#Non-Woven Fabrics Market Share

Link

The Non-Woven Fabrics Market size is estimated to reach US$58.7 billion by 2027 after growing at a CAGR of 6.1% during the forecast period 2022-2027.

0 notes

Text

Meet new sewing pattern <Komugi> Over shirt

A new item is just published from Waffle Patterns. Meet Over shirt <Komugi> sewing pattern, a work wear style over shirt with many functional pockets. Depending on your fabric and design choice, it will be a work shirt, uniform-like service shirt or outdoor style shirt jacket. You can make just a simple shirt as well.

<design options>

View A features a hidden button stand front opening + patch side pockets + an inside pocket. The patch side pockets are 2 types ; side opening or layered type. The cuff is no-opening design.

View B has a normal button stand + seam pocket + back bent and cuff opening.

The chest pocket design has 2 options, layer type or zipper pocket.

View A is intended as non-scratch design suitable for a work shirt especially if you are working on fragile things.

View B can be made as a more outdoor-like shirt jacket with details like cuff openings or a vent.

But of course you can choose and mix the options as you like!

The khaki sample in the photos features viewA, and the red plaid one is view B. The caramel brown one has mixed features.

My favourite feature is the sleeve patches. Adding compliment textures/colours is really fun! But you can sew without them, too.

Please make your creative style by mixing your favourite details.

<fabric recommendation>

The pattern is drafted for woven fabrics. Light-medium weight durable shirt fabrics are recommended. like corduroy, duck, twill, denim, linen, flannel, light wool or canvas etc.

It is not impossible to use very light drapery fabric, but those are not suitable for some details like patch pockets or vent.

Also, some very thick/stiff fabrics might not work well for details like pockets with facing. In that case, please consider using other lighter fabrics partly like the inside yoke, facing, or pocket parts.

Please choose a suitable one for your design intension.

For the caramel brown sample in the photos, I used cotton canvas. Suitable for work shirts and very easy to handle. The contrast fabric used for the sleeve patch and pocket layer is faux suede.

If you want very durable patches, leather or rubber-mixed fabrics are used for professional work apparel. But for general daily usage, like mine, design oriented choice like nice compliment colours or textures will be enough. Using leftover or old clothes is a fun choice, too.

The khaki sample is cotton ripstop. This one is also very suitable for work wear. The patch part is mixed twill.

The red plaid one is light wool backed fleece. I backed all the pieces with fleece except the folded parts like pocket openings or hem.

I bought all those fabrics from my local fabric market, but most of them are from years ago. I wanted to share where I bought them, but I actually forgot all.

I think light water repellent or windproof fabrics are nice functional options, too.

<Size>

The shirt is drafted regular fit.

I made on size bigger the red plaid sample because I wanted to wear this as a jacket. Also because the fabric gets thicker with fleece backing.

The caramel brown and khaki samples were made with just fit size.

<Other material>

If you attach the hidden button stand design, it is better to use flat and thin buttons for clean look opening.

*********************

The sewing pattern includes 18 pages of instructions and all the sewing processes are described with detailed illustrations. The pattern files are available for both home printers (A4 or US letter) and copyshop(A0 format).

You can check other photos of this model on my Flickr page.

The over shirt -Komugi- (size 32 - 54) PDF sewing pattern is available here. Also in the Etsy shop.

Special discount price until 13th Mar 2024 (CET) with other popular patterns. No discount code is needed! The sale page is here.

***** Special offer for Paper pattern and free shipping

Paper pattern + PDF option is available limited time. *The paper includes only the pattern, please print out the instruction by yourself or read it with your tablet or PC. The PDF + Paper listing page is here.

Enjoy your sewing!

(Japanese post here 日本語ポストはこちら).

**********************

follow me! Instagram /// Facebook /// Shop /// Pinterest /// Newsletter

62 notes

·

View notes

Text

Wilton Manors, FL: Embracing Life's Vibrancy Through Community and Diversity

Nestled in the heart of South Florida, Wilton Manors captures the essence of a vibrant and inclusive way of living that resonates with both residents and visitors. This charming city, often referred to as the "Island City," exudes a unique energy that stems from its strong sense of community, a celebration of diversity, and an array of engaging activities that enrich everyday life.

Wilton Manors is a haven where diversity isn't just acknowledged – it's celebrated. The city's LGBTQ+ inclusivity is woven into its fabric, creating an environment where individuals from all walks of life can find a place to call home. The Wilton Drive district serves as the epicenter of LGBTQ+-owned businesses, bustling nightlife, and lively events that promote acceptance, unity, and love.

Living in Wilton Manors means being part of a close-knit community that thrives on connections. The streets come alive with local gatherings, farmers' markets, and cultural festivals that foster a sense of togetherness. Whether you're enjoying a leisurely stroll along Wilton Drive, participating in community-driven initiatives, or simply sharing a friendly chat with neighbors, the city's emphasis on community engagement nurtures meaningful relationships that enhance the way of life.

Wilton Manors, FL, stands as a testament to the power of inclusivity, community, and the celebration of life's vibrancy. With its diverse culture, engaging activities, and the warm embrace of neighbors, the city offers a way of living that encourages connection, exploration, and the pursuit of happiness in all its forms.

When it comes to finding a reliable and efficient managed IT company, KB Technologies Managed IT Services emerges as the answer to all your technology needs. With expertise spanning cyber security, managed IT services, advanced control systems, and VOIP communication solutions, we are your trusted partner in navigating the complexities of the digital landscape.

In today's interconnected world, cyber security is non-negotiable. KB Technologies offers cutting-edge solutions that safeguard your business from ever-evolving threats. Our proactive approach involves implementing robust protocols to detect and neutralize potential breaches, ensuring your data remains secure and your operations undisturbed.

Beyond cyber security, our suite of services extends to optimizing your entire technology infrastructure. From seamless implementation of advanced access control systems to enhancing communication efficiency through VOIP solutions, KB Technologies ensures that your business operates smoothly. Our managed IT services provide the support you need, allowing you to focus on your core activities while we handle the intricacies of technology management.

Thank you for taking the time to read our article about Wilton Manors, FL. We hope you found it informative and inspiring. As you explore the vibrant community and consider your IT needs, remember that KB Technologies Managed IT is here to support you. Our comprehensive services, including cyber security, managed IT solutions, and more, are designed to empower your business for success. Feel free to reach out to us for all your technology requirements.

KB Technologies Managed IT

433 Plaza Real Ste 275, Boca Raton, FL 33432

(561) 288-2938

youtube

2 notes

·

View notes

Text

Polyester Staple Fiber Market: Regional Insights and Future Opportunities

Polyester Staple Fiber (PSF) is a synthetic fiber made from polyester, widely used in textiles, home furnishings, automotive, and non-woven fabrics. Known for its versatility, durability, and cost-effectiveness, PSF plays a crucial role in industries ranging from fashion to industrial applications. The market has seen steady growth due to increasing demand in various sectors, driven by rising urbanization, industrial development, and a growing focus on sustainability.

The global polyester staple fiber industry, valued at US$ 31.8 billion in 2023, is projected to grow at a CAGR of 4.7% from 2024 to 2034, reaching US$ 52.4 billion by the end of 2034.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/polyester-staple-fiber.html

Market Segmentation

By Service Type:

Virgin Polyester Staple Fiber

Recycled Polyester Staple Fiber

By Sourcing Type:

Polyethylene Terephthalate (PET)

Polybutylene Terephthalate (PBT)

By Application:

Apparel

Home Furnishings

Automotive

Construction

Industrial

By Industry Vertical:

Textile

Automotive

Healthcare

Packaging

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Analysis

Asia-Pacific: The dominant region due to the presence of large-scale textile industries in China and India. Favorable government policies supporting recycling and sustainability efforts further drive the market.

