects in North America.

Honeywell International Inc (US)

Honeywell International, Inc. operates under four business segments categorized under product and service lines: Aerospace, Honeywell Building Technologies, Performance Materials and Technologies, and Safety & Productivity Solutions. Honeywell Building Technologies offers and provides occupancy sensors and software applications like advanced building control and optimization with sensors, switches, control systems, as well as instruments for energy management, fire and safety, access control, video surveillance, and others. The Aerospace segment provides products for aircraft, Performance Materials and Technologies that produce high-performance chemicals and materials, and Safety & Productivity Solutions focuses on safety and asset performance in working environments.

0 notes

Text

Future of Cleanroom Technology In Healthcare Market: Insights from Industry Experts

The global cleanroom technology in healthcare market size is expected to reach USD 5.6 billion by 2030, according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 5.58% from 2023 to 2030. Growing compliance with stringent regulatory standards for new product approvals, technological advancements by key players to provide customized services to manufacturing companies, and an increase in awareness about contamination-free products coupled with growing demand in biopharmaceutical and pharma companies to develop high-quality products are some of the key factors driving the market growth.

Cleanroom is essential in several industries, including pharmaceuticals, biotechnology, medical devices, and electronics manufacturing. The advancement of cleanroom technology is a result of the growing demand for contamination-free production and the stringent regulations set by regulatory bodies. In recent years, the market for cleanroom technology in healthcare has witnessed significant growth, and it is expected to continue in the coming years.

With the integration of robotics, cleanrooms can operate with minimal human intervention, reducing the risk of contamination. The use of automation and robotics in cleanrooms also leads to increased efficiency and productivity, resulting in higher-quality products. In addition, the implementation of artificial intelligence (AI) and machine learning (ML) in cleanroom technology is also gaining momentum, as it enables real-time monitoring and control of the cleanroom environment.

The COVID-19 pandemic has had a significant impact on market. The pandemic has highlighted the importance of maintaining a clean and sterile environment in the pharmaceuticals, biotechnology, and medical devices industries, where contamination is a major concern. The pandemic has also increased the demand for cleanroom technology in the production of medical equipment, such as ventilators, masks, and personal protective equipment (PPE). These factors have positively impacted the market growth.

Gather more insights about the market drivers, restrains and growth of the Cleanroom Technology In Healthcare Market

Cleanroom Technology In Healthcare Market Report Highlights

• The market is projected to witness significant growth by 2030, owing to the rapidly increasing incidence of healthcare-acquired Infections (HAIs)

• In terms of product, the consumables segment dominated the market in 2022 owing to growing advancements in pharmaceutical cleanroom technology, both in terms of technicality and regulations

• In terms of end use, the pharmaceutical industry segment dominated the market in 2022. The growth is due to stringent regulations regarding the approval of pharmaceutical products, which has increased demand for cleanroom technology

• North America dominated the market for cleanroom technology and accounted for the largest revenue share in 2022. This can be attributed to the proper healthcare infrastructure in the region and the local presence of key pharmaceutical players

Cleanroom Technology In Healthcare Market Segmentation

Grand View Research has segmented the cleanroom technology in healthcare market based on product, end use, and region

Cleanroom Technology In Healthcare Product Outlook (Revenue, USD Million, 2018 - 2030)

• Equipment

o Heating Ventilation And Air Conditioning System (HVAC)

o Cleanroom Air Filters

o Air Shower And Diffuser

o Laminar Air Flow Unit

o Others

• Consumables

o Gloves

o Wipes

o Disinfectants

o Apparels

o Cleaning Products

Cleanroom Technology In Healthcare End Use Outlook (Revenue, USD Million, 2018 - 2030)

• Pharmaceutical Industry

• Medical Device Industry

• Biotechnology Industry

• Hospitals And Diagnostic Centers

Cleanroom Technology In Healthcare Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

o Sweden

o Norway

o Denmark

• Asia Pacific

o Japan

o China

o India

o Australia

o Thailand

o South Korea

• Latin America

o Brazil

o Mexico

o Argentina

• MEA

o South Africa

o Saudi Arabia

o UAE

o Kuwait

Order a free sample PDF of the Cleanroom Technology In Healthcare Market Intelligence Study, published by Grand View Research.

