#COVID-19 Impact On Medical Plastics Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 44% of users from Denmark used Tumblr daily.

Text

Exploring the Global Growth of the Sex Reassignment Surgery Market: Key Insights and Trends

Exploring the Global Growth of the Sex Reassignment Surgery Market: Key Insights and Trends

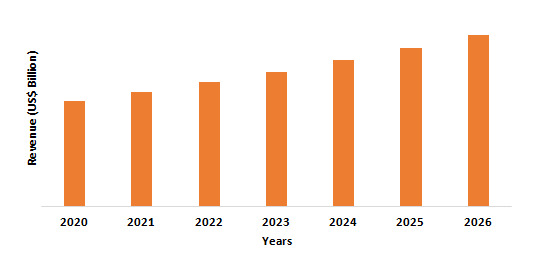

As society moves towards greater inclusivity and acceptance of diverse identities, the global market for sex reassignment surgery (SRS) has witnessed substantial growth. According to recent data, this market was valued at $8.4 billion in 2023 and is expected to skyrocket to $111.718 million by 2031, growing at an impressive CAGR of 31.6% from 2024 to 2031. This surge underscores the increasing demand for gender-affirming healthcare worldwide.

Understanding Sex Reassignment Surgery

Sex reassignment surgery (SRS) refers to a collection of surgical procedures designed to align an individual's physical characteristics with their gender identity. This can include vaginoplasty, phalloplasty, breast augmentation, and facial feminization surgery, depending on whether the transition is from male to female (MTF) or female to male (FTM). Beyond surgery, this transition often involves hormone therapy and psychological support to ensure a holistic transformation, aiming to improve quality of life and reduce gender dysphoria.

Browse Link : https://www.statsandresearch.com/report/40446-global-sex-reassignment-surgery-market/

Market Dynamics and Impact of COVID-19

The COVID-19 pandemic had a notable impact on the healthcare sector, including the SRS market. With disruptions in elective surgeries and medical services, the market faced challenges. However, as healthcare systems adapt and prioritize gender-affirming care, the market shows a resilient recovery trajectory.

Regional Insights: Global Footprint

The SRS market spans across North America, Asia-Pacific, Europe, the Middle East and Africa, and South America. Key countries like the United States, China, Japan, India, and Brazil lead in market activity, driven by growing awareness and improved medical facilities. Each region presents unique dynamics, from the advanced healthcare infrastructure in North America and Europe to the increasing acceptance and medical tourism in Asia-Pacific.

Get A Free Sample Here : https://www.statsandresearch.com/request-sample/40446-global-sex-reassignment-surgery-market

Competitive Landscape: Key Players Shaping the Market

Leading the charge in this evolving market are key players such as:

Cleveland Clinic

Mayo Clinic

Johns Hopkins Medicine

Massachusetts General Hospital

Stanford Health Care

The Gender Confirmation Center

Chrysalis Health

Beverly Hills Plastic Surgery

Dr. Toby Meltzer

Dr. Sherman Leis

These institutions and professionals are at the forefront, offering cutting-edge procedures and compassionate care. Their role is critical in advancing both the medical and social aspects of gender-affirming healthcare.

Procedure Types: MTF and FTM Surgeries

Procedures vary widely based on the transition pathway:

Male-to-Female (MTF): Common surgeries include vaginoplasty, breast augmentation, and facial feminization surgery. These procedures help align an individual’s body with their gender identity, enhancing both physical appearance and psychological well-being.

Female-to-Male (FTM): Surgeries like top surgery (chest reconstruction), phalloplasty, and metoidioplasty are key. They focus on creating a masculine physique and, in some cases, reconstructing genitalia for functional and aesthetic alignment.

The Role of Medical Professionals

A successful transition requires a multidisciplinary team:

Surgeons: Perform the actual procedures, ensuring alignment with the patient’s identity and medical needs.

Endocrinologists: Manage hormone therapy to develop secondary sexual characteristics.

Psychiatrists/Psychologists: Provide mental health support, preparing individuals for surgery and assisting with emotional resilience.

Where the Surgeries Take Place

SRS is conducted in various settings, from comprehensive hospitals to specialized clinics and general healthcare facilities. Each offers a unique approach, balancing personalized care with medical excellence.

For Enquiry : https://www.statsandresearch.com/enquire-before/40446-global-sex-reassignment-surgery-market

The Road Ahead

With a projected CAGR of 31.6% from 2024 to 2031, the SRS market is set for rapid expansion. As societal acceptance grows and medical technologies advance, more individuals are seeking these life-changing procedures.

The journey towards comprehensive gender-affirming care continues, driven by both market forces and a deepening understanding of the needs of transgender individuals. This growing market not only reflects economic potential but also the human stories behind each transition, advocating for a world where everyone can live authentically.

Find Out Top Trending Reports Here :

Global Sex Reassignment Surgery Market

Global Enzyme Engineering Market

Global Neuroelectronic Devices Market

Global Vitamin K2 Market Insights

Global Defibrillator Market Insights

1 note

·

View note

Text

Rising Demand for Aesthetic Procedures: Impact on the Scar Treatment Market

The global scar treatment market size is expected to reach USD 4.94 billion by 2030, and is expected to expand at 11.5% CAGR from 2024 to 2030, according to a new report by Grand View Research, Inc. Scar treatment market is developing at a fast rate due to the growing awareness among people regarding aesthetics.

The appearance of different types of scars poses a huge challenge to the day-to-day lifestyle of victims while affecting their aesthetic appeal. Hence, this factor is expected to develop an increased need for scar treatment. Acne scars are one of the most common concerns for women, which disrupt their aesthetic appeal, making them uncomfortable. Consequently, the demand for scar treatment products is expected to rise, owing to the growing concern for aesthetics.

The aesthetic industry witnessed significant setbacks due to the COVID-19 pandemic in the second and third quarters of 2020. Since the majority of procedures were not medical necessities, lockdowns in several countries led to the closure of beauty clinics, med spas, dermatology clinics, and retail stores. However, online consultancy helps patients overcome these problems.

The increasing number of road accidents globally continues to lead to several face and body marks, which frequently need surgical treatment. As a result, patients who have undergone such procedures are usually given topical scar reduction products. Cosmetic surgeries using laser instruments are also gaining popularity to treat severe road accident scars. A victim's daily life is hampered by post-burn marks. Plastic surgeries or resurfacing laser therapies are being used to remove these marks.

Scar removal products that are technologically advanced are widely available on the market, which reduces pain and makes scar treatment a simple process. For instance, UltraPulse by Lumenis uses CO2 laser to treat acne scars, which reduces the risk of pain during the treatment process.

Scar Treatment Market Report Highlights

Topical products dominated the market in 2023 due to the higher adoption of creams and gels for treating scars, such as acne, surgical marks, and burns

Laser products are anticipated to witness the highest growth over the forecast period due to the continuous introduction of technically advanced laser instruments

Atrophic scars held the largest share in 2023 as acne prevalence remains more common among women, who constitute the majority of the target population

North America dominated the market in 2023 owing to the high penetration of laser-based products in scar treatment and skin rejuvenation

Scar Treatment Market Segmentation

Grand View Research has segmented the global scar treatment market report based on product, scar type, end-use, and region:

Scar Treatment Product Outlook (Revenue, USD Million, 2018 - 2030)

Topical Products

Creams

Gels

Silicon Sheets

Others

Laser Products

CO2Laser

Pulse-dyed Laser

Others

Injectables

Others

Scar Treatment Scar Type Outlook (Revenue, USD Million, 2018 - 2030)

Atrophic Scars

Hypertrophic & Keloid Scars

Contracture Scars

Stretch Marks

Scar Treatment End-use Outlook (Revenue, USD Million, 2018 - 2030)

Hospitals

Clinics

Homecare

Scar Treatment Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Europe

Germany

UK

Spain

France

Italy

Russia

Denmark

Norway

Sweden

Asia Pacific

China

India

Japan

South Korea

Australia

Thailand

Latin America

Brazil

Mexico

Argentina

MEA

South Africa

Saudi Arabia

UAE

Kuwait

Key Players in Scar Treatment Market

Smith & Nephew PLC

Lumenis

Enaltus LLC

Merz Pharmaceuticals, LLC

Sonoma Pharmaceuticals, Inc.