North America: Steady growth, driven by the rising demand for sustainable fibers and advancements in technology.

Europe: Strong focus on sustainability and circular economies, with countries like Germany and France leading in recycled fiber adoption.

Latin America & Middle East/Africa: Growing demand for PSF, with a focus on industrial and automotive applications.

Market Drivers and Challenges

Drivers:

Growing demand for eco-friendly fibers and sustainable textiles.

Rising urbanization and disposable income, boosting the textile and home furnishings sectors.

Advancements in recycling technologies, increasing the availability of recycled PSF.

Increasing demand in automotive and construction industries due to the material's durability and versatility.

Challenges:

Fluctuating raw material prices, especially petroleum-based materials.

Environmental concerns related to non-recycled polyester production.

Competition from natural fibers and other synthetic alternatives like nylon and acrylic.

Market Trends

Sustainability and Recycling: The push towards circular economies has led to increased adoption of recycled polyester staple fibers.

Innovation in Manufacturing: Developments in PSF production technologies to reduce energy consumption and carbon emissions.

Increased Use in Automotive and Construction: The automotive and construction industries are increasingly adopting PSF due to its lightweight and durable properties.

Future Outlook

The future of the Polyester Staple Fiber market looks promising, driven by increased demand for sustainable fibers, advancements in recycling, and the continued growth of the textile and automotive industries. By 2034, recycled PSF is expected to account for a larger market share, as sustainability efforts and circular economies gain traction globally.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=2727<ype=S

Key Market Study Points

Analysis of market drivers and challenges.

Evaluation of sustainable practices and their impact on market growth.

Focus on technological advancements and innovations in PSF production.

Regional market dynamics and growth potential.

Competitive Landscape

Key players in the market include:

Indorama Ventures: A leader in PSF production with a strong focus on sustainability and innovation.

Toray Industries: Known for advancements in fiber technology and strong regional presence in Asia.

Reliance Industries: A major player with extensive production capabilities and focus on recycled fibers.

Alpek: A key producer with investments in recycled polyester fiber production.

Recent Developments

Sustainability Initiatives: Several leading companies have launched sustainability programs, emphasizing recycled PSF production.

Technological Advancements: Companies are increasingly investing in energy-efficient manufacturing processes, reducing their carbon footprint.

Expansion in Emerging Markets: Investments in production facilities in Asia-Pacific and Latin America are expanding market reach.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Carbon Fiber Market - Forecast (2024 - 2030)

Carbon Fiber Market Overview

Carbon Fiber Market size is forecast to reach $15.3 billion by 2030, after growing at a CAGR of 11% during 2024-2030. Carbon fiber is a high strength, low weight, high stiffness, conductive to electricity, and is one of the most corrosion and heat resistant material. Growing demand for lightweight products from aerospace & defense, automotive, and wind energy industries and minimizing carbon emissions are driving the market growth. Whereas, the growing building and construction sector in the emerging country is also driving the market growth. As carbon fiber is used primarily in the strengthening and reinforcement of concrete, steel, timber, and masonry. Furthermore, increasing demand for carbon fiber composite in consumer electronics has made the products lighter and thinner, and more textured is likely to drive the market growth. The carbon fiber market is witnessing a significant trend with an increased adoption in the automotive industry. As automotive manufacturers strive to enhance fuel efficiency and reduce emissions, carbon fiber composites offer a lightweight alternative to traditional materials. This shift is driven by the demand for electric and hybrid vehicles, where minimizing weight is crucial for optimizing energy efficiency and extending battery range. Carbon fiber's high strength-to-weight ratio contributes to improved vehicle performance and structural integrity. Moreover, advancements in manufacturing processes and cost reductions are making carbon fiber more economically viable for mass-produced automobiles. This trend signals a transformative shift in the automotive sector, with carbon fiber playing a pivotal role in the development of next-generation, sustainable transportation solutions. A notable development in the carbon fiber market is the increasing focus on sustainable production methods. With rising environmental concerns and a push for eco-friendly materials, carbon fiber manufacturers are exploring ways to minimize the environmental impact of their production processes. Innovations include the use of bio-based precursors, recycling of carbon fiber waste, and energy-efficient manufacturing techniques. This trend aligns with global efforts to achieve carbon neutrality and reduce the overall carbon footprint of industries. Sustainable carbon fiber production not only addresses environmental concerns but also caters to the growing demand for green products in various sectors, including aerospace, automotive, and renewable energy. As sustainability becomes a key consideration for businesses and consumers alike, the carbon fiber market is evolving to meet these changing expectations and contribute to a more environmentally responsible future.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐑𝐞𝐩𝐨𝐫𝐭 𝐒𝐚𝐦𝐩𝐥𝐞

Carbon Fiber Market Report Coverage

The report: “Carbon Fiber Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Carbon Fiber Industry.

By Raw Material: Polyacrylonitrile Based (PAN), Pitch Based (Mesophase Pitch Based, and Petroleum Pitch Based), and Others (Ultra High Elastic Modulus (UHM), High Elastic Modulus (HM), and Low Elastic Modulus (LM)).

By Tow Type: Continuous, and Chopped.

By Application: Composite, Non-Composite, Molding Compound, Woven Fabric, and Others.

By End-Use Industry: Aerospace & Defense (Fighter Jets, Armored Vehicles, Commercial Jets, Rotorcraft, Satellites, and Others), Automotive (Interior, Exterior, and Others), Sporting Goods (Tennis Rackets, Golf Club, Hockey Sticks, Archery, Others), Energy and Power (Wind, Solar, and Others), Building & Construction (Residential, Commercial, and Others), Marine, Healthcare, Electric & Electronic, and Others.

By Geography: North America, South America, Europe, Asia-Pacific, and Middle East & Africa

Key Takeaways

Europe will continue to have the major share of total worldwide wind energy carbon fiber demand during the forecast period owing to its renewable energy targets and use of offshore wind capacity.

High price of carbon fiber is one of the factors that’s hindering the markets growth.

COVID-19 will hinder the markets growth, as the end use industry are facing a slow growth, hence reducing the demand for carbon fiber.

Carbon Fiber Market Segment Analysis - By Raw Material

Polyacrylonitrile Based (PAN) segment held the largest share of more than 65% in the carbon fiber market in 2023. The PAN based component offers various benefits like low density, high strength, high modulus, high-temperature resistance, wear resistance, corrosion resistance, fatigue resistance, creepage resistance, electric conduction, heat conduction, and far-infrared radiation. These properties of PAN make it suitable to use across various end-use industries like the aerospace & aviation industry, automotive industry, wind turbines, anti-flame materials & clothes, and sports equipment. Thus, growth in these end-use industries further drive the market growth.

Carbon Fiber Market Segment Analysis - By Tow

Continuous tow segment held the largest share of more than 60% in the carbon fiber market in 2023. Continuous tow is the most widely used tow, due to its weight, compatibility with resins, and various range of sizing available for optimal processing. These are heavy tows with 50,000 filaments, each of these tows have heavy mechanical properties, which can be transferred to the finished products and components to enhance their properties such as strength, durability and structural properties. Furthermore, Continuous tows provide cost advantage, especially when used in a high-volume process, increases the reliability of the end product, enhance production efficiency and can be merged with all thermoset and thermoplastic resin systems. Continuous tow also makes carbon fiber far superior to glass and aramid fibers because of their added strength & stiffness and are used in manufacturing wind turbines, industrial, and automotive manufacturing. Therefore, these properties & advantages of continuous tow will further drive its demand in the market.