#Cleanroom Technology In Healthcare Market#Cleanroom Technology In Healthcare Market Size#Cleanroom Technology In Healthcare Market Share#Cleanroom Technology In Healthcare Market Analysis#Cleanroom Technology In Healthcare Market Growth

0 notes

Text

Automotive Heat Shields Market Trends, Innovations, and Future Outlook to 2030

The Automotive Heat Shields market is expected to grow from USD 12.67 Billion in 2024 to USD 16.31 Billion by 2030, at a CAGR of 4.30% during the forecast period.

The automotive heat shields market has emerged as a critical component of the global automotive industry, driven by the increasing demand for enhanced vehicle performance, efficiency, and safety. Automotive heat shields are designed to protect various components of a vehicle from excessive heat generated by the engine, exhaust systems, and other high-temperature areas. These shields play a vital role in improving the longevity of automotive parts, reducing heat-related wear and tear, and ensuring optimal performance.

One of the key factors contributing to the growth of the automotive heat shields market is the rising emphasis on lightweight materials in vehicle manufacturing. With stringent regulations aimed at reducing carbon emissions and improving fuel efficiency, automakers are incorporating lightweight heat shields made of advanced materials such as aluminum, composites, and multi-layered insulating fabrics. These materials not only reduce the overall weight of the vehicle but also enhance thermal management capabilities.

For More Insights into the Market, Request a Sample of this Report https://www.reportprime.com/enquiry/sample-report/19917

The increasing adoption of electric and hybrid vehicles (EVs and HEVs) has further accelerated the demand for automotive heat shields. EVs and HEVs generate significant heat from their batteries and powertrain systems, necessitating efficient heat shielding solutions to maintain safety and performance. Manufacturers are focusing on developing innovative heat shields tailored to the unique requirements of these vehicles, contributing to market expansion.

Regional dynamics play a crucial role in shaping the automotive heat shields market. In developed regions such as North America and Europe, the market is driven by the presence of leading automakers, advanced manufacturing capabilities, and stringent regulatory frameworks. Meanwhile, the Asia-Pacific region is witnessing rapid growth due to increasing vehicle production, rising disposable incomes, and the growing popularity of electric mobility in countries like China, Japan, and India.

Market Segmentations

By Type: Rigid Heat Shield, Flexible Heat Shield, Textile Heat Shield

By Applications: Passenger Vehicle, Light Commercial Vehicle

Get Full Access of This Premium Report https://www.reportprime.com/checkout?id=19917&price=3590

The competitive landscape of the automotive heat shields market is characterized by continuous innovation and strategic collaborations. Major players such as Dana Incorporated, ElringKlinger AG, Tenneco Inc., Lydall, Inc., and Autoneum are investing heavily in research and development to introduce advanced heat shield solutions. These companies are also expanding their manufacturing capacities and forging partnerships with automakers to strengthen their market position.

Despite the promising growth prospects, the automotive heat shields market faces several challenges. The fluctuating prices of raw materials and the high cost of advanced heat shielding technologies can impact profitability for manufacturers. Additionally, the complexity of designing heat shields for modern vehicles with compact engine compartments and intricate powertrains presents a technical challenge.

The future of the automotive heat shields market is promising, with numerous opportunities on the horizon. The global shift toward electric and autonomous vehicles is expected to drive innovation in heat shielding technologies. Furthermore, the integration of smart heat shields equipped with sensors and data-monitoring capabilities is anticipated to become a key trend, enhancing the efficiency and safety of next-generation vehicles.

0 notes

Text

Tin-Plated Copper Busbar Market: Trends, Growth Drivers, and Future Outlook

The tin-plated copper busbar market has emerged as a vital component in power distribution systems, owing to its superior conductivity, corrosion resistance, and reliability. With the growing demand for efficient power distribution in industries such as automotive, energy, and electronics, the market for tin-plated copper busbars is witnessing significant growth. This blog provides an in-depth analysis of the tin-plated copper busbar market, exploring key trends, drivers, challenges, and opportunities.

Market Overview

Tin-plated copper busbars are widely used in electrical power distribution systems to enhance conductivity and prevent oxidation. The global tin-plated copper busbar market size was valued at approximately $2.1 billion in 2023 and is projected to reach $3.5 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.5% during the forecast period.

Key Market Drivers:

Increasing Energy Demand: The rising need for efficient power distribution in residential, commercial, and industrial sectors drives the demand for tin-plated copper busbars.

Growth in Renewable Energy Projects: The adoption of renewable energy sources such as solar and wind power has created a surge in demand for durable and efficient electrical components.

