#Construction Elastomers Market Research

Text

Silicone Elastomers Market Analysis: Key Drivers and Challenges Ahead

Meticulous Research®, a recognized global leader in market research, has published a detailed report titled “Silicone Elastomers Market by Type (Liquid Silicone Rubber (LSR), High-temperature Vulcanize (HTV)), Process (Extrusion, Molding), End-use Industry (Automotive, Healthcare, Electrical & Electronics, Construction), and Geography - Global Forecast to 2031.” This report provides an in-depth analysis of the silicone elastomers market, highlighting its projected growth, market dynamics, and competitive landscape.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5844?utm_source=article&utm_medium=social&utm_campaign=product&utm_content=24-09-2024

Market Projections and Growth Drivers

The silicone elastomers market is projected to reach a substantial $15.1 billion by 2031, expanding at a compound annual growth rate (CAGR) of 7.9% from 2024 to 2031. This growth is largely attributed to the increasing utilization of silicone elastomers in various industries, including medical devices, automotive applications, and the electrical and electronics sectors. The material's adaptability, durability, and performance under extreme conditions are significant factors fueling its demand.

However, the market faces challenges due to environmental concerns and sustainability issues, which have become prominent in developed countries. Additionally, fluctuations in raw material prices present a challenge to manufacturers, affecting production costs and pricing strategies.

Opportunities in the Silicone Elastomers Market

Despite these challenges, the silicone elastomers market offers numerous growth opportunities. The integration of silicone elastomers with Internet of Things (IoT) devices is emerging as a trend, providing enhanced functionality and connectivity. Furthermore, the automotive industry's increasing demand for lightweight, durable materials presents an opportunity for silicone elastomer manufacturers to innovate and expand their product offerings.

Market Segmentation

The silicone elastomers market is segmented by type, process, end-use industry, and geography:

Type Segmentation

Room-Temperature Vulcanize (RTV)

Liquid Silicone Rubber (LSR)

High-Temperature Vulcanize (HTV)

In 2024, the high-temperature vulcanize (HTV) segment is expected to dominate the market, accounting for over 52% of total market share. This can be attributed to advancements in manufacturing technologies and the rising demand for HTV in industries such as automotive, aerospace, healthcare, and electronics, where products are often subjected to high temperatures. HTV is commonly used in the production of gaskets, seals, and critical components, reinforcing its importance in safety and efficiency standards.

Conversely, the liquid silicone rubber (LSR) segment is projected to witness the highest CAGR during the forecast period. This growth is fueled by innovations in material science and the increasing demand for biocompatible materials, particularly in the healthcare sector. In March 2021, The Dow Chemical Company launched a low-density LSR product designed for a variety of applications, including food dosing valves and dispensers, demonstrating the segment's potential for expansion.

Process Segmentation

The market is also segmented by process, including:

Extrusion Process

Molding Process (including injection molding, transfer molding, and compression molding)

Calendering Process

Other Processes

The molding process segment is anticipated to command the largest share of the market, exceeding 45% in 2024. This dominance is driven by the rising demand for LSR injection molding, which facilitates the creation of complex parts efficiently. Innovations in molding technology and advancements in material science contribute to this segment's continued growth, as manufacturers seek to enhance mass production capabilities.

End-Use Industry Segmentation

The silicone elastomers market is categorized into several end-use industries:

Automotive

Aviation & Aerospace

Consumer Goods

Electrical & Electronics

Healthcare

Energy

Industrial Machinery

Construction

In 2024, the electrical and electronics segment is projected to hold the largest market share, surpassing 35%. The increasing reliance on silicone elastomers for various electronic components, including power supplies and circuit boards, supports this growth. The demand for reliable and high-performance electronic devices is driving manufacturers to integrate silicone elastomers for protection against environmental factors and physical stresses.

On the other hand, the healthcare segment is poised to record the highest CAGR during the forecast period. The rising need for biocompatible materials in medical devices, drug delivery systems, and implants underscores the segment's importance. For instance, DuPont de Nemours, Inc. recently launched Liveo Silicone Elastomer Blends to cater to the growing consumer demand for products addressing skin conditions, illustrating the segment's potential for innovation.

Geographic Segmentation

The market is analyzed across several regions, including:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

In 2024, Asia-Pacific is expected to dominate the silicone elastomers market, accounting for over 53% of the total share. The region's rapid economic development, particularly in countries like China and India, is driving demand across various industries. The growth of the healthcare sector and increasing government investments in infrastructure projects contribute to the rising adoption of silicone elastomers in construction and industrial applications.

Notably, China has become a significant manufacturing hub for silicone elastomers. In September 2023, Wacker Chemie AG announced an expansion of its specialty silicone manufacturing capabilities in China, further solidifying the country's position in the global market. The Asia-Pacific region is also projected to exhibit the highest CAGR of above 9% during the forecast period.

Key Players in the Silicone Elastomers Market

The silicone elastomers market features a competitive landscape with several key players, including:

Momentive Performance Materials, Inc. (U.S.)

China National Bluestar (Group) Co., Ltd. (China)

The Dow Chemical Company (U.S.)

Shin-Etsu Chemical Co., Ltd. (Japan)

Wacker Chemie AG (Germany)

DuPont de Nemours, Inc. (U.S.)

Specialty Silicone Products, Inc. (U.S.)

Reiss Manufacturing, Inc. (U.S.)

MESGO S.p.A. (Italy)

Rogers Corporation (U.S.)

Stockwell Elastomerics, Inc. (U.S.)

Zhejiang Xinan Chemical Industrial Group Co., Ltd. (China)

Marsh Bellofram Group of Companies (U.S.)

Cabot Corporation (U.S.)

CHT Germany GmbH (Germany)

These companies are actively innovating and expanding their product offerings to meet the evolving demands of various industries. Strategic partnerships, acquisitions, and technological advancements are essential strategies employed by these key players to maintain a competitive edge in the silicone elastomers market.

Read Full Report :- https://www.meticulousresearch.com/product/silicone-elastomers-market-5844?utm_source=article&utm_medium=social&utm_campaign=product&utm_content=24-09-2024

Conclusion

The silicone elastomers market is on an upward trajectory, driven by technological advancements, increasing demand across multiple industries, and the integration of silicone elastomers in innovative applications. Despite challenges such as environmental concerns and raw material price fluctuations, the growth opportunities present a promising landscape for stakeholders. As the market evolves, continuous innovation and strategic investments will be crucial for maintaining momentum and capitalizing on emerging trends.

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Silicone Elastomers Market#Silicone Rubber#Silicone Injection Molding#Liquid Silicone Rubber#Silicone Rubber for Medical Devices

0 notes

Text

Cast Elastomer Market : Technology Advancements, Industry Insights, Trends And Forecast 2033

The cast elastomer global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Cast Elastomer Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size -

The cast elastomer market size has grown strongly in recent years. It will grow from $1.48 billion in 2023 to $1.58 billion in 2024 at a compound annual growth rate (CAGR) of 6.7%. The growth in the historic period can be attributed to automotive industry growth, increasing demand for cast elastomers in industrial machinery components, utilization of cast elastomers in oil and gas applications, increasing footwear industry, and increasing customer electronics.

The cast elastomer market size is expected to see strong growth in the next few years. It will grow to $2.08 billion in 2028 at a compound annual growth rate (CAGR) of 7.1%. The growth in the forecast period can be attributed to increasing focus on energy-efficiency, the growing emphasis on environmentally friendly and sustainable elastomeric materials, expanded use of cast elastomers in the aerospace sector, investments in research and development, and continued growth in the renewable energy sector. Major trends in the forecast period include customization and tailoring, automated manufacturing, advanced r&d and innovation, technological innovations, and the integration of cast elastomers into 3d printing technology.