Cynosure

Scar Heal Inc.

CCA Industries, Inc.

Newmedical Technology Inc.

Mölnlycke Health Care AB

Suneva Medical

Pacific World Corporation

Perrigo Company plc

Order a free sample PDF of the Scar Treatment Market Intelligence Study, published by Grand View Research.

0 notes

Text

Non Woven Fabric Prices: Trends and Insights for 2025

Non-woven fabrics have become an essential component in industries ranging from healthcare to automotive, construction, and packaging. These versatile materials are lightweight, durable, and cost-effective, making them a preferred choice for various applications. As we enter 2025, the prices of non-woven fabrics remain a critical area of interest for manufacturers, suppliers, and consumers alike. This article delves into the key factors influencing non-woven fabric prices, recent trends, and market projections.

Get Real time Prices for Non-Woven Fabric: https://www.chemanalyst.com/Pricing-data/non-woven-fabric-1089

Key Factors Influencing Non-Woven Fabric Prices

Raw Material Costs The primary raw materials for non-woven fabrics include polypropylene (PP), polyester (PET), and viscose. Fluctuations in the prices of these raw materials significantly impact the overall cost of non-woven fabrics. For instance, the volatility in crude oil prices directly affects polypropylene costs, as it is a petroleum-derived product. Similarly, supply chain disruptions or increased demand for polyester and viscose can lead to price hikes.

Supply Chain Dynamics Global supply chain disruptions, driven by geopolitical tensions, natural disasters, or pandemic-related restrictions, have a cascading effect on the availability and cost of non-woven fabrics. Shipping delays, increased freight charges, and labor shortages further exacerbate the situation.

Demand Fluctuations The demand for non-woven fabrics is heavily influenced by their end-use industries. For example, during the COVID-19 pandemic, the demand for medical-grade non-woven fabrics surged due to their use in masks, gowns, and other protective gear. On the other hand, demand may decrease in other sectors during economic slowdowns.

Technological Advancements Innovations in production techniques can either reduce costs or introduce premium-priced products. For example, advancements in spunbond and meltblown technologies have improved efficiency, potentially lowering production costs while enhancing product quality.

Environmental Regulations Growing environmental awareness and stricter regulations around single-use plastics have prompted manufacturers to explore sustainable alternatives. While eco-friendly non-woven fabrics may be more expensive to produce initially, they are gaining traction, influencing overall market pricing.

Recent Trends in Non-Woven Fabric Prices

Price Stabilization Post-Pandemic: After the price spikes during the pandemic due to unprecedented demand, the market has witnessed relative stabilization. However, prices remain higher than pre-pandemic levels due to persistent supply chain challenges.

Regional Variations: Non-woven fabric prices vary across regions based on local raw material availability, production capacity, and demand. For instance, Asia-Pacific, being a major producer, often enjoys lower prices compared to North America and Europe.

Shift Towards Sustainability: The increasing adoption of biodegradable and recycled non-woven fabrics has introduced a new pricing segment. While these products are costlier, their growing popularity is expected to influence standard non-woven fabric prices.

Market Projections for 2025

In conclusion, the pricing dynamics of non-woven fabrics in 2025 will be shaped by a blend of economic, technological, and environmental factors. Stakeholders must stay informed about global market trends and raw material developments to make strategic decisions. As sustainability continues to gain prominence, it will be interesting to observe how it reshapes the cost structure and consumer preferences in the non-woven fabric industry.

Get Real time Prices for Non-Woven Fabric: https://www.chemanalyst.com/Pricing-data/non-woven-fabric-1089

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Non Woven Fabric#Non Woven Fabric Price#Non Woven Fabric Prices#india#united kingdom#united states#germany#business#research#chemicals#Technology#Market Research#Canada#Japan#China

0 notes

Text

Medical Packaging Films Market

Medical Packaging Films Market Size, Share, Trends: Amcor plc Leads

Leveraging Sustainable and Eco-Friendly Packaging Solutions

Market Overview:

The global Medical Packaging Films Market is experiencing remarkable growth, driven by several key factors. The expanding healthcare industry, coupled with the increasing demand for flexible packaging solutions and stringent regulations governing medical packaging, is propelling the market forward. North America currently dominates the market, accounting for approximately 35% of the global market share, thanks to its advanced healthcare infrastructure. As the global population ages and chronic diseases become more prevalent, there is a growing need for innovative packaging solutions that ensure the safety, efficacy, and longevity of medical products. Additionally, the COVID-19 pandemic has further accelerated the demand for medical packaging films, particularly for the production of personal protective equipment (PPE) and diagnostic kits.

DOWNLOAD FREE SAMPLE

Market Trends:

A significant trend in the medical packaging films market is the increased demand for sustainable and eco-friendly packaging solutions. This shift is driven by growing environmental concerns, regulatory pressures, and changing consumer preferences. Manufacturers are increasingly focusing on developing biodegradable, compostable, and recyclable materials to reduce the environmental impact of their products. Bio-based polymers, such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA), are emerging as popular alternatives to traditional petroleum-based plastics. This trend towards sustainability is crucial as it aligns with global efforts to reduce carbon footprints and promote environmental stewardship in the healthcare sector.

Market Segmentation:

In the medical packaging films market, polyethylene (PE) stands out as the dominant material segment. This thermoplastic polymer is highly valued for its versatility, cost-effectiveness, and superior barrier properties. PE films exhibit exceptional moisture resistance, ensuring that moisture-sensitive medical devices and pharmaceuticals remain uncompromised throughout their shelf life. The material's inherent flexibility allows it to accommodate a wide array of medical items, from small tablets to large surgical instruments. One of PE's standout features is its excellent sealability, which is crucial for maintaining a sterile environment within the package. As of 2023, approximately 15% of PE films used in medical packaging were made from recycled or bio-based materials, with this percentage expected to reach 25% by 2026.

Market Key Players:

The medical packaging films market is characterized by intense competition, with several key players vying for market share. Major companies such as Amcor plc, Berry Global Inc., DuPont de Nemours, Inc., Weigao Group, Wipak Group, and Renolit SE are at the forefront, driving innovation and sustainability initiatives. These industry leaders are focusing on product development, strategic collaborations, and sustainability to maintain their competitive edge.

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Blood Collection Tubes Market: Key Trends Shaping the Future

The blood collection tubes market is witnessing transformative changes driven by advancements in technology, increasing demand for diagnostic testing, and the growing emphasis on patient safety. This dynamic market is evolving with the introduction of new products and solutions aimed at improving sample collection, storage, and analysis processes. Several key trends are influencing the blood collection tubes market, and they highlight the continuous innovation within the industry.

Technological Advancements in Blood Collection Tubes The development of advanced blood collection tubes is one of the most prominent trends in the market. New types of tubes with improved materials, additives, and coatings are being introduced. These innovations aim to reduce hemolysis, prevent clotting, and ensure better sample preservation. For instance, tubes with gel separators are gaining popularity as they provide better serum and plasma separation, enhancing the accuracy of diagnostic tests.

Integration of Automation and Smart Technologies Automation in laboratory procedures is a growing trend, and blood collection tubes are becoming a part of this shift. The integration of RFID (Radio Frequency Identification) and barcodes in blood collection tubes allows for seamless tracking and sample identification throughout the diagnostic process. This technology minimizes the risk of errors, enhances traceability, and improves the efficiency of laboratory operations. Automation is also helping reduce human error, which is crucial in high-volume testing environments.

