#Global Textile Coatings Market

Text

The Business Research Company offers textile coatings market research report 2023 with industry size, share, segments and market growth

#textile coatings market size#textile coatings market research#textile coatings market forecast#textile coatings market outlook#textile coatings market insights#textile coatings market trends#global textile coatings market#textile coatings market growth#textile coatings market analysis#textile coatings market share#textile coatings market report#textile coatings market segments

0 notes

Text

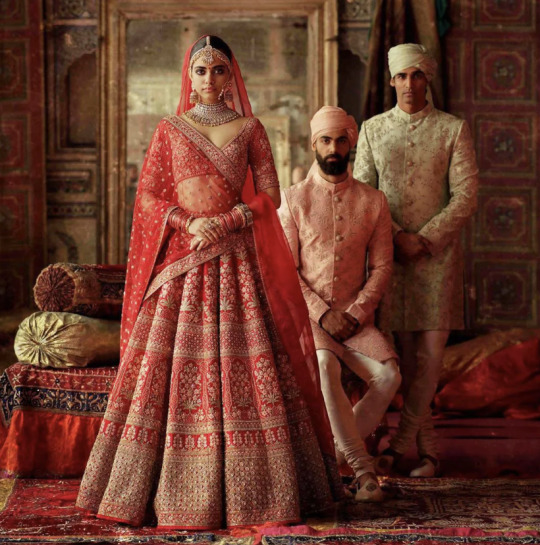

East Meets West: Bridging Fashion from Burberry to Sabyasachi and Papa Don't Preach by Shubhika

This case about Burberry made me think of Indian fashion and the axis of traditionality/heritage to modernity. It’s fascinating to see how global brands like Burberry parallel or diverge from Indian counterparts like Sabyasachi and Papa Don't Preach by Shubhika, especially in their approach to blending heritage with modern trends.

Burberry's Timeless Elegance

Burberry, with its quintessentially British roots, stands as a pillar of luxury and tradition. Famous for its classic trench coats and the iconic check pattern, the brand merges historical elements with modern needs seamlessly. Under leaderships like Angela Ahrendts', Burberry expanded its reach while keeping a tight grip on its classic British heritage, ensuring that each piece tells a story of timeless elegance.

Sabyasachi's Regal Craftsmanship

Crossing over to India, Sabyasachi is a brand that echoes similar sentiments but in a decidedly Indian context. Sabyasachi Mukherjee, the founder, emphasizes the grandeur of India’s artisan traditions. His designs are a homage to the past—lush fabrics, intricate embroideries, and vibrant palettes that speak volumes of India’s rich textile legacy. Much like Burberry, Sabyasachi caters to an elite clientele, offering pieces that combine the old-world charm with contemporary silhouettes.

Papa Don't Preach by Shubhika's Bold Modernity

On the other end of the spectrum is Papa Don't Preach by Shubhika, a label that challenges traditional norms and embraces a more rebellious, modern aesthetic. Shubhika Sharma’s creations are colorful, edgy, and experimental, incorporating unconventional materials and bold designs that stand out in a crowd. This brand caters to a younger, more daring demographic, looking to make a statement rather than adhere to classic styles.

Comparative Analysis: Tradition and Innovation

What’s interesting is how each of these brands, though operating in different cultural and market contexts, manages to find a balance between tradition and innovation. Burberry, maintaining its luxury heritage, adapts to the modern market with digital integration and global expansion strategies. Sabyasachi, while deeply rooted in Indian craftsmanship, continues to evolve, embracing new techniques and styles to keep his designs fresh and relevant.

Papa Don't Preach by Shubhika represents a leap towards modernity, focusing less on tradition and more on creating new trends and expressions in fashion. This brand is much like the new voices in the fashion industry worldwide, which prioritize breaking norms and setting new boundaries.

Conclusion: A Tapestry of Styles

The comparison between Burberry, Sabyasachi, and Papa Don't Preach by Shubhika illustrates a global tapestry of styles where every thread counts. Each brand, whether British or Indian, tells a story through its fashion, influenced by its heritage but driven by the modern world's demands. As global consumers become more interconnected, the influence of traditional and modern design elements blends even more, creating exciting, dynamic fashion landscapes for us to explore.

These brands show that whether in the lush countryside of England or the bustling streets of Mumbai, fashion remains a universal language, spoken fluently with both classic and contemporary dialects.

2 notes

·

View notes

Text

Melamine Market is Expected to Grow at a CAGR of 3.87% during the forecast period until 2032

The melamine market has witnessed remarkable growth and diversification in recent years, propelled by a myriad of factors shaping the global landscape. Melamine, a nitrogen-rich organic compound, finds extensive applications across various industries, including construction, automotive, textiles, packaging, and food service. Its unique properties, such as high flame resistance, thermal stability, durability, and chemical inertness, have made melamine a versatile and indispensable material in numerous manufacturing processes and end-use applications.

One of the primary drivers of the melamine market is the increasing demand from the construction industry. Melamine-based products, such as melamine formaldehyde resins and melamine foam insulation, are widely used in construction applications such as laminates, decorative panels, flooring, countertops, and insulation materials. With rapid urbanization, infrastructure development, and construction activities on the rise globally, the demand for melamine-based construction materials is expected to surge.

Read Full Report: https://www.chemanalyst.com/industry-report/melamine-market-812

Moreover, the automotive sector represents another significant market for melamine, driven by the increasing demand for lightweight, durable, and aesthetically appealing materials. Melamine-based components, such as automotive interior trim, dashboard panels, door panels, and decorative parts, offer excellent properties such as scratch resistance, color stability, and surface finish, thereby enhancing the overall aesthetics and functionality of vehicles. As automotive manufacturers focus on improving fuel efficiency, reducing emissions, and enhancing passenger comfort and safety, the demand for melamine-based automotive materials is projected to grow substantially.

Furthermore, the textiles industry presents lucrative opportunities for the melamine market, particularly in the manufacturing of melamine-formaldehyde resins for textile finishing and coating applications. Melamine resins impart crease resistance, wrinkle resistance, and color fastness to textiles, thereby enhancing their durability, appearance, and performance. With the growing demand for high-quality textiles, home furnishings, and apparel, the demand for melamine-based textile additives is expected to increase.

Additionally, the packaging industry represents a significant market for melamine, driven by the rising demand for lightweight, durable, and eco-friendly packaging materials. Melamine-based products, such as melamine-formaldehyde resins and melamine foam packaging, offer excellent properties such as thermal insulation, moisture resistance, and shock absorption, making them ideal for packaging applications such as food packaging, electronics packaging, and industrial packaging. As consumers increasingly prioritize sustainability, recyclability, and environmental friendliness, the demand for melamine-based packaging solutions is expected to grow.