Order your report now for swift delivery @

https://www.thebusinessresearchcompany.com/report/cast-elastomer-global-market-report

The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Market Drivers -

The rise in demand for cast elastomers in various end-use industries is expected to propel the growth of the cast elastomer market in the coming years. Cast elastomers are utilized in a variety of applications in the industrial sector, including seals and gaskets, forklift wheels, coupling elements, conveyor belts, and more. These materials are then employed in a variety of sectors, including construction, heavy industry, paper, and so on. For instance, Pacific Urethanes, an Australia-based company that specializes in the development and production of polyurethane systems developed UrePacSpraycast elastomers, which are operated through a dual-component spray machine. UrePacSpraycast elastomers have high elasticity, chemical resistance, and tensile strength. These are generally used as protective linings for utility vehicles, truck bed linings, and architectural moldings. Therefore, the rise in demand for cast elastomers in various end-use industries is driving the cast elastomers market growth.

The cast elastomer market covered in this report is segmented –

1) By Type: Hot Cast Elastomer, Cold Cast Elastomer

2) By Distribution: Online, Offline

3) By End-Use Industry: Mining, Automotive And Transportation, Industrial, Oil And Gas, Other End-Users

Get an inside scoop of the cast elastomer market, Request now for Sample Report @

https://www.thebusinessresearchcompany.com/sample.aspx?id=5561&type=smp

Regional Insights -

North America was the largest region in the cast elastomer market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the cast elastomer market report include Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

Key Companies -

Major companies operating in the cast elastomer market include Argonics Inc., BASF SE, Chemline Incorporation, Coim Group, Covestro AG, Du Pont De Nemours and Company, Era Polymers Pty Ltd., Huntsman International LLC, Lanxess AG, Mitsui Chemicals Inc., Notedome Limited, Synthesia Technology, Dow Chemical Company, Tosoh Corporation, Carlisle Polyurethane Systems, Wacker Chemie AG, Momentive Performance Materials Inc., Cast Urethane, Wanhua Chemical Group Co. Ltd., Polyurethane Products Corporation, Huntsman Corporation, Notedome Ltd., Trelleborg AB, RTP Company, PolyOne Corporation, Hexpol AB, Permali Gloucester Limited, Rubberlite Inc., Sanchem Inc.

Table of Contents

1. Executive Summary

2. Cast Elastomer Market Report Structure

3. Cast Elastomer Market Trends And Strategies

4. Cast Elastomer Market – Macro Economic Scenario

5. Cast Elastomer Market Size And Growth

…..

27. Cast Elastomer Market Competitor Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

30. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

Asia Pacific and Japan Wire Cable Market Future Trends to Look at | BIS Research

A wire cable is a strong, flexible assembly made of multiple strands of metal wire twisted or braided together. Wire cables are typically used for lifting, pulling, tensioning, or transmitting mechanical force. They are commonly made from steel, stainless steel, or other durable metals and are used in a variety of applications such as construction, cranes, elevators, bridges, and heavy machinery

The Asia-Pacific and Japan wire and cable market was valued at $88.26 billion in 2022, and it is expected to grow at a CAGR of 8.03% and reach $199.71 billion by 2032

At BIS Research, we focus exclusively on technologies related to precision medicine, medical devices, life sciences, artificial intelligence (AI), machine learning (ML), Internet of Things (IoT), big data, blockchain technology, Asia Pacific and Japan Wire Cable Material , advanced materials and chemicals, agriculture and FoodTech, mobility, robotics, and aerospace and defense, among others.

Asia Pacific and Japan Wire Cable Overview

Wire and cable are essential components used in electrical and mechanical systems for conducting electricity, transmitting signals, and supporting structural loads. While often used interchangeably, "wire" generally refers to a single conductor made of metal, such as copper or aluminum, whereas "cable" consists of two or more wires bundled or braided together, often with insulation or protective sheathing.

Types of Wire and Cable

Electrical Wire - Used to carry electrical current within buildings, appliances, or equipment. These wires are often insulated to prevent short circuits and protect users from electric shocks.

Communication Cable - Includes fiber optic and coaxial cables used for transmitting data, phone, or internet signals over distances.

Mechanical Wire Cables - Comprising twisted or braided metal strands, these are designed to bear loads and are commonly used in cranes, bridges, elevators, and other heavy-duty applications.

Key Features

Conductivity - Electrical wires and cables use materials like copper or aluminum for efficient electrical conduction.

Insulation - Protective layers, such as plastic, rubber, or PVC, are used to prevent electrical leakage and ensure safe handling.

Durability - Cables, especially mechanical wire cables, are designed to be strong, flexible, and resistant to wear, corrosion, and environmental factors.

Applications of Asia Pacific Japan Wire Cable Market

Electrical Wiring in Buildings

Data Transmission

Heavy Industries

Demand - Drivers and Limitations

Following are the demand drivers for the Asia-Pacific and Japan wire and cable market:

• Increase of Investments in the Telecommunications Industry

• Increase in Demand for Sustainable Wire and Cable Products

• Rise of Industrial Revolution 4.0

• Increase in Sales of Electric Vehicles

• Rise in the Demand for Energy Produced from Renewable Sources

Following are the limitations of the Asia-Pacific and Japan wire and cable market:

• Fluctuations in Raw Material Prices

• Ban by the Government on Materials Used in Wire and Cable Production

• Limited Availability of Sustainable Materials and its Related Standardization Challenges

• Challenges Faced by Wire and Cable Manufacturers Due to Plastic Disposal

Key Companies

Dow

Wacker Chemie AG

Momentive Performance Materials

Shin-Etsu Chemical Co., Ltd.

China National Bluestar (Group) Co., Ltd.

Rogers Corporation

Cabot Corporation

Reiss Manufacturing Inc.

MESGO S.p.A.

CHT Germany GmbH

Bellofram Elastomers

Grab a look at the report page click here !

Market Segmentation for Asia Pacific and Japan Wire Cable

Segmentation 1: by Application

Based on application, in the Asia-Pacific and Japan wire and cable market, the infrastructure application is poised to lead, indicating a strong demand for wiring and cabling solutions in construction and development projects.

Segmentation 2: by Product

Segmentation 3: by Voltage Type

Based on product, low voltage energy cables (<1kV) are leading the Asia-Pacific and Japan wire and cable market due to their widespread applications and compatibility with diverse electrical systems.

Segmentation 4: by Country

Based on the country, China is poised to lead the Asia-Pacific and Japan wire and cable market, holding the largest share due to robust industrialization, extensive infrastructure development, and growing demand for power solutions. Its role in manufacturing and technology adoption strengthens its market position, influencing trends and competitiveness in the region.

Visit our Next Generation Fuel/ Energy Storage Solutions

Recent Developments in the Asia-Pacific and Japan Wire and Cable Market

• In August 2023, LS Cable & System Ltd. invested an additional $118.5 million (KRW 155.5 billion) for its business establishment in Donghae City, Gangwon Province, South Korea, for the expansion of its submarine cable production facilities.

• In April 2023, Finolex Cables allocated $24.3 million (INR 200 crore) for its production center in Pune, India, to expand its production capabilities across several industries, including fiber optic cables, auto cables, and photovoltaic cables sector.

Have a look at the free sample click here !

Conclusion

In conclusion, the Asia Pacific and Japan Wire Cable market serves as the backbone of global communication, addressing the need for rapid and reliable data transmission. The growth of this market is fueled by technological advancements, the expanding telecommunications landscape, emerging 6G sector and the ongoing digital transformation.

The increasing adoption of 5G networks, the rise of cloud computing, and the growth of data centers are key factors propelling the demand for both Asia Pacific and Japan Wire Cable s.

Asia Pacific and Japan Wire Cable are integral to the functioning of the digital economy, enabling seamless communication, connectivity, and data sharing across industries, homes, and businesses.