Growing Focus on Point-of-Care Testing Point-of-care (POC) testing is gaining momentum, especially in remote or underserved regions where access to advanced healthcare facilities is limited. Blood collection tubes designed for POC applications are becoming increasingly important. These tubes are developed to provide quick and accurate results, enabling faster diagnostics and more effective treatment. This trend is particularly relevant in fields such as infectious diseases, where rapid testing is critical for timely medical intervention.

Sustainability and Eco-Friendly Products With growing awareness about environmental sustainability, the blood collection tubes market is seeing a shift towards eco-friendly products. Manufacturers are focusing on reducing the environmental impact of single-use plastic tubes. Biodegradable or recyclable materials are being explored to minimize the carbon footprint of these medical products. This trend is expected to increase in importance as environmental regulations become stricter and healthcare institutions adopt more sustainable practices.

Customization of Blood Collection Tubes Customization is an emerging trend in the blood collection tubes market. Manufacturers are increasingly offering tailored solutions to meet specific needs in various clinical and research applications. For example, tubes with specialized coatings or additives for specific tests, such as those used in toxicology, hematology, or microbiology, are becoming more common. This customization enables better sample preservation and more accurate results, which is crucial for specialized diagnostics.

Increase in Demand for Diagnostic Testing The growing demand for diagnostic testing, particularly in the wake of the COVID-19 pandemic, has accelerated the need for reliable blood collection tubes. With an increase in health check-ups, routine screenings, and disease surveillance programs, more blood samples are being collected globally. This trend is expected to continue as healthcare systems worldwide focus on early diagnosis and preventive care, further driving the growth of the blood collection tubes market.

Rise in Chronic Diseases and Aging Population The rise in chronic diseases such as diabetes, cancer, and cardiovascular conditions, along with the aging population, is creating a higher demand for diagnostic testing, which in turn fuels the need for blood collection tubes. As the elderly population continues to grow, there is an increased focus on monitoring and managing chronic conditions, which requires frequent blood tests. This demographic shift is a key driver behind the expanding blood collection tubes market.

Innovations in Blood Collection Tube Materials Innovations in materials used for blood collection tubes are another important trend. Manufacturers are exploring new materials such as silicone-coated surfaces and advanced plastic composites that improve tube performance and reduce contamination. These materials offer enhanced stability for blood samples, making them ideal for long-term storage and transportation. These innovations also improve the tube’s resistance to breakage and leakage, enhancing safety and convenience.

Expansion in Emerging Markets Emerging markets, especially in Asia-Pacific and Africa, are becoming a significant focus for growth in the blood collection tubes market. Increasing investments in healthcare infrastructure, rising disposable incomes, and greater awareness of healthcare services are driving demand for diagnostic tests and, by extension, blood collection tubes. As healthcare facilities improve and diagnostic testing becomes more widespread, the need for reliable and high-quality blood collection products will continue to rise in these regions.

Regulatory Developments and Standards Regulatory bodies worldwide are tightening standards for blood collection tubes to ensure better quality and patient safety. Compliance with these regulations is a critical trend in the market. Manufacturers are focusing on meeting international standards for medical devices and ensuring that their products are certified and safe for use. Regulatory pressures are encouraging more rigorous quality control measures and standardization across the industry.

Rise of Liquid Biopsy The liquid biopsy market, which involves analyzing blood samples for early detection of cancers and other diseases, is growing rapidly. Blood collection tubes used for liquid biopsy are designed to maintain the integrity of the sample, ensuring accurate and reliable results. This niche market is influencing the design and functionality of blood collection tubes, as they need to be optimized for the specific requirements of liquid biopsy tests.

Improved Blood Sample Preservation Techniques Blood sample preservation has become a priority in the blood collection tubes market. Innovations in additives and preservative technologies are helping extend the shelf life of blood samples without compromising their integrity. These advancements are crucial for ensuring that samples remain viable for a range of diagnostic tests, particularly in cases where immediate analysis is not possible.

In conclusion, the blood collection tubes market is experiencing significant trends that reflect advancements in technology, sustainability, and increasing demand for diagnostic testing. These trends are shaping the future of the industry and driving innovation that will ultimately improve patient care and diagnostic outcomes globally.

0 notes

Text

Electroactive Polymers Market — By Type , By Application , By Geography — Global Opportunity Analysis & Industry Forecast, 2024–2030

Electroactive Polymers Market Overview

Request Sample :

Electroactive Polymers Market COVID-19 Pandemic

The outbreak of Covid-19 is having a huge impact on the economy of electronic devices. The COVID-19 pandemic caused an unprecedented increased demand for some medical devices, as well as significant disruptions in the manufacturing and supply chain operations of global medical devices. The FDA monitors the supply chain of medical products and works closely with producers and other stakeholders to assess the risk of disruption and to prevent or reduce its impact on patients, health care providers, and the general public’s health. In addition, there is a delay in imports and exports of medical devices due to the import-export restriction by the governments in various regions. All these factors are having a major impact on the Electroactive Polymers Market during the pandemic.

Report Coverage

The report: “Electroactive Polymers Market — Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the electroactive polymers Industry.

By Type: Ionic Electroactive Polymers (Ionic Polymer Gels (IPG), Ionic Polymer Metal Composites (IPMC), Conductive Polymers (CP), and Carbon Nanotubes (CNT)), Electronic Electroactive Polymers (Ferroelectric Polymers, Electrostrictive Graft Elastomers, Dielectric Elastomers, Electro VIscoelastic Elastomers, Liquid Crystal Elastomer (LCE), and Others), and Others.

By Application: Actuators, Sensors, Plastic, Aviation Technology, Energy Generation, Automotive Devices, Prosthetics, Robotics, and Others.

By Geography: North America (U.S., Canada, and Mexico), Europe (U.K, Germany, France, Italy, Netherland, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East, and Africa).

Inquiry Before Buying :

Key Takeaways

Asia-Pacific dominates the Electroactive Polymers Market owing to the increasing demand for the electroactive polymers industry in the region. The increasing urbanization coupled with the rising population in APAC is the major factor driving the demand for electroactive polymers.

Electroactive polymers are extensively used for corrosion-preventing coatings in ferrous and non-ferrous alloys, actuators, damped harmonic oscillator, metamorphic biomaterials, and protective fabrics points. These properties of electroactive polymers are projected to increase market growth.

Electroactive polymers due to its unique properties find application in different end-use industries. These are lighter in weight, more durable, and have better conductive properties, unlike conventional materials (metals). During the forecast period, this factor is anticipated to drive the market.

Due to the Covid-19 pandemic, most of the countries have gone under lockdown, due to which the projects and operations of various industries such as energy generation and automotive are disruptively stopped, which is hampering the Electroactive Polymers Market growth.

Electroactive Polymers Market Segment Analysis — By Type

The conductive polymers segment held the largest share in the Electroactive Polymers Market in 2020 and is growing at a CAGR 8.10% over 2024–2030. The significant class of functional materials that have certain useful properties of both organic polymers (such as strength, plasticity, flexibility, strength, elasticity) and semiconductors (such as electric conductivity) are conducting polymers (CPs). The conductive polymers are often used in miniature boxes that have the ability to open and close, micro-robots, surgical tools, surgical robots that assemble other micro-devices. In addition, conductive polymers (CPs) are extensively used as an alternative to metallic interfaces within biomedical devices as a way of imparting electroactivity to normally passive devices such as tissue scaffolds. Thus, all these extensive characteristics of conductive polymers are the key factor anticipated to boost the demand for conductive polymers in various regions during the forecast period.