Despite the promising outlook, the melamine market faces challenges and constraints, including fluctuating raw material prices, regulatory compliance issues, and environmental concerns related to formaldehyde emissions. However, industry stakeholders are actively addressing these challenges through initiatives focused on product innovation, sustainability, and regulatory compliance. Moreover, strategic partnerships, mergers, and acquisitions are driving consolidation and market expansion in the melamine industry.

In conclusion, the melamine market is poised for continued growth and innovation, driven by its versatile applications, inherent properties, and compatibility with evolving market trends. By leveraging its strengths in construction, automotive, textiles, packaging, and other sectors, the melamine market can navigate towards a more sustainable and prosperous future, ensuring its relevance and competitiveness in the global marketplace.

About us:

ChemAnalyst is an online platform offering a comprehensive range of market analysis and pricing services, as well as up-to-date news and deals from the chemical and petrochemical industry, globally.

Being awarded ‘The Product Innovator of the Year, 2023’, ChemAnalyst is an indispensable tool for navigating the risks of today's ever-changing chemicals market.

The platform helps companies strategize and formulate their chemical procurement by tracking real time prices of more than 400 chemicals in more than 25 countries.

ChemAnalyst also provides market analysis for more than 1000 chemical commodities covering multifaceted parameters including Production, Demand, Supply, Plant Operating Rate, Imports, Exports, and much more. The users will not only be able to analyse historical data but will also get to inspect detailed forecasts for upto 10 years. With access to local field teams, the company provides high-quality, reliable market analysis data for more than 40 countries.

Contact us:

420 Lexington Avenue, Suite 300

New York, NY

United States, 10170

Email-id: [email protected]

Mobile no: +1-3322586602

#Melamine#Melaminemarket#Melaminemarketsize#Melaminemarkettrends#Melaminemarketgrowth#Melaminemarketshare#Melaminedemand

2 notes

·

View notes

Text

https://www.maximizemarketresearch.com/market-report/global-lignosulfonates-market/35743/

Lignosulfonate is used as an intermediate in the synthesis of numerous products. Its unique chemistry has directed to its application in diverse sectors like coatings, textile lubricants, polishes, detergents, pesticides, and personal care products.

0 notes

Text

Adipic Acid Prices | Pricing | Trend | News | Database | Chart | Forecast

Adipic Acid is an essential industrial chemical primarily used in the production of nylon 6,6, as well as in various resins, fibers, coatings, and plasticizers. It is also utilized in the food and pharmaceutical industries as a gelling agent and acidity regulator. The pricing of adipic acid has been a point of interest for various industries and businesses due to its substantial demand across multiple sectors. Over the years, adipic acid prices have been influenced by several factors, including raw material costs, global market dynamics, production levels, environmental regulations, and regional supply-demand imbalances.

A key driver in the pricing of adipic acid is the cost of raw materials. Adipic acid is produced mainly from cyclohexane, a chemical derived from crude oil. The volatility of crude oil prices often directly impacts the price of adipic acid. For instance, when crude oil prices soar, the cost of producing cyclohexane increases, driving up adipic acid prices. Conversely, when oil prices drop, adipic acid tends to become more affordable, barring any other external factors. This close correlation with oil prices makes the adipic acid market sensitive to fluctuations in the global energy market, including geopolitical tensions, supply chain disruptions, and economic shifts that affect oil prices.

Get Real Time Prices for Adipic Acid: https://www.chemanalyst.com/Pricing-data/adipic-acid-1106

In addition to raw material costs, the production capacity and operational efficiencies of manufacturers significantly influence adipic acid prices. Major producers are concentrated in regions such as North America, Europe, and Asia-Pacific, with China being one of the largest players in the market. The availability of production facilities, technological advancements in manufacturing processes, and innovations aimed at improving yield and efficiency all play crucial roles in shaping supply levels and, consequently, the pricing of adipic acid. Periods of reduced production capacity, whether due to planned maintenance shutdowns or unplanned operational challenges, can lead to reduced supply, which often results in price spikes. On the other hand, when production is robust and supply levels meet or exceed market demand, prices tend to stabilize or even decrease.

Environmental regulations are another critical factor that impacts adipic acid prices. The production of adipic acid involves the release of nitrous oxide, a potent greenhouse gas. As governments worldwide implement stricter environmental regulations and carbon emission policies, adipic acid producers are being forced to invest in cleaner technologies and adopt more sustainable production methods. These investments in green technology often lead to increased production costs, which are passed on to consumers in the form of higher adipic acid prices. In particular, regions with more stringent environmental policies, such as Europe, may experience higher adipic acid prices compared to regions with more lenient regulations. This regulatory pressure is expected to increase in the future as sustainability becomes a growing concern for industries across the globe.

Demand trends across various end-user industries also have a significant effect on adipic acid prices. The nylon 6,6 industry is the largest consumer of adipic acid, and any shifts in demand for nylon products can cause price fluctuations. For instance, the automotive and textile industries, which are major consumers of nylon, directly impact adipic acid demand. A downturn in these industries can lead to reduced demand for adipic acid, resulting in lower prices. Conversely, a booming automotive or textile market can drive up demand and subsequently increase prices. Other industries, such as food and pharmaceuticals, while smaller in terms of volume, also contribute to demand fluctuations, particularly in niche markets where adipic acid plays a specialized role.

The global supply chain dynamics also contribute to adipic acid price movements. Trade restrictions, tariffs, and transportation costs can all affect the global flow of adipic acid, creating regional price disparities. For example, shipping constraints or trade tariffs between major producing regions, such as China and the United States, can lead to higher adipic acid prices in regions dependent on imports. Similarly, logistical challenges such as port congestion or limited transportation capacity can result in delayed deliveries and temporary supply shortages, causing prices to surge in affected areas.

Seasonal variations also play a part in adipic acid pricing, though to a lesser extent. In some industries, demand for nylon or other adipic acid derivatives may be higher at specific times of the year, leading to short-term price fluctuations. For example, increased automotive production during certain seasons can lead to higher demand for nylon, which in turn drives up adipic acid prices. Likewise, maintenance cycles for production plants are often scheduled during periods of lower demand, but unexpected shutdowns during peak seasons can create supply shortages and lead to sudden price hikes.

Finally, the role of global economic conditions cannot be overlooked when analyzing adipic acid prices. Economic downturns, recessions, and fluctuations in currency exchange rates can all affect market dynamics. During periods of economic uncertainty, industries may scale back production, leading to reduced demand for adipic acid and subsequent price drops. However, during periods of economic recovery or growth, increased industrial activity can drive up demand and result in higher prices. Exchange rate fluctuations, particularly in major producing and consuming regions, can also affect adipic acid pricing, as a stronger currency may make imports more expensive, contributing to regional price increases.