Advancements in Electric Vehicles (EVs): The growing EV market relies heavily on high-quality electrical components, boosting demand for tin-plated copper busbars.

Corrosion Resistance: Tin plating provides enhanced corrosion resistance, ensuring long-term reliability and reduced maintenance.

Industrial Automation: Increasing adoption of automation and robotics in industries requires robust electrical systems, further driving the market.

Market Segmentation

The tin-plated copper busbar market can be segmented by material type, application, end-user industry, and region.

By Material Type:

Solid Copper Busbars: Commonly used for high-current applications.

Laminated Copper Busbars: Offer improved performance and heat dissipation.

By Application:

Power Distribution: Widely used in substations and switchgear.

Panel Boards: Essential for electrical distribution systems in buildings.

Battery Connections: Critical in EVs and energy storage systems.

Industrial Equipment: Supports heavy machinery and automation systems.

By End-User Industry:

Automotive: Increasing adoption in EV battery systems and charging infrastructure.

Energy and Utilities: Significant demand from renewable energy projects and power grids.

Industrial Manufacturing: Essential in automation and high-power equipment.

Electronics: Used in consumer electronics and telecommunications.

By Region:

North America: A mature market with significant adoption in energy and automotive sectors.

Europe: Driven by stringent regulations and renewable energy initiatives.

Asia-Pacific: The fastest-growing region, fueled by industrialization and EV adoption.

Middle East & Africa: Emerging markets with growing infrastructure investments.

Latin America: Increasing focus on renewable energy projects and industrial development.

Key Trends

Shift Towards Renewable Energy: Rising investments in solar and wind energy are increasing demand for robust electrical components.

Lightweight and Compact Designs: Manufacturers are focusing on developing compact busbars to optimize space and weight.

Sustainability Initiatives: Growing emphasis on eco-friendly and recyclable materials in busbar manufacturing.

Integration with Smart Grids: Advancements in smart grid technology are boosting the demand for innovative power distribution components.

Customization and Modular Solutions: Increased demand for tailored busbar solutions to meet specific industry requirements.

Challenges

High Material Costs: Fluctuating prices of copper and tin can impact manufacturing costs.

Competition from Alternatives: Aluminum busbars, though less efficient, are gaining traction due to lower costs.

Technical Limitations: Challenges in managing high-power density applications with existing designs.

Complex Manufacturing Processes: Precision requirements in tin plating and fabrication add to production complexities.

Competitive Landscape

The tin-plated copper busbar market is highly competitive, with key players focusing on innovation, sustainability, and strategic partnerships. Major players include:

Schneider Electric SE

Siemens AG

ABB Ltd.

Eaton Corporation

Rogers Corporation

Legrand SA

Mersen

Future Outlook

The tin-plated copper busbar market is poised for steady growth, driven by advancements in power distribution systems, renewable energy projects, and the expanding EV market. Emerging technologies and increasing focus on sustainability will further accelerate market expansion.

Key Opportunities:

Expansion in Emerging Markets: Infrastructure development in Asia-Pacific, Africa, and Latin America presents significant growth opportunities.

Focus on EV Infrastructure: Growing investments in EV charging stations will drive demand for busbars.

Innovation in Materials and Design: Development of high-performance and lightweight busbars to cater to advanced applications.

Government Initiatives: Supportive policies for renewable energy and industrial automation will fuel market growth.

Conclusion

The tin-plated copper busbar market is a critical enabler of efficient and reliable power distribution in various industries. By leveraging advancements in technology and addressing challenges such as material costs and competition, stakeholders can capitalize on the vast opportunities in this growing market. As the world transitions to a more sustainable energy future, tin-plated copper busbars will remain a key component of the global power infrastructure.

0 notes

Text

Global Polytetrafluoroethylene (PTFE) Market Report: Projected Growth and Key Insights

Global Polytetrafluoroethylene (PTFE) Market Report: Projected Growth and Key Insights

Straits Research is pleased to announce the release of its comprehensive report on the global Polytetrafluoroethylene (PTFE) market. The global polytetrafluoroethylene (PTFE) market was valued at USD 2.54 Billion in 2024. It is expected to reach USD 2.66 Billion in 2025 to USD 3.87 Billion in 2033, growing at a CAGR of 4.8% over the forecast period (2025-2033).