Schedule A Call :

Electroactive Polymers Market Segment Analysis — By Application

The actuator segment held the largest share in the Electroactive Polymers Market in 2020 and is expected to grow with a CAGR of 7.2% for forecast period. To maximize the actuation capability and durability, effective fabrication, shaping, and electrode techniques are being developed. Many engineers and scientists from many different disciplines are attracting attention with the impressive advances in improving their actuation strain. Due to their inherent piezoelectric effect, ferroelectric polymers, such as polyvinylidene fluoride (PVDF), are largely used in manufacturing electromechanical actuators. For biomimetic applications, these materials are especially attractive, as they can be used to make intelligent robots and other biologically inspired mechanisms. To form part of mass-produced products, many EAP actuators are still emerging and need further advancements. This requires the use of models of computational chemistry, comprehensive science of materials, electro-mechanical analytical tools, and research into material processing. Which will eventually drive is the Electroactive Polymers Market during the forecast period.

Electroactive Polymers Market Segment Analysis — By Geography

Asia-Pacific region held the largest share in the Electroactive Polymers Market in 2020 up to 38%, owing to the escalating medical device industry in the region. A key factor behind the growth of the region’s electroactive polymer market is the large demand for electroactive polymers for the manufacture of advanced implant devices for medical conditions. According to Invest India, the Indian medical device sector is projected to register a CAGR of 14.8% and is expected to reach $11.9 billion in 2021–22, and the sector is projected to reach $ 65 bn industry by 2024. According to the most recent official figures from the Ministry of Health, Labour and Welfare (MHLW), the Japanese medical devices market in 2018 was roughly $29.3 billion, up about 6.9 percent from 2017 in yen terms. And from 2018 to 2023, the medical device market in Japan is estimated to show an increment of 4.5% CAGR in yen terms. Furthermore, North America also holds a prominent market share of the Electroactive Polymers Market due to the escalating medical device industry. According to the Select USA, the United States medical device market is anticipated to rise to $208 billion by the year 2023. Thus, with the expanding medical device industry, the demand for electroactive polymers will also subsequently increase, which is anticipated to drive the Electroactive Polymers Market in the Asia Pacific and North America during the forecast period.

Electroactive Polymers Market Drivers

Increasing Automotive Production

In the automotive industry, electroactive polymers are used as actuators and sensors. For materials that are light in weight but strong and durable such as an electroactive polymer, there is high demand. By using modern electroactive polymers in numerous automotive electronic components, such as multiple sensors, accelerometers, and accelerator pedal modules, car manufacturers are attempting to achieve lightweight properties. China is the world’s largest vehicle market, according to the International Trade Administration (ITA), and the Chinese government expects the production of cars to reach 35 million by 2025. According to the International Trade Administration (ITA), in 2019 the Mexican market for electric, plug-in vehicles, and hybrid vehicles reached 25,608 units, representing a 43.8% growth over 2018. Thus, increasing automation production will require more electroactive polymers for manufacturing various automotive components, which will act as a driver for the Electroactive Polymers Market during the forecast period.

Increasing Application of Electroactive Polymers

Textiles called sensing and actuating microfibers can be directly woven into electromechanical systems such as sensors, actuators, electronics, and power sources. They can be used as smart fabrics because of the flexibility and low cost of electroactive polymers. In developing intelligent fabrics, polypyrrole and polyaniline are used. In addition, using electroactive polymers in robotics for muscle development is better, as it is more cost-effective than the semiconductor and metal materials. And robotics is widely used; hence the demand for electroactive polymers will also positively affect the market growth. Furthermore, Electroactive Polymers Market growth is increasing owing to its wide usage in areas such as medical devices, damped harmonic oscillator, electric displacement field, electrostatic discharge/electromagnetic interference, high-strain sensors, and biomimetic. Hence, the increasing application of electroactive polymers acts as a driver for the Electroactive Polymers Market.

Buy Now :

Electroactive Polymers Market Challenges

Environmental Hazards Related to the Electroactive Polymers

Raw materials which are used to produce electroactive polymers (EAPs) are difficult to extract and often harmful to the environment. The disposal of waste generated by electroactive polymers is one of the major concerns (EAPs). Improper disposal of EAP products could harm the environment and ultimately impact the food chain. Manufacturers of EAPs may experience increased costs associated with the disposal of certain electroactive polymers (EAPs) that cannot be disposed of by biodegradation. The government has, therefore, enforced strict regulations on the use of such polymers. Besides, the environmental regulations on the use of petroleum products restrict the growth of the EAPs market. These factors are hampering the electroactive polymer market growth.

Electroactive Polymers Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Electroactive Polymers Market. Major players in the Electroactive Polymers Market are Solvay, Parker Hannifin, Agfa-Gevaert, 3M, Merck, Lubrizol, Novasentis, Premix, PolyOne Corporation, Celanese Corporation, and KEMET Corporation.

Key Market Players:

The Top 5 companies in the Electroactive Polymers Market are:

Merck

3M

Solvay

Parker Hannifin

Agfa-Gevaert

For more Chemicals and Materials Market reports, Please click here

#ElectroactivePolymers#SmartMaterials#ConductivePolymers#FlexibleElectronics#ShapeMemoryAlloys#PolymersInElectronics#SoftRobotics

0 notes

Text

Europe Bioplastics Market Size 2024, Trends, Revenue, Key Player, Challenges, Growth, Future Opportunities and Forecast till 2033: SPER Market Research

A more sustainable substitute for conventional plastics made from petroleum, bioplastics are novel polymers made from renewable biological sources like plants, starch, and algae. They are made to be compostable or biodegradable, which lessens the amount of plastic waste that ends up in landfills and the ocean. From packaging materials to automobile parts, bioplastics can have a wide range of qualities and uses. Furthermore, bioplastics are gaining prominence as an alternative to traditional plastics, with consumers increasingly opting for green and environmentally friendly products. Even while they seem like a promising answer to the expanding problem of plastic waste, issues including production costs, competition for resources, and infrastructure for recycling still need to be resolved before they can be settled prior to their widespread adoption.

According to SPER Market Research, ‘Europe Bioplastics Market Size- By Product Type, By Application - Regional Outlook, Competitive Strategies and Segment Forecast to 2033’ states that The Europe Bioplastic Market is estimated to reach USD XX Billion by 2033 with a CAGR of 15.37%.

Drivers:

Growing worries about petrochemical toxicity and decreasing crude oil sources have fuelled the development of bio-based polymers. Government rules limiting petrochemical consumption in specific applications, including as food packaging and medical devices, are projected to further encourage the use of bioplastics. The market has seen a surge in demand for plastic alternatives as people become more concerned about the use of plastics. This is projected to open up chances for the market in the next years. The market's producers are shifting their attention to bioplastics due to the rapid pace of innovation and new product development. To address concerns about the hazardous impacts of plastic trash, companies are constantly developing new product lines that use biodegradable and non-biodegradable bioplastics as well as recycled materials.

Request Free Sample Report: https://www.sperresearch.com/report-store/europe-bioplastics-market.aspx?sample=1

Challenges:

Despite its rapid growth, the bioplastics business in Europe confronts a number of obstacles. Their high price in comparison to traditional plastics is one of the main obstacles impeding the market's expansion. Furthermore, it is challenging to secure competitive rates for bioplastics due to the cheap cost of traditional plastics. Furthermore, improper handling, storage, and disposal of biodegradable plastic trash can result in the release of chemicals into the environment. The market for biodegradable plastics is expected to grow slowly over the forecast period due to factors like a lack of knowledge about the health risks posed by biopharma plastic waste, insufficient training for waste management staff, and the lack of waste management and disposal systems.

The COVID-19 pandemic had a huge influence on the bioplastic business in Europe, first disrupting production and supply chains due to lockdowns and limitations. However, as people became more aware of environmental issues during the crisis, the demand for sustainable materials increased. Many consumers and businesses began to prioritize environmentally friendly alternatives, resulting in investments in bioplastic breakthroughs. The transition to online purchasing has also expedited the development of biodegradable packaging solutions, emphasizing the importance of sustainable practices in e-commerce. Despite hurdles such as changing raw material availability and economic uncertainty, Europe's bioplastic business is primed for expansion, fuelled by growing regulatory backing and a collaborative commitment to reduce plastic waste and carbon footprints. The dual impact of change and renewed dedication is altering the industry environment.

Europe Bioplastic Market is dominated by Germany due to its strong environmental policies and a robust commitment to sustainability. Some of the key players in the market are Arkema, BASF SE, Braskem, Corbion, Danimer Scientific and others.

Europe Bioplastics Market Segmentation:

By Product Type: Based on the Product Type, Europe Bioplastics Market is segmented as; Bio-based Biodegradables, Bio-based Non-biodegradables.

By Application: Based on the Application, Europe Bioplastics Market is segmented as; Flexible Pakaging, Rigid Packaging, Automotive and Assembly Operations, Agriculture and Horticulture, Construction, Textiles, Electrical and Electronics, Others.

By Region: This research also includes data for Germany, Australia, Switzerland, France, Great Britain, Spain, Italy.

For More Information, refer to below link: –

Europe Bioplastics Market Outlook

Related Reports:

Europe Sodium Reduction Ingredients Market Growth, Size, Trends Analysis- By Type, By Distribution Channel- Regional Outlook, Competitive Strategies and Segment Forecast to 2033

Latin America Petrochemicals Market Growth, Size, Trends Analysis- By Product- Regional Outlook, Competitive Strategies and Segment Forecast to 2033

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant – U.S.A.

+1-347-460-2899

#Europe Bioplastics Market#Bioplastics Market#Europe Bioplastics Market Growth#Europe Bioplastics Market Trends#Europe Bioplastics Market Size#Europe Bioplastics Market Share#Europe Bioplastics Market Revenue#Europe Bioplastics Market Demand#Europe Bioplastics Market Forecast#Europe Bioplastics Market Competition#Europe Bioplastics Market Report#Europe Bioplastics Market Future Outlook#Europe Bioplastics Market Segmentation#Europe Bioplastics Market Challenges

0 notes

Text

The Global Medical-Grade Polycarbonate Resin Market: Key Trends and Future Prospects

Introduction

The healthcare industry is constantly evolving, and with it, the materials that support its innovations. One material that is making significant strides in this space is medical-grade polycarbonate resin. Renowned for its exceptional durability, transparency, and resistance to impact and heat, this resin is integral to a wide array of medical applications, from surgical instruments to drug delivery systems. As the global demand for healthcare products continues to rise, the medical-grade polycarbonate resin market is also expanding. Let’s explore the key trends, drivers, challenges, and opportunities within this dynamic market.

more details : https://www.xinrenresearch.com/reports/comprehensive-market-overview-and-insights-for-global-medical-grade-polycarbonate-resin-market-market/

What Makes Medical-Grade Polycarbonate Resin So Important?

Medical-grade polycarbonate resin is a high-performance plastic that excels in clarity, strength, and flexibility, making it an ideal choice for a variety of medical devices. Its unique properties are particularly valuable in applications requiring transparency, such as IV bags and syringes, where monitoring fluid flow is critical. Furthermore, its ability to withstand high-temperature sterilization processes ensures its effectiveness in single-use and reusable medical devices.

Key Factors Driving Market Growth

Rising Demand for Medical Devices With an aging global population and an increase in chronic diseases, the demand for medical devices is surging. Medical-grade polycarbonate resin is widely used in devices that need to be durable, clear, and suitable for sterilization, thereby propelling its market growth.

Emphasis on Infection Control and Single-Use Devices The COVID-19 pandemic has heightened the need for infection control, accelerating the trend toward single-use medical devices. Polycarbonate resin’s compatibility with sterilization processes makes it a key material for manufacturing disposable devices, reducing cross-contamination risks.

Advancements in Medical Technology As medical devices become more sophisticated, there is a growing need for materials that can meet complex performance requirements. Medical-grade polycarbonate resin is utilized in advanced devices, including diagnostic equipment and telehealth applications, due to its superior mechanical properties and versatility.

Stringent Regulatory Standards Regulatory compliance is critical in the healthcare sector. Medical-grade polycarbonate resin adheres to strict quality and safety standards set by regulatory bodies like the FDA and ISO, reinforcing its status as a trusted material for medical applications.

Emerging Trends in the Market

Sustainability Initiatives With growing awareness of environmental issues, the medical industry is increasingly prioritizing sustainability. Manufacturers are exploring methods to produce polycarbonate resin more sustainably and investigating recyclable or biodegradable alternatives.

Customization for Specific Applications The complexity of modern medical devices calls for customized materials. Manufacturers are collaborating with healthcare providers to develop tailored polycarbonate resins that meet specific needs, ensuring optimal performance in diverse medical applications.

Expansion in Emerging Markets Emerging economies are experiencing significant growth in healthcare spending and infrastructure development, creating a surge in demand for high-quality medical devices. This presents an excellent opportunity for polycarbonate resin manufacturers to expand their presence in these regions.

Enhanced Sterilization Compatibility As medical devices require rigorous sterilization, polycarbonate resin is increasingly being developed to withstand various sterilization methods, ensuring it maintains its integrity and performance throughout the process.

Challenges in the Market

Raw Material Price Volatility The production of polycarbonate resin is closely linked to the petrochemical industry, making it vulnerable to fluctuations in raw material costs. This volatility can impact overall production expenses and pricing for end products.

Regulatory Compliance Complexities Navigating the regulatory landscape for medical-grade materials is intricate and costly. Manufacturers must undertake extensive testing to ensure compliance with safety, biocompatibility, and environmental standards, which can delay product launches.

Environmental Concerns The healthcare sector faces increasing scrutiny regarding the environmental impact of synthetic materials. Manufacturers are under pressure to adopt sustainable practices and explore alternatives that minimize ecological footprints.

Future Opportunities for Growth

Investments in R&D Ongoing investment in research and development can lead to innovative formulations of medical-grade polycarbonate resin with enhanced properties, such as improved biocompatibility and sterilization resistance. These advancements could broaden its application in the medical field.

Strategic Partnerships Collaborations between resin manufacturers and medical device companies can drive innovation, facilitating the development of specialized products that meet specific healthcare needs. These partnerships can also streamline the supply chain and enhance market access.

Capitalizing on Emerging Markets The expansion of healthcare infrastructure in emerging regions presents significant growth opportunities. Companies that strategically enter these markets can capture the increasing demand for medical devices and materials.

Conclusion

The global medical-grade polycarbonate resin market is set for continued growth as healthcare demands evolve. With a focus on innovation, sustainability, and compliance with regulatory standards, manufacturers can leverage opportunities to enhance their offerings and expand their market presence. As advancements in medical technology continue and patient safety remains a top priority, medical-grade polycarbonate resin will play a crucial role in shaping the future of healthcare products.

0 notes

Text

The Growing Lab Consumables Market: Trends, Challenges, and Future Prospects

Laboratory consumables play an essential role in scientific research, diagnostic testing, and manufacturing processes across numerous industries. From basic research and clinical testing to quality control in industrial labs, these single-use items are integral to ensuring accuracy, efficiency, and safety in laboratory environments. This article will delve into the evolving lab consumables market, exploring key trends, challenges, and future prospects.

Download PDF Brochure:

1. Understanding the Lab Consumables Market

Laboratory consumables encompass a wide array of disposable items used in laboratory procedures, including pipettes, test tubes, petri dishes, syringes, gloves, and vials. Unlike laboratory equipment, which can be reused over time, consumables are typically discarded after one use. This aspect contributes to the recurring demand for these products, making the consumables market a vital part of laboratory operations worldwide.

The lab consumables market serves several major sectors, including:

Pharmaceutical and Biotechnology industries

Clinical and Diagnostic Labs

Food and Beverage Testing

Environmental Testing

Academic and Research Institutions

2. Key Trends Shaping the Lab Consumables Market

The lab consumables market has witnessed substantial growth over the past few years, driven by several factors, including advancements in technology, the COVID-19 pandemic, and an increased focus on health and safety standards.

a. Rise of Automation in Laboratories

Laboratory automation is on the rise, and the demand for automation-compatible consumables has grown in response. Automation enables laboratories to handle high sample volumes efficiently, reducing manual errors, which is critical in fields such as clinical diagnostics, pharmaceuticals, and biotechnology.

Automated systems often require consumables that are precisely manufactured to work seamlessly with the machinery. This need has led to a market shift towards high-quality, reliable, and machine-compatible consumables that meet the demands of automated laboratory workflows.

b. Growing Emphasis on Sustainability

The increasing awareness of environmental impact has shifted the focus towards eco-friendly and sustainable lab consumables. The rise in single-use plastics usage, primarily due to concerns about contamination, has driven the demand for recyclable or biodegradable alternatives. Many companies are innovating by introducing products made from sustainable materials, such as biodegradable plastics and recycled components, to reduce the environmental footprint of laboratories.

c. Demand for Customization and Specialized Consumables

As scientific research becomes more specialized, the demand for customized consumables has surged. Researchers and lab professionals often require consumables tailored to specific experimental conditions, especially in niche fields such as genomics, proteomics, and personalized medicine. The need for specialized consumables, including PCR tubes, reagent reservoirs, and customized microplates, has contributed to the growth of the lab consumables market.

d. Expansion of the Clinical Diagnostic Sector

The clinical diagnostic sector has experienced significant growth, particularly due to the increased need for testing during the COVID-19 pandemic. This expansion has led to a surge in demand for lab consumables used in diagnostic testing, such as swabs, pipette tips, and sample containers. Additionally, with the rise in chronic and infectious diseases globally, the clinical diagnostics sector continues to rely heavily on lab consumables for consistent and accurate testing.

e. Innovations in Material and Manufacturing Techniques

The advancement of materials science has led to the development of consumables with enhanced durability, chemical resistance, and reduced reactivity. For instance, consumables made from medical-grade polymers offer superior performance and reliability, which is critical in sensitive laboratory applications. Furthermore, improvements in manufacturing techniques, such as 3D printing, have enabled companies to create complex designs and prototypes more efficiently, allowing rapid production of custom lab consumables.

Request Sample Pages:

3. Market Segmentation of Lab Consumables

The lab consumables market can be segmented into categories based on product type, end-users, and regions.

By Product Type: The market includes pipettes, tubes, petri dishes, beakers, gloves, cell culture consumables, and other disposable items.

By End-User: Major end-users include pharmaceutical and biotechnology companies, academic research institutions, clinical and diagnostic laboratories, and food and beverage testing facilities.

By Region: The market is geographically divided into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

Regional Insights

North America holds a significant share of the lab consumables market, driven by its robust pharmaceutical and biotechnology industries, advanced healthcare infrastructure, and investment in research and development. Europe follows closely, with a strong emphasis on high-quality, regulation-compliant consumables. The Asia-Pacific region is expected to witness the fastest growth due to the rapid expansion of the healthcare sector and increasing investment in life sciences research.

4. Challenges in the Lab Consumables Market

While the lab consumables market is growing, it faces several challenges that may hinder its potential.

a. Environmental Concerns Related to Plastic Waste

The reliance on single-use plastic products in laboratory settings has raised concerns about environmental sustainability. Many lab consumables are made from non-biodegradable materials, contributing to the accumulation of plastic waste. Balancing the need for safe, disposable consumables with environmental sustainability is a critical challenge for the industry.

b. Cost Constraints in Emerging Markets

In emerging economies, the high cost of lab consumables can be a limiting factor for smaller institutions and laboratories with tight budgets. Although automation and high-quality consumables enhance laboratory efficiency, they often come at a premium, making them inaccessible to some markets.

c. Quality and Regulatory Compliance

Maintaining quality and ensuring regulatory compliance can be complex, particularly in the pharmaceutical and clinical diagnostics sectors, where strict standards apply. Consumables must meet rigorous specifications to prevent contamination, ensure compatibility with automated systems, and support reliable results. Ensuring consistent quality across large-scale production while complying with regulatory requirements can pose a significant challenge for manufacturers.

d. Supply Chain Disruptions

The COVID-19 pandemic underscored the vulnerability of global supply chains, leading to shortages of essential consumables. The ongoing disruptions in the supply chain for raw materials, labor, and shipping have impacted the market and may continue to pose a risk in the future. Securing a stable supply chain is crucial to prevent interruptions in lab workflows, especially in clinical and diagnostic labs.

5. Future Prospects of the Lab Consumables Market

The future of the lab consumables market appears promising, with steady growth anticipated in the coming years. Key factors driving this growth include:

a. Increasing Investment in Life Sciences Research

Governments and private organizations are investing heavily in life sciences research, fueling demand for lab consumables. These investments support the growth of new research fields, such as genomics, proteomics, and regenerative medicine, which in turn increase the need for reliable and specialized consumables.

b. Expansion of the Healthcare Sector

The growing healthcare sector, especially in emerging markets, will continue to drive demand for diagnostic testing and, consequently, lab consumables. Additionally, the prevalence of chronic diseases and infectious outbreaks necessitates consistent testing and diagnostic procedures, reinforcing the need for consumables.

c. Technological Advancements and Sustainable Solutions

Technological advancements in manufacturing and materials science will continue to shape the market. The integration of sustainable practices and development of eco-friendly materials could help the industry reduce its environmental footprint while meeting the increasing demand for lab consumables. Companies that invest in green technologies may gain a competitive edge as environmental sustainability becomes a priority.

d. Growing Adoption of Point-of-Care Testing

Point-of-care (POC) testing is expanding, driven by the need for faster, decentralized diagnostic solutions. The POC sector relies heavily on consumables for sample collection, processing, and analysis. As POC testing becomes more widespread in hospitals, clinics, and remote areas, the demand for consumables will likely increase.

Conclusion

The lab consumables market is a dynamic and essential part of the laboratory industry, supporting a broad range of applications in research, diagnostics, and industrial testing. With rising investment in life sciences, advances in automation, and an increased focus on sustainability, the demand for lab consumables is expected to grow steadily.

However, the market faces challenges such as environmental concerns, cost constraints, and regulatory requirements. To remain competitive and sustainable, industry players will need to innovate in both product offerings and manufacturing practices. As laboratories continue to evolve, so will the lab consumables market, making it a vital area for continued investment and development in the scientific community.

0 notes

Text

From Precision to Safety: How Prefilled Syringes Are Transforming Healthcare Delivery

The global prefilled syringes market size is anticipated to reach USD 16.73 billion by 2030, expanding at a CAGR of 13.08% from 2024 to 2030, according to a new report by Grand View Research, Inc. Key factors driving the market expansion include technological advancements in auto-injectors and growing usage of prefilled syringes owing to its reduced prices per dose.

The current COVID-19 outbreak is expected to have a substantial impact on the industry. The pandemic has resulted in a significant surge in demand for emergency supplies, medical disposables, medicines, and hospital equipment. According to American Pharmaceutical Review in December 2021, COVID-19 vaccines are being created at an unprecedented rate in response to the worldwide pandemic. COVID-19 vaccination doses totaled 7.3 billion by November 9, 2021, with approximately 30.3 million doses provided daily.

As a result of COVID-19, there has been an increase in the production of COVID-19 vaccines, resulting in increased demand for prefilled syringes. For instance, in March 2022, Schott announced further investments in its pharma sector, including expanding its capacity in Hungary for prefillable glass syringe production. The increased capacity is likely to benefit the global market and provide greater supply security for major pharmaceutical corporations and contract manufacturing firms. As a result, due to the outbreak of coronavirus infection in 2020, sales of prefilled syringes increased globally.

Furthermore, emergency syringes used to treat some of COVID-19's most significant side effects such as heart damage have historically been scarce. Despite the heightened demand during the outbreak, manufacturers provide various programs that identifies high-quality, protected supply bases for medications that are or could be added to the national drug scarcity list. For instance, in October 2019, Premier Inc. teamed up with Amphastar Pharmaceuticals, Inc. to provide phytonadione injection and emergency, pre-filled syringes of sulphate, dextrose, sodium bicarbonate, epinephrine, atropine, calcium chloride, and lidocaine to healthcare practitioners through its ProvideGx programme. These characteristics are projected to generate lucrative market growth prospects.

Prefilled Syringes Market Report Highlights

The disposable segment accounted for the largest market share of 91.4% in 2023 and is expected to register the fastest CAGR over the forecast period.

The glass segment accounted for the largest share of 51.4% in 2023. The glass acts as a strong barrier against external elements like moisture, oxygen, and light.

The vaccines and immunizations segment accounted for the largest share of 25.8% in 2023. Numerous vaccines require multiple doses to be administered over a period of time.

The Europe prefilled syringes market dominated the global market and is driven by the strong preference of medical professionals for injectable devices that are prefilled to reduce damage caused by needles.

Prefilled Syringes Market Segmentation

Grand View Research has segmented the global prefilled syringes market on the basis of type, material, application, distribution channel, and region:

Prefilled Syringes Type Outlook (Revenue, USD Million, 2018 - 2030)

Disposable

Reusable

Prefilled Syringes Material Outlook (Revenue, USD Million, 2018 - 2030)

Glass

Plastic

Prefilled Syringes Application Outlook (Revenue, USD Million, 2018 - 2030)

Vaccines & Immunizations

Anaphylaxis

Rheumatoid Arthritis

Diabetes

Autoimmune Diseases

Oncology

Others

Prefilled Syringes Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

Hospitals

Mail Order Pharmacies

Ambulatory Surgery Centers

Prefilled Syringes Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Thailand

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Kuwait

List of Key Players

BD

Gerresheimer AG

SCHOTT Pharma AG

Stevanato Group

Nipro Corporation

Terumo

West pharmaceuticals

Fresenius

Catalent

Aptar Pharma

Recent Developments

In May 2023, Schott Pharma developed pre-fillable syringes specifically designed for medications that require storage in extremely cold conditions

In May 2023, Fresenius Kabi expanded its Simplist prefilled syringe line with a 100mcg per 2mL dose of Fentanyl Citrate Injection

In September 2022, Becton Dickinson and Company (BDX) launched a new, top-of-the-line glass pre-fillable syringe specifically for vaccines. This innovative product features enhanced specifications for manufacturability, visual quality, contamination control, and overall integrity

In May 2022, SCHOTT, opened a brand-new facility to manufacture pre-fillable syringes using innovative polymer materials

Order a free sample PDF of the Prefilled Syringes Market Intelligence Study, published by Grand View Research.

0 notes

Text

Urinary Catheters Market Research: Growth Opportunities by Regions, Types & Applications to 2030

The global urinary catheters market was valued at USD 5.2 billion in 2022, and it is projected to grow at a compound annual growth rate (CAGR) of 5.4% from 2023 to 2030. This growth is primarily driven by several key factors, including an increase in the number of patients experiencing Urinary Tract Infections (UTIs) and blockages in the urethra. Additionally, rising incidences of tumors affecting the urinary tract or reproductive organs, coupled with the rapidly aging global population, are also contributing to the expansion of the market. A urinary catheter is a partially flexible tube designed to drain urine from the bladder, and it is commonly made from materials such as plastic, rubber, and silicone. Medical professionals recommend urinary catheters for conditions such as Urinary Incontinence (UI), urinary retention, prostate surgeries, or in cases where patients suffer from spinal cord injuries, multiple sclerosis, or dementia.

Gather more insights about the market drivers, restrains and growth of the Urinary Catheters Market

Impact of COVID-19 on the Market:

The COVID-19 pandemic is expected to have a positive impact on the urinary catheter market. According to data from the National Center for Biotechnology Information (NCBI), the use of catheters, including urinary and central line catheters, saw an increase during the COVID-19 outbreak. For instance, in 2020, the Standardized Utilization Ratio (SUR) for urinary catheters increased by 7.4%, rising from 0.79 before the pandemic to 0.84 during the outbreak. Similarly, the SUR for central line catheters rose by 4.9%, from 0.88 pre-pandemic to 0.92 during the crisis. This increased demand for catheters, especially in critical care settings, is expected to contribute to the market's growth over the forecast period.

The pandemic also underscored the importance of infection prevention, leading to innovations in catheter technology. Several manufacturers have responded to the heightened awareness of infection control by developing products like coated urinary catheters with built-in temperature monitoring capabilities. These advancements are aimed at reducing the risk of secondary infections in critically ill patients. For instance, in February 2021, Health Canada approved Bactiguard's urinary catheter with a temperature sensor for infection prevention. This approval was expedited due to the urgency created by the pandemic, as these catheters have shown the potential to lower secondary infection rates, thereby supporting market growth.

Product Segmentation Insights:

In 2022, the intermittent catheter segment led the urinary catheters market, accounting for over 57.5% of total revenue. Intermittent catheters are medical devices used to intermittently drain the bladder. These catheters are considered a superior alternative to indwelling (continuous) catheters, which are more likely to lead to UTIs. Intermittent catheterization is often recommended for patients with spinal cord injuries or neurogenic bladder issues. As a result, these devices are considered the gold standard for bladder management in such cases. The availability of reimbursement for intermittent catheters under programs like Medicaid and Medicare has further contributed to the growth of this market segment.

The fastest-growing product segment is expected to be external catheters over the forecast period. These catheters are primarily used for male patients and offer a less invasive alternative to indwelling catheters, which must be inserted through the urethra. External catheters are also popular among patients who prefer to self-catheterize, especially in cases of UI or urinary retention. Additionally, these catheters come in a range of styles and sizes, providing patients with various options to suit their individual needs. Leading companies in the industry are offering advanced external catheter products. For example, BD (C.R. Bard) manufactures the ULTRAFLEX male external catheter, which features a more secure fit compared to traditional non-silicone sheaths, providing users with greater comfort and reliability.

Order a free sample PDF of the Urinary Catheters Market Intelligence Study, published by Grand View Research.

#Urinary Catheters Market Share#Urinary Catheters Market Analysis#Urinary Catheters Market Trends#Urinary Catheters Industry

0 notes

Text

Polylactic Acid Prices Trend | Pricing | News | Database | Chart

Polylactic Acid (PLA) prices have become a focal point within the global bioplastics market as the demand for sustainable materials continues to grow. PLA, a biodegradable thermoplastic derived from renewable resources like corn starch or sugarcane, is frequently used in packaging, textiles, medical implants, and 3D printing applications. The price of PLA has seen fluctuations influenced by numerous factors, including raw material costs, production capacity, regulatory trends, and global market demand for greener alternatives to conventional plastics.

The production process of PLA involves fermenting sugars to produce lactic acid, which is then polymerized. The cost of raw materials like corn or sugarcane directly affects PLA prices, and shifts in agricultural supply chains due to climate conditions, trade restrictions, or supply shortages can lead to price volatility. For example, periods of drought impacting crop yields can drive up the cost of lactic acid production, consequently raising PLA prices. Conversely, a bumper crop season may lead to a temporary decline in PLA production costs. Energy prices, including natural gas and electricity, also play a critical role, as the polymerization process demands significant energy input. Fluctuations in energy markets, therefore, have a direct influence on the cost structure of PLA manufacturing.

Get Real Time Prices for Polylactic Acid (PLA): https://www.chemanalyst.com/Pricing-data/polylactic-acid-1275

Another pivotal factor affecting the price trajectory of PLA is the increasing scale of production. As more companies invest in PLA production capacity, economies of scale have begun to emerge, potentially reducing per-unit costs over time. Large-scale production facilities, particularly in regions such as North America, Europe, and Asia-Pacific, aim to capitalize on the rising consumer demand for eco-friendly materials. New production plants, joint ventures, and technological advancements are helping streamline manufacturing processes, increasing yields, and reducing overall costs. However, there remains competition with petroleum-based plastics, which generally have a more established supply chain and cost advantage. As fossil fuel prices remain relatively stable or fluctuate within a predictable range, this affects the competitiveness of PLA pricing in the broader market for plastics and packaging materials.

Government policies and regulations that promote environmental sustainability and reduce the carbon footprint have also influenced PLA prices. Various regions have implemented bans or restrictions on single-use plastics, creating a favorable environment for PLA adoption. The European Union’s stringent regulations on plastics, for example, have spurred greater interest in biodegradable alternatives, driving up demand and prices. Similar regulatory changes in other markets, including North America and parts of Asia, further strengthen PLA demand. However, the legislative landscape also poses challenges. For instance, any delays or changes in regulatory frameworks, such as postponed bans on single-use plastics, can lead to uncertainty and price shifts in the PLA market.

The global supply chain dynamics significantly impact PLA prices as well. Trade tensions, tariffs, and geopolitical factors that affect the import and export of raw materials or PLA products can cause disruptions in pricing. The COVID-19 pandemic, for instance, exposed vulnerabilities in supply chains, leading to logistical challenges that drove up shipping costs, constrained production, and created pricing spikes in numerous industries, including bioplastics. While some of these challenges have subsided, supply chain resilience remains a crucial consideration for predicting future PLA price trends. Companies are looking to regionalize supply chains, which may lead to higher short-term costs but potentially stabilize pricing in the longer run.

Technological advancements and innovation within the PLA industry are driving efficiency gains, but they also have implications for prices. Developments in enzymatic recycling and improved polymerization techniques have the potential to enhance the recyclability and performance characteristics of PLA, making it more attractive to manufacturers. While these advancements may introduce higher initial costs, they contribute to the long-term viability of PLA as a key bioplastic, influencing pricing dynamics accordingly. Moreover, as new uses for PLA are discovered and commercialized, demand growth could outpace supply, contributing to price volatility.

Market demand for environmentally friendly materials plays a prominent role in determining PLA prices. Heightened consumer awareness around sustainability and the environmental impact of plastic pollution has led to increased demand for biodegradable materials. Companies across a variety of sectors, including packaging, textiles, automotive, and consumer goods, are incorporating PLA into their products to appeal to eco-conscious consumers and meet sustainability goals. This surge in demand has exerted upward pressure on prices, though it has also attracted new market entrants, potentially balancing supply and reducing price hikes over time.

Global competition among producers also influences PLA price dynamics. Major players in the market, including NatureWorks, Total Corbion PLA, and others, compete to capture market share through cost-efficient production, innovative product offerings, and regional expansion. This competition can lead to price wars or aggressive pricing strategies in certain regions, creating a mixed impact on overall pricing trends. Additionally, these companies' commitment to sustainability goals and reducing carbon footprints is shaping the overall cost structure of PLA production and, by extension, the pricing landscape.

In summary, the pricing of Polylactic Acid is shaped by a complex interplay of factors, including raw material costs, production capacities, regulatory influences, technological innovations, and market demand. While the market is driven by the global push for sustainability and the reduction of single-use plastics, challenges such as supply chain disruptions, competition from traditional plastics, and evolving legislation continue to influence the pricing landscape. As the industry matures, the expectation is that technological advancements and economies of scale will help stabilize prices, making PLA a more economically viable choice for manufacturers and a key player in the transition to a more sustainable future.

Welcome to ChemAnalyst App: https://www.chemanalyst.com/ChemAnalyst/ChemAnalystApp

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Polylactic Acid#Polylactic Acid Price#Polylactic Acid Prices#Polylactic Acid Pricing#Polylactic Acid News#Polylactic Acid Price Monitor

0 notes

Text

Urinary Catheters Market Size, Share, Research and Competitive Landscape 2030

The global urinary catheters market was valued at USD 5.2 billion in 2022, and it is projected to grow at a compound annual growth rate (CAGR) of 5.4% from 2023 to 2030. This growth is primarily driven by several key factors, including an increase in the number of patients experiencing Urinary Tract Infections (UTIs) and blockages in the urethra. Additionally, rising incidences of tumors affecting the urinary tract or reproductive organs, coupled with the rapidly aging global population, are also contributing to the expansion of the market. A urinary catheter is a partially flexible tube designed to drain urine from the bladder, and it is commonly made from materials such as plastic, rubber, and silicone. Medical professionals recommend urinary catheters for conditions such as Urinary Incontinence (UI), urinary retention, prostate surgeries, or in cases where patients suffer from spinal cord injuries, multiple sclerosis, or dementia.

Gather more insights about the market drivers, restrains and growth of the Urinary Catheters Market

Impact of COVID-19 on the Market:

The COVID-19 pandemic is expected to have a positive impact on the urinary catheter market. According to data from the National Center for Biotechnology Information (NCBI), the use of catheters, including urinary and central line catheters, saw an increase during the COVID-19 outbreak. For instance, in 2020, the Standardized Utilization Ratio (SUR) for urinary catheters increased by 7.4%, rising from 0.79 before the pandemic to 0.84 during the outbreak. Similarly, the SUR for central line catheters rose by 4.9%, from 0.88 pre-pandemic to 0.92 during the crisis. This increased demand for catheters, especially in critical care settings, is expected to contribute to the market's growth over the forecast period.

The pandemic also underscored the importance of infection prevention, leading to innovations in catheter technology. Several manufacturers have responded to the heightened awareness of infection control by developing products like coated urinary catheters with built-in temperature monitoring capabilities. These advancements are aimed at reducing the risk of secondary infections in critically ill patients. For instance, in February 2021, Health Canada approved Bactiguard's urinary catheter with a temperature sensor for infection prevention. This approval was expedited due to the urgency created by the pandemic, as these catheters have shown the potential to lower secondary infection rates, thereby supporting market growth.

Product Segmentation Insights:

In 2022, the intermittent catheter segment led the urinary catheters market, accounting for over 57.5% of total revenue. Intermittent catheters are medical devices used to intermittently drain the bladder. These catheters are considered a superior alternative to indwelling (continuous) catheters, which are more likely to lead to UTIs. Intermittent catheterization is often recommended for patients with spinal cord injuries or neurogenic bladder issues. As a result, these devices are considered the gold standard for bladder management in such cases. The availability of reimbursement for intermittent catheters under programs like Medicaid and Medicare has further contributed to the growth of this market segment.

The fastest-growing product segment is expected to be external catheters over the forecast period. These catheters are primarily used for male patients and offer a less invasive alternative to indwelling catheters, which must be inserted through the urethra. External catheters are also popular among patients who prefer to self-catheterize, especially in cases of UI or urinary retention. Additionally, these catheters come in a range of styles and sizes, providing patients with various options to suit their individual needs. Leading companies in the industry are offering advanced external catheter products. For example, BD (C.R. Bard) manufactures the ULTRAFLEX male external catheter, which features a more secure fit compared to traditional non-silicone sheaths, providing users with greater comfort and reliability.