In conclusion, adipic acid prices are influenced by a complex interplay of factors ranging from raw material costs and production capacity to environmental regulations, demand trends, and global supply chain dynamics. The price of adipic acid is highly susceptible to external factors such as crude oil price fluctuations, regulatory changes, and shifts in global demand. As industries continue to evolve and adopt more sustainable practices, adipic acid prices are likely to face further fluctuations, making it essential for businesses to stay informed about market trends and developments in order to navigate the challenges of this volatile market.

Get Real Time Prices for Adipic Acid: https://www.chemanalyst.com/Pricing-data/adipic-acid-1106

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

#Adipic Acid#Adipic Acid Price#Adipic Acid Prices#Adipic Acid Pricing#Adipic Acid News#Adipic Acid Price Monitor#Adipic Acid Database

0 notes

Text

Ashwini Industries: A Trusted Leader in Specialty Chemicals and Dyes

Ashwini Industries has carved a niche for itself in the global market, offering high-quality chemical solutions and dyes across various industries. As renowned Acid Black 2 Exporters, Antifoaming Agent AI-010 Manufacturers, Solvent Black 5 Manufacturers, Vat Paste Manufacturers, and Fluorescent Pigment Paste Manufacturers, We are committed to delivering innovative products that meet the highest industry standards.

Acid Black 2 Exporters

Ashwini Industries is a leading name among Acid Black 2 Exporters, providing premium-grade dyes for textiles, leather, and ink applications. Known for its deep black shade and excellent solubility, Acid Black 2 is widely used across various sectors. We ensures that the product is manufactured under strict quality control, offering consistency and reliability to its clients globally.

Antifoaming Agent AI-010 Manufacturers

Foam control is a critical factor in many industrial processes, and We excels as Antifoaming Agent AI-010 Manufacturers. Their AI-010 formulation, available in silicone and non-silicone variants, is designed to efficiently reduce and prevent foam in industries such as water treatment, textiles, and food processing. The environmentally friendly and non-toxic composition ensures that the product meets industry requirements while maintaining operational efficiency.

Solvent Black 5 Manufacturers

As leading Solvent Black 5 Manufacturers, We offers a versatile dye widely used in inks, coatings, and plastics. Solvent Black 5 is prized for its excellent solubility in organic solvents, making it a top choice for industries such as printing, leather, and synthetic materials. Ashwini's production processes ensure high-quality color consistency, meeting the specific demands of various industrial applications.

Vat Paste Manufacturers

Specializing as Vat Paste Manufacturers, Ashwini Industries produces concentrated dye pastes used in textile printing and dyeing. Known for their vibrant, long-lasting colors, vat pastes are commonly applied to natural fibers like cotton and wool. The paste undergoes a reduction process, allowing for deep, rich shades that offer excellent wash and light fastness, making it a popular choice in the textile industry.

Fluorescent Pigment Paste Manufacturers

Innovation in color technology is one of Ashwini’s strengths, especially as Fluorescent Pigment Paste Manufacturers. These pigment pastes are used to produce bright, eye-catching colors in industries such as printing, paints, and coatings. Ashwini’s fluorescent pigment pastes provide superior color strength and durability, making them an ideal choice for applications that demand vivid, high-visibility hues.

Why Choose Ashwini Industries?

With a focus on quality, sustainability, and innovation, We continues to lead the way in the specialty chemicals and dyes sector. Their expertise across a wide range of products ensures that industries worldwide can rely on them for high-performance solutions tailored to their specific needs.

Hence, whether you're looking for Acid Black 2, Antifoaming Agents, Solvent Black 5, Vat Pastes, or Fluorescent Pigment Pastes, We are your trusted partner for top-quality, reliable chemical solutions. Their commitment to excellence guarantees that your business benefits from the best products in the industry.

#Acid Black 2 Exporters#Antifoaming Agent AI-010 Manufacturers#Solvent Black 5 Manufacturers#Vat Paste Manufacturers#Fluorescent Pigment Paste Manufacturers

1 note

·

View note

Text

Biopolymers Market - Forecast(2024 - 2030)

Biopolymers Market Overview

The Biopolymers Market size is projected to reach US$27.5 billion by 2030, after growing at a CAGR of 11.5% over the forecast period 2024-2030. The various benefits associated with the biopolymers such as polyesters, polylactic acid, polyhydroxy butyrate, polybutylene succinate and more include biocompatibility, biodegradability, renewability and more. These benefits make biopolymers a sustainable replacement for petroleum-derived materials. The bolstering food & beverage industry, including poultry products, dried food and more is the primary factor driving the biopolymers market growth. For instance, the FAO’s food outlook published in June 2023 expects global poultry meat production to reach more than 142 million mt, a 1.3% increase compared to 2022’s value. However, The COVID-19 pandemic resulted in restrictions affecting various aspects of the supply chain, including logistics, which had a detrimental impact on production activities in the biopolymers industry. Following the pandemic, government measures aimed at rejuvenating production activities played a crucial role in fueling the recovery and growth of the biopolymers industry. Moreover, the growth of the medical and healthcare industry is fueling the demand for biopolymers. As a result, the biopolymers market size will grow throughout the forecast period.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞

Report Coverage

The "Biopolymers Market Report – Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Biopolymers Market.

By Type: Bio-based Polyesters [Polylactic Acid (PLA), Polyhydroxybutyrate (PHB), Polybutylene Succinate (PBS), Polybutylene Succinate Adipate (PBSA), Polytrimethylene Terephthalate (PTT) and Others], Bio-based Polyolefins, Bio-based Polyamides (Bio-PA) (Homopolyamides, Bio-PA 6, Bio-PA 11, Copolyamides and Others), Polyurethanes, Polysaccharide Polymers (Cellulose-based Polymers and Starch-based Polymers) and Others.

By Molding Process: Extrusion, Injection, Melt compounding and Others.

By Application: Packaging (Rigid Packaging and Flexible Packaging), Fibers, Paper & Cardboard Coatings, Agricultural Seed Coatings, Automotive Interiors & Exteriors, Medical Implants, Circuit Boards, Insulators, Laminates and Others.

By End-use Industry: Food & Beverage (Fresh Food, Bakery, Frozen Food, Dried Food, Poultry Products, Dairy Products, Confectionery, Alcoholic Beverages, Non-alcoholic Beverages and Others), Medical & Healthcare (Pharmaceuticals, Medical Devices and Others), Agriculture, Consumer Electronics (Computers, Smartphones, Refrigerators and Others), Automotive [Passenger Vehicles (PV), Light Commercial Vehicles (LCV) and Heavy Commercial Vehicles (HCV)], Textile, Aerospace (Commercial, Military and Others), Building & Construction (Residential, Commercial, Industrial and Others) and Others

By Geography: North America (the USA, Canada and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile and Rest of South America), Rest of the World [Middle East (Saudi Arabia, UAE, Israel and Rest of Middle East) and Africa (South Africa, Nigeria and Rest of Africa)]

Key Takeaways

• Europe dominated the Biopolymers Market, owing to the growth of the fresh food industry in the region. For instance, according to the Federal Statistical Office of Germany,roughly 6,100 agricultural holdings in Germany harvested a total 3.8 million tonnes of vegetables in 2022.

