#Extended-Release Drugs Market size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

If you dial 1-866-584-6757, you can leave an audio post for your followers.

Text

Morphine Market Product Development Strategies by Prominent Players, 2032

Morphine is a powerful analgesic and one of the most widely used medications for managing severe pain, particularly in cases of post-surgical recovery, chronic pain, and cancer. As an opioid, morphine works by binding to opioid receptors in the brain, blocking pain signals and providing relief that allows patients to regain comfort and functionality. While it is highly effective, morphine requires careful administration to avoid dependency and adverse effects, making safe and controlled use essential for effective pain management.

The Morphine Market Size was valued at USD 20.03 billion in 2023 and is expected to reach USD 32.81 billion by 2032 and grow at a CAGR of 5.66% over the forecast period 2024-2032.

Future Scope

The future of morphine use is shaped by the development of safer, controlled-release formulations and novel drug delivery systems aimed at reducing the risk of addiction and side effects. Research is focused on creating abuse-deterrent formulations (ADFs) that prevent misuse, and extended-release versions that offer long-lasting relief with lower doses. Additionally, advancements in personalized medicine may provide dosing regimens tailored to individual patient profiles, offering safer, more effective pain management.

Trends

Current trends in morphine administration include the rise of patient-controlled analgesia (PCA) systems, which allow patients to manage their pain relief within safe limits, and the development of transdermal patches for non-invasive, continuous delivery. Furthermore, abuse-deterrent technologies and combination therapies with non-opioid analgesics are being adopted to minimize morphine dependency. These trends aim to enhance the safety, efficiency, and patient autonomy in pain management practices.

Applications

Morphine is extensively used for managing acute and chronic pain in settings such as post-operative care, oncology, and palliative care. It is also employed in emergency medicine to treat severe injuries and trauma. In hospice care, morphine remains a vital component in alleviating pain and providing comfort to terminally ill patients. Given its efficacy in various healthcare settings, morphine continues to be an essential medication in the toolkit for pain management, tailored to specific patient needs and health conditions.

Key Points

Morphine is an effective analgesic for severe pain relief in post-surgery, chronic pain, and palliative care.

Innovations include controlled-release formulations and abuse-deterrent options to minimize risks.

Patient-controlled analgesia and transdermal patches are trending for safer, non-invasive administration.

Extensively applied in oncology, emergency medicine, and hospice care for tailored pain relief.

Morphine remains essential in managing pain but requires careful administration to prevent dependency.

Conclusion

Morphine remains a cornerstone in pain management due to its potent analgesic properties. As new formulations and delivery systems are developed, the administration of morphine is becoming safer and more tailored to patient needs. By advancing pain management techniques and improving patient control, morphine continues to offer essential relief, ensuring that patients receive effective care with minimized risks. The future of morphine use holds promise for enhancing patient safety and comfort, cementing its role in modern healthcare.

#Morphine Market#Morphine Market Size#Morphine Market Share#Morphine Market Growth#Morphine Market Report

0 notes

Text

Microencapsulation Market Global Outlook, Trends, and Forecast

The microencapsulation market size, valued at USD 15.38 billion in 2024, is projected to reach USD 24.07 billion by 2029, growing at a CAGR of 9.4% over the forecast period. With rising demand across pharmaceuticals, food, and personal care sectors, the market is transforming how products are designed and delivered for enhanced efficacy and consumer experience.

Pharmaceutical Innovations: Enhanced Drug Delivery and Patient Compliance

In the pharmaceutical industry, microencapsulation enables controlled drug delivery, allowing active ingredients to be released at specific times and locations within the body. This technology reduces potential side effects and improves patient adherence by enhancing treatment effectiveness. By encapsulating drugs in protective coatings, sensitive ingredients are shielded from degradation, preserving their potency until the moment they are needed within the body.

Unlock further insights—request your PDF copy!

Functional Foods: Catering to Health-Conscious Consumers

With health awareness on the rise, consumers are seeking more than just basic nutrition from their food. Functional foods fortified with essential nutrients like vitamins, minerals, and probiotics are gaining popularity, and microencapsulation plays a vital role in this trend. By protecting ingredients such as omega-3 fatty acids from oxidation, microencapsulation extends the shelf life of these functional foods, making them more accessible and reliable.

One example of this trend is the launch of Humiome B2 by DSM-firmenich in May 2024, the first biotic vitamin that uses Microbiome Targeted Technology™ to deliver vitamin B2 directly to the colon. This approach enhances bioavailability and supports gut health, showcasing how microencapsulation can promote holistic wellness through targeted nutrient delivery.

Asia Pacific: A Fast-Growing Market for Microencapsulation

APAC microencapsulation market is expected to lead the global market growth from 2024 to 2029, driven by an increasing demand for fortified food and beverages in countries like China, India, and Japan. As health awareness rises, so does the demand for improved nutrient stability and bioavailability, making microencapsulation essential in regional food and beverage markets. Furthermore, the pharmaceutical and cosmetics industries are thriving in Asia Pacific, fueling the demand for controlled release formulations and enhancing regional market growth.

Government incentives for local production, along with investments in innovation, are attracting major industry players to establish R&D and manufacturing facilities in the region. BASF SE, for example, expanded its Innovation Campus Shanghai in 2021, with a USD 296.8 million investment to drive research and collaboration, further advancing microencapsulation technologies.

Dripping Technology: Revolutionizing Encapsulation

The dripping method has gained momentum within the microencapsulation market due to its versatility in encapsulating a wide range of active ingredients, from flavors to nutrients and fragrances. This technique supports large-scale production and allows companies to meet demand in food, pharmaceutical, and personal care markets.

Recent advancements in dripping technology include the development of biodegradable components, fostering sustainable practices. These innovations respond to consumer demand for eco-friendly products and drive growth in industries where sustainability and efficacy are paramount.

The microencapsulation market growth is spurred by consumer demand for functional foods, innovative pharmaceutical applications, and personal care products. With advancements in encapsulation technologies like spray drying and coacervation, production has become more efficient and cost-effective, making microencapsulation accessible to a wider range of industries. As companies continue to innovate and expand into emerging markets, the microencapsulation industry is set to play a critical role in shaping the future of health-conscious and sustainable product development.

Key Microencapsulation Leaders

BASF (Germany)

FrieslandCampina (Netherlands)

DSM-firmenich (Switzerland)

Givaudan (Switzerland)

International Flavors & Fragrances Inc. (US)

Sensient Technologies Corporation (US)

Microencapsulation Industry Trends

· Rise in Functional Foods: Demand for health-focused foods drives microencapsulation for vitamins and probiotics, enhancing stability and shelf life.

· Pharma Advancements: Controlled drug release and biodegradable polymers are boosting microencapsulation in pharmaceuticals for targeted delivery.

· Agricultural Applications: Precision agriculture benefits from encapsulated pesticides and fertilizers, offering controlled release and reduced environmental impact.

· Cosmetics Innovation: Microencapsulation in personal care products enables sustained release of fragrances and active ingredients, meeting consumer demand for longevity.

· New Materials & Nanocapsulation: Innovations in encapsulation materials and nanocapsulation techniques enhance absorption and stability, especially in food and pharma.

0 notes

Text

Regional Analysis of the Tablet Coating Market and Competitive Landscape

Tablet coating is a critical process in the pharmaceutical industry, primarily used to improve the stability, appearance, and efficacy of tablets. This process involves applying a layer of coating material onto the surface of a tablet core, which can serve various purposes, from masking unpleasant tastes and odors to controlling drug release rates and enhancing durability. Tablet coating materials include polymers, sugars, and colorants, which can be selected to suit the specific therapeutic needs of the medication. Advanced coating technologies have made it possible to create tablets with multiple functions, such as sustained-release, enteric coatings for delayed drug release, and protective layers to extend shelf life.