0 notes

Text

South Africa Specialty Chemicals Market Trends, Report 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated South Africa Specialty Chemicals Market size at USD 8.7 million in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4.50% reaching a value of USD 11.1 million by 2030. By volume, BlueWeave estimated South Africa Specialty Chemicals Market size at 13.1 million tons in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4% reaching the volume of 17.2 million tons by 2030.

The expanding usage of specialty chemicals in a range of end-user sectors, such as water treatment, chemicals, oilfields, pharmaceuticals, and others, together with improvements in process technology, are key growth drivers for South Africa specialty chemicals market. The government's financial support and other initiatives to increase domestic manufacturing are also expected to propel South Africa specialty chemicals market over the forecast period.

Sample Request @ https://www.blueweaveconsulting.com/report/south-africa-specialty-chemicals-market/report-sample

Opportunity - Expanding automobile manufacturing operations

The expanding automobile production is emerging as one of the major driving factors for the growth of South Africa Specialty Chemicals Market. South Africa ranks 22 in global vehicle production and has been attracting significant foreign direct investment and adopting various growth strategies to boost the automotive industry. Specialty chemicals are widely used in the production of high-performance lubricants and additives. These are essential to reduce wear and friction in engines and engines, improving automobiles' general efficiency and dependability.

Agrochemicals Product Type to Grow at Fastest CAGR

South Africa Specialty Chemicals Market, on the basis of product type, is comprised of agrochemicals, rubber processing chemicals, construction chemicals, food & feed additives, cosmetic chemicals, oilfield chemicals, specialty pulp & paper chemicals, specialty textile chemicals, water treatment chemicals, pharmaceutical & nutraceutical additives, CASE (coatings, adhesives, sealants & elastomers), and other (institutional & industrial cleaners, electronic chemicals, and mining chemicals) segments. Among these product types, the agrochemicals segment is anticipated to register fastest growth rate during the period in analysis. The expanding agriculture sector and rising food demand are expected to fuel the demand for agrochemicals in the South African Specialty Chemicals Market.

Competitive Landscape

South Africa Specialty Chemicals Market is intensely competitive, as a number of companies are competing to gain a significant market share. Key players in the market include Durban Speciality Chemicals, AECI Specialty Chemicals, SUN ACE South Africa, Safic Alcan Southern Africa (Pty) Ltd, IMCD South Africa, Protea Chemicals, Reba Chemicals (Pty) Ltd, BASF, Gold Reef Speciality Chemicals (Pty) Ltd, and Southern Chemicals (Pty) Ltd.

To further enhance their market share, these companies employ various strategies, including mergers and acquisitions, partnerships, joint ventures, license agreements, and new product launches.

Contact Us:

BlueWeave Consulting & Research Pvt. Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

EPDM Gaskets Manufacturers and Dealers in India: A Focus on Dirak India

Gaskets play a vital role in various industrial applications by providing a reliable seal between two surfaces, preventing leakage of fluids or gases, and ensuring safety and efficiency. Among the various types of gaskets, EPDM (Ethylene Propylene Diene Monomer) gaskets are highly sought after due to their excellent resistance to weathering, ozone, and temperature extremes. In India, numerous manufacturers and dealers specialize in EPDM gaskets, with Dirak India standing out as a leading name in this domain.

What are EPDM Gaskets?

EPDM gaskets are made from Ethylene Propylene Diene Monomer rubber, a synthetic elastomer known for its outstanding durability, flexibility, and resistance to a wide range of environmental factors. These gaskets are commonly used in automotive, industrial, and construction applications due to their ability to withstand harsh conditions, including exposure to UV rays, ozone, and varying temperatures. EPDM gaskets are also resistant to water, steam, and some chemicals, making them ideal for outdoor and high-performance sealing applications.

Key Features of EPDM Gaskets

When selecting EPDM gaskets, it's essential to understand their key features, which contribute to their widespread use across various industries:

Excellent Weather Resistance: EPDM gaskets are highly resistant to environmental elements such as UV rays, ozone, and extreme temperatures, making them ideal for outdoor applications.

High Elasticity and Flexibility: These gaskets maintain their shape and elasticity even under extreme stress and pressure, ensuring a reliable seal.

Resistance to Chemicals and Water: EPDM gaskets are resistant to a range of chemicals, including acids and alkalis, as well as water and steam, enhancing their versatility in industrial settings.

Durability and Longevity: With high resistance to wear and tear, EPDM gaskets offer long-lasting performance, reducing maintenance costs and downtime.

Cost-Effective: Compared to other types of gaskets, EPDM gaskets provide an economical solution without compromising on quality and performance.

Leading EPDM Gasket Manufacturers and Dealers in India

India is home to several reputable manufacturers and dealers specializing in EPDM gaskets, offering a wide range of products to cater to diverse industrial requirements. Among these, Dirak India has established itself as a trusted leader in the market.

Dirak India: Known for its commitment to quality and innovation, Dirak India offers a comprehensive range of EPDM gaskets designed to meet the specific needs of various industries. The company focuses on delivering products that are not only durable and reliable but also customizable to suit different applications. With a strong emphasis on research and development, Dirak India continually enhances its product portfolio to incorporate the latest materials and technologies, ensuring top-notch performance and safety.

Nobel Gaskets Pvt. Ltd.: A prominent name in the gasket manufacturing industry, Nobel Gaskets offers a wide range of EPDM gaskets that cater to various sectors, including automotive, construction, and HVAC.

Spareage Sealing Solutions: This company specializes in sealing solutions and offers a variety of EPDM gaskets known for their high quality and excellent sealing properties.

Perfect Gasket & Seals: A well-known manufacturer and supplier of industrial gaskets, Perfect Gasket & Seals provides a wide range of EPDM gaskets with a focus on precision and durability.

Why Choose Dirak India for EPDM Gaskets?

Dirak India has emerged as a leading manufacturer and dealer of EPDM gaskets in India, thanks to its unwavering commitment to quality, innovation, and customer satisfaction. Here are some reasons why Dirak India is the preferred choice for EPDM gaskets:

Superior Quality Materials: Dirak India uses high-grade EPDM rubber that ensures excellent performance, durability, and resistance to harsh environmental conditions.

Customizable Solutions: The company offers a wide range of EPDM gaskets that can be customized in terms of size, shape, and thickness to meet specific client requirements.

Advanced Manufacturing Techniques: With state-of-the-art manufacturing facilities and a focus on continuous improvement, Dirak India delivers products that adhere to international quality standards.

Comprehensive Product Range: Whether you need standard or specialized EPDM gaskets, Dirak India provides a diverse range of options to suit various industrial needs.

Excellent Customer Support: Dirak India is committed to providing exceptional customer service, from product selection to after-sales support, ensuring a seamless experience for its clients.

Applications of EPDM Gaskets from Dirak India

EPDM gaskets from Dirak India are used in a wide range of applications across various industries:

Automotive: EPDM gaskets are widely used in automotive doors, windows, and sealing systems due to their excellent weather resistance and flexibility.

Construction: In the construction industry, these gaskets provide reliable sealing solutions for windows, doors, facades, and roofing systems.

HVAC Systems: EPDM gaskets are used in heating, ventilation, and air conditioning (HVAC) systems to provide airtight seals and reduce energy loss.

Electrical Enclosures: They are also used in electrical enclosures to protect sensitive equipment from dust, moisture, and other environmental factors.

Conclusion

When it comes to choosing EPDM gaskets for industrial applications, it is crucial to select a manufacturer and supplier that offers a combination of quality, reliability, and innovation. Dirak India, with its extensive range of high-quality EPDM gaskets, meets these criteria and more. Whether you are looking for standard or custom solutions, Dirak India provides products that ensure optimal performance, durability, and safety.