• The government initiatives for green initiatives are fuelling the demand for Biopolymers such as polyesters, polyethylene and more are driving the market growth.

• Moreover, the increasing adoption of Biopolymers in packaging applications is also accelerating market growth.

• However, the high cost of the Biopolymers is expected to create a retrain for the market growth during the projected forecast period.

Biopolymers Market Segment Analysis – by Application

The packaging segment held the largest Biopolymers Market share in 2023 and is estimated to grow at a CAGR of 10.4% over the forecast period 2024-2030. Biopolymers such as polyesters, polylactic acid, polyhydroxybutyrate and more are frequently deployed in packaging because they enhance the shelf-life of the product and also it reduces the overall carbon footprint related to food packaging. The films composed of biopolymers such as polysaccharides and protein-composed increase mechanical and optical properties. As a result, biopolymers packaging is employed across various end-use industries, including food & beverages, medical & healthcare and more. Thus, owing to the above-mentioned benefits, the adoption of biopolymers is surging in packaging applications, which is accelerating market growth.

Biopolymers Market Segment Analysis – by End-use Industry

The food & beverage segment held a significant Biopolymers Market share in 2023. The key properties of biopolymers are high strength, lightweight and heat resistance. As a result, biopolymers are frequently used in the food and beverage industry. Moreover, due to their superior quality, functionality, affordability and composability, they are an ideal replacement for single-use plastic food & beverage packaging. The surging development of food & beverage facilities, governmental initiatives and others are the crucial variables propelling the food & beverage industry's growth. For instance, according to Invest India, the food processing sector in India is one of the world’s largest, with output anticipated to reach US$535 billion by 2025-2026. Hence, the growth of the food & beverage industry is expected to fuel the demand for biopolymers. As a result, the market growth will accelerate during the upcoming years.

Biopolymers Market Segment Analysis – by Geography

Europe is the dominating region as it held the largest Biopolymers Market share in 2023. The economic growth of Europe is driven by the growth of the various industries, including food and beverage, medical & healthcare and other similar industries. The food and beverages industry growth are vital for food security in the European region. For instance, according to Food Drink Europe, the food and drink industry in Europe produced a 107.7 production index in the fourth quarter of 2022 and a 109.2 production index in the first quarter of 2023, an increase of 1.4 percent. Also, according to the European Union, in 2022, the production of fruits in the European Union countries was about 35.9 million metric tons and out of this, apples and pears production were the highest at 14.7 million metric tons, which was 40.9% of the total fruit production. Therefore, the booming food & beverage industry in Europe is boosting the demand for biopolymers. This, in turn, is proliferating the biopolymers market size growth.

0 notes

Text

Growth Projections and Trends in the Hybrid Textile Industry: 2024-2034

Hybrid textiles are advanced materials that blend different fibers or fabric types to achieve superior characteristics. These textiles are known for their enhanced strength, durability, flexibility, and resistance to environmental factors. Industries such as automotive, aerospace, defense, sportswear, and medical are adopting hybrid textiles to meet their high-performance material needs. The market for hybrid textiles is projected to witness substantial growth due to increasing demand for lightweight and strong materials.

The hybrid textile market is expected to grow significantly from 2024 to 2034. This growth is driven by advancements in fiber technologies and rising demand for multifunctional textiles across various industries. The global Hybrid Textile industry, valued at US$ 316.6 million in 2023, is projected to grow at a CAGR of 8.0%, reaching US$ 738.1 million by 2034.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/hybrid-textile-market.html

Market Segmentation

The hybrid textile market can be segmented as follows:

By Service Type:

Fabric Development

Weaving

Knitting

Coating and Laminating

By Sourcing Type:

Natural Fiber Blends (cotton, wool, silk)

Synthetic Fiber Blends (polyester, nylon, spandex)

Composite Fiber Blends (carbon, glass, aramid)

By Application:

Automotive

Aerospace

Medical

Sportswear and Protective Clothing

Defense

By Industry Vertical:

Transportation

Healthcare

Industrial

Consumer Goods

Defense and Aerospace

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Analysis

North America: Dominates the market with its mature automotive and aerospace industries driving demand for hybrid textiles. The U.S. leads in research and development of high-performance fibers.

Europe: Focuses on sustainability and technological advancements in automotive and medical sectors, which are key factors for growth. Countries like Germany and France are pioneers in adopting hybrid textile solutions.

Asia-Pacific: Expected to witness the highest growth, driven by expanding automotive, construction, and sports sectors in countries such as China, India, and Japan.

Latin America and Middle East & Africa: These regions are still developing but have significant potential, especially with the growing industrial sectors in Brazil, South Africa, and GCC nations.

Market Drivers and Challenges

Drivers:

Growing demand for lightweight and durable materials in automotive and aerospace industries.

Increasing use of hybrid textiles in sportswear and medical applications due to their performance-enhancing characteristics.

Advancements in fiber technology, leading to the production of cost-effective and high-performance textiles.

Challenges:

High production costs associated with advanced hybrid textiles.

Complex manufacturing processes, requiring skilled labor and specialized machinery.

Limited awareness in some developing regions regarding the benefits of hybrid textiles.

Market Trends

Growing focus on sustainable materials and eco-friendly production processes in hybrid textiles, with an emphasis on using recycled fibers.

Increased demand for smart textiles that integrate sensors and electronic components for applications in sports, healthcare, and military sectors.

Development of bio-based hybrid textiles, combining natural and synthetic fibers to reduce environmental impact without compromising performance.

Future Outlook

The hybrid textile market is poised for sustained growth over the next decade. Innovations in fiber blending technologies and increasing applications in diverse sectors will fuel demand. By 2034, hybrid textiles are expected to play a crucial role in industries focused on reducing weight, improving strength, and enhancing sustainability.

Key Market Study Points

Assessment of growing demand in automotive and aerospace sectors.

Analysis of advancements in smart textiles and bio-based materials.

Regional growth trends, particularly in Asia-Pacific and Europe.

Future potential of sustainable production techniques and their impact on market dynamics.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=86369<ype=S

Competitive Landscape

The hybrid textile market features a mix of global and regional players, with companies focusing on product innovation, partnerships, and expanding manufacturing capacities. Key players in the market include:

Teijin Limited

Toray Industries Inc.

Koninklijke Ten Cate BV

Gurit Holding AG

Hexcel Corporation

These companies are investing in research and development to create advanced hybrid textile products and maintain a competitive edge.

Recent Developments

Several market players are exploring sustainable fibers and recyclable materials, aiming to align with environmental regulations.