The tablet coating market size was projected at 8.82 (USD billion) in 2022 based on MRFR analysis. By 2032, the tablet coating market is projected to have grown from 9.45 billion USD in 2023 to 17.46 billion USD. During the forecast period (2024-2032), the tablet coating market's compound annual growth rate (CAGR) is anticipated to be approximately 7.06%.

Tablet Coating Analysis

Tablet Coating analysis shows that the demand for coated tablets is increasing across the pharmaceutical industry. This growth is driven by the benefits coating provides, such as improved patient adherence, especially for medications with bitter tastes. Additionally, coating helps to prevent tablet breakage and provides physical stability under various environmental conditions. Different coating techniques, such as sugar coating, film coating, and compression coating, have specific applications depending on the tablet’s intended use. An in-depth Tablet Coating analysis highlights a shift towards more sophisticated, multi-functional coatings that offer tailored release profiles and protect sensitive drug formulations. Innovations in coating materials and methods have also made production processes more efficient, helping manufacturers meet regulatory standards more easily.

Tablet Coating Market Trends

One of the main Tablet Coating market trends is the increased focus on functional and multi-layer coatings, which are engineered to release the active pharmaceutical ingredient (API) at targeted sites within the body. The rise of personalized medicine is also shaping market trends, as there is a need for coatings that cater to specific patient requirements, such as allergen-free or vegan coatings. Another significant trend in the Tablet Coating market is the adoption of aqueous coating processes as they reduce the use of organic solvents, making the process safer and more environmentally friendly. Additionally, advancements in coating machinery, including high-efficiency and automated systems, are enabling faster production and ensuring higher quality control.

Reasons to Buy the Reports

Detailed Market Insights: Comprehensive analysis of the Tablet Coating market, offering insights into current and emerging trends.

Competitive Analysis: In-depth evaluation of key players and their strategies, helping stakeholders understand competitive dynamics.

Technological Advancements: Information on innovative coating techniques and materials, essential for companies aiming to improve product performance.

Regulatory Information: Covers regulations affecting tablet coating processes, essential for compliance and quality assurance in pharmaceutical production.

Growth Forecasts: Offers projections on the future growth of the Tablet Coating market, aiding stakeholders in making informed investment decisions.

Recent Developments

Recent developments in the Tablet Coating market reflect ongoing efforts to enhance the quality and functionality of coated tablets. In 2023, several pharmaceutical companies announced the adoption of advanced coating techniques that improve the dissolution profiles of tablets, allowing for better-controlled release of APIs. Companies like BASF and Colorcon introduced eco-friendly coating solutions that eliminate the need for organic solvents, thereby reducing environmental impact. Additionally, new enteric coating materials have been developed to protect sensitive APIs from degradation in the stomach, ensuring they reach the intended site of absorption in the intestines. Automated tablet coating machines with advanced monitoring features have also been introduced to the market, helping to streamline the coating process and maintain high-quality standards. These advancements reflect the industry's commitment to innovation and the growing demand for versatile, high-performance tablet coating solutions.

Related reports:

pet sitting market

fungal keratitis treatment market

gastrointestinal stent market

gene therapy clinical trial service market

0 notes

Text

Atenolol Market 2024-2033 : Demand, Trend, Segmentation, Forecast, Overview And Top Companies

The atenolol global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Atenolol Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size -

The atenolol market size has grown strongly in recent years. It will grow from $11.05 billion in 2023 to $12.01 billion in 2024 at a compound annual growth rate (CAGR) of 8.7%. The growth in the historic period can be attributed to increased demand and consumption of antihypertensive drugs, increased patient pool of arrhythmia, and angina, increased prevalence of glaucoma, increased prevalence of arrhythmia, rise in online pharmacies.

The atenolol market size is expected to see strong growth in the next few years. It will grow to $15.85 billion in 2028 at a compound annual growth rate (CAGR) of 7.2%. The growth in the forecast period can be attributed to increasing demand for atenolol, growing prevalence of hypertension, surging awareness regarding hypertension complexities, significant rise in the aged population, poor lifestyle and dietary habits. Major trends in the forecast period include demand for beta blockers, demand for beta-1 selective blockers, recent regulatory approvals for new formulations, development of extended-release formulations, demand for combination therapies.

Order your report now for swift delivery @

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers -

The growing prevalence of cardiovascular diseases is expected to propel the growth of the atenolol market going forward. Cardiovascular diseases (CVDs) encompass a range of disorders affecting the heart and blood vessels. The growing prevalence of cardiovascular diseases is due to population growth and aging, risk factors, and lack of implementation of proven prevention and treatment strategies. Atenolol plays a crucial role in managing various cardiovascular diseases by reducing heart rate, lowering blood pressure, relieving angina symptoms, preventing heart attacks, and managing arrhythmias. It helps to stabilize heart function, control blood pressure, and prevent complications, contributing to better long-term cardiovascular health. For instance, in May 2022, according to the Centers for Disease Control and Prevention, a US-based governmental organization, the prevalence of coronary heart disease among adults aged 18 and over stood at 4.6% in 2020, experiencing a slight uptick to 4.9% in 2021. Therefore, the growing prevalence of cardiovascular diseases is driving the growth of the atenolol market.

The atenolol market covered in this report is segmented –

1) By Type: 98% Purity, 99% Purity

2) By Form: Tablets, IV Solution, Other Forms

3) By Distribution Channel: Hospital Pharmacies, Drug Stores, Online Pharmacies, Other Distribution Channels

4) By Application: Hypertension, Angina, Arrhythmia, Other Applications

Get an inside scoop of the atenolol market, Request now for Sample Report @

Regional Insights -

North America was the largest region in the atenolol market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the atenolol market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies -

Major companies operating in the atenolol market are <b>F. Hoffmann-La Roche Ltd., AstraZeneca Plc, Abbott Laboratories Inc., Shanghai Pharmaceuticals Holding Co. Ltd., LGM Pharma, Torrent Pharmaceuticals GmbH, Cipla Inc., Intas Pharmaceuticals Limited, Lupin Limited, Macleods Pharmaceuticals Ltd., Ipca Laboratories Limited, Aristo Pharmaceuticals Pvt. Ltd, Medley Pharmaceuticals Ltd., Micro Labs Ltd., Unichem Laboratories Limited, Harman Finochem Ltd., Axplora, Erregierre SpA, Darou Pakhsh Pharma Chem Co., Zydus Pharmaceuticals (USA) Inc., Anant Pharmaceuticals Pvt. Ltd., Enomark LLC, Hairui Chemical, Octavius Pharma Pvt. Ltd., Hoventa Pharma</b>

Table of Contents

1. Executive Summary

2. Atenolol Market Report Structure

3. Atenolol Market Trends And Strategies

4. Atenolol Market – Macro Economic Scenario

5. Atenolol Market Size And Growth

…..

27. Atenolol Market Competitor Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Wear Your Vitamins: The Rise of Wellness Patches for Optimal Living

In today’s fast-paced world, wellness patches are becoming a go-to solution for individuals seeking an easy and effective way to enhance their health. Wellness patches provide a convenient method for delivering vitamins and nutrients directly through the skin, allowing for a more efficient absorption than traditional oral supplements. The rising popularity of wellness patches can be attributed to their ease of use, flexibility, and targeted delivery of essential nutrients, making them an attractive option for those looking to optimize their health. Whether it’s boosting energy levels, improving sleep quality, or supporting immune function, wellness patches cater to a wide array of health needs. The convenience of applying a patch and going about your day has made wellness patches an increasingly popular choice among wellness enthusiasts and health-conscious individuals alike.

Understanding Wellness Patches

Wellness patches are transdermal patches that release vitamins, minerals, and other beneficial compounds into the bloodstream through the skin. This method bypasses the digestive system, which can sometimes reduce the efficacy of oral supplements due to factors like absorption issues or digestive problems. Each patch is designed to deliver a specific set of nutrients that target various aspects of health, such as energy levels, mental clarity, and stress reduction.

These patches come in various formulations, catering to diverse health goals. Some may contain a blend of B vitamins for energy, while others might focus on ingredients like melatonin for better sleep. The versatility of wellness patches makes them appealing to a broad audience, as individuals can choose patches that align with their specific health objectives.

The Benefits of Using Wellness Patches

One of the most significant advantages of wellness patches is their ease of use. Unlike traditional supplements, which often require precise dosing and timing, patches can be applied once and left to work for an extended period. Many patches are designed for 24-hour wear, providing a steady release of nutrients without the need for frequent dosing.

Additionally, wellness patches are discreet and convenient. They can be worn under clothing, making them suitable for individuals with busy lifestyles who may struggle to remember to take multiple supplements throughout the day. This convenience factor contributes to better adherence to wellness routines, ensuring that users receive the benefits of their chosen nutrients consistently.

Furthermore, the targeted delivery of wellness patches can lead to enhanced bioavailability of the vitamins and minerals they contain. Studies suggest that transdermal delivery can result in higher concentrations of active ingredients in the bloodstream compared to oral consumption, leading to potentially more significant health benefits.

The Science Behind Wellness Patches

The effectiveness of wellness patches lies in the science of transdermal drug delivery. These patches typically consist of a backing layer, an adhesive layer, and a drug reservoir that contains the active ingredients. When applied to the skin, the warmth of the body helps activate the ingredients, allowing them to penetrate the skin barrier and enter the bloodstream.

Various factors influence the absorption rate of wellness patches, including the thickness of the skin, the type of formulation used, and the size of the molecules being delivered. Many manufacturers conduct extensive research and testing to optimize their formulations, ensuring that their wellness patches are not only effective but also safe for long-term use.

Choosing the Right Wellness Patch

With the growing market for wellness patches, it’s essential for consumers to choose high-quality products that meet their health needs. When selecting a patch, look for reputable brands that provide transparent ingredient lists and third-party testing to ensure product safety and efficacy. Additionally, consider your specific health goals—whether you want to enhance energy levels, improve mood, or support overall wellness—and choose a patch that aligns with these objectives.

Moreover, it’s advisable to consult with a healthcare professional before starting any new wellness routine, especially if you have underlying health conditions or are taking medications. A professional can help you navigate the myriad of options available and determine which wellness patches are best suited to your individual needs.

The Future of Wellness Patches

As the wellness industry continues to evolve, wellness patches are likely to gain even more traction. The integration of technology into health products is already on the rise, and we can expect to see more innovative patches that offer real-time monitoring of nutrient levels, personalized formulations based on individual health data, and enhanced delivery mechanisms.

The potential for customization and innovation positions wellness patches as a significant player in the future of health and wellness. As people seek more accessible and effective methods to manage their health, the demand for these patches will undoubtedly increase, offering new opportunities for both consumers and manufacturers alike.

Conclusion

In summary, the rise of wellness patches marks a new era in health optimization. With their ability to deliver essential nutrients conveniently and effectively, these patches are transforming how individuals approach their wellness routines. By choosing high-quality wellness patches tailored to their specific health goals, users can enhance their overall well-being and embrace a healthier lifestyle. As the popularity of wellness patches continues to grow, they are poised to become a staple in the wellness industry, helping people achieve optimal living effortlessly.

1 note

·

View note

Text

Phospholipids & Lecithin Market : Opportunities, Application and Forecast 2030

Phospholipids and Lecithin to Reach USD 9.66 Billion by 2030, Growing at a CAGR of 6.9%

Global Phospholipids and Lecithin Size, Share, and Forecast Report 2023-2030

Introduction

The Phospholipids & Lecithin Market Size is experiencing significant growth, driven by its expanding use in industries such as food and beverages, pharmaceuticals, animal feed, and cosmetics. Valued at USD 5.66 billion in 2022, the is expected to grow at a compound annual growth rate (CAGR) of 6.9%, reaching USD 9.66 billion by 2030. Phospholipids and lecithin, naturally occurring fatty substances, are widely recognized for their emulsifying properties and essential roles in cellular function, making them indispensable in a variety of applications.

This press release delves into the key drivers, emerging trends, detailed segmentation, and regional analysis of the phospholipids and lecithin as it continues to expand globally.

Drivers and Growth Factors

Several factors are fueling the growth of the global phospholipids and lecithin :

Rising Demand for Natural Emulsifiers in the Food Industry: Phospholipids and lecithin are commonly used as emulsifiers in food products such as chocolate, margarine, and processed foods. The increasing demand for natural ingredients in food and beverages is driving the adoption of lecithin, which is derived from sources such as soy, sunflower, and rapeseed. Its ability to improve texture, extend shelf life, and enhance the stability of food products makes it a valuable ingredient in the food industry.

Growth in Nutraceuticals and Functional Foods: With growing consumer awareness of health and wellness, the demand for nutraceuticals and functional foods is increasing. Phospholipids, known for their role in promoting brain health, cardiovascular wellness, and liver function, are being incorporated into dietary supplements and functional food products. This trend is expected to drive growth over the forecast period.

Expanding Pharmaceutical and Healthcare Applications: Phospholipids are widely used in the pharmaceutical industry for drug delivery systems, particularly in liposomal formulations and encapsulation technologies. Their ability to enhance the bioavailability of active ingredients makes them an essential component in modern pharmaceuticals. As the healthcare sector grows and focuses on innovative drug delivery solutions, the demand for phospholipids is expected to rise.

Growing Use in Cosmetics and Personal Care Products: Lecithin and phospholipids are gaining popularity in the cosmetics industry due to their moisturizing and emollient properties. They are increasingly used in skincare products, haircare formulations, and makeup, providing hydration and improving texture. The trend toward natural and organic cosmetics is further boosting the demand for lecithin and phospholipids in personal care products.

Sustainability and Consumer Preference for Plant-based Ingredients: As consumers shift toward plant-based and sustainable products, lecithin derived from sources such as soy, sunflower, and rapeseed is in high demand. Plant-based lecithin is widely used as a vegan-friendly alternative to egg-based lecithin, catering to the preferences of health-conscious and environmentally aware consumers.

Segmentation

The global phospholipids and lecithin can be segmented by source, type, application, nature, and region.

By Source:

Soy: Soy lecithin is the most commonly used source due to its cost-effectiveness and widespread availability. It is used across various industries, including food, feed, and pharmaceuticals.

Sunflower: Sunflower lecithin is gaining popularity as a non-GMO and allergen-free alternative to soy lecithin. It is preferred by manufacturers producing clean-label and allergen-free products.

Rapeseed: Rapeseed lecithin is valued for its natural emulsifying properties and is increasingly used in food and industrial applications.

Egg: Egg-derived lecithin is primarily used in high-end food products and pharmaceuticals. It is favored for its natural composition but faces competition from plant-based alternatives.

By Type:

Fluid Lecithin: Fluid lecithin is widely used in applications where easy dispersibility is required, such as in chocolate, margarine, and dairy products. It is also used in cosmetics and pharmaceuticals for its emulsifying properties.

De-oiled Lecithin: De-oiled lecithin, which is lecithin in powder form, is popular in applications requiring high-purity lecithin without any residual oils. It is used in baked goods, pharmaceuticals, and dietary supplements.

Modified Lecithin: Modified lecithin undergoes chemical or enzymatic treatment to enhance its functionality. It is used in specialized applications, including pharmaceuticals, cosmetics, and industrial uses.

By Application:

Feed: Lecithin is used in animal feed to improve feed efficiency, promote growth, and enhance the absorption of fat-soluble vitamins. It is particularly beneficial for poultry and livestock nutrition.

Food: In the food industry, lecithin serves as an emulsifier, stabilizer, and texturizer in products such as confectionery, baked goods, convenience foods, and margarine. It helps improve product consistency, extend shelf life, and enhance the sensory experience.

Confectionery Products: Lecithin is widely used in chocolate and candy manufacturing to improve texture and prevent ingredients from separating.

Convenience Food: The demand for ready-to-eat meals and convenience foods is driving the use of lecithin in processed food formulations.

Baked Goods: Lecithin improves dough handling, extends shelf life, and enhances the crumb structure of baked products.

Industrial: Lecithin and phospholipids are used in various industrial applications, including lubricants, coatings, and bio-based plastics. Their natural emulsifying and stabilizing properties make them ideal for use in industrial formulations.

Healthcare: The healthcare sector uses phospholipids in drug delivery systems, liposomal formulations, and supplements aimed at improving cognitive and cardiovascular health. Phospholipids also play a key role in cellular health and liver function.

By Nature:

Conventional: Conventional lecithin and phospholipids are widely used in large-scale industrial applications due to their cost-effectiveness and availability.

Organic: Organic lecithin is increasingly in demand in the food and personal care industries, particularly among consumers seeking clean-label and non-GMO products. Organic lecithin is derived from organically grown soy, sunflower, or rapeseed.

Regional Outlook

North America: North America holds a significant share of the global phospholipids and lecithin , driven by the growing demand for natural emulsifiers in the food and pharmaceutical industries. The U.S. and Canada are key s, with a focus on clean-label and plant-based products.

Europe: Europe is the second-largest for phospholipids and lecithin, with demand driven by the region’s strong food processing industry and increasing use of lecithin in functional foods and nutraceuticals. Countries like Germany, France, and the U.K. are leading the in this region.

Asia-Pacific: The Asia-Pacific region is expected to witness the fastest growth during the forecast period, driven by rising health consciousness, increasing demand for convenience foods, and expanding industrial applications in countries like China, India, and Japan.

Latin America and Middle East & Africa: These regions are emerging s for phospholipids and lecithin, with growing demand in the food and pharmaceutical sectors. Brazil and South Africa are key contributors to growth in these regions.

Trends Shaping the Future of the Phospholipids and Lecithin

Growing Demand for Clean-label Ingredients: As consumers become more conscious of the ingredients in their food, the demand for clean-label products is rising. Lecithin, particularly from non-GMO and organic sources, is increasingly sought after in the food and beverage industry.

Increased Use in Liposomal Drug Delivery: Phospholipids are gaining attention in the pharmaceutical industry for their use in liposomal drug delivery systems. These systems enhance the bioavailability and efficacy of active ingredients, driving demand for high-quality phospholipids.

Expansion of Plant-based and Vegan Products: The growing popularity of plant-based diets is driving the demand for lecithin derived from soy, sunflower, and rapeseed as alternatives to egg-based lecithin. This trend is particularly strong in the food and nutraceutical sectors.

Key Players

Several key players are driving growth in the global phospholipids and lecithin , including:

Cargill, Inc.

ADM (Archer Daniels Midland Company)

Lipoid GmbH

DuPont de Nemours, Inc.

Stern-Wywiol Gruppe GmbH & Co. KG

These companies are investing in product innovation, expanding their production capabilities, and focusing on sustainability to meet the growing demand for natural emulsifiers.

Conclusion

The global phospholipids and lecithin is on a path of significant growth, driven by increasing demand across food, pharmaceutical, and cosmetic industries.

Read More Details @ https://www.snsinsider.com/reports/phospholipids-and-lecithin-market-1317

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

SNS Insider Offering/ Consulting Services:

Go To Market Assessment Service

Total Addressable Market (TAM) Assessment

Competitive Benchmarking and Market Share Gain

0 notes

Text

The Olanzapine Market is projected to grow from USD 2625 million in 2024 to an estimated USD 3510.422 million by 2032, with a compound annual growth rate (CAGR) of 3.7% from 2024 to 2032.The global market for Olanzapine, a well-established antipsychotic medication primarily used in the treatment of mental health disorders like schizophrenia and bipolar disorder, has experienced significant growth in recent years. This article delves into the current market dynamics, growth prospects, key players, and factors influencing the Olanzapine market.

Browse the full report at https://www.credenceresearch.com/report/olanzapine-market

Overview of Olanzapine

Olanzapine belongs to a class of drugs called atypical antipsychotics. It is widely prescribed to manage conditions such as schizophrenia, where patients experience disturbed thinking, emotional instability, and hallucinations, and bipolar disorder, characterized by episodes of depression and mania. The drug works by affecting neurotransmitters in the brain, particularly serotonin and dopamine, to stabilize mood and thought processes.

Introduced by Eli Lilly and Company in the late 1990s under the brand name Zyprexa, Olanzapine has been available in generic forms since 2011. Its established efficacy, along with its side effect profile, including weight gain and metabolic changes, makes it a critical therapeutic option for healthcare providers in treating serious mental illnesses.

Market Drivers and Growth Opportunities

1. Rising Mental Health Awareness: One of the primary drivers of the Olanzapine market is the growing awareness of mental health issues globally. Over the past decade, there has been a significant shift in attitudes toward mental health, with increased advocacy and public health campaigns focusing on reducing stigma and encouraging treatment. This rising awareness is pushing healthcare systems to prioritize mental health, leading to increased demand for antipsychotic drugs like Olanzapine.

2. Prevalence of Schizophrenia and Bipolar Disorder: The prevalence of schizophrenia and bipolar disorder continues to increase. According to the World Health Organization (WHO), schizophrenia affects approximately 20 million people worldwide, while bipolar disorder impacts about 45 million people. With the rise in mental health diagnoses, the need for effective treatment options like Olanzapine is growing, which in turn, drives market expansion.

3. Technological Advancements in Drug Delivery: Recent technological advancements have introduced novel drug delivery methods, such as extended-release injections and orally disintegrating tablets (ODTs), enhancing patient adherence and convenience. These innovations are crucial for improving patient outcomes, especially for those who may struggle with daily oral medication adherence. The development of such formulations has further expanded the scope of Olanzapine’s market.

4. Growing Generic Competition: Since the expiration of Eli Lilly’s patent in 2011, generic versions of Olanzapine have flooded the market, making the drug more accessible and affordable. Generic manufacturers have contributed to market growth by increasing the drug’s availability in both developed and developing regions. The increased affordability of generics has expanded the patient base, particularly in low- and middle-income countries.

Market Challenges

1. Side Effects and Alternatives: One of the major challenges facing the Olanzapine market is its side effect profile. While highly effective, Olanzapine is associated with significant side effects, including weight gain, metabolic syndrome, and an increased risk of diabetes. These side effects can limit its long-term use, especially in patients with preexisting health conditions. This has opened the door for alternative antipsychotics with potentially fewer adverse effects, such as aripiprazole and risperidone, to gain market share.

2. Regulatory and Compliance Issues: Regulatory hurdles remain a critical challenge for drug manufacturers. The approval process for new formulations and generic versions of Olanzapine is rigorous and requires extensive clinical data to ensure safety and efficacy. Delays in regulatory approvals can slow down the entry of new generic versions into the market, impacting competition and pricing dynamics.

3. Patent Expirations and Price Erosion: The expiration of patents has resulted in increased generic competition, leading to price erosion in many regions. While this has improved access to Olanzapine, it has also put pressure on original manufacturers to maintain market share through innovation, strategic partnerships, and marketing efforts.

Regional Insights

The Olanzapine market shows varying growth patterns across different regions. North America, led by the U.S., remains the largest market for Olanzapine due to high prevalence rates of mental health disorders and a well-established healthcare infrastructure. Europe follows closely, with countries like Germany, France, and the U.K. accounting for significant demand due to the increasing focus on mental health treatment and the widespread availability of generics.