Carbon Fiber Market Segment Analysis - By Application

Composite segment held the largest share of more than 55% in 2023 and is forecasted to be the most utilized application of carbon fiber. The high strength, high thermal & electrical conductivity, light weight, and high modulus properties of composite makes them suitable to use across aerospace & defense, automotive, sports, and wind turbine industry, which are ideal for its growth. According to a 2022 report released by Aerospace Industries Association (AIA), in 2022 American aerospace & defense industry export amounted for $100.4 billion, which rose by 11.2 percent from 2021. The other industry driving the markets growth is automobile industry. For instance, a report released by Indian Brand Equity Foundation (IBEF) in 2023, In the first quarter of 2023-24, total production of passenger vehicles, commercial vehicles, three wheelers, two wheelers, and quadricycles was 6.01 million units. Furthermore, the growing demand for BMW i3 is also driving the market growth. As the BMW i3 is still the only car with a significant amount of carbon composite content.

#Carbon Fiber Market size#Carbon Fiber Market price#Carbon Fiber Market share#Carbon Fiber Market forecast

0 notes

Text

Industrial Filtration Market Analysis by Trends, Size, Share, Growth Opportunities, and Emerging Technologies

Market Overview

In 2024, the worldwide industrial filtration industry revenue was USD 34.2 billion, and the market is also projected to touch USD 55.7 billion by the end of 2030. This can be credited to the improvements in the filtration techs, severe government guidelines regarding emission control, increasing requirement for safe working atmosphere in industrial sites, and increasing need for equipment reliability and lifespan extension.

Furthermore, the constant growth of new products for industrial filtration and the rising food & beverage, metal & mining, and automotive industries are accountable for the market expansion.

The adoption of digital technology in filtration equipment presents a significant growth opportunity for the industry. This technology allows for continuous monitoring of industrial filters, incorporating sensors that track the status of air cleaners and provide real-time data to operators. By proactively identifying issues, digitalization enhances maintenance planning, minimizing unexpected downtime and optimizing equipment lifespan.

Moreover, it ensures filters are replaced promptly when necessary, preventing operational inefficiencies and extending machine longevity. The integration of Industry 4.0 further accelerates this digital transformation, enabling manufacturers to streamline operations, automate workflows, and leverage data for enhanced operational performance.

Key Insights

The non-woven fabric category held 35% revenue share, expected to remain dominant due to attributes like low weight, durability, and fire resistance, vital for pharmaceutical and mineral processing industries.

Activated carbon/charcoal category significant for its regenerable properties in continuous-filtration operations.

In the recent years, the chemicals & petrochemicals sector led with 40% revenue share, driven by pollutant production in manufacturing and environmental risks.

Pharmaceuticals category poised for growth, driven by stringent hygiene requirements to prevent contamination.

The liquid category dominated with over 60% revenue share, driven by environmental regulations and demand for clean water.

Filter press category forecasted fastest growth with over 7% CAGR, essential in food & beverage, metals & mining, pharmaceuticals, and industrial sectors.

HEPA system category prominent in the recent years for high efficiency in filtering airborne contaminants.

North America led with 45% revenue share in the recent years, driven by environmental concerns, workplace safety regulations, emissions control mandates, and R&D initiatives.

Industrial filtration critical for maintaining operational efficiency and compliance with environmental standards.

Increasing adoption of digitalization in filtration processes to enhance monitoring and maintenance efficiency.

Growing demand for filtration equipment in diverse industries such as food processing, automotive, and healthcare.

Innovations in filtration technologies to improve performance and reduce environmental impact.

Strategic partnerships and collaborations among key players to expand market presence and technological capabilities.

Rising investments in wastewater treatment infrastructure to meet stringent regulatory requirements.

Asia-Pacific emerging as a significant market due to industrial growth and increasing environmental awareness.

Source: P&S Intelligence

#Industrial Filtration Market Share#Industrial Filtration Market Size#Industrial Filtration Market Growth#Industrial Filtration Market Applications#Industrial Filtration Market Trends

1 note

·

View note

Text

A Comprehensive Guide to Medical Coveralls Procurement Intelligence

The global medical coveralls category is anticipated to grow at a CAGR of 7.4% from 2023 to 2030. The most important PPE in the world was the hooded disposable coveralls in 2020 - 2021. Due to the COVID-19 pandemic, there has been an increase in demand for disposable protective coveralls/apparel because of heightened awareness of self-protection. On a parent level, the PPE category is experiencing tremendous growth due to its industry-agnostic nature and varied applications. The growth of the category is being driven by emerging diseases, such as the September 2022 Ebola outbreak in Uganda and the SARS, new Omicron, and flu variants worldwide. This has increased the need for protection for frontline healthcare workers. All such factors are boosting the demand for medical coveralls globally.

Disposable protective coveralls can be categorized into various levels based on their strength of protection such as - Categories I (minimal risk), II (medium risk), and III (complex PPE). According to EU standards, the medical coveralls can be classified into different types - Type 1, 2, 3, 4, 5, and 6. The compliance requirements for types 1 to 4 include EN 14605 and EN 13982-1 for types 5 and 6. With advancements in technology, compliance requirements also play a key role. Over the years, medical coveralls have evolved from being basic garments into technologically advanced protective gear. As a result of technological advancements, coverall fabrics have also been designed to contain antimicrobial properties. Nanotechnology enabled the creation of nanoparticles embedded in coverall fibers for added protection. The latest medical coverall technology involves ‘smart’ coveralls with built-in sensors to monitor vital signs and alert healthcare professionals of any anomalies.

The medical coveralls category is highly fragmented. The top fifteen to twenty players account for a nominal share of the market. The major players in this category include raw-material suppliers, PPE divisions of major conglomerates, pure-play PPE/medical coveralls manufacturers, and wholesale and retail distributors. Within each segment again, the dynamics vary, which further reduces the bargaining power of suppliers. Manufacturers of coveralls are constantly trying to innovate by employing different types of materials. One instance is the use of SMS fabrics. These fabrics can withstand liquid while being available at competitive prices.

Order your copy of the Medical Coveralls Procurement Intelligence Report, 2023 - 2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

The major cost components in the medical coveralls category include raw materials, equipment and machinery, labor, facilities and storage, packaging, freight and transportation, and others. Other costs can include testing and inspection, marketing, insurance, tax, overhead expenses, administrative expenses, etc. Medical coveralls are critical for healthcare workers to prevent and control infection. They are designed to provide out-and-out protection from any kind of exposure. Hence the selection of the fabric or the raw material must be considered carefully. Synthetic fibers such as nylon 6,6, polyester (PET), polypropylene (PP), and polyethylene (PE) are some of the key fabrics considered to manufacture medical or PPE coveralls.

The majority of disposable coveralls are made of synthetic non-woven fabric, which is a single-use material. However, to improve the longevity and range of applications, woven cloth has witnessed some advancements in recent times. Raw materials form the largest cost component in this category. Factors such as the thickness and weight of the fabric, production or order quantity, single-layer or multi-layer structures, and the type of material chosen can further influence the total cost.

Polypropylene is also another cost-effective material that is widely used. In Q3 2023, PP prices in the North American region fluctuated a lot. The start of the third quarter witnessed a 1 - 2% drop in prices owing to a reduction in feedstock PP prices amid inflationary pressure. The continuous inflation forced consumers to reduce their consumption. As a result, demand remained low amid ample supply, which supported the decline. However, at the end of Q3 PP prices increased by 3 - 4% owing to a 5 - 6% rebound increase in feedstock PP prices and a positive demand from the automotive industry. In October 2023, PP prices in the EU region reached EUR 1,393 per MT. This was a 6% increase from September 2023.