The rise of customized textiles for specific industry applications has led to collaborations between textile manufacturers and industry players, particularly in aerospace and defense sectors.

Ongoing advancements in digital fabric development technologies are expected to streamline production and reduce costs.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Nanocellulose 2023 Industry – Challenges, Drivers, Outlook, Segmentation - Analysis to 2030

Nanocellulose Industry Overview

The global nanocellulose market size was valued at USD 351.5 million in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 20.1% from 2023 to 2030.

The growth is attributable to the rise in demand for various applications and the shifting trend for using bio-based goods are the factors responsible to drive demand for product. Due to its various qualities, such as increased paper machine efficiency, better filler content, lighter base mass, and higher freeness, nanocellulose is suitable for the producing a wide range of products. The paper industry uses nanocellulose as a prominent sustainable nanomaterial additive owing to its high strength, strong oxygen barrier performance, low density, mechanical qualities, and biocompatibility among the available bio-based resources. Additionally, the construction of materials, aqueous coating, and others are some of the major uses of nanocellulose composite materials.

Gather more insights about the market drivers, restrains and growth of the Nanocellulose Market

The U.S. is the largest market for nanocellulose in North America contributing a considerable amount to global revenue. People in the U.S. are concerned about their health, which has greatly aided the use of MFC (Micro fibrillated Cellulose) and CNF (Cellulose nanofibers) in the production of functional food products thus increasing the demand for nanocellulose in the country.

The food & beverage, and paper & pulp industry are majorly driving product growth in the country. Demand in the country is majorly driven by the increasing awareness and insistence on highly advanced sustainable products along with paper-based packaging in the food & beverage industries.

The pulp & paper business heavily utilizes nanocellulose as an ingredient to create light and white paper that further accelerates the market growth. Owing to its benign qualities it is used in healthcare applications such as biomedicines and personal hygiene products. Additionally, owing to its superior adsorption abilities, Nanocellulose is a suitable constituent for sanitary napkins and wound dressings. The market has been further stimulated by expanding product research activity.

Nanocellulose Market Segmentation

Grand View Research has segmented the global nanocellulose market report based on the type, application, and region:

Type Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

CNF (NFC, MFC)

Bacterial Cellulose

CNC

Application Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

Pulp & Paperboard

Composites

Pharmaceuticals & Biomedical

Electronics

Food & Beverages

Others (Textile, Paints, cosmetics, Oil & Gas, Cement)

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

Netherlands

France

Finland

Norway

Sweden

Switzerland

Spain

Asia Pacific

China

India

Japan

South Korea

Australia

Thailand

Malaysia

Singapore

Central & South America

Brazil

Colombia

Chile

Middle East & Africa

Saudi Arabia

South Africa

Israel

Iran

Browse through Grand View Research's Renewable Chemicals Industry Research Reports.

The global chondroitin sulfate market size was valued at USD 1.29 billion in 2023 and is projected to grow at a CAGR of 3.6% from 2024 to 2030.

The global pine-derived chemicals market size was estimated at USD 5.82 billion in 2023 and is projected to grow at a CAGR of 4.4% from 2024 to 2030.

Key Companies & Market Share Insights

The market is consolidated owing to the existence of a few major players in the market including Cellu Force, Fiber Lean, Kruger INC., and others. Manufacturers operating in the market engage in strategic mergers & acquisitions, geographical expansion, product developments, and innovation in order to strengthen their positions, increase profitability, and simultaneously generate innovations and advancements.

When compared to other nanotechnology high-performance materials, nanocellulose offers a lower cost and the potential to replace many products made from petrochemicals. It has exceptional qualities like biodegradability, transparency, flexibility, high mechanical strength, and barrier characteristics, among others. Growing interest in health issues and the food & beverage industries will both have a significant impact on the market share in the years to come.

Consequently, the focus on manufacture of the product has increased owing to increasing awareness about health and environmental concerns arising from harmful chemical products. The global market has witnessed several new product developments, mergers & acquisitions and joint ventures due to several industrial challenges. Some prominent players in the global nanocellulose market include:

Cellu Force

Fiber Lean

NIPPON PAPER INDUSTRIES CO., LTD.

Kruger INC

Borregaard AS

CelluComp

Melodea Ltd

Blue Goose Refineries

GranBio Technologies

Stora Enso Biomaterials

Order a free sample PDF of the Nanocellulose Market Intelligence Study, published by Grand View Research.

0 notes

Text

Ethyleneamines Market Analysis: Key Drivers and Regional Trends

The ethyleneamines market has gained significant attention over the past few years. With projections pointing towards steady growth from USD 2.2 billion in 2023 to approximately USD 2.9 billion by 2030, it's clear that ethyleneamines are set to play an even larger role in multiple industries. This article will delve into the market trends, growth drivers, key applications, and much more.

What Are Ethyleneamines?

Ethyleneamines are a group of compounds made primarily from ethylene dichloride and ammonia. They are essential components in various chemical reactions and have a broad range of applications, making them highly valuable in industries like agriculture, personal care, and pharmaceuticals.

Key Drivers Behind the Ethyleneamines Market Growth

The ethyleneamines market is experiencing consistent growth due to several key factors:

1. Increasing Demand in the Agriculture Industry

Ethyleneamines are vital in the production of agrochemicals like pesticides and fertilizers. As the global population continues to grow, the need for enhanced agricultural output is driving demand for these chemicals.

2. Expanding Use in Pharmaceuticals

Ethyleneamines are crucial in the production of several pharmaceutical compounds, including antibiotics and cancer treatments. The global expansion of the pharmaceutical industry is fueling their demand.

3. Rising Demand for Personal Care Products

Products like shampoos, lotions, and creams often contain ethyleneamines, which enhance their properties. The growing consumer awareness and demand for personal care items contribute to the market's growth.

4. Growth in Water Treatment Applications

Ethyleneamines are essential in water treatment processes, where they help remove harmful substances. As governments enforce stricter water treatment regulations, the need for ethyleneamines is on the rise.

5. Increasing Use in Textile Chemicals

Ethyleneamines play a significant role in producing textiles, particularly in dyeing and finishing processes. The textile industry’s rapid growth, particularly in developing countries, is a significant market driver.

Download Sample Report @ https://intentmarketresearch.com/request-sample/ethyleneamines-market-3564.html

Market Segmentation of Ethyleneamines

1. By Type

Ethyleneamines come in different forms, each with unique applications:

Ethylenediamine (EDA): Widely used in the manufacture of bleach activators, fungicides, and chelating agents.

Diethylenetriamine (DETA): Used in the production of paper, rubber chemicals, and fuel additives.

Triethylenetetramine (TETA): Common in adhesives, coatings, and corrosion inhibitors.

Tetraethylenepentamine (TEPA): Important for surfactants, lubricants, and various other industrial products.

2. By Application

Agrochemicals: Ethyleneamines are integral in manufacturing herbicides, insecticides, and fungicides.