Investing in EPDM gaskets from a trusted supplier like Dirak India not only guarantees a reliable sealing solution but also contributes to the overall efficiency and longevity of your equipment and systems.

0 notes

Text

North America Silicone Market To Reach USD 6.69 Billion By 2030

North America Silicone Market Growth & Trends

The global North America silicone market size is expected to reach USD 6.69 billion by 2030, registering a CAGR of 5.5% from 2024 to 2030, according to a new report by Grand View Research, Inc. The market is poised for growth due to increasing demand across multiple industries, such as automotive, construction, electronics, healthcare, and consumer goods. Silicone's versatility and wide range of applications, including sealants, adhesives, coatings, and elastomers, make it a sought-after material. In addition, the market is driven by the growing emphasis on sustainability, as silicone offers eco-friendly properties, recyclability, durability, and low toxicity.

The silicone market is expected to perform moderately owing to limited opportunities by market maturity of both manufacturing industries in general and the use of silicones. However, continuous product innovation and ongoing technological developments are expected to promote the application of silicone in emerging markets, such as electric vehicles (EVs) and health & personal care, which, in turn, is expected to fuel the market growth over the forecast period. Moreover, suppliers continue gaining market share through value-added product development and creating inroads into applications that conventionally use other materials.

In terms of product, the fluid segment's dominance is reinforced by the reliability and trust that the industry places in silicone fluids. Their resistance to extreme temperatures, chemical inertness, and low toxicity make them a preferred choice in critical applications. In addition, the ease of handling and formulation flexibility further bolster their popularity among manufacturers. Therefore, the fluid segment has firmly established itself as the go-to solution in the North America silicone industry, meeting the diverse demands of different industries and solidifying its position as the primary driver of the market's growth.

In terms of end-use, the industrial processes segment led the market in 2022, which is attributed to the remarkable properties of silicone that cater to a wide array of industrial applications. Silicone's unique characteristics, such as high thermal stability, excellent electrical insulation, and resistance to chemicals, make it highly sought-after in various industrial settings. Silicone finds extensive use in industries such as automotive, electronics, construction, and aerospace, where it serves as a crucial component in coatings, lubricants, adhesives and sealants. Its ability to withstand extreme temperatures and harsh environments makes it invaluable in industrial processes, where reliability and performance are of utmost importance.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/north-america-silicone-market-report

North America Silicone Market Report Highlights

In terms of product, The fluid product segment led the market and accounted for a revenue share of over 45.0% in 2023, which is attributed to rising product demand from the end-use industries such as electronics, transportation, construction, healthcare, personal care, and consumer goods, energy, and industrial processes

Silicone fluid offers resistance to extreme temperatures, chemical inertness, and low toxicity making them a preferred choice in critical applications. In addition, the ease of handling and formulation flexibility further bolster their popularity among manufacturers

Expanding manufacturing base and increasing investments in advanced technologies for vehicular production are expected to bring about a new era of automobiles, positively influencing the market for silicone

The industrial processes segment led the market and accounted for a significant revenue share in 2023. This is attributed to the remarkable properties of silicone that cater to a wide array of industrial applications. Silicone's unique characteristics, such as high thermal stability, excellent electrical insulation, and resistance to chemicals, make it highly sought after in various industrial settings

In terms of region, t U.S. silicone market held the largest revenue share of 89.5% in 2023. This is attributed to its robust industrial and economic landscape. The U.S. is home to a diverse range of industries, such as automotive, electronics, healthcare, and construction, which are significant consumers of silicone-based products

North America Silicone Market Segmentation

Grand View Research has segmented the North America silicone market on the basis of on product, end-use, and region:

North America Silicone Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Fluids

Straight Silicone Fluids

Modified Silicone Fluids

Gels

Resins

Elastomers

High Temperature Vulcanized

Liquid Silicone Rubber

Room Temperature Vulcanizaed (RTV)

Others

Adhesives

Emulsions

North America Silicone End use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Electronics

Transportation

Construction

Healthcare

Personal Care and Consumer goods

Energy

Industrial Processes

Others (Textiles)

North America Silicone Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

List of Key Players in the North America Silicone Market

CHT Group

Dow Inc.

Elkem ASA

Evonik Industries

GELEST, INC.

Jiangsu Mingzhu Silicone Rubber Material Co., Ltd.

KCC CORPORATION

Kaneka Corporation

Momentive

Shin-Etsu Chemical Co. Ltd

Wacker Chemie AG

HEXPOL AB.

Silchem Inc.

Specialty Silicone Products, Inc.

Illinois Tool Works Inc.

Abbvie Inc.

CRI-SIL Silicone Technologies, LLC

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/north-america-silicone-market-report

#North America Silicone Market#North America Silicone Market Size#North America Silicone Market Share#North America Silicone Market Trends

0 notes

Text

Thermoplastic Polyolefin Market: Current Analysis and Forecast (2022-2028)

According to a new report published by UnivDatos Markets Insights, the Thermoplastic Polyolefin Market was valued at more than USD 4.5 billion in 2020 and is expected to grow at a CAGR of around 6% from 2022-2028. The analysis has been segmented into Type (In-Situ TPO, Compounded TPO, Others); Application (Automotive, Building & Construction, Medical, Industrial, Footwear, Home Appliances); Region/Country.

The thermoplastic polyolefin market report has been aggregated by collecting informative data on various dynamics such as market drivers, restraints, and opportunities. This innovative report makes use of several analyses to get a closer outlook on the thermoplastic polyolefin market. The thermoplastic polyolefin market report offers a detailed analysis of the latest industry developments and trending factors in the market that are influencing the market growth. Furthermore, this statistical market research repository examines and estimates the thermoplastic polyolefin market at the global and regional levels.

Market Overview

Thermoplastic Polyolefin (TPO) is defined as a polymer/filler blend that usually consists of some fraction of a thermoplastic, an elastomer, or rubber, and usually a filler. Also, TPO compounds are resin blends of polypropylene (PP) and uncrosslinked EPDM rubber and polyethylene. They are characterized by high impact resistance, low density, and good chemical resistance. Furthermore, TPOs are used for exterior body parts such as bumpers, rocker panels, body seals, automotive gaskets, doors & windows, and other parts. Moreover, many companies are expanding their product portfolio by focusing on launching new products in the market which in turn is also contributing to the growth of the market. For instance, in Dec 2020, SABIC launched a new polyolefin plastomer-based solution for liquid containers with superior leakage resistance.

Some of the major players operating in the market include The Dow Chemical Company, Lyondellbasell Industries Holdings B.V., ExxonMobil Corporation, Mitsui Chemicals, Borealis AG, Mitsubishi Chemical Holdings Corporation, Chevron Phillips Chemical Company LLC, Avient Corporation, A.Schulman, and INEOS Capital Limited.

COVID-19 Impact

The recent covid-19 pandemic has disrupted the world and has brought a state of shock to the global economy. The global pandemic has impacted many industries and has transformed the way industries work is delivered. The thermoplastic polyolefin market has been significantly affected during these times owing to the delay in construction, manufacturing of vehicles, and others during the pandemic.

The global thermoplastic polyolefin market report is studied thoroughly with several aspects that would help stakeholders in making their decisions more curated.