In terms of sourcing intelligence, India, China, Malaysia, and Thailand are the most preferred countries to source medical coveralls. In 2022, China was the largest manufacturer of non-woven fabrics. The majority of medical coveralls use nonwoven fabrics. However, production in India has also ramped up steadily since the pandemic. The PPE industry in India has thrived due to low production costs, easy access to raw materials, and zero border restrictions for trade. India’s regulatory framework has significantly improved since 2021 in the PPE industry. It is common for most large end-user organizations to outsource the production of their medical coveralls.

When procuring medical coveralls, it is important to evaluate the suppliers based on product durability, quality, certifications, and protection parameters. Another key sourcing strategy is to ensure that the production process adheres to regulatory requirements and good manufacturing practices (GMP). For instance, the WHO states that the coveralls (or gowns) must meet AAMI-PB70 requirements. Other important regulatory bodies include the American National Standards Institute (ANSI) and the Association of the Advancement of Medical Instrumentation (AAMI). In the case of the raw material or fabrics used, the different standards include ISO 16604, EN 14126 Annex A, ISO 22611, ISO 22612, EN 16604 or ASTM D1238 for testing purposes, AAMI 4 level compliant coverall, etc.

Browse through Grand View Research’s collection of procurement intelligence studies:

• Medical Waste Disposal Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

• Medical Writing Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

Medical Coveralls Procurement Intelligence Report Scope

• Medical Coveralls Category Growth Rate: CAGR of 7.4% from 2023 to 2030

• Pricing Growth Outlook: 8% - 9% (Annually)

• Pricing Models: Volume-based and contract-based pricing model

• Supplier Selection Scope: Cost and pricing, past engagements, productivity, geographical presence

• Supplier Selection Criteria: Production capacity, type of material (PP, PET, PE), material thickness, sterility, compliance and safety measures, certifications, testing, operational and functional capabilities, technology used, and others

• Report Coverage: Revenue forecast, supplier ranking, supplier positioning matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Key Companies

• 3M

• Ansell

• Kimberly-Clark Worldwide, Inc.

• Cardinal Health

• O&M Halyard, Inc.

• Lakeland, Inc.

• Derekduck Industries Corp.

• Plasti Surge Industries

• Winner Medical Co., Ltd.

• DuPont de Nemours Inc.

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

• Market Intelligence involving – market size and forecast, growth factors, and driving trends

• Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

• Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

• Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions

#Medical Coveralls Procurement Intelligence#Medical Coveralls Procurement#Medical Coveralls Market#Medical Coveralls Industry

0 notes

Text

2024 Non Woven Bags Wholesale Price Secrets

2024 Non Woven Bags Wholesale Price Secrets

As the demand for eco-friendly packaging solutions continues to rise, non-woven bags have become a popular choice across various industries. Whether you’re a retailer, event planner, or promotional product distributor, understanding the wholesale pricing secrets of non-woven bags in 2024 can give you a competitive edge. In this guide, we'll unveil the key factors that influence non-woven bag prices and share strategies to help you secure the best deals.

1. Material Costs

Polypropylene Prices: Non-woven bags are primarily made from polypropylene (PP), a material whose price can fluctuate based on global market conditions. Monitoring trends in PP prices can help you time your purchases for better deals.

GSM (Grams per Square Meter): The weight and thickness of the non-woven fabric, measured in GSM, directly impact the cost. Higher GSM fabrics are more durable but also more expensive, so choose the right balance for your needs.

2. Customization and Printing

Design Complexity: Customized designs, logos, and multicolor printing can significantly increase the cost of non-woven bags. Opt for simpler designs if you’re looking to keep costs down.

Printing Methods: The type of printing (screen printing, heat transfer, digital printing) also affects the price. While digital printing offers high-quality results, screen printing is often more cost-effective for large quantities.

3. Order Quantity

Economies of Scale: The more you order, the lower the per-unit cost. Suppliers often provide discounts for bulk orders, so it’s advantageous to order in large quantities whenever possible.

MOQ (Minimum Order Quantity): Suppliers usually have a minimum order quantity that affects pricing. Understanding and negotiating MOQ can help you achieve better pricing without overstocking.

4. Bag Size and Style

Size Variations: Larger bags require more material and hence cost more. Selecting the appropriate size based on your specific requirements can help manage costs.

Bag Styles: Different styles such as D-cut, U-cut, loop handle, or drawstring bags have varying manufacturing complexities and material requirements, influencing their price.

5. Manufacturing Location

Local vs. Overseas Production: Bags produced locally may have higher labor costs but offer faster delivery and lower shipping fees. On the other hand, overseas suppliers, especially in countries like China or India, may offer lower prices but come with longer lead times and potential import duties.

Logistics and Shipping Costs: Factor in the shipping and logistics costs, especially when importing. Bulk shipping can reduce per-unit shipping costs, but be sure to calculate these expenses to get an accurate total cost.

6. Market Demand and Trends

Seasonal Demand: Non-woven bags may see price increases during peak seasons such as holidays or event-heavy periods. Planning your orders ahead of time can help you avoid these price hikes.

Eco-Friendly Trend: As consumers and businesses increasingly prioritize sustainability, demand for non-woven bags has surged. This demand can influence pricing, especially for bags made from recycled or organic materials.

7. Supplier Relationships

Long-Term Partnerships: Building strong relationships with suppliers can lead to better pricing, priority service, and more favorable payment terms. Regular communication and loyalty can go a long way in securing discounts.

Negotiation Tactics: Don’t hesitate to negotiate. Many suppliers are willing to offer discounts or added value services like free shipping or faster delivery for loyal or high-volume customers.

8. Hidden Costs to Watch For

Setup Fees: Some suppliers may charge setup fees for printing or customizing bags, which can add to the overall cost. Be sure to clarify these fees upfront.

Quality Control: Lower prices might come at the expense of quality. Always request samples and conduct quality checks before finalizing your order to avoid costly returns or dissatisfied customers.

9. Environmental Certifications

Certification Costs: If you require bags with specific eco-friendly certifications (like OEKO-TEX or GRS), be prepared to pay a premium. These certifications ensure that the bags meet certain environmental and safety standards.

Market Value: Bags with eco-friendly certifications may command higher prices in the market, allowing you to offset the initial higher costs with better margins.

10. Future Price Predictions

Economic Factors: Keep an eye on global economic conditions, which can affect material costs, manufacturing expenses, and shipping fees. Inflation, currency fluctuations, and supply chain disruptions can all influence pricing in 2024.

Technological Advancements: As technology in non-woven fabric production advances, costs may decrease over time. Staying informed about these developments can help you take advantage of lower prices as new manufacturing techniques emerge.

Conclusion

Navigating the wholesale pricing of non-woven bags in 2024 requires a keen understanding of the factors that influence costs. By considering material choices, customization options, order quantities, and supplier relationships, you can optimize your purchasing strategy to secure the best deals. Keep these secrets in mind as you plan your orders, and you'll be well-equipped to maximize your investment in non-woven bags.

0 notes

Text

Nonwoven Medical Fabrics Market Size, Analyzing Forecasted Outlook and Growth for 2024-2030

On 2024-8-1 Global Info Research released【Global Nonwoven Medical Fabrics Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030】. This report includes an overview of the development of the Nonwoven Medical Fabrics industry chain, the market status of Consumer Electronics (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), Household Appliances (Nickel-Zinc Ferrite Core, Mn-Zn Ferrite Core), and key enterprises in developed and developing market, and analysed the cutting-edge technology, patent, hot applications and market trends of Nonwoven Medical Fabrics.