Pharmaceuticals: Used in the synthesis of active ingredients and intermediates.

Personal Care: Employed in formulating shampoos, lotions, and other cosmetic items.

Textile Industry: Critical for dyeing, softening, and finishing processes in fabric production.

Water Treatment: Used in water purification to remove contaminants and improve water quality.

Geographical Insights

The ethyleneamines market is segmented based on regions:

1. North America

North America remains a dominant player in the global ethyleneamines market, driven by the robust demand in the pharmaceutical and personal care industries. The U.S. and Canada are the key contributors to this market growth.

2. Europe

Europe’s growth is driven by its strong manufacturing sector, particularly in agrochemicals and pharmaceuticals. Countries like Germany and France are leading the market.

3. Asia-Pacific

The Asia-Pacific region is projected to witness the highest growth rate due to the rapid industrialization in countries like China, India, and Japan. Increasing demand for agrochemicals, pharmaceuticals, and textiles in these nations propels the ethyleneamines market.

4. Latin America and Middle East

These regions are expected to see moderate growth, largely due to expanding agricultural sectors and rising water treatment needs.

Challenges in the Ethyleneamines Market

Despite the positive outlook, the market faces several challenges:

1. Environmental Concerns

The production of ethyleneamines can release harmful by-products that may have environmental consequences. Stricter environmental regulations could potentially hinder market growth.

2. Fluctuating Raw Material Prices

The cost of raw materials like ethylene and ammonia can be volatile, impacting the overall cost structure of ethyleneamine production.

3. Intense Competition

The presence of established players in the market makes it highly competitive, which can affect profit margins.

Opportunities for Growth

1. Innovations in Product Development

Research and development into new and more sustainable ethyleneamine products are creating opportunities. Biodegradable and environmentally friendly ethyleneamines could open up new markets.

2. Growing Demand for Green Solutions

The push for sustainable and eco-friendly solutions is driving innovation in industries like agriculture and water treatment, where ethyleneamines can play a role in reducing environmental impact.

3. Emerging Markets in Developing Countries

Developing regions, particularly in Asia-Pacific, present untapped potential. As industrialization increases, so does the demand for ethyleneamines across various sectors.

Access Full Report @ https://intentmarketresearch.com/latest-reports/ethyleneamines-market-3564.html

These companies are involved in expanding their market presence through partnerships, product development, and acquisitions to stay ahead of the competition.

Ethyleneamines Market Forecast (2023–2030)

The ethyleneamines market is projected to grow at a steady rate of 4.2% CAGR from 2023 to 2030. The rise in demand from key industries such as pharmaceuticals, agriculture, and personal care will be the primary growth drivers during this period. Technological advancements in product development will also contribute to this growth.

Conclusion

The ethyleneamines market is poised for sustained growth, with a projected increase in demand across multiple industries. The versatility of these compounds, coupled with expanding industrial applications, makes them essential for various sectors. While challenges such as environmental concerns and raw material costs exist, innovations and growing demand in emerging markets provide ample opportunities for expansion.

FAQs

1. What are ethyleneamines used for?

Ethyleneamines are used in agrochemicals, pharmaceuticals, personal care products, water treatment, and the textile industry.

2. What is driving the growth of the ethyleneamines market?

Growth is driven by the increasing demand for agrochemicals, pharmaceuticals, personal care products, and water treatment solutions.

3. Which region is expected to dominate the ethyleneamines market?

The Asia-Pacific region is expected to witness the highest growth, while North America remains a dominant player.

4. What challenges does the ethyleneamines market face?

Challenges include environmental concerns, fluctuating raw material prices, and intense competition among market players.

5. How is the market forecasted to grow by 2030?

The ethyleneamines market is expected to grow from USD 2.2 billion in 2023 to USD 2.9 billion by 2030 at a CAGR of 4.2%.

Contact Us

US: +1 463-583-2713

0 notes

Text

Informative Report on PFAS Chemical Material Market | Bis Research

Per- and polyfluoroalkyl substances (PFAS) are a class of synthetic chemicals that have seen extensive global application across various industries and consumer products.

These substances are commonly found in items such as non-stick cookware, water-resistant clothing, stain-resistant carpets, certain cosmetics, firefighting foams, and products designed to repel grease, water, and oil.

The PFAS chemicals market is projected to reach $51,727.5 million by 2034 from $29,500.0 million in 2023, growing at a CAGR of 5.19% during the forecast period 2024-2034

Overview

Per- and polyfluoroalkyl substances (PFAS) are a group of synthetic chemicals that have been manufactured and used in various industries since the 1940s. These chemicals are characterized by their strong carbon-fluorine bonds, making them highly resistant to heat, water, and oil. PFAS are commonly referred to as "forever chemicals" due to their persistence in the environment and resistance to natural degradation.

Types of PFAS

Perfluoroalkyl substances: Fully fluorinated carbon chains.

Polyfluoroalkyl substances: Partially fluorinated carbon chains.

Properties and Uses

Non Stick Cookwares - PTFE (Teflon) coatings are made with PFAS chemicals.

Waterproofing- Used in clothing, furniture, and carpets to resist water and stains.

Firefighting Foam- Aqueous film-forming foams (AFFFs) containing PFAS are effective at suppressing fuel fires.

Electronics- PFAS are used in wiring and semiconductor manufacturing due to their insulating and heat-resistant properties.

Download our Report to know more !

Key Features and Benefits for PFAS Chemical Material

Key Features and Benefits

Key features are as follows

Chemical Stability

Hydrophobic and Lipophilic Stability

Thermal Resistance

Low Surface Energy

Electrical Insulation

Chemical Inertness

Key Benefits are as follows

Consumer Product Enhancement

Industrial Applications

Medical and Healthcare Uses

Electronics and Electrical Industry

Food Packaging

Visit our sample page click here !

Market Segmentation for PFAS Chemical Material

1 By Application

Blowing Agents, Refrigerants and Coolants, and Flame Retardants to Lead the Market - Blowing agents, refrigerants, coolants, and flame retardants are expected to dominate the PFAS chemicals market by application, given their essential roles in high-demand industries such as construction, electronics, and automotive. The unique properties of PFAS chemicals, such as thermal stability, non-flammability, and durability, make them critical in enhancing product performance. For instance, blowing agents are pivotal in creating insulating foams that boost energy efficiency, while refrigerants and coolants are vital for thermal regulation in various systems. Flame retardants contribute significantly to safety standards across numerous applications.

2 By Product - Others Segment to Lead the Market

The other segment is expected to lead the PFAS chemicals market by product due to its broad applicability and distinctive chemical properties. This category includes specialized PFAS compounds that do not fall under conventional classifications but are essential for industries requiring advanced performance and versatility.