Based on type, the market is segmented into in-situ TPO, compounded TPO, and others. The compound TPO category is to witness a higher CAGR during the forecast period. This is mainly because these are high-performance elastomers designed to improve performance in a wide range of end products and applications. Additionally, properties such as weather resistance and non-degradable to sunlight exposure are also some of the factors due to which they are widely used in the production of roofing and other exterior materials

On the basis of application, the market is categorized into automotive, building & construction, medical, industrial, footwear, and home appliances. Among these, the automotive to hold a significant share of the market in 2020. The growth of this segment can be attributed to the growing usage of TPO in automobiles mainly because it provides lightweight and highly durable auto parts. In addition, rapid economic growth in various countries leading to improvements in the transportation infrastructure and construction of vehicle production plants are also expected to positively influence the market of this segment in the upcoming years

Thermoplastic Polyolefin Market Geographical Segmentation Includes:

North America (U.S., Canada, and Rest of North America)

Europe (Germany, UK, Spain, Italy, France, and the Rest of Europe)

Asia-Pacific (China, Japan, India, and the Rest of Asia-Pacific)

Rest of the World

Asia-Pacific is anticipated to grow at a substantial CAGR during the forecast period. This is mainly due to the increasing construction and automotive industries. In addition, the growth of the healthcare sector and the development of the renewable energy industry is also driving the growth of the market. Furthermore, increased construction production is contributing to the demand for the thermoplastic polyolefin industry in the Asia-Pacific region as it finds applications in commercial and residential roofing owing to its properties such as weather resistance and cold resistance. Further, the TPO roofing systems offer significant reflectivity and energy efficiency, as well as strong UV resistance. Therefore, the use of the TPO in the roof system reduces the heat gain of the building

Request Free Sample Pages with Graphs and Figures Here https://univdatos.com/get-a-free-sample-form-php/?product_id=26877

The major players targeting the market include

The Dow Chemical Company

Lyondellbasell Industries Holdings B.V.

ExxonMobil Corporation

Mitsui Chemicals

Borealis AG

Mitsubishi Chemical Holdings Corporation

Chevron Phillips Chemical Company LLC

Avient Corporation

A.Schulman

INEOS Capital Limited

Competitive Landscape

The degree of competition among prominent global companies has been elaborated by analyzing several leading key players operating worldwide. The specialist team of research analysts sheds light on various traits such as global market competition, market share, most recent industry advancements, innovative product launches, partnerships, mergers, or acquisitions by leading companies in the Thermoplastic Polyolefin market. The major players have been analyzed by using research methodologies for getting insight views on global competition.

Key questions resolved through this analytical market research report include:

• What are the latest trends, new patterns, and technological advancements in the thermoplastic polyolefin market?

• Which factors are influencing the thermoplastic polyolefin market over the forecast period?

• What are the global challenges, threats, and risks in the thermoplastic polyolefin market?

• Which factors are propelling and restraining the thermoplastic polyolefin market?

• What are the demanding global regions of the thermoplastic polyolefin market?

• What will be the global market size in the upcoming years?

• What are the crucial market acquisition strategies and policies applied by global companies?

We understand the requirement of different businesses, regions, and countries, we offer customized reports as per your requirements of business nature and geography. Please let us know If you have any custom needs.

About UnivDatos Market Insights (UMI)

Browse Other Related Research Reports from UnivDatos Market Insights

Flotation Reagent Market

Graphite Market

Ammonium Sulfate Market

Oilfield Chemicals Market

Gear Oil Market

About UnivDatos Market Insights

UnivDatos Market Insights (UMI) is a passionate market research firm and a subsidiary of Universal Data Solutions. We believe in delivering insights through Market Intelligence Reports, Customized Business Research, and Primary Research. Our research studies are spread across topics across the world, we cover markets in over 100 countries using smart research techniques and agile methodologies. We offer in-depth studies, detailed analysis, and customized reports that help shape winning business strategies for our clients.

Contact us:

UnivDatos Market Insights (UMI)

Email: [email protected]

Web: https://univdatos.com

LinkedIn: www.linkedin.com/company/univ-datos-market-insight/

Ph: +91 7838604911

0 notes

Text

Worldwide Silicone Market 2024- Strategy Resources, Manufacturers, Supply and Forecasts 2030

Silicone Industry Overview

The global silicone market size was estimated at USD 21.33 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 6.0% from 2024 to 2030. Growing demand for silicone in various end-use industries including personal care, consumer goods, industrial processes, and construction is expected to drive market growth. The U.S. silicone industry is expected to perform moderately owing to limited opportunities by market maturity of both manufacturing industries in general and use of silicones. However, continuous product innovation and ongoing technological developments are expected to promote application of silicone in emerging markets.

Emerging applications include electric vehicles (EVs) and health & personal care, which, in turn, are expected to fuel market growth over the forecast period. Moreover, suppliers continue to gain market share through value-added product development and by creating inroads into applications that conventionally use other materials.

Gather more insights about the market drivers, restrains and growth of the Silicone Market

Silicone is widely used in the construction industry owing to weather resistant, highly stable, and inert & high-water repellent properties. It is used in conjugation with several materials such as marble, glass, concrete, aluminum, steel, and polymers, which find application in residential and commercial constructions. In addition, they are also used in construction of roads, bridges, pipelines, oil rigs, and industrial units. Rising population, increasing urbanization, and rapid industrial growth have resulted in a growing need for construction and infrastructure development globally.

The silicone industry is expected to grow owing to increasing application scope of silicone in various end-use industries. Across electronics industry, silicone is used in a broad range of electronic applications such as for protecting insulators from salt air damage, moisture-proofing of boards, modification of semiconductor encapsulating materials, and protecting ends of heating element wires in printed circuit boards (PCBs), semiconductors, and electronic control units (ECUs), LED devices, and others.

Browse through Grand View Research's Plastics, Polymers & Resins Industry Research Reports.

The global cenospheres market size was estimated at USD 592.32 million in 2023 and is projected to grow at a CAGR of 12.1% from 2024 to 2030.

The global curing agent market size was estimated at USD 6.62 billion in 2023 growing at a CAGR of 6.3% from 2024 to 2030.

Key Companies & Market Share Insights

Global silicone industry is significantly fragmented in nature with the presence of big manufacturing players globally. Market players compete mainly on the basis of technology used for production of silicone and quality of products. Key market players are inclined towards adopting marketing strategies such as mergers & acquisitions, new and innovative products along with production capacity expansions are some of popular strategies adopted by a majority of the market players operating in the global silicone market.

In September 2023, Wacker Chemie AG, a silicone manufacturer, announced the expansion of their silicone production capacities in China with an investment of USD 160.34 million (EUR 150 million). The facility will be capable of manufacturing silicone fluids, silicone emulsions, and silicone elastomer gels.

Key Silicone Companies:

Elkay Chemicals Pvt. Ltd.

Supreme Silicones

Shin-Etsu Chemical Co., Ltd.

Silchem Inc.

Silteq Ltd

Amul Polymers

Wacker Chemie AG

Specialty Silicone Products, Inc.

Illinois Tool Works Inc.

Evonik Industries AG

Hutchinson

Kemira Oyj

Dow Inc.

Nano Tech Chemical Brothers Private Limited

Elkem ASA

Order a free sample PDF of the Silicone Market Study, published by Grand View Research.

0 notes

Text

"The Rise of Bio Polyurethane: Real Innovation or Just Marketing Hype?"

Introduction

Bio polyurethane is a sustainable alternative to traditional petroleum-based polyurethane, produced from renewable resources like vegetable oils or other biomass. This eco-friendly material is increasingly used in various applications, including foams, coatings, adhesives, and elastomers. With the growing emphasis on sustainability and reducing carbon footprints, the demand for bio polyurethane is rising across industries such as automotive, construction, and furniture. This report examines the bio polyurethane market, exploring its dynamics, regional trends, segmentation, competitive landscape, and future outlook.

Market Dynamics

Drivers

Growing Demand for Sustainable Materials: The increasing awareness of environmental issues and the push for sustainable practices drive the demand for bio polyurethane. Industries are seeking greener alternatives to traditional materials, making bio polyurethane an attractive option.

Government Regulations and Incentives: Government regulations aimed at reducing carbon emissions and promoting the use of renewable resources are supporting the growth of the bio polyurethane market. Incentives and subsidies for green technologies further boost market adoption.