Non-woven medical fabrics are a special type of textiles, usually made of non-woven materials, used in the medical field. This fabric has the characteristics of non-woven, smooth surface, good breathability, strong absorbency, softness and easy processing.

According to our (Global Info Research) latest study, the global Nonwoven Medical Fabrics market size was valued at US$ million in 2023 and is forecast to a readjusted size of USD million by 2030 with a CAGR of %during review period.

This report is a detailed and comprehensive analysis for global Nonwoven Medical Fabrics market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2024, are provided.

Market segment by Type: Absorbent Materials、Covering Materials、Securing Materials、Protective Materials、Others

Market segment by Application:Operating Room、Patient Care、Others

Major players covered: 3M、Herculite、Swift Textile、Freudenberg、ATEX Technologies、WPT Nonwovens、Kimberly-Clark、Precision Fabrics Group、Favourite Hub、Trelleborg、Warren Nonwovens、Winner Medical、Pratrivero、Changzhou Care-De Sanitary Material

Market segment by region, regional analysis covers: North America (United States, Canada and Mexico), Europe (Germany, France, United Kingdom, Russia, Italy, and Rest of Europe), Asia-Pacific (China, Japan, Korea, India, Southeast Asia, and Australia),South America (Brazil, Argentina, Colombia, and Rest of South America),Middle East & Africa (Saudi Arabia, UAE, Egypt, South Africa, and Rest of Middle East & Africa).

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Nonwoven Medical Fabrics product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Nonwoven Medical Fabrics, with price, sales, revenue and global market share of Nonwoven Medical Fabrics from 2019 to 2024.

Chapter 3, the Nonwoven Medical Fabrics competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Nonwoven Medical Fabrics breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Nonwoven Medical Fabrics market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Nonwoven Medical Fabrics.

Chapter 14 and 15, to describe Nonwoven Medical Fabrics sales channel, distributors, customers, research findings and conclusion.

Data Sources:

Via authorized organizations:customs statistics, industrial associations, relevant international societies, and academic publications etc.

Via trusted Internet sources.Such as industry news, publications on this industry, annual reports of public companies, Bloomberg Business, Wind Info, Hoovers, Factiva (Dow Jones & Company), Trading Economics, News Network, Statista, Federal Reserve Economic Data, BIS Statistics, ICIS, Companies House Documentsm, investor presentations, SEC filings of companies, etc.

Via interviews. Our interviewees includes manufacturers, related companies, industry experts, distributors, business (sales) staff, directors, CEO, marketing executives, executives from related industries/organizations, customers and raw material suppliers to obtain the latest information on the primary market;

Via data exchange. We have been consulting in this industry for 16 years and have collaborations with the players in this field. Thus, we get access to (part of) their unpublished data, by exchanging with them the data we have.

From our partners.We have information agencies as partners and they are located worldwide, thus we get (or purchase) the latest data from them.

Via our long-term tracking and gathering of data from this industry.We have a database that contains history data regarding the market.

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provides market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Europe Geotextiles Market Analysis, Growth, Forecast 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated the Europe Geotextiles Market size by value at USD 3.02 billion in 2023. During the forecast period between 2024 and 2030, BlueWeave expects the Europe Geotextiles Market size to expand at a CAGR of 8.65% reaching a value of USD 5.22 billion by 2030. The Geotextiles Market in Europe is propelled by the increasing urbanization and industrialization and rising civil engineering projects. Geotextiles are preferred for their cost-effectiveness and durability compared to alternative materials. Also, increased attention to environmental issues like soil erosion is likely to boost demand for these products in Europe. Notably, geotextiles are experiencing substantial growth as governments enforce strict regulations on their commercial use.

By volume, BlueWeave estimated the Europe Geotextiles Market size at 370.2 billion sq. meters in 2023. During the forecast period between 2024 and 2030, BlueWeave expects the Europe Geotextiles Market size by volume is projected to grow at a CAGR of 8.11% reaching the volume of 395.6 billion sq. meters by 2030. The spurring demand for geotextiles is due to their unique functional properties, such as mechanical strength, filtration capabilities, and chemical resistance, which outclass other materials.

Impact of Escalating Geopolitical Tensions on Europe Geotextiles Market

Geopolitical tensions can have a multifaceted impact on the Europe Geotextiles Market. Political instability, trade conflicts, and international sanctions disrupt supply chains, leading to delays in raw material sourcing and increased transportation costs. These disruptions can raise production costs and create uncertainty among manufacturers, affecting pricing stability and market competitiveness. Also, geopolitical tensions may lead to stricter import/export regulations, hindering the movement of geotextiles across borders. It can reduce market expansion opportunities and make it challenging for companies to meet customer demands. Overall, such tensions contribute to a volatile business environment, discouraging investment and impeding the long-term growth of the European Geotextiles Market.

Sample Request @ https://www.blueweaveconsulting.com/report/europe-geotextiles-market/report-sample

Europe Geotextiles Market

Segmental Coverage

Europe Geotextiles Market – By Product

By product, the Europe Geotextiles Market is divided into Woven, Non-woven, and Knitted segments. The non-woven segment holds the highest share in the Europe Geotextiles Market by product. Non-woven geotextiles play a crucial role in the geotextile market, offering permeable solutions made from nonwoven fabrics designed to work with soil, rock, or other geotechnical materials as part of civil engineering projects, structures, or systems. Their ability to facilitate water flow makes them ideal for road construction, drainage, and erosion control. Innovations in drainage subsystems and the extended lifespan of landfills are expected to further boost market growth. Additionally, non-woven geotextiles are increasingly in demand for transportation infrastructure projects due to their high tensile strength and cost-effectiveness, underscoring their importance in this rapidly expanding sector.

Competitive Landscape

The Europe Geotextiles Market is fragmented, with numerous players serving the market. The key players dominating the Europe Geotextiles Market include CETCO, TenCate Geosynthetics, HUESKER Synthetic GmbH, Naue GmbH & Co. KG, Bontex Geo NV, Mahina-TST, Internationale Geotextil GmbH, Tessilbrenta Srl, BontexGeo NV, and Geotex SA. The key marketing strategies adopted by the players are facility expansion, product diversification, alliances, collaborations, partnerships, and acquisitions to expand their customer reach and gain a competitive edge in the overall market.

Contact Us:

BlueWeave Consulting & Research Pvt Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

Non Woven Fabric Prices, Price Trend, Pricing, News, Analysis & Forecast

Non Woven Fabric Prices fluctuate based on a variety of factors, including raw material costs, manufacturing processes, market demand, and global economic conditions. One of the primary determinants of non-woven fabric prices is the cost of raw materials, which typically include polypropylene, polyester, and other synthetic fibers. Fluctuations in oil prices can directly impact the cost of these materials, as they are derived from petroleum products. Additionally, the manufacturing process used to create non-woven fabrics can influence prices. Methods such as spunbond, meltblown, and needle punching each have their own associated costs, with meltblown often being the most expensive due to its intricate process and specialized equipment requirements.

Market demand plays a significant role in non-woven fabric pricing dynamics. Industries such as healthcare, hygiene products, automotive, and construction are major consumers of non-woven fabrics. During periods of high demand, prices may rise due to increased competition for limited manufacturing capacity and raw materials. Conversely, during economic downturns or when demand decreases, prices may soften as manufacturers adjust their production levels to match market needs.

Get Real Time Prices of Non Woven Fabric: https://www.chemanalyst.com/Pricing-data/non-woven-fabric-1089

Global economic conditions also impact non-woven fabric prices. Factors such as currency fluctuations, trade policies, and geopolitical tensions can all influence the cost of production and distribution. For example, tariffs on imported raw materials or finished goods can drive up costs for manufacturers, leading to higher prices for non-woven fabrics. Similarly, disruptions to supply chains, such as natural disasters or political unrest in key manufacturing regions, can cause temporary shortages and price spikes.

In addition to these external factors, internal considerations within the non-woven fabric industry can also affect pricing. Competition among manufacturers, advancements in technology, and changes in consumer preferences all play a role in shaping pricing strategies. Some manufacturers may focus on cost leadership, offering lower prices to gain market share, while others may emphasize product differentiation or quality to justify higher prices.

Despite these complexities, buyers of non-woven fabrics can take certain steps to manage costs effectively. Building strong relationships with suppliers, negotiating favorable contracts, and exploring alternative materials or manufacturing methods are all strategies that can help mitigate price volatility. Additionally, staying informed about market trends, industry developments, and regulatory changes can provide valuable insights for anticipating and responding to price fluctuations.

Overall, non-woven fabric prices are influenced by a multitude of factors, both internal and external to the industry. While fluctuations are inevitable, understanding the underlying drivers of these price movements can empower buyers to make informed decisions and effectively manage their procurement processes. By staying vigilant, adaptable, and proactive, businesses can navigate the dynamic landscape of non-woven fabric pricing with confidence and agility.

Get Real Time Prices of Non Woven Fabric: https://www.chemanalyst.com/Pricing-data/non-woven-fabric-1089

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

0 notes

Text

Exploring the Flourishing Tea Market: Trends and Insights

In the realm of beverages, few have the cultural significance, versatility, and global appeal of tea. From ancient rituals to modern indulgence, tea has woven itself into the fabric of societies worldwide. As we navigate the ever-evolving landscape of consumer preferences and market dynamics, let's delve into the current state of the tea market, uncovering trends and insights that shape its trajectory.

1. Health and Wellness Drive Demand: With an increasing focus on health-conscious lifestyles, consumers are turning to tea not only for its refreshing taste but also for its perceived health benefits. Varieties like green tea, known for its antioxidant properties, and herbal infusions, celebrated for their calming effects, are witnessing surging demand. Additionally, functional teas infused with ingredients like turmeric, ginger, and matcha are gaining traction for their potential health-boosting properties.

2. Premiumization and Specialty Offerings: The tea market is experiencing a shift towards premium and specialty offerings as consumers seek unique and elevated experiences. Artisanal blends, rare teas sourced from specific regions, and organic varieties are commanding attention from discerning tea enthusiasts. This trend is fueled by the desire for authenticity, craftsmanship, and an immersive journey into the world of tea.

3. Sustainability and Ethical Sourcing: With sustainability becoming a non-negotiable criterion for conscientious consumers, tea companies are increasingly focusing on ethical sourcing practices and eco-friendly packaging. Fair trade certifications, traceable supply chains, and initiatives promoting environmental stewardship resonate with consumers who prioritize ethical consumption. Moreover, the rise of biodegradable tea bags and innovative packaging solutions reflects the industry's commitment to reducing its ecological footprint.

4. Innovation in Formats and Flavors: The tea market is witnessing a wave of innovation, with brands introducing novel formats and flavor profiles to cater to evolving consumer tastes. Ready-to-drink teas, tea concentrates, and powdered tea mixes offer convenience and versatility to on-the-go consumers. Furthermore, exotic flavor combinations, such as floral infusions, spicy chai blends, and fruity concoctions, cater to diverse palates and elevate the tea-drinking experience.

5. Digitalization and E-Commerce: The proliferation of e-commerce platforms and digital marketing channels has transformed the way tea is bought and sold. Online tea retailers, subscription services, and direct-to-consumer brands are capitalizing on digitalization to reach a wider audience and offer personalized shopping experiences. Social media platforms serve as hubs for tea enthusiasts to discover new brands, share brewing tips, and engage with tea communities globally.

6. Cultural Influences and Globalization: As global connectivity continues to blur geographical boundaries, the tea market is enriched by cross-cultural influences and globalization. Traditional tea ceremonies, such as the Japanese tea ceremony and the Chinese gongfu cha, are celebrated worldwide, fostering appreciation for tea's cultural heritage. Moreover, fusion teas that blend culinary traditions from different cultures are gaining popularity, reflecting the diverse palate preferences of today's consumers.

In conclusion, the tea market remains vibrant and dynamic, driven by evolving consumer preferences, health-conscious trends, and a growing appreciation for quality and sustainability. As tea continues to transcend borders and generations, its timeless appeal promises an exciting journey of exploration and innovation for both consumers and industry players alike.

#tea market#beverages#food and beverage industry#market research#market trends#industry analysis#innovation

0 notes

Text

Crafting a Greener Future: Innovations in Recycled Textile Production

Recycled Textile: A Growing Industry Cashing in on Sustainable Fashion

India Leading the Way in Recycling Textile Waste

With the Indian textile industry generating huge amounts of post-consumer and post-industrial waste every year, the country has become a leader in recycling these discarded materials. An estimated 60% of textile waste in India is currently being recycled either by the informal sectors or small and medium enterprises. The government has also been actively promoting recycling through various policies and schemes. Several initiatives have been launched to collect, sort and process old and used garments and fibers that would otherwise end up in landfills. Due to low labor and production costs, many large international brands are also partnering with or outsourcing recycling activities to Indian companies.

New Businesses Emerging Around Recycled Fibers Production

Recycled fibers like recycled polyester, cotton loden and modal are fast gaining popularity as eco-friendly and sustainable alternatives to virgin materials. Indian companies are setting up large-scale recycling facilities and repurposing post-consumer textiles into new fibers that can be re-spun and re-woven. These recycled fibers are finding applications in apparel, home textiles, industrial textiles and even hygiene products. New business models are emerging where rag pickers and kabadiwalas are being integrated with recycling units as suppliers of raw materials. Several startups are also focusing on innovative recycling technologies to break down fabrics into their basic fibers and filaments for reuse. This is opening up new employment opportunities and giving old textiles a second life cycle.

Garment Rental and Resale Gaining Traction

With rising awareness about fast fashion's environmental costs, sustainable consumption practices like clothing rental, resale and repair are on the rise. A number of companies are launching clothing rental and resale platforms where consumers can rent designer outfits for special occasions or sell their used clothing in exchange for store credit. Digital resale platforms are making it easy to list, buy and sell pre-owned clothes. Popular international brands are also experimenting with take-back programs where old garments are refurbished or recycled. Such initiatives encourage multiple wears and extend the lifespan of clothes, keeping more material out of landfills for longer. They also open up newer customer segments interested in affordable eco-conscious options.

Focus on Recycled Fabrics in Home and Workwear Segment

While recycled fabrics were earlier perceived as low quality, they are now gaining widespread acceptance in application segments other than just apparel. Several companies have started marketing recycled cotton, polyester and modal-based fabrics for home textiles like curtains, towels and upholstery. These are comparable to regular fabrics in aesthetics and functionality but with the added environmental benefit. Recycled fabrics are also being widely used in industrial workwear, military and PPE clothing where durability takes priority over looks. With larger fabric manufacturers integrating recycling into their portfolio, the market for such fabrics is expanding rapidly. It is helping divert tonnes of fabric waste from the wasted stream every year.

In Summary, the recycled textiles sector in India has witnessed rapid growth driven by rising awareness, technology advancements and supportive policies. With large volumes of post-consumer waste being channeled for recycling, it is evolving as a viable alternative raw material source for the textile industry. New business models are tapping opportunities spanning informal waste collectors to high-tech fiber producers. As technologies solve more complex waste sorting issues, recycled textiles appear poised to gain bigger market shares in both apparel and non-apparel applications going forward.