By Region- Asia-Pacific Region to Lead the Market

The Asia-Pacific region is positioned to lead the PFAS chemicals market, driven by rapid industrialization, urbanization, and the growth of key sectors such as electronics, textiles, and automotive manufacturing. Countries such as China, Japan, and South Korea are significant consumers of PFAS chemicals, essential in applications such as water and stain repellents, firefighting foams, and semiconductor production

Visit our Advanced Materials Chemical Vertical Page here !

Key Players

3M

AGC Inc.

Archroma

Arkema

BASF

Bayer AG

BIONA JERSÍN s.r.o.

The Chemours Company

Market Drivers for PFAS Chemical Material

1 Growing demand for Non Stick and Strain Resistant Products

Consumer Goods: The increasing demand for non-stick cookware, water-resistant textiles, and stain-resistant fabrics is a significant driver for PFAS chemicals.

Home Furnishings: Carpets, upholstery, and other home textiles benefit from PFAS coatings, enhancing their durability and stain resistance.

2 Expanding Use in the Automotive and Aerospace Industries

High-Performance Materials: PFAS materials are used in automotive and aerospace sectors for seals, gaskets, hoses, and lightweight components.

Fuel Resistance: PFAS-based components that resist exposure to fuels, oils, and other chemicals are critical for engine performance and efficiency.

3. Increased Adoption in Electronics and Semiconductors

Electrical Insulation: PFAS materials are widely used in the electronics industry due to their excellent insulating properties, making them ideal for use in wiring, cables, and connectors.

Semiconductor Manufacturing: The semiconductor industry requires materials with high purity, chemical resistance, and stability, all of which PFAS provide, ensuring their continued use in the production of microchips and other components.

4 Growth in Food Packaging and Food Safety Concerns

Grease-Resistant Packaging: The food packaging industry continues to rely on PFAS materials for grease-proof and water-resistant packaging, which helps extend the shelf life of food products and maintain quality during transportation and storage.

Regulatory Compliance in Packaging: PFAS coatings in food packaging also provide a barrier against contaminants and help meet stringent food safety regulations.

Conclusion

The market for PFAS Chemical Material s is poised for significant growth, driven by a confluence of regulatory pressures, increasing consumer demand for sustainable practices, and the urgent global need to address climate change. As innovation in materials science and manufacturing processes continues to advance, low carbon materials are becoming more accessible and cost-effective, further accelerating their adoption.

0 notes

Text

South Africa Specialty Chemicals Market Trends, Report 2023-2030

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated South Africa Specialty Chemicals Market size at USD 8.7 million in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4.50% reaching a value of USD 11.1 million by 2030. By volume, BlueWeave estimated South Africa Specialty Chemicals Market size at 13.1 million tons in 2023. During the forecast period between 2024 and 2030, BlueWeave expects South Africa Specialty Chemicals Market size to expand at a CAGR of 4% reaching the volume of 17.2 million tons by 2030.

The expanding usage of specialty chemicals in a range of end-user sectors, such as water treatment, chemicals, oilfields, pharmaceuticals, and others, together with improvements in process technology, are key growth drivers for South Africa specialty chemicals market. The government's financial support and other initiatives to increase domestic manufacturing are also expected to propel South Africa specialty chemicals market over the forecast period.

Sample Request @ https://www.blueweaveconsulting.com/report/south-africa-specialty-chemicals-market/report-sample

Opportunity - Expanding automobile manufacturing operations

The expanding automobile production is emerging as one of the major driving factors for the growth of South Africa Specialty Chemicals Market. South Africa ranks 22 in global vehicle production and has been attracting significant foreign direct investment and adopting various growth strategies to boost the automotive industry. Specialty chemicals are widely used in the production of high-performance lubricants and additives. These are essential to reduce wear and friction in engines and engines, improving automobiles' general efficiency and dependability.

Agrochemicals Product Type to Grow at Fastest CAGR

South Africa Specialty Chemicals Market, on the basis of product type, is comprised of agrochemicals, rubber processing chemicals, construction chemicals, food & feed additives, cosmetic chemicals, oilfield chemicals, specialty pulp & paper chemicals, specialty textile chemicals, water treatment chemicals, pharmaceutical & nutraceutical additives, CASE (coatings, adhesives, sealants & elastomers), and other (institutional & industrial cleaners, electronic chemicals, and mining chemicals) segments. Among these product types, the agrochemicals segment is anticipated to register fastest growth rate during the period in analysis. The expanding agriculture sector and rising food demand are expected to fuel the demand for agrochemicals in the South African Specialty Chemicals Market.

Competitive Landscape

South Africa Specialty Chemicals Market is intensely competitive, as a number of companies are competing to gain a significant market share. Key players in the market include Durban Speciality Chemicals, AECI Specialty Chemicals, SUN ACE South Africa, Safic Alcan Southern Africa (Pty) Ltd, IMCD South Africa, Protea Chemicals, Reba Chemicals (Pty) Ltd, BASF, Gold Reef Speciality Chemicals (Pty) Ltd, and Southern Chemicals (Pty) Ltd.

To further enhance their market share, these companies employ various strategies, including mergers and acquisitions, partnerships, joint ventures, license agreements, and new product launches.

Contact Us:

BlueWeave Consulting & Research Pvt. Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

0 notes

Text

Top Technical Textile Products Shaping Various Industries Essential Technical Textiles Products for Modern Industry Needs

Technical textiles have radically transformed the textile industry by putting functionality before aesthetics. The prominent characteristics of these types of high-end products essentially aim at tackling critical technical and engineering issues that in turn benefit different industries, making them essential in various industries. Pidilite’s advanced technical textiles products are designed to meet these modern industry needs with unparalleled efficiency and reliability.

Pidilite’s Expertise in Technical Textiles Products

Advanced Coating Solutions

Pidilite offers cutting-edge technologies like acrylic binders and VAM emulsions that enhance the performance of technical textiles. Products such as Pidicryl 3640 H provide durable, hard films suitable for a variety of substrates, including textiles and metals, ensuring long-lasting performance and stability.

Innovative Functional Additives

Pidilite's assortment covers chemicals like fire retardants, antimicrobial agents, and water repellents. Texeltek AM 700 and Texeltek DE 3236, for example, provide fundamental features such as antimicrobial protection and oil and water repellency, thus being vital for many uses in technical textiles.

Customisable Solutions

Pidilite develops custom-made solutions tailored to specific needs, from textile coatings to binding agents. With products like Pidicryl 3699, which offers flexibility and durability, Pidilite ensures that their technical textile products meet the precise requirements of diverse industries.