Industry Overview

Polytetrafluoroethylene (PTFE), commonly known as Teflon, is a synthetic fluoropolymer known for its high resistance to heat and chemical reactions. Its unique properties make it an essential material in various applications, including automotive components, electrical insulation, and non-stick cookware. As industries increasingly seek durable and efficient materials, the demand for PTFE continues to rise.

Key Drivers in the PTFE Market

The growth of the PTFE market is driven by several factors:

Increasing Demand in Automotive and Aerospace Industries: The automotive sector's need for high-performance materials that can withstand extreme conditions is propelling PTFE adoption in gaskets, seals, and bearings.

Growth in Chemical Processing: PTFE’s exceptional chemical resistance makes it indispensable for lining vessels and piping in chemical processing applications.

Healthcare Applications: The healthcare industry’s growing reliance on PTFE for medical devices and equipment is contributing to market expansion.

Consumer Products: The popularity of non-stick cookware continues to drive demand for PTFE coatings.

Request a Sample Report of Polytetrafluoroethylene (PTFE) Market

Key Developments in the PTFE Market

Recent developments indicate a dynamic shift within the PTFE market:

Technological Innovations: Advancements in manufacturing processes are enhancing the efficiency and safety of PTFE production.

Sustainability Initiatives: Manufacturers are increasingly focusing on developing eco-friendly alternatives to traditional PTFE products.

Rising Competition: The market is witnessing intense competition from manufacturers aiming to capture larger market shares through innovation and cost-effective solutions.

Market Segmentation Analysis

The global PTFE market can be segmented into various categories:

By Form:

Granular

Fine Powder

Dispersion

By Applications:

Sheets

Coatings

Pipes

Films

Others

By End-User Industry:

Automotive and Transportation

Chemical and Industrial Processing

Healthcare

Construction

Cookware

Electrical and Electronics

Others

Buy Polytetrafluoroethylene (PTFE) Market Report here!

Regional Trends

The PTFE market exhibits diverse trends across different regions:

North America:

The United States remains a significant player due to its robust automotive and aerospace industries. The demand for high-performance materials is driving growth in this region.

Asia-Pacific (APAC):

Dominated by countries like China and Japan, this region is experiencing rapid industrialization. China’s extensive use of PTFE in electronics and automotive applications significantly contributes to market growth.

Europe:

Countries such as Germany and France are leading the European market due to increasing requirements for improved materials in industries like chemical processing and electrical engineering.

Latin America, Middle East, and Africa (LAMEA):

This region is gradually adopting PTFE products, driven by infrastructure development and rising industrial activities.

Top Players in the PTFE Market

Straits Research identifies several key players driving innovation within the PTFE market:

AGC Inc.

BEMU Fluorkunststoffe GmbH

Aidmer (JiangXi Aidmer Seal & Packing Co. Ltd)

Daikin Industries Ltd.

Gujarat Fluorochemicals Limited

Dyneon GmbH & Co. KG (3M)

HaloPolymer

Freudenberg FST GmbH

Jiangsu Meilan Chemical Co. Ltd.

These companies are actively investing in research and development to enhance product offerings and meet evolving customer demands.

Conclusion

The global Polytetrafluoroethylene (PTFE) market is poised for steady growth driven by increasing demand across various industries, particularly automotive, healthcare, and consumer products. As stakeholders navigate this evolving landscape, opportunities abound for innovation and collaboration aimed at enhancing the efficiency and sustainability of PTFE applications.For more detailed insights into the Polytetrafluoroethylene (PTFE) Market trends and forecasts, please refer to our full report or contact Straits Research directly.

Browse Full Report and TOC of Polytetrafluoroethylene (PTFE) Market

About Straits Research

Straits Research is a premier provider of business intelligence specializing in research, analytics, and advisory services aimed at delivering comprehensive insights through detailed reports. For further information or inquiries regarding this press release or our research services, please contact us at [email protected] or call +1 646 905 0080.

Contact:

Straits Research Email: [email protected] Phone: +1 646 905 0080 Address: 825 3rd Avenue, New York, NY, USA, 10022

#Polytetrafluoroethylene (PTFE) Market Share#Polytetrafluoroethylene (PTFE) Market Size#Polytetrafluoroethylene (PTFE) Market Growth#Polytetrafluoroethylene (PTFE) Market Insights#Polytetrafluoroethylene (PTFE) Market Trends#Polytetrafluoroethylene (PTFE) Market Analysis#Polytetrafluoroethylene (PTFE) Market Industry#Polytetrafluoroethylene (PTFE) Market Forecast

0 notes

Text

Ballistic Composites Market

Ballistic Composites Market Size, Share, Trends: DuPont de Nemours, Inc. Leads

Growing Demand for Lightweight and High-Performance Protection Drives Market Forward

Market Overview:

The Ballistic Composites Market is projected to grow significantly from 2024 to 2031. North America is anticipated to be the dominant region in this market. Key metrics include increasing defense spending, growing demand for lightweight armor solutions, and rising concerns over personnel safety in law enforcement and military applications. The market for ballistic composites is growing steadily, driven by continuous military modernization programs, an increase in armed conflicts and terrorist activities, and advances in composite materials technology. These materials are becoming increasingly popular due to their high strength-to-weight ratio, good impact resistance, and ability to provide enhanced protection against ballistic threats.

DOWNLOAD FREE SAMPLE

Market Trends:

The ballistic composites market is seeing a substantial shift towards the development of lighter, more flexible protective systems. This move is motivated by the need for increased mobility and comfort for workers in the defense and law enforcement sectors, without sacrificing ballistic protection. Manufacturers are working to create innovative composite materials that provide higher protection while decreasing the total weight of armor systems. Recent advancements include the use of nanomaterials and hybrid composites to improve ballistic performance. For example, graphene-enhanced composites show potential for increasing the strength and flexibility of body armor. There is also a rising emphasis on developing multi-threat armor solutions that can withstand both ballistic and stabbing threats, particularly for law enforcement applications.

Market Segmentation:

The Aramid Fibers segment is expected to dominate the Ballistic Composites Market. This dominance can be attributed to aramid fibers' excellent strength-to-weight ratio, high tensile strength, and superior heat resistance, making them suitable for a wide range of ballistic protection applications. Aramid fibers, such as Kevlar® (DuPont) and Twaron® (Teijin), have been widely utilized in ballistic protection for decades and remain the preferred material for many armor applications. These fibers provide a unique mix of high strength, low weight, and flexibility, which is essential for personal protection equipment and vehicle armor systems. The automotive and aerospace sectors are also major consumers of aramid-based ballistic composites for armoured vehicles and aircraft protection systems.

Market Key Players:

Prominent players in the Ballistic Composites Market include DuPont de Nemours, Inc., Teijin Limited, Koninklijke DSM N.V., Honeywell International Inc., BAE Systems plc, Gurit Holding AG, Morgan Advanced Materials plc, Southern States LLC, Barrday Corporation, and PRF Composite Materials. These companies are at the forefront of the industry, continuously innovating and expanding their product portfolios to meet the evolving market demands. Their strategic initiatives and robust distribution networks have enabled them to maintain a strong market presence and drive growth.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Building Automation Market

Building Automation Market Size, Share, Trends: Siemens AG Leads

Integration of AI and Machine Learning in Building Management Systems

Market Overview:

The Building Automation Market is projected to grow at a CAGR of 10.7% from 2024 to 2031. The market value is expected to increase from XX USD in 2024 to YY USD by 2031.

North America is anticipated to be the dominant region in this market. Key metrics include increasing adoption of IoT in building management, rising demand for energy-efficient buildings, and growing investments in smart city projects.

The building automation sector is quickly growing, driven by a greater emphasis on energy saving, the introduction of smart buildings, and the incorporation of modern technology such as artificial intelligence and the Internet of Things (IoT). The industry is seeing increased demand from the commercial, residential, and industrial sectors as they seek to reduce operating costs, improve occupant comfort, and enhance overall building efficiency.

DOWNLOAD FREE SAMPLE

Market Trends:

The integration of artificial intelligence (AI) and machine learning (ML) into building automation systems is revolutionising the industry. This advancement dramatically expands the possibilities of building management systems, allowing for better maintenance forecasting, energy efficiency, and occupant comfort. AI-powered building automation systems can analyse vast amounts of data from several sensors and devices in real time to make smart decisions about lighting, heating, cooling, and security. For example, these technologies can predict equipment malfunctions, reducing downtime and maintenance costs. They may also identify occupancy trends and adjust building systems accordingly, resulting in significant energy savings. As AI and machine learning technologies advance, their integration with building automation systems is anticipated to become more complicated, resulting in even greater efficiency and personalisation in building management.

Market Segmentation:

The HVAC (Heating, Ventilation, and Air Conditioning) category is predicted to hold the largest market share in the building automation industry. This dominance can be attributed to the critical role HVAC systems play in maintaining interior environmental quality, as well as their significant impact on building energy consumption. Building automation systems for HVAC deliver significant energy savings and better occupant comfort, thus they are a major priority for building owners and managers.

Recent advancements in HVAC automation technology have reinforced this segment's leadership position. For example, the introduction of AI-powered HVAC management systems has enabled more precise temperature and air quality monitoring, resulting in energy savings of up to 20-30% over traditional systems. According to studies conducted by the American Council for an Energy-Efficient Economy (ACEEE), efficient HVAC controls can reduce energy usage in commercial buildings by an average of 13%.

Market Key Players:

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

Schneider Electric SE

Carrier Global Corporation

Robert Bosch GmbH

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

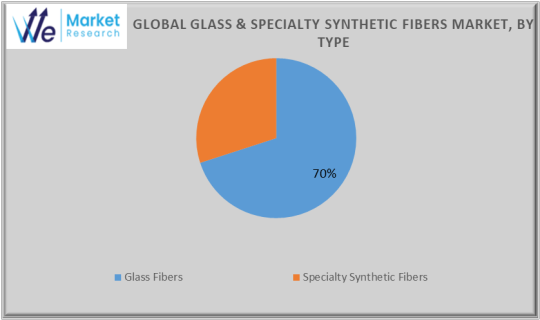

Glass Fibers & Specialty Synthetic Fibers Market Challenges, Analysis and Forecast to 2034

The Glass Fibers & Specialty Synthetic Fibers Market is a dynamic segment within the materials industry, driven by the increasing demand for lightweight, durable, and high-performance materials across various sectors. These fibers are engineered for applications that require superior mechanical properties, thermal stability, and resistance to environmental factors

The market for glass fiber and specialty synthetic fibers is expected to increase at a compound annual growth rate (CAGR) of 6.4% between 2024 and 2034. According to an average growth trend, the market is expected to reach USD 144.58 billion in 2034. The global market for glass fibers and specialty synthetic fibers is expected to generate USD 85.59 billion by 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/glass-and-specialty-synthetic-fibers-market/1603

Glass Fibers & Specialty Synthetic Fibers Market Growth Drivers

Urbanization and Infrastructure Growth:

Increasing investments in construction and urban development drive demand for glass fibers.

Rising Defense Budgets:

Governments worldwide are increasing investments in protective equipment using synthetic fibers.

Shift Toward Renewable Energy:

Wind energy projects favor glass fibers for turbine blades.

Advancements in Material Engineering:

Innovations are improving the properties and reducing production costs of synthetic fibers.

Specialty Synthetic Fibers: Types

Aramid Fibers:

Examples: Kevlar, Twaron.

High tensile strength and resistance to impact and heat.

Used in bulletproof vests, fire-resistant clothing, and ropes.

Carbon Fibers:

Lightweight and exceptionally strong.

Applications: Aerospace, sports equipment, automotive (luxury cars).

Ultra-High-Molecular-Weight Polyethylene (UHMWPE):

Examples: Dyneema, Spectra.

Extremely lightweight with high impact resistance.

Used in personal armor, fishing lines, and medical implants.

Polybenzimidazole (PBI):

High thermal and chemical stability.

Used in firefighting gear and aerospace insulation.

Polyimide Fibers:

Heat-resistant fibers ideal for use in high-temperature industrial applications.

Glass Fibers & Specialty Synthetic Fibers Market Challenges

High Costs of Specialty Fibers:

The manufacturing process for carbon and aramid fibers is resource-intensive.

Environmental Impact:

Synthetic fibers contribute to pollution if not recycled properly.

Competition from Emerging Materials:

Natural fibers like hemp and bamboo, as well as metal composites, are gaining attention.

Emerging Trends

Integration with Smart Technologies:

Development of fibers with embedded sensors for structural health monitoring.

Circular Economy Initiatives:

Companies are investing in recycling technologies for glass and synthetic fibers.

Hybrid Materials:

Combining glass and synthetic fibers to create composites with enhanced properties.

Glass Fibers & Specialty Synthetic Fibers Market Segmentation,

By Type

Glass Fibers

E-Glass

S-Glass

C-Glass

Others

Specialty Synthetic Fibers