Advancements in Bio-Based Technologies: Ongoing research and development in bio-based materials are enhancing the performance and cost-effectiveness of bio polyurethane. Improved properties, such as durability and versatility, are expanding its applications.

Challenges

High Production Costs: The production of bio polyurethane can be more expensive than traditional polyurethane due to the cost of raw materials and processing. This cost disparity can be a barrier to widespread adoption, especially in price-sensitive markets.

Limited Raw Material Availability: The availability of raw materials for bio polyurethane production, such as specific vegetable oils, can be limited and subject to price fluctuations. This dependence on agricultural resources can lead to supply chain vulnerabilities.

Performance Limitations: While bio polyurethane offers environmental benefits, it may not always match the performance characteristics of traditional polyurethane in certain applications. Addressing these performance gaps is crucial for broader market acceptance.

Opportunities

Expansion into Emerging Markets: Emerging markets, particularly in Asia-Pacific and Latin America, present significant growth opportunities for bio polyurethane. Rapid industrialization, urbanization, and increasing environmental awareness are driving demand for sustainable materials in these regions.

Innovation in Applications: Developing new applications for bio polyurethane, such as in bioplastics and advanced composites, offers opportunities for market expansion. Innovations that enhance the material's performance and cost-competitiveness will likely drive further growth.

Partnerships and Collaborations: Collaborations between bio polyurethane producers, research institutions, and end-users can lead to the development of customized solutions that meet specific industry needs. Such partnerships can accelerate market adoption and innovation.

Sample Pages of Report: https://www.infiniumglobalresearch.com/reports/sample-request/1083

Regional Analysis

North America: The North American market for bio polyurethane is driven by stringent environmental regulations, a strong focus on sustainability, and growing demand from industries such as automotive and construction. The U.S. and Canada are leading markets, with increasing investments in green technologies.

Europe: Europe has a mature market for bio polyurethane, supported by robust regulatory frameworks promoting the use of renewable resources. Countries like Germany, France, and the UK are key markets, with strong demand from the automotive and furniture sectors.

Asia-Pacific: The Asia-Pacific region is experiencing rapid growth in the bio polyurethane market, fueled by industrialization, urbanization, and rising environmental awareness. China, India, and Japan are significant markets, with expanding applications in construction, packaging, and automotive industries.

Latin America: In Latin America, the market for bio polyurethane is growing due to increasing industrialization and a focus on sustainable practices. Brazil and Mexico are leading markets, with demand driven by the construction and automotive sectors.

Middle East & Africa: The market in the Middle East and Africa is in the early stages of development, with growing interest in sustainable materials. The demand for bio polyurethane is expected to rise as industries in the region adopt greener practices.

Market Segmentation

By Type:

Flexible Bio Polyurethane

Rigid Bio Polyurethane

Coatings

Adhesives & Sealants

Elastomers

Others

By Application:

Automotive

Construction

Furniture & Bedding

Packaging

Footwear

Others

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Competitive Landscape

Market Share of Large Players: Large players like BASF SE, Dow Inc., and Covestro AG dominate the bio polyurethane market, leveraging their extensive research capabilities, global presence, and strong supply chains.

Price Control: Major players have some control over pricing due to their scale and market influence. However, the price of bio polyurethane remains higher than traditional polyurethane, which affects market dynamics.

Competition from Small and Mid-Size Companies: Smaller and mid-size companies are challenging the large players by focusing on niche markets and offering innovative, customized bio polyurethane solutions. These companies often cater to specific regional demands or specialized applications.

Key Players:

BASF SE

Dow Inc.

Covestro AG

Huntsman Corporation

Lubrizol Corporation

Report Overview: https://www.infiniumglobalresearch.com/reports/global-bio-polyurethane-market

Future Outlook

New Product Development: Developing new bio polyurethane products with enhanced performance characteristics and lower costs is crucial for market growth. Companies investing in R&D to innovate and improve bio polyurethane formulations are likely to gain a competitive edge.

Sustainability: The growing emphasis on sustainability continues to drive demand for bio polyurethane. Companies that prioritize sustainable sourcing, production, and product development will resonate strongly with environmentally conscious consumers and industries.

Conclusion

The bio polyurethane market is poised for growth, driven by increasing demand for sustainable materials, government support, and advancements in bio-based technologies. While challenges such as high production costs and raw material limitations exist, opportunities in emerging markets and innovation in applications present significant potential for expansion. Companies that focus on new product development and sustainability are well-positioned to succeed in this evolving market, meeting the needs of industries seeking greener alternatives.

0 notes

Text

Aircraft Tires Procurement Intelligence: Key Factors to Consider

The aircraft tires category is anticipated to grow at a CAGR of 5.5% from 2023 to 2030. The U.S. is the world's largest market, with a share of 40%, while Europe is the second largest with 33%. Michelin, Goodyear, Bridgestone, and Dunlop are among the leading manufacturers, accounting for approximately 85% of the market.

This category is driven by the demand for military aircraft, UAVs, and commercial planes. They experience wear and tear during takeoff, landing, and taxiing due to intense temperatures and pressures. The condition of the tires is influenced by a series of factors, e.g. weather, rough landing conditions, crossing winds, Antiskid braking actions, and rough runway surfaces, all leading to frequent tire replacement or retreading which leads to increased growth in this category.

RFID technology was implemented in the aircraft tire sector in 2021, allowing for efficient and automated tracking of tire information. Michelin introduced its "RFID-enabled Connected Tire" solution, which incorporates RFID tags embedded in the tires. This technology enables real-time monitoring of tire condition and performance, helping airlines and maintenance teams manage maintenance schedules, identify potential issues, and optimize tire usage. It improves operational efficiency, reduces manual data entry errors, and enhances safety and maintenance practices. The use of elastomers in tire manufacturing improves performance significantly. Tire rubber's chemical systems benefit from intermediates that give durability, flexibility, and reliable seal qualities that elastomers provide directly.

Business jets are adopting tubeless tires, which are expected to be adopted by commercial planes as well. Hence, the tubeless tire segment is expected to grow by 3.4% between 2022 and 2030. Furthermore, the usage of elastomers reduces tire maintenance costs while improving traction. Heat and cold resistance also improve, extending tire life and assisting in maintaining optimum inflation throughout temperature changes.

Order your copy of the Aircraft Tires Procurement Intelligence Report, 2023 – 2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

The Covid-19 pandemic has had a negative impact on the aviation tire industry, causing manufacturing to decline and export activities to shift to other modes of transportation. Even when the lockdown was relaxed, the production rate was not enough to meet demand.

This sector is dominated by Goodyear, Michelin, Dunlop Aircraft Tires, and Bridgestone, leading to an oligopolistic structure that controls 85% of the market share and accounts for most of the retread. The industry is subject to strict regulations and certifications to ensure safety and compliance with international standards. New entrants face high entry barriers due to the research and development required to meet stringent safety and performance standards. The procurement of this category requires consideration of several factors, such as tire size, load capacity, speed rating, aircraft type, and operational conditions and construction

Natural and synthetic rubber are the primary raw materials used in the production of aircraft tires. The raw materials account for around 65 % to 75 % of the production costs, with natural and synthetic rubber as major raw materials. Tires used in commercial planes cost USD 1,200 to USD 5,500. Commercial aircraft tires, on the other hand, are more difficult to locate in a distributor's store. The majority of airlines have long-standing relationships with tire manufacturers. These agreements allow manufacturers to subsidize the cost of each tire unit. Airlines and tire manufacturers have a lease agreement under which the manufacturer owns the tires and the airline pays for each landing cycle. The manufacturer also covers all necessary maintenance costs under this agreement.