Pidilite offers a wide range of technical textiles products for different applications like:

Nonwoven Wadding for insulation and padding

Curtain Fabrics to enhance durability and performance

Shoe Sole Boards to provide sturdy and reliable support

Flocking Binders to secure flocked textiles

Textile Coatings for improved fabric performance

Carpet Backing to add strength and durability

Tent Coatings for waterproofing for outdoor use

Soft Luggage to add resilience and flexibility

Flame Retardant Finishes for safety applications

Water Repellents to protect against moisture

Antimicrobial Finishes to enhance hygiene and longevity

Oil Repellent Coatings to prevent stains and damage

Why Choose Pidilite Industrial Products?

Superior Quality and Performance

Pidilite has gained its reputation due to the use of the highest quality materials and the superior performance of the products. The Pidicryl 3681 and Teknotex WR 830 are both products that exhibit the commitment of Pidilite to delivering exceptional functionality and thus prove its dedication in achieving the highest possible utility and strength in textiles.

Customer-Centric Innovation

Pidilite's top concern is to know what the clients want and then to make products that will fulfil their needs. Teknotex AM 300 is one such product that the company, through their collaborative method, manages to follow the unique needs of different industries, enhancing production efficiency and product value.

Global Expertise and Reach

With a global footprint, Pidilite provides innovative textile solutions across various markets. Their extensive experience and diverse product range, including Jowat hot melts and Teknotex antimicrobial agents, make Pidilite a trusted partner in the technical textiles sector.

Conclusion

Pidilite’s advanced technical textiles products are essential for meeting the modern industry's demands for high-performance and functional fabrics. With innovative technologies, a customer-centric approach, and a global reach, Pidilite provides reliable solutions that drive efficiency and value across each application of technical textiles. Choose Pidilite for superior technical textile solutions that stand the test of time.

0 notes

Text

Polyvinyl Alcohol Market Share and Trends, Analysis by Top Key Vendors by 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Polyvinyl Alcohol Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Polyvinyl Alcohol Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Polyvinyl Alcohol Market?

The global polyvinyl alcohol market was valued at US$ 3.7 Billion in 2023, and is expected to register a CAGR of 6.0% over the forecast period and reach US$ 6.3 Bn in 2032.

What are Polyvinyl Alcohol?

Polyvinyl Alcohol is a synthetic polymer with water solubility, extensively employed in diverse industrial and commercial applications. It is created by polymerizing vinyl acetate, followed by hydrolysis to produce the alcohol. PVA is recognized for its exceptional film-forming, emulsifying, and adhesive qualities, making it essential in products like paper coatings, textile sizing agents, adhesives, and films. PVA finds use in medical realms, including contact lens solutions and drug delivery systems, owing to its biocompatibility and low toxicity. Its capacity to dissolve in water and create robust films also renders it valuable in environmentally friendly packaging solutions.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2316

What are the growth prospects and trends in the Polyvinyl Alcohol industry?

The polyvinyl alcohol market growth is driven by various factors and trends. The global Polyvinyl Alcohol (PVA) market is experiencing steady growth, fueled by its versatile applications across various industries such as packaging, textiles, construction, and pharmaceuticals. PVA's appeal lies in its biodegradability and water solubility, making it a preferred choice in regions with strong environmental concerns. It serves as an eco-friendly substitute for traditional plastics in packaging and enhances fiber strength and abrasion resistance in textiles. PVA also improves the workability and adhesion of cement and mortar in construction and is used in pharmaceuticals for oral dosage forms and medical devices. However, challenges such as fluctuating raw material prices and competition from other biodegradable materials could impact market growth. Hence, all these factors contribute to polyvinyl alcohol market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

North America

United States

Canada

Europe

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

Benelux

Nordic

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Kuraray Co., Ltd.

Anhui Wanwei Group Co Ltd.

Chang Chun Petrochemicals Co Ltd.

Ningxia Dadi Circular Development Corp Ltd.

Sinopec Sichuan Vinylon Works

Sekisui Specialty Chemicals

Mitsubishi Chemical Corporation

Japan Vam and Poval Co Ltd.

Merck Kgaa

Wacker Chemie AG

Denka Company Ltd.

View Full Report: https://www.reportsandinsights.com/report/Polyvinyl Alcohol-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Adhesives & Sealants Market - Forecast(2024 - 2030)

Adhesives & Sealants Market Overview

Global Adhesives & Sealants market size is estimated to reach US$ 89.1 billion by 2027, after growing at a CAGR of 5.7% during the forecast period 2022-2027. Adhesives and sealants are the chemical products which are used to create a mechanical seal between components. Adhesives are the non-metallic materials used to hold two substances together, while sealants are material used to fill space between these substances and to provide a protective coating. Adhesives are of various types like polyurethane adhesives, cyanoacrylate adhesive and epoxy adhesives, while sealants consist of resin like silicon, acrylic and butyl. These materials are chemically made with the help of rheology modifiers which are used to improve their viscosity. Adhesives and sealants have high applicability in sectors like construction, automotive, paper, textile, electronics and wood. Their major applicability is in construction sector where adhesives are used in polycarboxylate for concrete production. Factors like growing construction activities, increase in production volume of automotive, increase in aircraft production and high consumption of clothing & apparel items are driving the growth of global adhesives & sealants market. However, adhesives and sealants manufacturing produce volatile organic compounds which can cause environment problems like pollution. The regulation imposed by government to restrict VOC emission can hamper the growth of global adhesives & sealants industry.

COVID-19 Impact

The wide spread of COVID-19 left a negative impact on the activities of various industrial sectors, as the necessary measures taken by countries like consequential lockdown led to lack of availability of labors and raw materials. This disrupted the functionality of various end users of adhesives and sealants like construction, automotive, textile, and aerospace. For instance, as per, International Construction and Infrastructure Surveys, the construction and infrastructure activities across all regions went down in Q1 of 2020 with China in the Asia-Pacific region having the sharpest workload contraction. Also, as per the International Organization of Motor Vehicle Manufacturing, in 2020 there was a 16% global decline in vehicles production. Further, as per the 2021 report of the General Aviation Manufacturers Association, the Global business jet deliveries declined 20.4% to 644 aircraft in 2020 due to the COVID-19 pandemic. Polycarboxylate is used in cement concrete application, cyanoacrylate adhesive is used in automotive interiors while acrylic sealants are used in aircraft to prevent corrosion and fuel leak. Hence, the decrease in productivity of such sector led to decrease in usage of adhesives and sealants in them.

Request Sample

Report Coverage

The report: “Adhesives & Sealants Market Report – Forecast (2022 – 2027)”, by IndustryARC, covers an in-depth analysis of the following segments of the Global Adhesives & Sealants Industry

By Type – Water Based Latex, Acrylic, Polysulfide, Silicone, Polyurethane, Epoxies, Polyamides, Cyanoacrylate, Polyethylene Glycol, and Others (Polyisobutylene, Dextrin, Butyl)

By Form – Water based (Solution, Polymer Dispersion), Solvent based (Wet Bonding, Contact Adhesives), Hot Melt, and Reactive

By Application – Bonding (Paper Bonding, Wood Bonding), