#Airborne Surveillance Market Research

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

couponcodesforcoachfactoryo-blog

Coupon codes for coach factory outlet online - Coach outline onl

2 posts

Fun Fact

There are dozens of funny blogs to kill time on Tumblr.

Text

Chinese Hospitals Are Housing Another Deadly Outbreak

In Beijing and other megacities in China, hospitals are overflowing with children suffering pneumonia or similar severe ailments. However, the Chinese government claims that no new pathogen has been found and that the surge in chest infections is due simply to the usual winter coughs and colds, aggravated by the lifting of stringent COVID-19 restrictions in December 2022. The World Health Organization (WHO) has dutifully repeated this reassurance, as if it learned nothing from Beijing’s disastrous cover-up of the COVID-19 outbreak.

There is an element of truth in Beijing’s assertion, but it is only part of the story. The general acceptance that China is not covering up a novel pathogen this time appears reassuring. In fact, however, China could be incubating an even greater threat: the cultivation of antibiotic-resistant strains of a common, and potentially deadly, bacteria.

Fears of another novel respiratory pathogen emerging from China are understandable after the SARS and COVID-19 pandemics, both of which Beijing covered up. Concerns are amplified by Beijing’s ongoing obstruction of any independent investigation into the origins of SARS-CoV-2, the virus that causes COVID-19—whether it accidentally leaked from the Wuhan lab performing dangerous gain-of-function research or derived from the illegal trade in racoon dogs and other wildlife at the now-infamous Wuhan wet-market.

Four years ago, during the early weeks of the COVID-19 outbreak, Beijing failed to report the new virus and then denied airborne spread. At pains to maintain their fiction, Chinese authorities punished doctors who raised concerns and prohibited doctors from speaking even to Chinese colleagues, let alone international counterparts. Chinese medical statistics remain deeply unreliable; the country still claims that total COVID-19 deaths sit at just over 120,000, whereas independent estimates suggest the number may have been over 2 million in just the initial outbreak alone. Now, Chinese doctors are once again being silenced and not communicating with their counterparts abroad, which suggests another potentially dangerous cover-up may be underway.

We don’t know exactly what is happening, but we can offer some informed guesses.

The microbe causing the surge in hospitalization of children is Mycoplasma pneumoniae, which causes M. pneumoniae pneumonia, or MPP. First discovered in 1938, the microbe was believed for decades to be a virus because of its lack of a cell membrane and tiny size, although in fact it is an atypical bacterium. These unusual characteristics makes it invulnerable to most antibiotics (which typically work by destroying the cell membrane). The few attempts to make a vaccine in the 1970s failed, and low mortality has provided little incentive for renewed efforts. Although MPP surges are seen every few years around the world, the combination of low mortality and difficult diagnostics has meant there is no routine surveillance.

Although MPP is the most common cause of community-acquired pneumonia in school children and teenagers, pediatricians such as myself refer to it as “walking pneumonia” because symptoms are relatively mild. Respiratory Syncytial Virus (RSV), influenza, adenoviruses, and rhinoviruses (also known as the common cold) all cause severe inflammation of the lungs and are far more common causes of emergency-room visits, hospitalization, and death in infants and young children. Why should MPP be acting differently now?

One contributing factor to the severity of this outbreak may be “immunity debt.” Around the globe, COVID-19 lockdowns and other non-pharmaceutical measures meant that children were less exposed to the usual range of pathogens, including MPP, for several years. Many countries have since seen rebound surges in RSV. Several experts agree with Beijing’s explanation that the combination of winter’s arrival, the end of COVID-19 restrictions, and a lack of prior immunity in children are likely behind the surging infections. Some even speculate that that substantial lockdown may have particularly compromised young children’s immunity, because exposure to germs in infancy is essential for immune systems to develop.

In China, MPP infections began in early summer and accelerated. By mid-October, the National Health Commission had taken the unusual step of adding MPP to its surveillance system. That was just after Golden Week, the biggest tourism week in China.

Infection by two diseases at the same time can make things worse. The usual candidates for coinfection in children—RSV and flu—have not previously caused comparable surges in pneumonia. One difference this time is COVID-19. It is possible that the combination of COVID-19 and MPP is particularly dangerous. Although adults are less susceptible to MPP due to years of exposure, adults hospitalized for COVID-19 who were simultaneously or recently coinfected by MPP had a significantly higher mortality rate, according to a 2020 study.

Infants and toddlers are immunologically naive to MPP, and unlike COVID-19, RSV, and influenza, there is no vaccine against MPP. It seems implausible that no child (or adult) has died from MPP, yet China has not released any data on mortality, or on extrapulmonary complications such as meningitis.

Most disturbing, and a fact being downplayed by Beijing, is that M. pneumoniae in China has mutated to a strain resistant to macrolides, the only class of antibiotics that are safe for children less than eight years of age. Beyond discouraging parents to start ad hoc treatment with azithromycin, the most common macrolide and the usual first-line antibiotic for MPP, Beijing has barely mentioned this fact. Even more worrying is that WHO has assessed the risk of the current outbreak as low on the basis that MPP is readily treated with antibiotics. Broader azithromycin resistance in MPP is common across the world, and China’s resistant strain rates in particular are exceptionally high. Beijing’s Centers for Disease Control and Prevention reported macrolide resistance rates for MPP in the Beijing population between 90 and 98.4 percent from 2009 to 2012. This means there is no treatment for MPP in children under age eight.

Fears over a novel pathogen are already abating. After all, MPP is rarely lethal. But antimicrobial resistance (AMR) is. Responsible for 1.3 million deaths a year, AMR kills more people than COVID-19. No country is immune to this growing threat. Since China, where antibiotics are regularly available over the counter, leads the world in AMR, it is inconceivable that this issue hasn’t yet come up, particularly during WHO’s World AMR Awareness week, from Nov. 18 to Nov. 24.

Any infectious disease physician would want to know: Did WHO asked China the obvious question—what is the level of azithromycin resistance of M. pneumonia in the current outbreak—and include the answer in its risk assessment? Or did it ask about resistance to doxycycline and quinolones, antibiotics that can be used to treat MPP in adults? Even if WHO did ask, China isn’t telling, and WHO isn’t talking.

China’s silence isn’t surprising. Its antibiotic consumption per person is ten times that of the United States, and policies for AMR stewardship are predominantly cosmetic. While surveillance is China’s strong point, reporting is not.

Despite Spring Festival, the Chinese celebration of the Lunar New Year and another peak travel period, approaching in February 2024, WHO hasn’t advised any travel restrictions. It should have learned the danger of accepting Beijing’s statements at face value. Four years ago, Beijing’s delay enabled more than 200 million people to travel from and through Wuhan for Spring Festival. That helped COVID-19 go global. Since China’s AMR rates are already so high, importing AMR from other countries isn’t a major concern for China. Export is the issue, and China’s track record in protecting other countries is abysmal.

Rather than repeating the self-serving whitewashing coming from Beijing, WHO should be publicly pressing China about the threat of mutant microbes. Halting AMR is essential. Before antisepsis and antibiotics, surgery was a treatment of last resort. Without antibiotics, we lose 150 years of clinical and surgical advances. Within ten years, we are at risk of few antibiotics being effective. It may not be the novel virus that people were expecting, but the next pandemic is already here.

13 notes

·

View notes

Text

Airborne Radars Market Analysis: Emerging Trends & Growth Factors

Introduction:

The Airborne Radars Market is a rapidly expanding sector driven by increasing demand for advanced surveillance, reconnaissance, and navigation technologies across defense and commercial aviation industries. Airborne radar systems are crucial for detecting and tracking aerial threats, improving situational awareness, and enhancing the operational capabilities of modern aircraft. With rising security concerns, military forces worldwide are investing heavily in radar-equipped fighter jets, drones, and surveillance aircraft.

Airborne Radars Market growth is fueled by technological advancements, increasing defense expenditures, and the growing use of unmanned aerial vehicles (UAVs). The integration of artificial intelligence (AI), synthetic aperture radar (SAR), and active electronically scanned array (AESA) technologies is further revolutionizing airborne radar capabilities, making them more efficient, accurate, and versatile.

Market Trends & Growth:

Rising Defense Expenditure – Governments worldwide are increasing defense budgets, leading to higher investments in airborne radar systems for national security.

Advancements in Radar Technologies – The adoption of AESA, SAR, and AI-powered radar systems is enhancing accuracy, detection range, and operational efficiency.

Growing Use of UAVs and Drones – Increasing deployment of UAVs for surveillance and military operations is driving demand for lightweight, high-performance airborne radars.

Commercial Aviation Growth – Expanding air traffic and stringent safety regulations are boosting the adoption of radar systems for air traffic control and collision avoidance.

Demand for Multi-Mode Radar Systems – Multi-functional radars capable of operating in different environments are gaining traction in both defense and commercial sectors.

Regional Military Modernization Programs – Emerging economies are investing in modernizing their air forces, creating new opportunities in the airborne radar market.

Challenges:

Despite its promising growth, the Airborne Radars Market faces several challenges. High development and integration costs of advanced radar systems remain a significant barrier for budget-constrained defense programs. Additionally, the complexity of integrating modern radar technologies with existing aircraft platforms poses technical difficulties. Regulatory constraints and export restrictions on military-grade radar systems also limit market expansion in some regions. Furthermore, competition from alternative surveillance technologies, such as satellite-based monitoring, may impact the demand for airborne radar solutions.

Future Outlook:

The Airborne Radars Market is expected to witness substantial growth in the coming years, driven by continuous advancements in radar technology and increasing defense and aviation sector investments. The shift towards AI-powered and software-defined radar systems will enhance detection capabilities, adaptability, and efficiency. Furthermore, the growing adoption of airborne radars in commercial aviation for collision avoidance and weather monitoring will contribute to market expansion. Emerging markets in Asia-Pacific, the Middle East, and Latin America are expected to offer lucrative opportunities due to rising defense modernization programs.

Conclusion:

The Airborne Radars Market is poised for significant expansion, fueled by rising defense expenditures, technological innovations, and increasing demand for UAV-based surveillance. While challenges such as high costs and regulatory constraints exist, ongoing research and development efforts are expected to overcome these barriers. As airborne radar systems continue to evolve, they will play a crucial role in enhancing security, safety, and operational efficiency across military and commercial aviation sectors.

Read More Insights @ https://www.snsinsider.com/reports/airborne-radars-market-4638

Contact Us:

Akash Anand – Head of Business Development & Strategy

Phone: +1-415-230-0044 (US) | +91-7798602273 (IND)

0 notes

Text

Spy Tech is Evolving! Airborne ISR Market to Double to $10.4B by 2033 🛩️📡

Airborne ISR : Airborne ISR (Intelligence, Surveillance, and Reconnaissance) plays a critical role in modern defense, security, and strategic operations. By leveraging advanced sensors, AI-powered analytics, and real-time data transmission, ISR platforms provide military and government agencies with enhanced situational awareness, threat detection, and mission success.

To Request Sample Report: https://www.globalinsightservices.com/request-sample/?id=GIS25512 &utm_source=SnehaPatil&utm_medium=Article

Airborne ISR systems, integrated into drones, manned aircraft, and satellites, gather and process vast amounts of intelligence. These platforms use cutting-edge technologies such as electro-optical/infrared (EO/IR) cameras, radar, signals intelligence (SIGINT), and synthetic aperture radar (SAR) to track enemy movements, monitor borders, and conduct reconnaissance missions.

With the increasing demand for real-time intelligence, ISR aircraft and UAVs (Unmanned Aerial Vehicles) are transforming the way military forces operate. AI-powered ISR solutions enable automated target recognition, predictive analysis, and enhanced geospatial intelligence (GEOINT), allowing for faster and more accurate decision-making in critical situations.

Beyond military applications, airborne ISR is also vital for disaster response, border security, anti-piracy missions, and environmental monitoring. These systems help in tracking wildfires, illegal trafficking, and natural disasters, providing real-time updates to first responders and government agencies.

As technology evolves, next-generation ISR platforms are becoming more autonomous, networked, and data-driven. With advancements in hypersonic surveillance, quantum computing, and AI-powered analytics, the future of ISR will redefine global security and intelligence gathering.

How do you see ISR shaping the future of defense and security? Share your thoughts below! 👇

#AirborneISR #ISRTechnology #Surveillance #IntelligenceGathering #MilitaryTech #DefenseInnovation #SituationalAwareness #ISRSystems #AerospaceTechnology #Drones #UAVs #MilitaryIntelligence #TacticalISR #NationalSecurity #RealTimeIntelligence #GEOINT #SIGINT #SyntheticApertureRadar #AIinDefense #SecuritySolutions #BorderSecurity #ElectronicWarfare #AviationTech #NextGenISR #StrategicOperations #DefenseTech

Research Scope:

· Estimates and forecast the overall market size for the total market, across type, application, and region

· Detailed information and key takeaways on qualitative and quantitative trends, dynamics, business framework, competitive landscape, and company profiling

· Identify factors influencing market growth and challenges, opportunities, drivers, and restraints

· Identify factors that could limit company participation in identified international markets to help properly calibrate market share expectations and growth rates

· Trace and evaluate key development strategies like acquisitions, product launches, mergers, collaborations, business expansions, agreements, partnerships, and R&D activities

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

India, Brazil, and Australia are the new opportunity grounds for Synthetic Aperture Radar market players

According to a recent research, Industry revenue for Synthetic Aperture Radar is expected to rise to $19.2 billion by 2035 from $5.1 billion of 2023. U.S., Germany and China are the top 5 markets and combinely holds substantial demand share. The revenue growth of market players in these countries is expected to range between 8.5% and 12.3% annually for period 2024 to 2035.

Industry transition including shift toward small satellite constellations and increased application in climate monitoring, are transforming the supply chain of Synthetic Aperture Radar market. Small groups of satellites, with SAR technology are becoming increasingly popular as they provide frequent data collection and wider coverage.

Check detailed report here - https://datastringconsulting.com/industry-analysis/synthetic-aperture-radar-market-research-report

Research Study addresses the market dynamics including opportunities, competition analysis, industry insights for Type (Space-Based, Airborne, Ground-Based), Mode (Single Polarization, Dual Polarization, Full Polarization) and Frequency Band (X-Band, C-Band, L-Band, S-Band).

Industry Leadership and Strategies

Companies such as Airbus, Capella Space, MDA, ICEYE, Northrop Grumman, Raytheon Technologies, Lockheed Martin, Qorvo, Cobham, Boeing, Honeywell and Synspective are well placed in the market. Below table summarize the strategies employed by these players within the eco-system.

Evolving & Shifting Regional Markets

North America and Asia-Pacific are the two most active and leading regions in the market. With different regional dynamics and industry challenges like high development and launch costs, complex data processing requirements and limited bandwidth in some regions; market supply chain from component supplier to end-user is expected to evolve & expand further, especially within emerging markets

The market in emerging countries is expected to expand substantially between 2024 and 2030, supported by market drivers such as increasing demand for earth observation, advancements in satellite and uav technology, and growing need for surveillance and security.

About DataString Consulting

DataString Consulting assist companies in strategy formulations & roadmap creation including TAM expansion, revenue diversification strategies and venturing into new markets; by offering in depth insights into developing trends and competitor landscapes as well as customer demographics. Our customized & direct strategies, filters industry noises into new opportunities; and reduces the effective connect time between products and its market niche.

DataString Consulting offers complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. Our Industry experts and data aggregators continuously track & monitor high growth segments within more than 15 industries and 60 sub-industries.

0 notes

Text

Exploring Anti-jamming Market: Trends and Future Outlook

The global anti-jamming market size was estimated at USD 4.69 billion in 2023 and is expected to grow at a CAGR of 9.4% from 2024 to 2030.The rapid advancement in communication technology is significantly driving the anti-jamming market. Innovations in communication and navigation systems have led to an increased reliance on secure and reliable signal processing.

As defense and commercial sectors adopt more sophisticated systems, the need for advanced anti-jamming solutions becomes paramount. Enhanced signal processing techniques and adaptive algorithms are continually being developed to combat evolving threats. This technological evolution is expanding the anti-jamming market's scope and application, thereby contributing to the growth of the market.

The proliferation of electronic warfare is a critical factor fueling growth in the anti-jamming market. As geopolitical tensions escalate, there is a heightened focus on electronic warfare capabilities. This includes the development of advanced jamming and anti-jamming technologies to safeguard critical communication channels. The increased investment in military and defense sectors for electronic warfare readiness drives demand for effective anti-jamming solutions. Consequently, this trend is pushing the market towards more innovative and robust anti-jamming technologies.

Gather more insights about the market drivers, restrains and growth of the Anti-jamming Market

Key Anti-jamming Company Insights

Key players operating in the anti-jamming market include BAE Systems., Raytheon Systems Limited, Hexagon AB, ST Engineering, Thales, TUALCOM, Collins Aerospace, Lockheed Martin Corporation, Israel Aerospace Industries Ltd., and Meteksan Defence Industry Inc. These companies invest heavily in research and development to enhance their anti-jamming solutions, ensuring they meet the evolving demands of modern warfare and secure communications. In addition, collaborations and strategic partnerships between these leading firms and smaller, specialized technology companies are common, fostering the development of state-of-the-art anti-jamming systems.

Companies across the globe are securing investment to enhance their GPS signal capabilities. For instance, in November 2023, BAE Systems secured investment for the subsequent phase of the Eurofighter Typhoon aircraft's anti-jamming system. The Digital GPS Anti-jam Receiver (DIGAR) Phase 4 Enhancement was designed to enhance the aircraft’s survivability against radio frequency interference and GPS signal spoofing and jamming, The funding also included BAE’s new GEMVII-6 airborne digital GPS receiver, which enabled the aircraft to use digital beamforming for anti-jamming.

Global Anti-jamming Market Report Segmentation

The report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For the purpose of this study, Grand View Research has segmented the global anti-jamming market report based on receiver, technique, application, end-use, and region.

Receiver Outlook (Revenue, USD Million, 2018 - 2030)

• Military & Government Grade

• Commercial Transportation Grade

Technique Outlook (Revenue, USD Million, 2018 - 2030)

• Nulling Technique

• Beam Steering Technique

• Civilian Technique

Application Outlook (Revenue, USD Million, 2018 - 2030)

• Flight Control

• Surveillance and Reconnaissance

• Position, Navigation, and Timing

• Targeting

• Casualty Evacuation

• Other Applications

End-use Outlook (Revenue, USD Million, 2018 - 2030)

• Military

o Airborne

o Ground

o Naval

o Unmanned Vehicles

• Civilian

Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o UK

o Germany

o France

• Asia Pacific

o China

o India

o Japan

o South Korea

o Australia

• Latin America

o Brazil

• Middle East & Africa (MEA)

o Kingdom of Saudi Arabia (KSA)

o UAE

o South Africa

Order a free sample PDF of the Anti-jamming Market Intelligence Study, published by Grand View Research.

#Anti-jamming Market#Anti-jamming Market Size#Anti-jamming Market Share#Anti-jamming Market Analysis#Anti-jamming Market Growth

0 notes

Text

Military Radars Market Report: Growth, Trends, and Forecast (2025–2033)

Military Radars Market Report: Growth, Trends, and Forecast (2025–2033)

Global Military Radars Market Overview

The global military radars market is rapidly evolving to meet the demands of modern defense systems. Valued at USD 16.74 billion in 2024, it is projected to grow significantly, reaching USD 28.05 billion by 2033. This represents a robust CAGR of 5.9% during the forecast period of 2025 to 2033.

Military radars play a vital role in defense applications, ranging from surveillance to weapon guidance. Key advancements and increased investments are driving market growth, offering vast opportunities for industry stakeholders.

Download Free Sample Report: https://straitsresearch.com/report/military-radars-market/request-sample

Key Drivers in the Military Radars Market

Rising Defense Expenditures Governments worldwide are increasing their defense budgets to address rising geopolitical tensions and security threats. Advanced radar systems are a priority for enhancing national defense capabilities.

Technological Advancements Innovations in radar technology, such as phased-array systems and multi-functionality radars, are revolutionizing military operations. These advancements enable improved target detection, tracking, and classification.

Demand for Air and Missile Defense Systems Increasing threats from unmanned aerial vehicles (UAVs) and hypersonic missiles have surged the demand for cutting-edge air and missile defense radars.

Market Segmentation Analysis

By Platform

Ground-Based Radars Widely used for border security and missile defense systems, ground-based radars dominate the market.

Naval Radars Essential for maritime surveillance, these radars aid in detecting surface and underwater threats.

Airborne Radars Installed on military aircraft, they play a critical role in intelligence, surveillance, and reconnaissance (ISR).

Space-Based Radars Used for space situational awareness, these radars are gaining traction in satellite monitoring and defense against extraterrestrial threats.

By Applications

Air and Missile Defense Airborne threats necessitate advanced radar systems for early detection and interception.

Intelligence, Surveillance, and Reconnaissance (ISR) Military operations depend heavily on ISR radars for real-time situational awareness.

Navigation and Weapon Guidance These radars ensure precision targeting and enhance mission success rates.

Space Situational Awareness Increasing satellite launches and space debris have boosted the demand for radars that monitor space activities.

Other Applications These include search and rescue operations and weather monitoring for military purposes.

Market Segmentation: https://straitsresearch.com/report/military-radars-market/segmentation

Key Developments in the Military Radars Market

Technological Advancements

Development of AI-powered radars for enhanced automation and decision-making.

Implementation of 3D radar systems offering superior resolution and range.

Strategic Collaborations

Companies are entering partnerships to integrate advanced technologies into radar systems.

Military Modernization Programs

Nations are upgrading their radar systems to strengthen their defense forces.

Top Key Players in the Military Radars Market

The military radars market is highly competitive, with key players focusing on innovation and expansion. Prominent companies include:

Thales Group

Raytheon Technologies Corporation

BAE Systems PLC

Lockheed Martin Corporation

Northrop Grumman Corporation

Saab AB

Leonardo SpA

Airbus SE

FLIR Systems Inc.

Hensoldt AG

Israel Aerospace Industries

RTX Corporation

Hanwha Systems Co. Ltd.

These companies are investing in research and development to offer advanced radar solutions tailored to diverse defense needs.

Future Outlook and Opportunities

The military radars market is poised for substantial growth in the coming years. With increasing global tensions and technological advancements, the demand for sophisticated radar systems will continue to rise. Companies must focus on innovation and strategic partnerships to capture emerging opportunities.

Buy Full Report: https://straitsresearch.com/buy-now/military-radars-market

About Straits Research

Straits Research specializes in delivering high-quality business intelligence. Their in-depth market insights and advisory services empower businesses to make informed decisions.

0 notes

Text

Sonar System Market Size, Share, Industry Growth, Trends, and Segment Analysis by 2032

The SONAR system market size is predicted to reach USD 3.76 billion by 2029 and exhibit a CAGR of 7.96% during the projected period. Fortune Business InsightsTM has presented this information in its report titled, “SONAR System Market, 2022-2029”. The market stood at USD 2.09 billion in 2021 and USD 2.20 billion in 2022. Sound Navigation and Ranging (SONAR) is a sophisticated technique that uses sound propagation to navigate and communicate with underwater objects.

Informational Source:

The use of SONAR systems with deep neural networks is revolutionizing fish monitoring, especially in aquaculture farms where expanding fish resources is a priority. These systems combine high-precision imaging SONAR with advanced underwater optical cameras, enabling clear monitoring even at night. This technology is improving the efficiency of fish farming and driving demand in the market.

Traditional optical cameras struggle to capture images in low light or murky water, making night monitoring challenging. However, advancements in underwater optical cameras that work seamlessly with SONAR systems are boosting market growth. For example, the SCAN-650 sector scanning SONAR, developed by JW Fishers, is widely used globally. It delivers detailed images of underwater environments, regardless of water clarity, enhancing fish monitoring capabilities.

List of Key Market Players:

ASELSAN A.Ş. (Turkey)

ATLAS ELEKTRONIK INDIA Pvt. Ltd. (India)

DSIT Solutions Ltd. (Israel)

EdgeTech (U.S.)

FURUNO ELECTRIC CO., LTD. (Japan)

Japan Radio Co. (Japan)

KONGSBERG (Norway)

Lockheed Martin Corporation (U.S.)

L3Harris Technologies, Inc. (U.S.)

NAVICO (Norway)

Raytheon Technologies Corporation (U.S.)

SONARDYNE (U.K)

Teledyne Technologies Incorporated. (U.S.)

Thales Group (France)

Ultra (U.K)

The SONAR systems market is highly competitive, with many companies contributing to its development. Key trends in the market include surveillance network SONAR, diver detection systems, dual-axis SONAR (DAS), and chirp technology. Leading players dominate due to their diverse product offerings and strong focus on research and development. For instance, in March 2020, Impact Subsea introduced the ISS360 SONAR, the world’s smallest imaging SONAR. It delivers high-quality images with a range of up to 90 meters (295 feet).

Teledyne Technologies Incorporated stands out by offering a wide range of 2D and 3D SONARs, acoustic modems, and data visualization/charting software. Their technology is designed to accommodate all types of sound navigation systems for naval vessels.

Segments:

On the basis of product type, the market is divided into sonobuoy, stern-mounted, hull-mounted, and DDS. On the basis of application, the market is split into defense and commercial. On the basis of platform, the market is divided into airborne and ship type. On the basis of solution, the market is divided into hardware (control units, transmitter and receiver, displays sensors, which is further divided into ultrasonic diffuse proximity sensors, VME-ADC, ultrasonic through-beam sensors, ultrasonic retro-reflective sensors, and others), and software. On the basis of end-user, the market is bifurcated into retrofit and line fit. Geographically, the market is classified into Europe, North America, Asia Pacific, and the Rest of the World.

Report Coverage:

The research report provides a thorough examination of the market. It focuses on key aspects such as leading companies, various platforms, product types, solutions, and SONAR system applications. Apart from that, the report provides insights into market trends and highlights important industry developments. In addition to the aforementioned factors, the report includes a number of factors that have contributed to the development of the developed market in recent years.

Drivers & Restraints:

Tactical Defense Operations are Surging the Demand for Sonobuoys

A sonobuoy is a sophisticated underwater acoustic research system that naval ships drop or eject. Sonobuoys use a sophisticated transducer and a radio transmitter to record and transmit underwater sounds. Other environmental data, such as wave height and water temperature, are also provided by special-purpose buoys. The market is expected to expand as the use of sonobuoys in military vessels expands. However, the steep cost associated with SONAR development may impede the SONAR system market growth.

Regional Insights:

North America to be a Dominant Region of the Global Market

North America dominated the market in 2021, with market size of USD 665.5 million. North America's dominance is owing to the rise in naval shipbuilding in the U.S. 82 new ships costing up to USD 147 billion will be added in the U.S. between 2022 - 2026, according to a shipbuilding plan announced in 2020.

Asia Pacific will experience remarkable growth as a result of increased naval spending and an increase in domestic ship manufacturing in China and South Korea. Ship deliveries in Japan have grown and various South Korean shipbuilding players have integrated automation into ship systems to drive the market development.

As the SONAR system market share increases in Europe, this is largely driven by the introduction of a new generation of threat detection and identification capabilities in ships and the retrofitting of vessels with autonomous engineering systems. Increased investment in marine system upgrades is anticipated to fuel the market in the U.K.

Competitive Landscape:

The dominant factor responsible for these key market players' dominance is a diverse product portfolio combined with R&D activity. Impact Subsea will launch the ISS360 SONAR, the world's tiniest imaging SONAR, in March 2020. It has a capacity of up to 90 meters/295 feet and provides excellent image quality.

Key Industry Development:

February 2022: Leonardo SpA awarded ELAC SONAR a USD 58 million contract to supply SONAR systems for two new submarines supplied by Fincantieri for the Italian Navy.

0 notes

Text

Securing the Skies: The Role of AI in Aerospace and Defense

The global AI in aerospace and defense market size was valued at USD 22.45 billion in 2023 and is projected to grow at a CAGR of 9.8% from 2024 to 2030. AI-driven systems analyze data from various sources to optimize maintenance schedules, manage supply chains, and improve logistics. Predictive maintenance powered by AI reduces unexpected equipment failures and downtime by forecasting when components need service before they break down. Additionally, AI enhances decision-making processes by providing actionable insights through data analytics, leading to streamlined operations, reduced costs, and improved resource allocation.

AI advancements in surveillance and threat detection revolutionize aerospace and defense operations by processing and analyzing vast amounts of data from sensors, satellites, and other sources in real time. AI systems use machine learning algorithms to detect and identify potential threats with high accuracy, reducing false alarms and improving overall situational awareness. These systems can integrate data from diverse sources to provide comprehensive and timely intelligence, enabling more effective monitoring of borders, airspace, and strategic locations. Enhanced threat detection capabilities lead to quicker and more precise responses, improving national security and defense readiness while ensuring better protection of assets and personnel.

AI In Aerospace And Defense Market Segmentation Highlights

The hardware segment accounted for the largest market share in 2023. The market is driven by the increasing demand for advanced computing and processing power necessary for AI applications.

The on-premises segment accounted for the largest market revenue share in 2023. The market is growing due to the need for secure and controlled environments where sensitive data and applications can be managed with high confidentiality.

The airborne segment accounted for the largest market revenue share in 2023. The market is driven by the growing use of AI technologies in aviation and military aircraft to enhance operational capabilities and safety.

The machine learning segment accounted for the largest market revenue share in 2023. The market is driven by the ability to analyze complex datasets and make data-driven predictions.

Surveillance and monitoring accounted for the largest market revenue share in 2023. The market is expanding due to the critical need for enhanced security and situational awareness.

Segments Covered in the Report

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global AI in aerospace & defense market report based on offering, deployment type, platform, technology, application, end use, and region.

Offering Outlook (Revenue, USD Million, 2018 - 2030)

Hardware

Processors

Memory Devices

Network Devices

Software

AI Solutions

AI Platforms

Services

Deployment & Integration

Support & Maintenance

Deployment Type Outlook (Revenue, USD Million, 2018 - 2030)

Cloud-based

On-premises

Platform Outlook (Revenue, USD Million, 2018 - 2030)

Land

Naval

Airborne

Space

Technology Outlook (Revenue, USD Million, 2018 - 2030)

Machine Learning

Natural Language Processing (NLP)

Computer Vision

Context-Aware Computing

Robotics

Big Data Analytics

Application Outlook (Revenue, USD Million, 2018 - 2030)

Predictive Maintenance

Surveillance & Monitoring

Mission Systems

Cybersecurity

Data Analytics

Autonomous Systems

Navigation & Guidance Systems

Others

End-use Outlook (Revenue, USD Million, 2018 - 2030)

Commercial

Government & Law Enforcement

Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

UK

France

Asia Pacific

China

Japan

India

South Korea

Australia

Latin America

Brazil

Middle East and Africa (MEA)

UAE

Saudi Arabia

South Africa

Order a free sample PDF of the AI In Aerospace And Defense Market Intelligence Study, published by Grand View Research.

0 notes

Text

The Ascending Aerostat Market: A Comprehensive Analysis

The aerostat market is surging, incorporating its high diversity of airborne platforms such as airships, blimps, and tethered balloons, driven by the combination of technological breakthroughs with growing demand across various fields. Aerostats have benefits toward surveillance and communications, scientific research, and even advertising, thereby offering unique advantages over traditional aircraft as well as drones.

The aerostat market is expected to rise from US$ 8.45 billion in 2023 to US$ 16.70 billion by 2031, at a CAGR of 8.9% during the forecast period of 2023–2031.

Market Dynamics

Key Drivers

Improved Surveillance Capabilities: Aerostats are used for persistent, wide-area surveillance for border security, disaster management, and law enforcement purposes.

Telecommunications Infrastructure: The equipment can be used for rapid or permanent installation of the telephone network in sparsely populated or disaster-hitting areas.

Scientific Research: The Aerostat is put to practical applications for atmospheric and climatic studies and space explorations. Advertising and Marketing: Aerostats offers an adventurous and glamorous way of showing brands and products.

Market Restraints

Adverse weather factors could increase the sensitivity of operating such aerostats which in turn include strong winds along with heavy rains.

High Upfront Investment: Building and launching aerostat systems demand a lot of upfront investment.

Strict Airspace and Aviation Safety Regulations: Aerostat operations are bound by regulations that regulate airspace and ensure aviation safety.

Market Segmentation

By Product Type

Airships

Balloons

Hybrid Aerostat

HAPS

By Payload

Surveillance Radar

Navigation System

Communication Relays

By Application

Military and Commercial

By Region

North America

Europe

Asia-Pacific

South and Central America

Middle East and Africa

Key Players

Aero

Allsopp Helikites Ltd

ILC Dover

Israel Aerospace Industries Ltd

Lindstrand Technologies Inc

Lockheed Martin Corporation

Raven Industries Inc

Raytheon Company

RT

Future Outlook

Aerostat Market to grow with immense momentum ahead, considering the developments and advancements in technology, raising demand for surveillance and communication solutions, and the newer applications that are coming along. Key trends to keep an eye on include AI and IoT integration - integration of artificial intelligence and Internet of Things will further empower aerostats by giving advanced data analysis capabilities and autonomous operation.

Hybrid Airships- Incorporating into the airships the advantages of aircraft for improved performance and efficiency.

Increased Use in Renewable Energy: Aerostats can carry heavy elements of renewable energy projects to reduce transportation costs while saving the environment.

Conclusion-

The aerostat market is dynamic and highly evolving. With the help of technological advancement and overcoming regulatory challenges, this industry is very well poised to play a critical role in the future of aviation and aerospace. Frequently Asked Questions-

Which is the largest regional market for Aerostat?

Ans: - North America is the largest regional market for Aerostat.

Which companies have the maximum share in the Aerostat market?

Ans: - Aeros, Allsopp Helikites Ltd, ILC Dover, Israel Aerospace Industries (IAI), Lindstrand Technologies Limited, Raven Industries Inc, Raytheon Technologies Corporation, Lockheed Martin Corporation, RT, and TCOM LP are some top companies that hold maximum market shares.

What is the growth rate expected for this market during the period from 2023 to 2031?

Ans: - The Aerostat market is expected to grow at a growth rate of 8.9% during the forecast period.

How big is the Aerostat market?

Ans: - The global market size for Aerostat reached US$ 8.45 billion in 2023 and is expected to reach US$ 16.70 billion by 2031.

What are the different segments in the Aerostat market?

Ans: The Aerostat market is segmented into Product Type, Payload, Application, and region.

About Us-

The Insight Partners is among the leading market research and consulting firms in the world. We take pride in delivering exclusive reports and sophisticated strategic and tactical insights into the industry. Reports are generated through a combination of primary and secondary research, solely aimed at giving our clientele a knowledge-based insight into the market and domain. This is done to assist clients in making wiser business decisions. A holistic perspective in every study undertaken forms an integral part of our research methodology and makes the report unique and reliable.

0 notes

Text

Driving Forces in the UAV Propulsion Systems Market: Key Insights and Forecast

The UAV (Drone) Propulsion System Market is experiencing significant growth, driven by advances in technology, increased demand across various sectors, and innovations in propulsion system efficiency. Projected to grow from USD 6,994 million in 2024 to USD 11,098 million by 2029, this market is expanding at a compound annual growth rate (CAGR) of 10.9%. In this post, we’ll dive into the fundamentals of UAV propulsion systems, explore how they work, identify key growth drivers and opportunities, examine leading players in the field, and review recent developments shaping this industry.

What is a UAV (Drone) Propulsion System?

UAV propulsion systems are essential components that power unmanned aerial vehicles (UAVs), enabling them to take off, maneuver, and perform a variety of tasks. Depending on their mission requirements, UAVs are fitted with propulsion systems ranging from electric motors and battery-powered systems to more complex internal combustion engines.

The choice of propulsion system impacts the UAV’s efficiency, range, and endurance, making it a critical factor in UAV design and application.

How UAV (Drone) Propulsion Systems Work

UAV propulsion systems convert stored energy (from fuel or batteries) into thrust, which allows the UAV to fly. Here are some common types of UAV propulsion systems:

Electric Propulsion Systems Electric propulsion, often powered by lithium-ion or lithium-polymer batteries, is widely used in smaller UAVs. Electric motors convert electrical energy into mechanical energy, which drives the propellers and allows the drone to lift and maneuver. Electric systems are quiet, have fewer emissions, and are easy to maintain, making them popular for commercial and recreational drones.

Internal Combustion Engines (ICE) For larger UAVs and those with extended range requirements, internal combustion engines (ICE) are often used. ICE systems, such as gasoline or diesel engines, offer greater power and endurance than electric systems, making them ideal for military and industrial applications.

Hybrid Propulsion Systems Hybrid propulsion systems combine electric and internal combustion engines, offering the benefits of both. The electric motor powers the drone during take-off and landing, while the ICE takes over during cruising, optimizing fuel efficiency and extending the UAV’s range.

Solar-Powered Systems Solar-powered propulsion systems use solar panels mounted on the UAV to generate energy from sunlight. These systems are used primarily for long-endurance drones, such as those used for environmental monitoring or telecommunications, allowing them to stay airborne for extended periods without refueling.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=211810670

UAV (Drone) Propulsion System Market Growth Drivers

Several key factors are driving the growth of the UAV propulsion system market:

Increased Demand for UAVs Across Industries Drones are increasingly used in sectors such as agriculture, logistics, defense, surveillance, and environmental monitoring. This diversified application drives the demand for more efficient and specialized propulsion systems, especially as industries seek longer flight times and improved efficiency.

Technological Advancements in Propulsion Systems Advances in battery technology, hybrid propulsion systems, and lightweight materials contribute to the development of UAV propulsion systems with longer endurance, greater efficiency, and reduced emissions. Innovations such as hydrogen fuel cells and solar-powered UAVs are also pushing the boundaries of drone capabilities.

Rising Military and Defense Expenditure Military and defense agencies worldwide are investing heavily in UAVs for surveillance, reconnaissance, and combat operations. This investment includes research and development in high-performance propulsion systems that enhance the endurance, range, and payload capacity of military drones.

Regulatory Support and Initiatives Governments globally are recognizing the potential of UAVs and are establishing regulations to enable safe drone operation. These regulations, coupled with government initiatives to promote drone usage, support the growth of the propulsion system market.

Growing Adoption in E-commerce and Delivery Services The use of UAVs in last-mile delivery is gaining traction, with companies such as Amazon and UPS investing in drone fleets for package delivery. This application requires efficient propulsion systems to support the frequent take-offs, landings, and short-haul flights needed for urban delivery.

Market Opportunities for UAV (Drone) Propulsion Systems

The UAV propulsion system market presents numerous growth opportunities, including:

Development of High-Efficiency Batteries With the increased use of electric propulsion systems, there is a growing demand for advanced battery technology. Lightweight, high-density batteries with fast-charging capabilities are crucial for enhancing the range and flight time of electric UAVs.

Emerging Markets in Developing Countries Countries in Asia, Africa, and Latin America are witnessing a rise in UAV adoption for agricultural monitoring, infrastructure inspection, and mapping. This expansion offers opportunities for propulsion system manufacturers to enter these emerging markets.

Integration of Renewable Energy Sources Solar-powered UAVs are becoming a popular choice for long-endurance applications such as environmental monitoring and disaster management. As technology advances, there are opportunities to develop more efficient solar panels and energy storage systems for UAVs.

Focus on Lightweight and Compact Propulsion Systems Miniaturization and material advancements are enabling the production of lightweight and compact propulsion systems, which can support smaller UAV designs and increase payload capacity. This trend is particularly relevant for applications in surveillance and inspection.

Demand for Hybrid Systems Hybrid propulsion systems, combining electric and internal combustion engines, are increasingly in demand for their flexibility and extended flight duration. Companies investing in hybrid propulsion technology have the potential to lead the market as hybrid systems become more popular.

Ask for Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=211810670

Key Players in the UAV (Drone) Propulsion Systems Market

Several key players dominate the UAV propulsion system market:

Honeywell International Inc. Known for its extensive experience in aerospace technologies, Honeywell produces propulsion systems tailored to various UAV applications, focusing on efficiency and durability.

Rolls-Royce Holdings Rolls-Royce specializes in high-performance propulsion systems for military drones, leveraging its expertise in aviation engines.

Orbital Corporation Orbital Corporation offers innovative propulsion systems for UAVs, including heavy-fuel engines that provide increased endurance for military applications.

AeroVironment, Inc. A leader in electric propulsion systems, AeroVironment focuses on creating lightweight and efficient solutions for tactical UAVs.

GE Aviation GE Aviation supplies advanced propulsion technologies, with an emphasis on hybrid-electric systems and fuel efficiency.

Recent Developments in the UAV Propulsion Systems Market

Honeywell’s New Turbo Engines for Tactical Drones In 2023, Honeywell introduced a new line of turbo engines designed for small tactical UAVs, providing enhanced performance in harsh environments.

Rolls-Royce’s Hybrid Propulsion System Rolls-Royce developed a hybrid-electric propulsion system that offers extended endurance and reduced fuel consumption, set to be integrated into UAVs used in defense applications by 2024.

Partnership Between GE Aviation and Hybrid-Electric Tech Firms GE Aviation partnered with companies specializing in hybrid-electric propulsion to accelerate the development of hybrid systems for commercial UAV applications.

AeroVironment’s High-Density Battery Packs AeroVironment launched a new series of high-density battery packs, which provide longer flight times for electric UAVs used in surveillance and reconnaissance.

Frequently Asked Questions (FAQs)

Q1: What is a UAV propulsion system? A UAV propulsion system powers drones, enabling them to fly by converting stored energy into thrust. Common systems include electric motors, internal combustion engines, and hybrid systems.

Q2: What are the key drivers of the UAV propulsion system market? Key drivers include increased demand for drones across industries, technological advancements, rising defense expenditure, regulatory support, and adoption in delivery services.

Q3: What are some emerging trends in UAV propulsion technology? Trends include the use of hybrid propulsion systems, high-density batteries, solar-powered systems, and lightweight materials.

Q4: Which regions are experiencing the highest growth in this market? North America and Europe lead the market, with Asia Pacific projected to show the fastest growth due to rising UAV adoption for commercial and defense purposes.

Q5: Who are the major players in the UAV propulsion systems market? Key players include Honeywell International Inc., Rolls-Royce Holdings, Orbital Corporation, AeroVironment, and GE Aviation.

To Gain Deeper Insights Into This Dynamic Market, Speak to Our Analyst Here: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=211810670

Key Takeaways

The UAV propulsion system market is set to grow from USD 6,994 million in 2024 to USD 11,098 million by 2029, at a CAGR of 10.9%.

Electric, internal combustion, and hybrid propulsion systems are the most common types used in drones, each catering to different operational requirements.

The market is driven by advancements in battery technology, increased UAV adoption across industries, and government support.

Key players like Honeywell, Rolls-Royce, and AeroVironment are making significant strides in UAV propulsion innovations.

Opportunities lie in developing high-efficiency batteries, entering emerging markets, and integrating renewable energy sources.

The UAV propulsion system market is set to expand rapidly as new technologies emerge, and as drones become indispensable across multiple industries. With a projected market value of $11,098 million by 2029, companies investing in efficient and innovative propulsion systems are well-positioned to capitalize on this growth. Whether you’re an investor, manufacturer, or technology enthusiast, the UAV propulsion system market offers exciting opportunities and remains an area to watch closely in the coming years.

#uav propulsion systems#drone propulsion market#uav engine technology#drone motor growth#uav power systems#key players uav propulsion#uav market opportunities

0 notes

Text

Synthetic Aperture Radar Market set to rise $11.1 billion by 2030, as Increased Application in Climate Monitoring hits transformation ground

According to a recent research, Industry revenue for Synthetic Aperture Radar is expected to rise to $11.1 billion by 2030 from $5.1 billion of 2023. The revenue growth of industry players is estimated to average at 11.7% annually for period 2023 to 2030. Growing end-industry applications in major countries like U.S., Germany and China, is driving the market demand high.

Research Study analyse the new revenue pockets, emerging markets, competition landscape, opportunities & niche insights for Type (Space-Based, Airborne, Ground-Based), Mode (Single Polarization, Dual Polarization, Full Polarization) and Frequency Band (X-Band, C-Band, L-Band, S-Band).

Access the detailed report here - https://datastringconsulting.com/industry-analysis/synthetic-aperture-radar-market-research-report

Regional Analysis

North America and Asia-Pacific are the two most active and leading regions in the market. SAR technology is being increasingly embraced in the Asia Pacific region for purposes such as disaster response and environmental surveillance with a focus in Japan and China where companies such as ICEYE and Synspective are scaling up to cater to the growing needs of the region.

With challenges like high development and launch costs, complex data processing requirements and limited bandwidth in some regions, Synthetic Aperture Radar market’s supply chain from component supplier to end-user is expected to evolve & expand further; and industry players will make strategic advancement in emerging markets including India, Brazil and Australia for revenue diversification and TAM expansion. Satellite based remote sensing (RS) is becoming more prevalent in monitoring climate change by offering information on changes in land use patterns and forests as well as the thickness of ice.

Industry Leadership and Strategies

The Synthetic Aperture Radar market is characterized by intense competition, with a number of leading players such as Airbus, Capella Space, MDA, ICEYE, Northrop Grumman, Raytheon Technologies, Lockheed Martin, Qorvo, Cobham, Boeing, Honeywell and Synspective. These players are pushing & penetrating the market with their strategies.

About DataString Consulting

DataString Consulting assist companies in strategy formulations & roadmap creation including TAM expansion, revenue diversification strategies and venturing into new markets; by offering in depth insights into developing trends and competitor landscapes as well as customer demographics. Our customized & direct strategies, filters industry noises into new opportunities; and reduces the effective connect time between products and its market niche.

DataString Consulting offers complete range of market research and business intelligence solutions for both B2C and B2B markets all under one roof. DataString’s leadership team has more than 30 years of combined experience in Market & business research and strategy advisory across the world. Our Industry experts and data aggregators continuously track & monitor high growth segments within more than 15 industries and 60 sub-industries.

0 notes

Text

The solar-powered drone market is currently experiencing a transformative phase, solidifying its position as a key player in the UAV sector. The financial landscape of this market reveals substantial growth, reaching 986.54 million USD in 2023 and projected to surge to 3,181.2 million USD by 2032, reflecting an impressive compound annual growth rate (CAGR) of 13.9%.The solar-powered drone market has emerged as a promising sector within the larger landscape of unmanned aerial vehicles (UAVs). With the increasing global push for renewable energy sources and the expanding use of drones across various industries, solar-powered drones are at the forefront of innovation. These drones are equipped with solar panels that enable them to harness solar energy, extending their flight endurance and reducing their reliance on conventional power sources like batteries or fuel. This article delves into the current trends, key applications, and the future potential of the solar-powered drone market.

Browse the full report https://www.credenceresearch.com/report/solar-powered-drone-market

Market Overview

Solar-powered drones are designed to use photovoltaic cells to convert sunlight into electricity, which is then used to power their engines and systems. This technology offers numerous advantages, including longer flight times and reduced operational costs, making it appealing for both commercial and military applications. As the demand for sustainable and energy-efficient solutions grows, so too does the interest in solar-powered drones. The market is currently experiencing rapid expansion, with several key players such as AeroVironment, Facebook (through its Aquila project), and Google (through Project Titan) spearheading development.

Current Trends in the Solar-Powered Drone Market

1. Growing Adoption in Surveillance and Monitoring One of the primary applications of solar-powered drones is in the field of surveillance and monitoring. These drones are ideal for use in remote areas where traditional power sources are limited. They can stay airborne for extended periods, making them suitable for border security, wildlife monitoring, agricultural surveys, and environmental studies. For example, in agriculture, solar-powered drones can monitor crop health, optimize irrigation, and provide real-time data on soil conditions, allowing farmers to make informed decisions.

2. Increasing Interest from the Military Sector The military has shown significant interest in solar-powered drones for reconnaissance and intelligence-gathering missions. Unlike traditional drones, which need to land frequently for refueling or battery recharging, solar-powered drones can remain in the air for days or even weeks, making them ideal for long-duration missions. This capability offers a strategic advantage in areas where constant surveillance is critical. Additionally, solar-powered drones are often quieter than their fuel-powered counterparts, making them less detectable during operations.

3. Sustainable Solutions for Communication Solar-powered drones are increasingly being explored for use in communication networks. In areas with limited or no access to internet infrastructure, these drones can serve as high-altitude communication relays, providing connectivity to remote regions. Companies like Facebook and Google have experimented with solar-powered drones to create airborne networks, aiming to bring the internet to underserved areas. If successful, these initiatives could revolutionize global connectivity and bridge the digital divide.

4. Technological Advancements The solar-powered drone market is witnessing rapid technological advancements, particularly in solar cell efficiency, lightweight materials, and battery storage systems. Researchers are working to improve the energy conversion rates of photovoltaic cells and develop more efficient energy storage systems to enhance drone performance. Furthermore, the use of lightweight, durable materials is helping manufacturers design drones that can carry larger payloads without compromising flight duration.

Key Challenges Facing the Market

While the solar-powered drone market is poised for growth, it also faces several challenges. One of the primary obstacles is the limited efficiency of current solar cells. Even the most advanced solar cells can only convert a fraction of the sunlight they receive into usable energy. This limitation restricts the payload capacity and operational range of solar-powered drones. Additionally, solar-powered drones may struggle to perform optimally in regions with inconsistent sunlight or during nighttime operations.

Regulatory hurdles also present a challenge. As the number of drones in the sky increases, so too does the need for clear regulatory frameworks to ensure safe and efficient airspace management. Governments around the world are working to develop policies and regulations that accommodate the growing use of drones while addressing safety, privacy, and security concerns.

Future Prospects and Market Outlook

Despite these challenges, the future of the solar-powered drone market looks promising. The growing demand for renewable energy solutions, coupled with advances in solar technology, is expected to drive market growth in the coming years. According to market research, the global solar-powered drone market is projected to grow significantly, with applications in agriculture, defense, telecommunications, and disaster management leading the way.

As solar cells become more efficient and lightweight, solar-powered drones will be able to carry heavier payloads and operate in more challenging environments. Additionally, the development of hybrid drones, which can switch between solar power and conventional energy sources, may further expand the range of applications for these UAVs.

Key Players

Airbus Group

AeroVironment, Inc.

SunPower Corporation

Bye Aerospace

NASA (National Aeronautics and Space Administration)

Alta Devices

Sunlight Aerospace

Segmentation of the solar-powered drone market

By Product Type:

Fixed Wing

Rotary Wing

Hybrid Wing

By Application:

Mapping and Survey

Inspection and Maintenance

Filming and photographing

Surveillance and Monitoring

Precision Agriculture

Others

By End User:

Delivery and Logistics

Agriculture and Forestry

Oil & Gas

Construction and Mining

Media & Entertainment

Security and Law Enforcement

Recreational Activity

Others

By Region

North America

The U.S.

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/solar-powered-drone-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

0 notes

Text

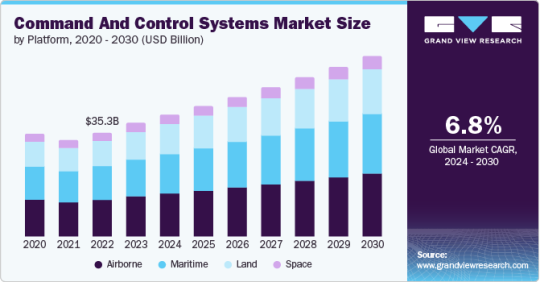

Command And Control Systems Market To Reach $61.09 Billion By 2030

The global command and control systems market size is expected to reach USD 61.09 billion by 2030, expanding at a CAGR of 6.8% from 2024 to 2030, according to a new report by Grand View Research, Inc. The growing significance of situational awareness in the military, coupled with the increasing need for security and surveillance in law enforcement activities, manufacturing industries, and utilities, is driving the market growth. Moreover, geopolitical conflicts across various parts of the world are stimulating the demand for command and control (C2) systems due to the technological competencies provided by them, thereby positively influencing the market.

Market growth is further driven by the rising demand for C2 technology in the defense and commercial sectors, owing to its ability to combine various disciplines and interconnect them to optimize operations. In the commercial sector, fixed command and control centers are used to monitor and manage vital infrastructure, industrial sites, ports, harbors, and private airports, increasing demand in this segment, and thereby favoring market expansion.

A significant rise in military budgets across various countries and the emergence of cutting-edge defense technologies are major factors expected to boost C2 systems' demand. For instance, in April 2024, the U.S. Marine Corps awarded a USD 25 million contract to BAE Systems plc in addition to the previous USD 181 million contract for Amphibious Combat Vehicles (ACVs). ACV-P is the first in a range of four variants to be delivered to the Marine Corps, and its additional variants are comprised of ACV Command and Control (ACV-C), which is currently in production. Such initiatives are creating significant growth opportunities for the C2 systems market.

Growing investments in naval development worldwide, along with increasing global trade activities and the use of cargo ships in maritime trade, contribute to market growth. For instance, in November 2023, the U.S. Department of Transportation’s Maritime Administration announced allocating more than USD 653 million to fund 41 port improvement projects across the country as part of the Port Infrastructure Development Program (PIDP).

Request a free sample copy or view report summary: Command And Control Systems Market Report

Command And Control Systems Market Report Highlights

Based on platform, the maritime segment is estimated to register the highest CAGR from 2024 to 2030 owing to increasing marine trade, the need for safety and security of shipping operations, and growing investments in naval forces across various countries

Based on solution, the hardware segment accounted for the largest revenue share in 2023 owing to rising demand for robust hardware that enhances the functionality and effectiveness of C2 systems

Based on application, the defense segment dominated the market in 2023 as several governments are aggressively pursuing defense modernization initiatives amid rising security concerns and growing armed conflicts in different parts of the world

In February 2024, Northrop Grumman demonstrated a new software that receives, displays, and shares critical situational awareness data through handheld devices without connecting to a cloud server, protecting warfighters in support of Joint All-Domain Command and Control

Command And Control Systems Market Segmentation

Grand View Research has segmented the global command and control systems market report based on platform, solution, application, and region:

C2 Systems Platform Outlook (Revenue, USD Million, 2018 - 2030)

Land

Maritime

Space

Airborne

C2 Systems Solution Outlook (Revenue, USD Million, 2018 - 2030)

Hardware

Software

Services

C2 Systems Application Outlook (Revenue, USD Million, 2018 - 2030)

Defense

Commercial

C2 Systems Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Asia Pacific

China

India

Japan

South Korea

Australia

Latin America

Brazil

Middle East & Africa (MEA)

UAE

Saudi Arabia

South Africa

List of Key Players of Command And Control Systems Market

Lockheed Martin Corporation

BAE Systems

Collins Aerospace

Thales Group

Leonardo S.p.A.

Elbit Systems Ltd.

Boeing

Northrop Grumman

Saab

CACI International Inc

Barco NV

Christie Digital Systems USA, Inc.

InFocus Corporation

Activu

Panasonic Corporation

Planar

Datapath Ltd.

Extron Electronics

Matrox

Hiperwall, Inc.

Green Hippo Ltd. (tvOne)

RTX Corporation

tvONE

RGB Spectrum

Userful Corporation

VuWall Technology Inc.

0 notes

Text

0 notes

Text

0 notes