Browse through Grand View Research’s collection of procurement intelligence studies:

• Bearings Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

• Conveyor Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

Aircraft Tires Procurement Intelligence Report scope

• Aircraft Tires Category Growth Rate: CAGR of 5.5% from 2023 to 2030

• Pricing Growth Outlook: 6 - 8%

• Pricing Models: Volume-based pricing model, spot pricing model

• Supplier Selection Scope: Quality and Reliability, Cost and pricing, Past engagements, Productivity, Geographical presence

• Supplier selection criteria: Product Range and Compatibility, Manufacturing Capacity and Facilities, Sustainability and Environmental Responsibility, technical specifications, operational capabilities, regulatory standards and mandates, category innovations, and others.

• Report Coverage: Revenue forecast, supplier ranking, supplier matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Key companies

• Michelin

• Goodyear

• Bridgestone

• Dunlop

• Safran

• Honeywell Internationalc

• Meggit

• GKN Aerospace

• Rosen Aviation

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

• Market Intelligence involving – market size and forecast, growth factors, and driving trends

• Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

• Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

• Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions

#Aircraft Tires Procurement Intelligence#Aircraft Tires Procurement#Procurement Intelligence#Aircraft Tires Market#Aircraft Tires Industry

0 notes

Text

Silicone Elastomers Market Growth: Key Trends and Opportunities

Silicone Elastomers Market to Reach $15.1 Billion by 2031: Key Drivers and Trends

According to the latest publication from Meticulous Research®, the silicone elastomers market is set to reach $15.1 billion by 2031, growing at a compound annual growth rate (CAGR) of 7.9% from 2024 to 2031. This growth is driven by the increasing utilization of silicone elastomers in medical devices, advancements in material science, and the high demand from the electrical & electronics industry. However, environmental concerns, sustainability issues, and stagnant growth in developed countries are restraining market expansion. Additionally, the integration of silicone elastomers with IoT devices and the rising demand for automotive applications present new growth opportunities. The market, however, faces challenges from fluctuations in raw material prices.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5844

The market is segmented by type into room-temperature vulcanize (RTV), liquid silicone rubber (LSR), and high-temperature vulcanize (HTV). In 2024, the HTV segment is expected to dominate with over 52% of the market share. This dominance is due to advancements in manufacturing technologies and the increasing use of HTV in industries such as automotive, aerospace, healthcare, and electronics, where high temperatures are common. The demand for HTV continues to grow as industries prioritize safety, efficiency, and durability in their products and processes. Meanwhile, the LSR segment is anticipated to register the highest CAGR during the forecast period, driven by innovations in material science and the demand for biocompatible materials.

Based on the process, the silicone elastomers market is divided into extrusion, molding, calendering, and other processes. The molding process segment is expected to hold the largest share of over 45% in 2024. This segment's large market share is attributed to the increasing demand for LSR injection molding for creating complex parts and advancements in molding technologies. The growing need for molding processes for the mass production of silicone elastomer parts across various industries further boosts this segment. Additionally, the molding process segment is projected to witness the highest CAGR during the forecast period due to ongoing technological advancements.

The end-use industries for silicone elastomers include automotive, aviation & aerospace, consumer goods, electrical & electronics, healthcare, energy, industrial machinery, construction, and other sectors. In 2024, the electrical & electronics segment is expected to account for the largest share of above 35%. This is due to the increasing use of silicone elastomers in manufacturing components such as power supplies, circuit boards, and LED lighting components. The healthcare segment is projected to register the highest CAGR during the forecast period, driven by the demand for biocompatible materials for medical devices and various implants.

Geographically, the silicone elastomers market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific is expected to dominate the market in 2024 with over 53% of the market share. The region's growth is fueled by rapid economic development, particularly in China and India, and the growing healthcare and construction industries. Increased government investments in infrastructure projects and the adoption of silicone elastomers in various industries further drive market growth. Asia-Pacific is also projected to register the highest CAGR of over 9% during the forecast period.

Key players in the silicone elastomers market include Momentive Performance Materials, Inc. (U.S.), China National Bluestar (Group) Co, Ltd. (China), The Dow Chemical Company (U.S.), Shin-Etsu Chemical Co., Ltd. (Japan), Wacker Chemie AG (Germany), DuPont de Nemours, Inc. (U.S.), Specialty Silicone Products, Inc. (U.S.), Reiss Manufacturing, Inc. (U.S.), MESGO S.p.A.(Italy), Rogers Corporation (U.S.), Stockwell Elastomerics, Inc. (U.S.), Zhejiang Xinan Chemical Industrial Group Co., Ltd. (China), Marsh Bellofram Group of Companies (U.S.), Cabot Corporation (U.S.), and CHT Germany GmbH (Germany).

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#SiliconeIndustry#Elastomers2024#MarketDynamics#SiliconeTechnology#PolymerMarket#MaterialScience#IndustrialInnovation#SiliconeApplications#FutureMaterials#SustainableElastomers#SiliconeElastomersMarket#IndustryTrends#MarketGrowth#SiliconeSolutions#ElastomerInnovation

0 notes

Text

Silicone Elastomers Market Future Trends to Look at | BIS Research

Silicone Elastomers are a class of synthetic polymers known for their exceptional flexibility, durability, and resistance to extreme temperatures and environmental conditions

The Silicone Elastomers market was valued at $19.18 billion in 2022, and it is expected to grow at a CAGR of 8.51% and reach $45.37 billion by 2032.

At BIS Research, we focus exclusively on technologies related to precision medicine, medical devices, life sciences, artificial intelligence (AI), machine learning (ML), Internet of Things (IoT), big data, blockchain technology, Silicone Elastomers Material , advanced materials and chemicals, agriculture and FoodTech, mobility, robotics, and aerospace and defense, among others.

Silicone Elastomers Overview

The silicone elastomers encompass synthetic rubber materials derived from silicone polymers. These elastomers, formulated with reactive linear molecules, cross-linking agents, and reinforcement materials, offer exceptional mechanical properties, including elasticity, tear strength, and resilience. Their high flexibility and ability to withstand mechanical stress without permanent deformation make them ideal for dynamic applications. Notably, silicone elastomers exhibit superior heat resistance, enduring temperatures from -50°C to over 200°C, making them suitable for extreme environments.

The silicone elastomers are defined by the versatile applications of synthetic rubber materials derived from silicone polymers. These elastomers are created by compounding reactive linear molecules with cross-linking agents and reinforcement materials, resulting in excellent mechanical properties such as elasticity, tear strength, and resilience. Known for their flexibility and ability to endure mechanical stress without permanent deformation, silicone elastomers are ideal for dynamic uses

Market Drivers

By Advancements in the Electronics and Electrical Sectors

Growing demand in Automotive Industry

Advancements in Medical Technology

Rising Electronics and Electrical Sector

Sustainability Trends

Growing Consumer Goods

Key Companies

Dow

Wacker Chemie AG

Momentive Performance Materials

Shin-Etsu Chemical Co., Ltd.

China National Bluestar (Group) Co., Ltd.

Rogers Corporation

Cabot Corporation

Reiss Manufacturing Inc.

MESGO S.p.A.

CHT Germany GmbH

Bellofram Elastomers

Grab a look at the report page click here !

Market Segmentation for Silicone Elastomers

By End User Industry

By Type

By Process

By Region

Recent Developments in the Global Silicone Elastomers Market

• In June 2024, Wacker Chemie AG announced the construction of a new production site in Karlovy Vary, Czech Republic, marking a significant step in enhancing its focus on silicone specialties in Europe.

• In January 2024, SIGMA Engineering and Momentive Performance Materials announced a strategic partnership aimed at optimizing material data for silicone elastomers to enhance the reliability of process simulations using SIGMASOFT Virtual Molding.