In contrast, the Asia-Pacific region is emerging as a fast-growing market due to rising awareness, expanding healthcare access, and increasing government initiatives to improve mental healthcare services. Countries like China and India are seeing rapid adoption of Olanzapine, driven by the growing burden of psychiatric disorders and improving healthcare infrastructure.

Key Players and Competitive Landscape

The Olanzapine market is highly competitive, with both branded and generic manufacturers vying for market share. Some of the leading companies in the Olanzapine market include:

- Eli Lilly and Company (the original manufacturer of Zyprexa) - Teva Pharmaceuticals - Mylan N.V. - Sun Pharmaceutical Industries Ltd. - Dr. Reddy's Laboratories

These companies are focusing on strategies such as product innovation, partnerships, mergers, and acquisitions to strengthen their market position. The rise of generic players, especially in developing regions, continues to shape the competitive landscape, forcing original manufacturers to adopt innovative approaches to maintain profitability.

Key Player Analysis:

AstraZeneca (U.K.)

Aurobindo Pharma (India)

Bristol-Myers Squibb Company (U.S.)

Cipla Inc (India)

Reddy’s Laboratories Ltd (India)

Endo International plc (Ireland)

Lupin (India)

Mylan N.V. (U.S.)

Novartis AG (Switzerland)

Pfizer Inc (U.S.)

Sun Pharmaceutical Industries Ltd (India)

Teva Pharmaceutical Industries Ltd (Israel)

Zydus Group (India)

Segmentation:

By Type

Monotherapy

Combinational therapy.

By Application

Schizophrenia,

Bipolar disorder,

By Indication

Schizophrenia,

Bipolar disorder,

Other indications.

By End User

Hospitals,

Homecare,

Specialty clinics,

By Region

North America

The U.S

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/olanzapine-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

신재생 나프타 시장 전망, 시장 동향 및 영향 분석(2024~2031)

신재생 나프타 시장 개요 및 보고서 적용 범위

재생 나프타 시장은 2022년 6억7460만 달러에서 2030년 1억73940만 달러로 급증할 것으로 전망되며, 예측 기간 동안 14.49%의 놀라운 CAGR을 기록할 것으로 예상됩니다. 이 보고서는 재생 나프타 산업 환경을 형성하는 시장 상황, 성장 동인, 과제 및 기회에 대해 설명합니다.

선도적인 재생 가능 나프타 산업 참가자

바이오매스와 유기성 폐기물에서 추출한 재생 가능한 나프타는 전통적인 석유 기반의 나프타에 대한 지속 가능한 대안입니다. UPM 바이오 연료, 네��테, 재생 가능 에너지 그룹과 같은 주요 업체들이 시장의 혁신과 확장을 주도하고 있습니다. 이 회사들은 기술 발전과 지속 가능한 관행을 통해 시장 성장에 크게 기여할 것으로 예상됩니다.

보고서의 샘플 PDF 가져오기

시장 세분화 2024-2031:

재생 가능 나프타 시장은 제품 유형에 따라 다음과 같이 분류됩니다:

라이트 나프타

헤비 나프타

제품 적용에 따라 시장은 다음과 같이 구분됩니다:

자동차용 플라스틱 부품

소비자 제품용 포장

지역별 재생 가능 나프타 시장 참가자:

북아메리카

유럽

아시아 태평양

라틴 아메리카

중동 및 아프리카

지역 내 신재생 나프타 시장의 성장:

재생 가능 나프타 시장은 환경에 대한 관심 증가와 지속 가능한 에너지원에 대한 수요 증가로 전 지역에 걸쳐 큰 폭의 성장이 예상됩니다. 아시아 태평양 지역에 이어 북미와 유럽 지역이 시장을 장악할 것으로 예상됩니다.

재생 가능 나프타 시장 역학(Drivers, Restraints, Opportunity, 과제)

재생 가능한 나프타 시장은 환경의 지속 가능성에 대한 인식을 높이고 재생 가능한 에너지원을 촉진하기 위한 정부의 노력에 의해 주로 추진됩니다. 그러나 규제 및 기술 제한과 같은 문제가 시장 성장을 방해할 수 있습니다. 재생 가능한 나프타 생산 효율성을 높이기 위한 지속적인 연구 개발 노력에 기회가 있습니다.

신재생 나프타 시장에 영향을 미치는 시장 동향

대체 연료 공급원에 대한 수요 증가

환경의 지속가능성에 대한 인식 제고

재생 가능 에너지원을 촉진하기 위한 정부 이니셔티브

이러한 트렌드는 혁신을 촉진하고 시장 기회를 확대하여 시장 성장을 견인할 것으로 예상됩니다.

이 보고서 구매

Browse more reports:

https://www.linkedin.com/pulse/unlocking-growth-potential-market-strategic-analysis-qy8te?trackingId=dXimzEwYRkeaTCG1wOp4Bw%3D%3D

https://www.linkedin.com/pulse/property-inspection-software-market-size-segmentation-trends-mafre?trackingId=2yRsqlphTLCPbMDo2e%2FnMQ%3D%3D

https://www.linkedin.com/pulse/vehicle-inspection-software-market-research-report-exploring-kuq7e?trackingId=jFRFeK5JT6OlnCRIZLNVMA%3D%3D

https://www.linkedin.com/pulse/extended-release-drug-market-overview-regional-outlook-competitive-wa3ee?trackingId=JigPGQ6YSfqWj3WIUBJZmg%3D%3D

https://www.linkedin.com/pulse/genetically-engineered-mouse-model-gemm-market-research-report-dyeyc?trackingId=dbTXz381QN2ifvAcR6IoIA%3D%3D

0 notes

Text

The Iron Deficiency Anemia Treatment Market Is Thriving On Growing Demand

The iron deficiency anemia treatment market consists of oral iron replacement therapies that are used to treat low iron levels in the blood. Oral iron supplements offer convenience as they can be taken at home and have advantages like lower cost and fewer side effects compared to intravenous infusions. Iron deficiency anemia is a widespread nutritional disorder globally owing to insufficient dietary intake of iron or absorption issues. It can cause fatigue, weakness, and shortness of breath if left untreated. Global iron deficiency anemia treatment market is estimated to be valued at US$ 12.1 Bn in 2024 and is expected to reach US$ 21.6 Bn by 2031, exhibiting a compound annual growth rate (CAGR) of 8.6% from 2024 to 2031.

Key Takeaways Key players operating in the iron deficiency anemia treatment market are AdvaCare Pharma, Otsuka Pharmaceutical Co., Ltd., Sanofi, Emcure Pharmaceuticals, Wellona Pharma, SiNi Pharma Pvt Ltd, Sun Pharmaceutical Industries Ltd., Zydus Group, Akebia Therapeutics., Rockwell Medical, Inc., AbbVie Inc., Pfizer, Inc., Velnex Medicare, PHAEDRUS LIFE SCIENCE PVT. LTD., Inopha International Co, Limited, PharmaNutra S.p.A., Pharmascience Inc., American Regent, Inc. The growing Iron Deficiency Anemia Treatment Market Growth for oral iron replacement therapies owing to advantages like convenience of use and less side effects compared to intravenous infusions is fueling the market growth. Oral iron supplements can easily be taken at home without much supervision. The market is witnessing expansion in developing regions due to rising awareness and healthcare investments. There is a growing focus of market players on these regions through product launches, collaborations and mergers & acquisitions to strengthen their presence. Market Key Trends The market is witnessing high research and development activities by players to come up with innovative oral iron formulations. Iron Deficiency Anemia Treatment Market Size and Trends includes extended-release formulations with lower dosing frequency and tablets with enhanced biocompatibility for better iron absorption. Development of new pediatric formulations suitable for infants and children is also among the key research areas.

Porter’s Analysis Threat of new entrants: Low due to high costs involved to established production and distribution networks along with high capital requirements. Also, presence of few large players makes it difficult for new entrants. Bargaining power of buyers: Moderate as large number of generic alternatives available. However, severity and risk associated with condition increases buyer power. Bargaining power of suppliers: Moderate as raw material suppliers have limited control over pricing due to availability of substitutes. Threat of new substitutes: High due to emergence of alternative therapies and newer oral and injectable formulations. Competitive rivalry: Very high due to presence of many global and local players providing different treatment options. Intense competition keeps pricing pressure on existing products. Geographical Regions In terms of value, North America accounts for the largest share of the iron deficiency anemia treatment market due to growing prevalence of the disease and presence of advanced healthcare facilities. The U.S. is the major revenue generator within North America. Asia Pacific is the fastest growing region owing to rising geriatric population, increasing awareness regarding anemia, and improving access to healthcare services in emerging countries like India and China. The availability of low-cost generic drugs provides an impetus to market growth in Asia Pacific.

Get more insights on Iron Deficiency Anemia Treatment Market

Discover the Report for More Insights, Tailored to Your Language

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups.

(LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)

#Coherent Market Insights#Iron Deficiency Anemia Treatment Market#Iron Deficiency Anemia Treatment#Iron Supplements#Anemia Treatment#Iron Deficiency#Oral Iron Therapy#Intravenous Iron#Iron Absorption#Ferrous Sulfate

0 notes

Text

OTC Allergy Medicine Market: Size, Share, and Industry Trends Forecasted Through 2032

Introduction

Over-the-counter (OTC) allergy medicines are a popular choice for individuals seeking relief from allergy symptoms without the need for a prescription. These medications, including antihistamines, decongestants, and combination products, are widely used to manage symptoms such as sneezing, itching, nasal congestion, and watery eyes. The OTC allergy medicine market has seen considerable growth due to increasing allergy prevalence, advancements in drug formulations, and growing consumer awareness. This article provides an in-depth analysis of the OTC allergy medicine market, focusing on its size, share, industry trends, and forecast through 2032.

Market Size and Growth

Otc allergy medicine Market Size was estimated at 6.86 (USD Billion) in 2023. The Otc Allergy Medicine Market Industry is expected to grow from 7.02 (USD Billion) in 2024 to 8.47 (USD Billion) by 2032. The otc allergy medicine Market CAGR (growth rate) is expected to be around 2.38% during the forecast period (2024 - 2032).The market's growth is driven by several factors, including the rising prevalence of allergic conditions, increasing consumer preference for self-medication, and the availability of a wide range of OTC allergy products.

Allergic conditions, such as allergic rhinitis, hay fever, and seasonal allergies, are becoming more common globally due to environmental factors, lifestyle changes, and genetic predisposition. This growing prevalence has increased the demand for effective and accessible allergy relief options. OTC allergy medicines offer a convenient and cost-effective solution for managing allergy symptoms, contributing to the market's expansion.

Advancements in drug formulations and the development of new and improved OTC allergy products also play a significant role in driving market growth. Innovations such as extended-release formulations, non-drowsy antihistamines, and combination therapies have enhanced the effectiveness and convenience of OTC allergy medicines, attracting more consumers.

Market Share Analysis

North America is currently the largest market for OTC allergy medicines, holding a substantial share. The region's dominant position is due to high consumer awareness, a well-established retail distribution network, and the presence of major pharmaceutical companies. The United States, in particular, has a large consumer base for OTC allergy products, driven by the high prevalence of allergies and the availability of a wide range of over-the-counter options.

Europe follows North America in terms of market share, with countries like Germany, the United Kingdom, and France leading the region's market growth. The European market is supported by increasing allergy prevalence, rising healthcare expenditure, and a growing focus on self-medication. Regulatory approvals and the availability of OTC allergy medicines in various European countries further contribute to market expansion.

The region's rapid market expansion is driven by increasing urbanization, rising awareness of allergy management, and improving healthcare infrastructure. Countries like China, India, and Japan are key contributors to the growth of the OTC allergy medicine market in Asia-Pacific, supported by a large population base and increasing healthcare spending.

Industry Trends

Several key trends are shaping the OTC allergy medicine market:

Rising Allergic Conditions: The increasing prevalence of allergic conditions, including allergic rhinitis, asthma, and eczema, is a significant driver of market growth. Environmental factors such as pollution, climate change, and exposure to allergens contribute to the rising incidence of allergies, leading to higher demand for OTC allergy medications.

Growing Preference for Self-Medication: There is a growing trend towards self-medication, with consumers seeking convenient and accessible solutions for managing their health conditions. OTC allergy medicines offer a convenient option for individuals to manage their allergy symptoms without requiring a prescription. This trend is expected to continue driving market growth as more consumers opt for over-the-counter solutions.

Advancements in Drug Formulations: The development of new and improved drug formulations is enhancing the effectiveness and appeal of OTC allergy medicines. Innovations such as non-drowsy antihistamines, extended-release formulations, and combination products provide more options for consumers and improve their overall experience with allergy management.

Increased Consumer Awareness: Growing awareness about the availability and benefits of OTC allergy medicines is contributing to market growth. Educational campaigns, online resources, and increased visibility of allergy products in retail stores are helping consumers make informed decisions about their allergy management options.

Expansion of Retail Channels: The expansion of retail channels, including online pharmacies and e-commerce platforms, is making OTC allergy medicines more accessible to consumers. The convenience of online shopping and the availability of various OTC products through digital channels are driving market growth and providing consumers with more options for purchasing allergy medications.

Market Forecast

The OTC allergy medicine market is expected to continue growing through 2032, driven by the increasing prevalence of allergies, advancements in drug formulations, and the growing preference for self-medication. Key players in the market will need to focus on innovation, expanding their product offerings, and leveraging digital channels to stay competitive.

Key Market Segments: The OTC allergy medicine market can be segmented based on product type, distribution channel, and region. Product types include antihistamines, decongestants, combination products, and nasal sprays. Distribution channels encompass pharmacies, drug stores, online pharmacies, and retail stores. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Challenges: Despite the positive growth outlook, the OTC allergy medicine market faces challenges such as regulatory hurdles, the presence of counterfeit products, and potential side effects of certain medications. Additionally, the availability of prescription allergy treatments may impact the demand for OTC options.

Conclusion

The OTC allergy medicine market is poised for significant growth through 2032, driven by the increasing prevalence of allergies, advancements in drug formulations, and the rising preference for self-medication. As the market evolves, key players will need to focus on innovation, expanding their product portfolios, and exploring new growth opportunities. The OTC allergy medicine market offers substantial opportunities for growth, particularly in emerging markets and through digital retail channels.

0 notes

Text

Topical Drug Delivery Market Current Trends, Technology and Industry Analysis 2032

Topical drug delivery has become a critical method in modern healthcare, offering a non-invasive and direct approach to treating localized conditions. By administering drugs directly onto the skin or mucous membranes, topical drug delivery enables targeted treatment with minimal systemic side effects. This method is widely utilized for various conditions, including skin disorders, pain management, and infections. The appeal of topical drug delivery lies in its convenience, efficiency, and potential to improve patient compliance, as it reduces the need for oral or injectable medications.

The Topical Drug Delivery Market Size was valued at USD 210.03 Billion in 2023 and is expected to reach USD 499.39 Billion by 2032 and grow at a CAGR of 10.62% over the forecast period 2024-2032.

Future Scope

The future of topical drug delivery looks promising, with ongoing research focused on enhancing drug absorption and developing more advanced delivery systems. Innovations such as nanotechnology and liposomal formulations are paving the way for better drug penetration and sustained release, allowing medications to act more effectively over extended periods. These advancements are expected to expand the range of drugs suitable for topical application, creating new possibilities for treating chronic and hard-to-reach conditions without systemic side effects.

Trends

Key trends in topical drug delivery include the use of transdermal patches for controlled drug release, advancements in microencapsulation, and the development of active delivery systems like iontophoresis. There is also a growing interest in utilizing natural polymers for drug carriers, which provide biodegradable and biocompatible options for topical treatments. These trends are geared towards enhancing drug delivery precision, stability, and patient adherence, ultimately leading to better therapeutic outcomes.