0 notes

Text

Biodegradable Plastics Market Size to be Worth USD 7.1 billion by 2031, with a Notable CAGR of 6.5 %

The global biodegradable plastics market is estimated to flourish at a CAGR of 6.5% from 2021 to 2031. Transparency Market Research projects that the overall sales revenue for biodegradable plastics is estimated to reach US$ 7.1 billion by the end of 2031.

An emerging driver in the biodegradable plastics market revolves around circular economy initiatives, specifically focusing on end-of-life solutions. Innovations now aim at creating robust infrastructures for the effective collection, sorting, and composting or recycling of biodegradable plastics. This shift addresses concerns about disposal methods and streamlines the life cycle of these materials, fostering a closed-loop system that minimizes waste and maximizes resource efficiency.

Grab Sample Pages Of The Report: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=9158

Market Segmentation

By Service Type

Packaging: The largest segment, driven by the food and beverage industry's demand for sustainable packaging solutions.

Agriculture: Usage in mulch films and plant pots.

Textiles: Growing use in eco-friendly clothing and accessories.

Consumer Goods: Biodegradable plastics are increasingly used in products like disposable cutlery and bags.

By Sourcing Type

Bio-based: Derived from renewable sources like corn starch and sugarcane.

Petrochemical-based: Produced from petrochemicals with additives to enhance biodegradability.

By Application

Packaging: Food packaging, beverage bottles, and shopping bags.

Agriculture: Mulch films, plant pots, and other farming tools.

Textiles: Fabrics and non-woven textiles.

Consumer Goods: Disposable items, electronics casings, and more.

By Industry Vertical

Food & Beverage: Major adopter due to the need for sustainable packaging.

Agriculture: Increasing demand for eco-friendly farming solutions.

Healthcare: Usage in medical disposables and packaging.

Retail: Rising use in shopping bags and packaging materials.

By Region

North America: Significant market share due to high consumer awareness and strict regulations.

Europe: Leading the market with stringent environmental policies and a high rate of adoption.

Asia-Pacific: Rapid growth driven by emerging economies and increased manufacturing.

Latin America: Growing adoption in packaging and agriculture sectors.

Middle East & Africa: Gradual adoption with potential for future growth.

Regional Analysis

North America

North America holds a substantial share of the biodegradable plastics market, driven by strong environmental regulations and increasing consumer preference for sustainable products. The U.S. and Canada are leading contributors in this region.

Europe

Europe is at the forefront of the biodegradable plastics market, supported by the EU’s strict regulations on plastic usage and waste management. Countries like Germany, France, and the UK are major players.

Asia-Pacific

The Asia-Pacific region is experiencing rapid market growth due to rising environmental concerns and increased manufacturing capabilities. China, Japan, and India are key contributors to this growth.

Latin America

In Latin America, the market is growing steadily, with countries like Brazil and Mexico showing increased adoption in the packaging and agriculture sectors.

Middle East & Africa

The market in the Middle East and Africa is in the nascent stage but holds significant potential for future growth as awareness and regulations regarding biodegradable plastics increase.

Market Drivers and Challenges

Market Drivers

Environmental Concerns: Increasing awareness about plastic pollution and its impact on the environment.

Government Regulations: Stricter laws and regulations on plastic usage and waste management.

Consumer Demand: Rising consumer preference for sustainable and eco-friendly products.

Technological Advancements: Innovations in production techniques and materials.

Market Challenges

High Costs: Biodegradable plastics are often more expensive than conventional plastics.

Limited Availability: Limited raw material sources and production facilities.

Performance Issues: Inconsistent performance and shorter shelf life compared to traditional plastics.

Lack of Awareness: Insufficient consumer awareness in certain regions.

Market Trends

Innovative Materials: Development of new biodegradable polymers and composites.

Expanded Applications: Increased use in various industries beyond packaging.

Corporate Sustainability Initiatives: Companies adopting biodegradable plastics to meet sustainability goals.

Circular Economy: Emphasis on recycling and sustainable resource management.

Future Outlook

The biodegradable plastics market is poised for substantial growth, with increasing investments in research and development, expansion of production capacities, and broader adoption across various sectors. Advancements in technology and materials are expected to enhance the performance and cost-effectiveness of biodegradable plastics, making them a more viable alternative to traditional plastics.

Key Market Study Points

Market Valuation: $4.3 billion in 2021, projected to reach $17.7 billion by 2031.

CAGR: Approximately 15% over the forecast period.

Primary Segments: Packaging, agriculture, textiles, and consumer goods.

Leading Regions: North America, Europe, and Asia-Pacific.

Key Drivers: Environmental concerns, government regulations, consumer demand, and technological advancements.

Main Challenges: High costs, limited availability, performance issues, and lack of awareness.

Competitive Landscape

The biodegradable plastics market is highly competitive, with several key players driving innovation and market expansion. Major companies include:

BASF SE

Nature Works LLC

Novamont S.p.A.

Corbion N.V.

Biome Bioplastics

These companies are focusing on strategic partnerships, mergers, acquisitions, and product innovations to strengthen their market position and expand their product portfolios.

Buy this Premium Research Report | Immediate Delivery Available at https://www.transparencymarketresearch.com/checkout.php?rep_id=9158<ype=S

Recent Developments

BASF SE announced a new line of biodegradable plastics designed for agricultural applications in early 2023.

Nature Works LLC expanded its production capacity with a new facility in Thailand, set to open in late 2024.

Novamont S.p.A. introduced a new biodegradable polymer with enhanced properties for food packaging in mid-2022.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Kanpur Plastipack’s W&H Filmex II castline

Kanpur Plastipack, a public limited company quoted on the stock exchange, is a provider of industrial bulk packaging solutions. It has recently enhanced its capacity with the installation of W&H’s seven-layer Filmex II castline with metallizer and a Titan slitter rewinder from Applied Materials. The Kanpur-based converter offers high-density PE sack and flexible intermediate bulk containers (FIBCs), and also woven fabric, sulzer fabric, and multi-filament yarn (MFY).

Among the company’s diversifications is the manufacturing of UV masterbaches used for the protection of outdoor films and products against UV degradation and discoloration. KPL offers food-grade UV, non-food grade UV, and masterbatches with white TIO2.

Agarwal, also the president of the Indian Flexible Intermediate Bulk Container Association (IFIBCA), met us at Interpack 2023 in Dusseldorf, Germany. He told us that the Indian FIBC industry has come a long way since the formation of IFIBCA more than two decades ago. “Twenty years ago, India was producing about 10,000 metric tons a year of FIBCs. Today the production amounts to more than 400,000 tons. India is among the biggest players in the FIBC export market and the leading exporter to the US and European countries with a strong penetration in the German market.”

Good share for Indian FIBC exporters

In a recent interaction, Agarwal said, “India holds a massive share in the US and European markets. Although the growth is consistent, it won’t be an easy task to expand further in these markets. Japan and South Korea are the two markets unexplored by the Indian FIBC manufacturers and thus expanding in these markets is the next step for us. We are working hard to expand our footprint there. Indian FIBCs are expected to replace the Chinese and Vietnamese in Japan and South Korea.”

According to him, the flexible packaging market that was surging during the pandemic has slowed down recently. “We all have seen so many geo-political issues happening globally — the Russia-Ukraine war, Gaza War, the Red Sea crisis, and to top it all, inflation is moving in a constant upward spiral. These factors have also resulted in slowing down of innovations as well,” Agarwal said.

The flexible packaging and UV masterbatch manufacturer has four production plants in India and a base of operations in Brazil. Agarwal suggests that the growth of the Indian packaging industry has huge potential and a knowledge or technology-intensive approach is the only way forward. “With the rise in Industry 4.0, technologies such as the Internet of Things, artificial intelligence, traceability, and authentication will be the differentiators,” he says.

0 notes

Text

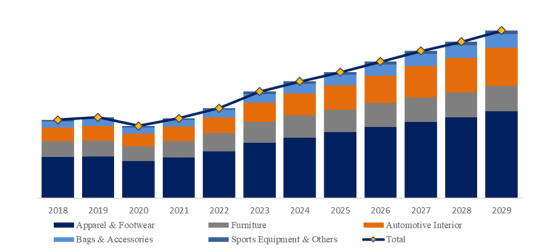

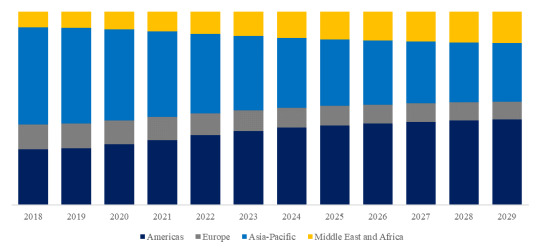

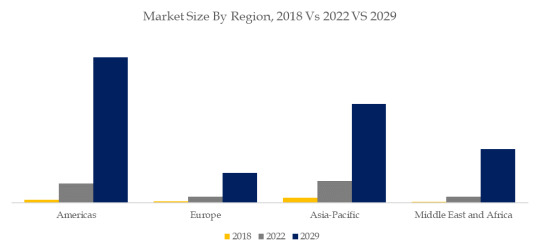

Microfiber Artificial Leather, Global Market Size Forecast, Top 15 Players Rank and Market Share

Microfiber Artificial Leather Market Summary

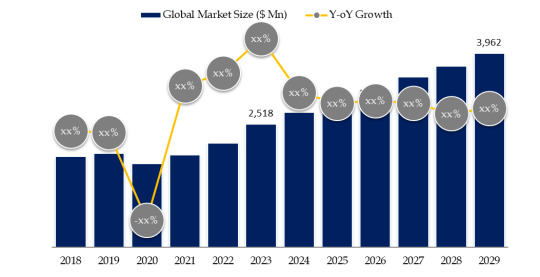

According to the new market research report "Global Microfiber Artificial Leather Market Report 2023-2029", published by QYResearch, the global Microfiber Artificial Leather market size is projected to grow from USD 2.5 Billion in 2023 to USD 3.9 Billion by 2029, at a CAGR of 7.8% during the forecast period.

Microfiber Artificial Leather is an artificial leather material that mimics real leather. It is usually made from a coating of polyurethane (PU) or polyvinyl chloride (PVC) applied to microfiber fabric. Synthetic leather with microfiber nonwoven fabric as the base fabric and PU resin as the coating is called microfiber super real leather (also called microfiber synthetic leather). The process of making other synthetic leather begins with laying down strips of fabric and coating them with polyurethane resin. But for microfiber leather, it starts with a synthetic fiber mat, using a microfiber leather non-woven fabric with a three-dimensional structure as the base fabric, which is interwoven and bonded together using polyurethane. Microfiber leather is considered the best synthetic material. It is considered the best grade of artificial leather available due to its durability, cost, and manufacturing process. Microfiber leather also has advantages that real leather does not have, such as not peeling off and aging quickly.

Figure. Microfiber Artificial Leather Product Picture

Source: Toray

Figure. Global Microfiber Artificial Leather Market Size (US$ Million), 2018-2029

Based on or includes research from QYResearch: Global Microfiber Artificial Leather Market Report 2023-2029.

Market Drivers:

Environmental Protection Needs

As environmental protection requirements become increasingly stringent, the pollution problem of leather has attracted more and more social attention. The production process of microfiber synthetic leather does not produce solid waste. Compared with the processing of natural leather, the entire post-finishing process The water consumption is very small, the amount of chemicals used is also very small, the process design is reasonable, and the BOD and COD values in the wastewater are very low, which can meet the requirements of clean production and reduce the difficulty of sewage treatment. From an industrial sense, it is not only suitable for modern scale production, but also protects the ecology, reduces environmental pollution, and makes full use of non-natural resources. Due to the limited resources of natural leather, along with the advancement of science and technology , many physical properties of high-grade synthetic leather have greatly exceeded those of natural leather, and its external performance has the characteristics of natural leather.

Consumption-Driven

With the continuous development of the economy and the improvement of residents' income levels, market consumption capacity continues to increase, and people's demand for leather products is also increasing.

Downstream Demand Boom

Microfiber leather is mostly used in clothing, shoes, household items, bags, automobile interiors and other fields. Most of the downstream industries belong to the category of social consumer goods. The continuous increase in the demand for social consumer goods is an important driving force for the development of the leather industry. With the continuous development of the national economy and the high growth of consumer demand, the market continues to expand, and there is no weakness or significant shrinkage.

Restraint:

High Product Prices

Superfiber synthetic leather is a technological product, and its production is concentrated in powerful domestic and foreign manufacturing companies. It has a certain monopoly, resulting in high product prices.

High Technical Requirements

The production of microfiber leather involves many professional fields and requires high professional skills and experience. Failure to meet the requirements in a certain process will affect the quality of the final product.

Large Capital Investment

Hundreds of millions to billions of capital need to be invested, otherwise economies of scale cannot be achieved and production costs cannot be reduced. Enterprises in the microfiber leather industry generally need to reach a production scale of at least 3 million square meters in order to have relatively sufficient market competitiveness, which has also led to the elimination of many small-scale production capacities in recent years.

High Industry Barriers

Products newly entering the enterprise need to be inspected and quality certified by customers, which can take several years. After entering the market, they also need to continuously launch differentiated new products suitable for various fields, and product materials, patterns, processes, etc. need to be continuously adjusted.

Challenge:

Technology Monopoly

The world's high-end microfiber leather is mainly monopolized by Japanese and Korean companies such as Japan's Toray, Teijin, Kuraray, and South Korea's Cologne.

Unbalanced Product Structure

In the entire industry, traditional ingredients are still heavy, high-end products are still few, and the product structure lacks competitiveness.

Products Follow Changes In Downstream Industries

Most companies implement a production model based on sales and organize production according to customer order needs. The production process is generally divided into two parts: first, standard semi-finished products are produced, and then the semi-finished products are processed according to the customer's specific requirements in terms of specifications, colors, patterns, etc. to manufacture finished products.

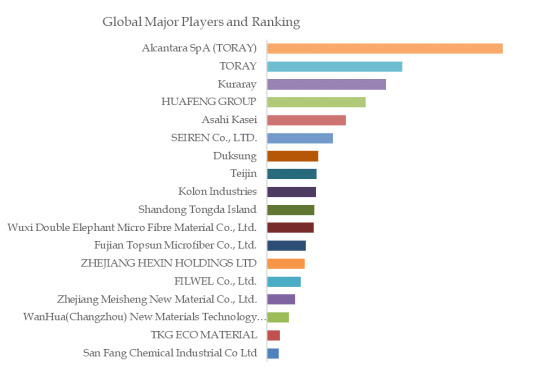

Figure. Microfiber Artificial Leather, Global Market Size, The Top Five Players Hold 42.2% of Overall Market

Based on or includes research from QYResearch: Global Microfiber Artificial Leather Market Report 2023-2029.

This report profiles key players of Microfiber Artificial Leather such as Alcantara SpA, TORAY, Kuraray, HUAFENG GROUP, Asahi Kasei, etc.