• In April 2022, Shin-Etsu Chemical Co., Ltd. announced the development of its new TC-BGI Series, a thermal interface silicone rubber sheet designed for high-voltage electric vehicle components. This series addresses the growing demand for electric cars, which require smaller, lighter components with high energy density.

Have a look at the free sample click here !

Applications of Silicone Elastomers Market

Automotive Industry: Seals, gaskets, and hoses.

Medical Devices: Implants, seals, and flexible tubing.

Electronics: Insulating components and encapsulation.

Consumer Goods: Kitchenware, seals, and flexible membranes.

Visit our Next Generation Fuel/ Energy Storage Solutions

Key Players

Dow

Henkel

Chase Corporation

H.B. Fuller

Electrolube

Conclusion

In conclusion, the Silicone Elastomers market serves as the backbone of global communication, addressing the need for rapid and reliable data transmission. The growth of this market is fueled by technological advancements, the expanding telecommunications landscape, emerging 6G sector and the ongoing digital transformation.

The increasing adoption of 5G networks, the rise of cloud computing, and the growth of data centers are key factors propelling the demand for both Silicone Elastomers s.

Silicone Elastomers are integral to the functioning of the digital economy, enabling seamless communication, connectivity, and data sharing across industries, homes, and businesses.

0 notes

Text

Cyclodextrin Market Trends, Demand & Future Scope till 2032

Cyclodextrin Market provides in-depth analysis of the market state of Cyclodextrin manufacturers, including best facts and figures, overview, definition, SWOT analysis, expert opinions, and the most current global developments. The research also calculates market size, price, revenue, cost structure, gross margin, sales, and market share, as well as forecasts and growth rates. The report assists in determining the revenue earned by the selling of this report and technology across different application areas.

Geographically, this report is segmented into several key regions, with sales, revenue, market share and growth Rate of Cyclodextrin in these regions till the forecast period

North America

Middle East and Africa

Asia-Pacific

South America

Europe

Key Attentions of Cyclodextrin Market Report:

The report offers a comprehensive and broad perspective on the global Cyclodextrin Market.

The market statistics represented in different Cyclodextrin segments offers complete industry picture.

Market growth drivers, challenges affecting the development of Cyclodextrin are analyzed in detail.

The report will help in the analysis of major competitive market scenario, market dynamics of Cyclodextrin.

Major stakeholders, key companies Cyclodextrin, investment feasibility and new market entrants study is offered.

Development scope of Cyclodextrin in each market segment is covered in this report. The macro and micro-economic factors affecting the Cyclodextrin Market

Advancement is elaborated in this report. The upstream and downstream components of Cyclodextrin and a comprehensive value chain are explained.

Browse More Details On This Report at @https://www.globalgrowthinsights.com/market-reports/cyclodextrin-market-100564

Global Growth Insights

Web: https://www.globalgrowthinsights.com

Our Other Reports:

Blood Clot Retrieval Devices MarketMarket Growth Rate

Waste Derived Biogas MarketMarket Forecast

Global Cosmetic Lasers MarketMarket Size

Clinical Trial Patient Recruitment Services MarketMarket Growth

Geosynthetics MarketMarket Analysis

Portable Solar Charger MarketMarket Size

Global Polyolefin Elastomers (POE) MarketMarket Share

Global Wireless Gigabit MarketMarket Growth

Underwater ROV MarketMarket

Recreation Management Software MarketMarket Share

Construction Management Software MarketMarket Growth Rate

Screenless Display MarketMarket Forecast

Global Sheep Milk Soap MarketMarket Size

Healthcare Education Learning Management System MarketMarket Growth

Gastroenterology MarketMarket Analysis

Alf3 (Aluminium Fluoride) MarketMarket Size

Global Tamping Machine MarketMarket Share

Global Fixed Wing Unmanned Aerial Vehicles MarketMarket Growth

In-wheel Motors MarketMarket

Indoor Location-based Services (LBS) MarketMarket Share

Pvc Cling Film MarketMarket Growth Rate

Membrane Distillation MarketMarket Forecast

Global Defatted Wheat Germ Powder MarketMarket Size

Sequins Apparels MarketMarket Growth

Gene Sequencing MarketMarket Analysis

CNC Video Measuring MarketMarket Size

Global Hospital Commode MarketMarket Share

Global Fireproofing Material MarketMarket Growth

Microplate Reader MarketMarket

Sulfonated Melamine Formaldehyde Condensate MarketMarket Share

Comic Book MarketMarket Growth Rate

Patient Engagement Software MarketMarket Forecast

Global Ultralight and Light Aircraft MarketMarket Size

Neuropathy Screening Devices MarketMarket Growth

Panoramic Camera APP MarketMarket Analysis

Automatic Capacitor Winding Machine MarketMarket Size

Global Fin Seal Overwrapping Machine MarketMarket Share

Global Mine Escape Rescue Capsule MarketMarket Growth

Beating Heart Surgery Stabilizer MarketMarket

Ultrasonic Thickness Coating Gauge MarketMarket Share

0 notes

Text

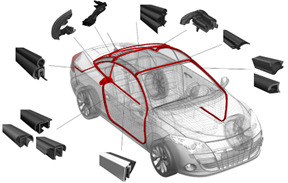

Global Top 15 Companies Accounted for 57% of total Automotive Body Sealing Systems market (QYResearch, 2021)

Body sealing system is commonly made of EPDM rubber and PVC, a thermoplastic elastomer (TPE) mix of plastic and rubber, and a thermoplastic olefin (TPO) polymer/filler blend. The goal of body sealing system is to prevent rain and water from entering entirely or partially and accomplishes this by either returning or rerouting water. A secondary goal of body sealing system is to keep interior air in, thus saving energy on heating and air conditioning.

The automotive body sealing system means the edges of a vehicle's windshield, windows, doors and trunk lid, etc. Automobile Sealing System strip is usually made into a hollow sponge foam tube.

According to the new market research report “Global Automotive Body Sealing Systems Market Report 2023-2029”, published by QYResearch, the global Automotive Body Sealing Systems market size is projected to reach USD 25.95 billion by 2029, at a CAGR of 13.3% during the forecast period.

Figure. Global Automotive Body Sealing Systems Market Size (US$ Million), 2018-2029

Figure. Global Automotive Body Sealing Systems Top 15 Players Ranking and Market Share(Based on data of 2021, Continually updated)

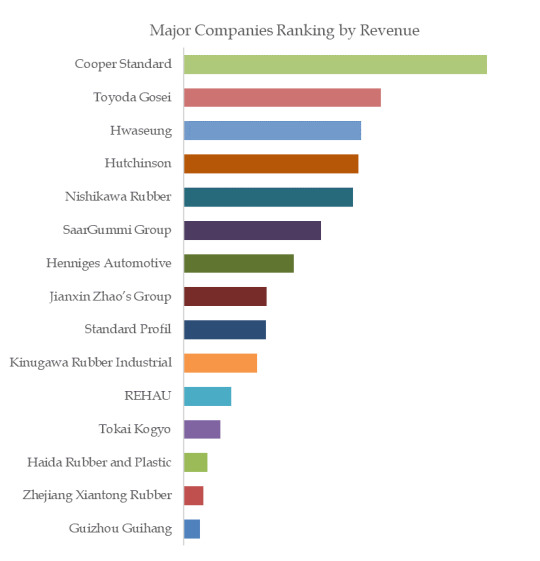

The global key manufacturers of Automotive Body Sealing Systems include Cooper Standard, Toyoda Gosei, Hwaseung, Hutchinson, Nishikawa Rubber, SaarGummi Group, Henniges Automotive, Jianxin Zhao’s Group, Standard Profil, Kinugawa Rubber Industrial, etc. In 2021, the global top five players had a share approximately 57.0% in terms of revenue.

About QYResearch