Applications

Topical drug delivery is commonly applied in dermatology to treat conditions such as acne, eczema, and psoriasis, as well as in pain management through analgesic creams and gels. It is also used in wound care, ophthalmology, and hormone replacement therapies. With innovations in transdermal patches and targeted creams, topical drug delivery is expanding into new fields, including cancer treatment and chronic pain management, making it a versatile and valuable option in various medical fields.

Key Points

Topical drug delivery provides targeted treatment with minimal systemic side effects.

Innovations in nanotechnology are enhancing drug penetration and sustained release.

Transdermal patches and iontophoresis are popular trends in controlled drug delivery.

Applied in dermatology, pain management, wound care, and hormone replacement therapy.

Expands into new areas, including cancer treatment and chronic pain management.

Conclusion

Topical drug delivery is revolutionizing healthcare by providing an efficient, non-invasive treatment option for localized conditions. With continued advancements in drug formulations and delivery mechanisms, this method is set to offer even more precise, long-lasting, and convenient solutions for patients. As the demand for safer and more effective treatments grows, topical drug delivery is poised to play a significant role in advancing personalized healthcare.

#Topical Drug Delivery Market#Topical Drug Delivery Market Size#Topical Drug Delivery Market Share#Topical Drug Delivery Market Growth#Topical Drug Delivery Market Report

0 notes

Text

Growth Drivers in the Alginates and Derivatives Market: A Global Perspective

Alginates and Derivatives Market Overview

The alginates and derivatives market refers to the industry involved in the production, distribution, and sale of alginate compounds and their various derivatives. Alginates are a group of naturally occurring polysaccharides found in brown seaweeds, primarily consisting of mannuronic acid and guluronic acid residues. They are widely used in various industries due to their unique properties, including thickening, gelling, stabilizing, and film-forming capabilities.

Alginates and their derivatives, derived from brown seaweed, exhibit remarkable versatility and have established themselves as indispensable multifunctional ingredients across a variety of industries. Sodium alginate, a key derivative, showcases its adaptability in numerous applications spanning from culinary endeavors to agricultural practices. In the culinary field, alginates function as essential gelling, thickening, and stabilizing agents, enabling the creation of diverse textures and presentations in foods ranging from sauces to desserts.

Beyond the culinary realm, alginates are proving their worth in agriculture, serving as effective soil conditioners that enhance soil structure, moisture retention, and nutrient availability, thereby fostering sustainable farming methods. Moreover, the unique attributes of alginates make them valuable in biotechnological applications, such as cell encapsulation for drug delivery and the development of biocompatible matrices for bioartificial organs. Additionally, alginates contribute significantly to water treatment processes, acting as flocculating agents that aid in the removal of impurities and the clarification of water.

The alginates and derivatives market size is estimated at USD 494 million in 2023 and is projected to reach USD 651 million by 2028, at a CAGR of 5.7% from 2023 to 2028.

Factors Driving the Alginates and Derivatives Industry Growth

Alginate, a natural polysaccharide extracted from brown seaweed, offers a remarkable range of functionalities due to its gelling, thickening, biocompatible, and encapsulating properties. These functionalities translate into a vast array of applications across various industries.

Food Industry: Alginate excels as a gelling agent in desserts, dairy products, and meat products. It also acts as a thickening and stabilizing agent in sauces, dressings, and texturizer for various food items, improving texture and mouthfeel. Additionally, alginate films with good water retention properties extend the shelf life of fruits and vegetables.

Pharmaceuticals and Biomedical Applications: Alginate’s biocompatibility and low toxicity make it ideal for wound care products, drug delivery systems with controlled release, and tissue engineering.

Other Applications: Alginate derivatives function as emulsifiers in salad dressings, ice cream, and cosmetics. Furthermore, alginate-based materials play a role in environmental applications like wastewater treatment and bioremediation by binding pollutants.

The multifunctionality of alginates and their derivatives results in their widespread adoption across diverse industries, driving the alginate market growth. As industries continue to seek sustainable and natural alternatives, alginate’s eco-friendly nature further contributes to its market appeal.

Make an Inquiry to Address your Specific Business Needs

Opportunities for manufacturers in the global alginates and derivatives industry

The global rise in convenience food consumption is driven by factors like busy lifestyles, increased female workforce participation, and longer working hours. This trend creates a significant demand for food additives that enhance the quality, texture, and taste of processed foods like soups, cakes, pastries, bread, gravies, and snacks. Alginates perfectly fit this role.

Functional Benefits of Alginates: Alginates act as thickening, gelling, and binding agents, allowing manufacturers to create appealing textures and mouthfeel in convenience foods. Additionally, alginates can help reduce fat content, catering to the growing consumer preference for low-calorie and low-fat options.

Market Opportunity for Alginate Manufacturers: The demand for customized food additives presents an opportunity for alginate producers. Companies like Ashland Inc. offer specialized alginates for various applications in dairy, confectionery, bakery, and other convenience food sectors.

According to type, sodium alginate is expected to hold the largest alginates and derivatives market share

Culinary Artistry: Sodium alginate’s gelling properties revolutionize food presentation through techniques like spherification, while also stabilizing and enhancing textures of sauces and dairy products.

Pharmaceutical Advancements: In the medical field, sodium alginate acts as a disintegrant in drugs, promoting absorption, and facilitates controlled-release drug delivery systems.

Textile Industry: During dyeing and printing, sodium alginate’s thickening properties ensure even dye distribution for better color retention in fabrics.

Healthcare Applications: Wound dressings containing sodium alginate manage moisture balance in exuding wounds, accelerating healing.

Biotechnology Frontiers: Sodium alginate plays a crucial role in cell encapsulation, advancing cell culture, tissue engineering, and regenerative medicine. Furthermore, it acts as a flocculating agent in water treatment, aiding in purification.

Creative Realm: Beyond industrial applications, artists and designers utilize sodium alginate’s gel-forming properties to create unique molds and casts.

Sodium alginate, derived from seaweed, is a remarkably versatile material with applications that span numerous industries.

The European market will make the most significant contribution to the global alginates and derivatives processing market

The alginates and derivatives market in Europe is experiencing significant growth, driven by industries embracing the diverse applications of this natural compound. The active participation of European countries in global trade enhances the accessibility of alginates, facilitating their flow across borders and supporting various industries with their versatile applications. European nations play pivotal roles in global trade, serving as both importers of raw materials and exporters of finished products. The demand for alginates in Europe influences international trade dynamics, impacting production, pricing, and supply chains on a global scale.

Furthermore, Europe has been leading environmental awareness and sustainability initiatives. Alginate, being a natural and biodegradable material, stands to benefit from the region’s growing emphasis on eco-friendly products and practices.

Key Questions Addressed by the alginates and derivatives market report

What is the current size of the global alginates and derivatives market?

What is the economic importance of alginate?

What drives the alginates & derivatives market?

Alginates and Derivatives Companies Highlighted

Alginates and derivatives market key players include FMC Corporation (US), Kimica Corporation (Japan), Cargill, Inc (US), E.I. Dupont De Nemours And Company (US), The Dow Chemical Company (UK), Penford Corporation (US), Ashland Inc. (US), Brenntag AG (Germany), Dastech International, Inc (US), Snap Natural & Alginate Products Pvt. Ltd (India), Bright Moon Group (China), and Döhler Group (Germany). These players in this market are focusing on increasing their presence through expansion

0 notes

Text

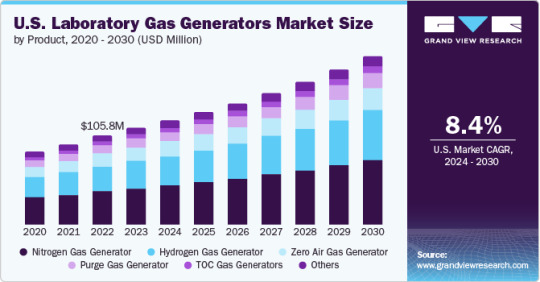

Laboratory Gas Generators Market To Reach $777.4 Million By 2030

The global laboratory gas generators market size is anticipated to reach USD 777.4 million by 2030 and is expected to expand at a CAGR of 8.3% during the forecast period, according to a new report by Grand View Research, Inc. The growth of the market is attributed to the growing importance of analytical techniques in drug and food safety testing, growing safety concerns related to the use of conventional gas cylinders, and increasing R&D spending in the life science sector.

Laboratory gas generators operate across diverse applications, including chromatography and mass spectrometry, wherein they provide high-purity gas essential for accurately identifying various substances within samples, contributing to drug development and quality control. Further in drug detection and analysis, gas supplied from generators ensures efficient and accurate analysis of drug composition, purity, and potential contaminants.

In pharmaceutical packaging, nitrogen gas generators create an inert environment, shielding products from oxidation and degradation during transport and storage, ultimately preserving their integrity and efficacy. However, their role goes beyond mere protection. The nitrogen blanketing facilitated by generators also helps improve the quality of pharmaceutical products. Oxygen exposure can degrade various medications, affecting their potency and shelf life. By creating an oxygen-free environment, generators maintain product quality and extend their usable window.

The laboratory gas generators industry is characterized by intense competition, with numerous manufacturers and suppliers vying for market share. Some of the key players operating in the market include Peak Scientific Instruments, PerkinElmer Inc., Linde plc., VICI DBS, Dürr Technik GmbH & Co. KG, Erre Due S.p.a., and CLAIND srl. Companies are focusing on product innovation, technological advancements, and strategic collaborations to differentiate their offerings and gain a competitive edge. In addition, the growing trend towards customization and modularization in gas generation systems allows end-users to tailor solutions to their specific requirements, further driving market growth and adoption.

Request a free sample copy or view report summary: Laboratory Gas Generators Market Report

Laboratory Gas Generators Market Report Highlights

The nitrogen gas generator segment led the market and accounted for 38% in 2023. The adoption of nitrogen gas generators is driven by their ability to provide high-purity nitrogen on-demand, eliminating the need for gas cylinder handling and storage.

Growing Liquid Chromatography-Mass Spectrometry (LC-MS) field, crucial for drug discovery and metabolomics, drives the need for high-purity nitrogen and helium gas generators for nebulization and collision gas.

The life science sector represents a significant end-user segment for laboratory gas generators, driven by the increasing demand for analytical instruments in drug discovery, development, and quality control processes.

North America dominated the market owing to the increasing investments in the life science, food & beverage, and chemical sectors in the region.

In July 2023, Peak Scientific Instruments introduced nitrogen gas generation solutions with the release of the Corona 1010A. This innovative solution delivers high-purity, filtered nitrogen gas, empowering various applications with a reliable and potent source. Capable of delivering flows up to 5 liters per minute at pressures reaching 80psi.

Laboratory Gas Generators Market Segmentation

Grand View Research has segmented the global laboratory gas generators market based on product, application, end-use, and region:

Laboratory Gas Generators Product Outlook (Revenue, USD Million, 2018 - 2030)

Nitrogen Gas Generator

Hydrogen Gas Generator

Zero Air Gas Generator

Purge Gas Generator

TOC Gas Generators

Others

Laboratory Gas Generators Application Outlook (Revenue, USD Million, 2018 - 2030)

Gas Chromatography

Liquid Chromatography-mass Spectrometry (LC-MS)

Gas Analyzers

Others

Laboratory Gas Generators End Use Outlook (Revenue, USD Million, 2018 - 2030)

Life Science

Chemical & Petrochemical

Food & Beverage

Others

Laboratory Gas Generators Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Spain

Italy

Asia Pacific

China

India

Japan

South Korea

Australia

Central & South America

Brazil

Argentina

Middle East & Africa

Saudi Arabia

UAE

South Africa

List of Key Players in the Laboratory Gas Generators Market

Peak Scientific Instruments

PerkinElmer Inc.

Linde plc.

VICI DBS

Dürr Technik GmbH & Co. KG

Erre Due S.p.a.

Tisch Environmental, Inc.

CLAIND srl

Isolcell

OXYMAT

0 notes

Text

Over The Counter Pain Medication market will grow at highest pace owing to rising geriatric population

The over the counter pain medication market consists of non-prescription drugs used to relieve pain such as headaches, muscle pains, backaches, toothaches, colds, menstrual cramps and arthritis. These drugs provide temporary relief from pain and include analgesics like paracetamol and non-steroidal anti-inflammatory drugs such as ibuprofen and aspirin. Non-prescription pain medications are widely available as tablets, capsules and liquids in retail pharmacies and online stores, providing convenience to consumers. With growing aging population suffering from arthritis and other joint pains, the demand for these medications is increasing rapidly.

The Global Over The Counter Pain Medication Market is estimated to be valued at US$ 27.12 Bn in 2024 and is expected to exhibit a CAGR of 4.1% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the Over The Counter Pain Medication market include Johnson & Johnson, Pfizer Inc., Bayer AG, GlaxoSmithKline plc, Sanofi S.A., Reckitt Benckiser Group plc, Novartis AG, Perrigo Company plc, Takeda Pharmaceutical Company Limited, Teva Pharmaceutical Industries Ltd., Boehringer Ingelheim International GmbH, Sun Pharmaceutical Industries Ltd., Alkem Laboratories Ltd., Cipla Ltd., Dr. Reddy's Laboratories Ltd., Glenmark Pharmaceuticals Ltd., Lupin Limited, Aurobindo Pharma Limited. The dominance of these key players is attributed to their diverse product portfolio and strong global distribution network.

Over The Counter Pain Medication Market Demand rapidly owing to increasing incidences of headache, joint pains and menstrual problems across major countries. Self-medication has become popular as consumers frequently purchase these drugs for quick relief from minor pains without doctor's prescription.

Technological advancements are leading to development of innovative drug delivery systems for over the counter pain medications such as fast-dissolving oral thin films and gels providing pain relief more quickly. Development of combination drugs offering relief from multiple symptoms with a single drug is another key trend observed in this market. Market Trends Sustained release formulations are gaining popularity in the over the counter pain medication market. These ensure drugs remain effective for longer duration, releasing medicine slowly into the body. For example, Advil has introduced extended release gels providing all-day relief from pain.

Combination drugs offering relief from pain as well as symptoms like cold, cough and fever are witnessing strong demand. Consumers prefer single drugs treating multiple conditions. Manufacturers are developing combination pills accordingly to increase sales.

Market Opportunities The rising geriatric population suffering from arthritis and joint pains worldwide presents significant growth opportunities. Around 100 million US adults suffer from arthritis currently and the number is projected to rise to 130 million by 2060.

Online pharmacies are emerging as an important sales channel for over the counter pain medications. Expanding e-commerce and increasing preference of consumers to shop online from the convenience of their homes will drive future revenues in this distribution segment.

Impact of COVID-19 on Over The Counter Pain Medication Market Size And Trends The COVID-19 pandemic has immensely impacted the growth of the over the counter pain medication market globally. During the initial phase of the pandemic, there was a sharp surge in demand for pain relieving drugs like paracetamol, ibuprofen etc. as people stocked up medicines fearing potential shortages. This led to a significant spike in sales revenues for OTC pain medication manufacturers in 2020. However, as the pandemic prolonged, lockdowns imposed worldwide disrupted manufacturing and supply chain operations. Strict movement restrictions made it difficult for companies to transport raw materials and finished drugs. The declining disposable incomes and job losses during the economic downturn also reduced people's spending power which hindered the market growth post-2020.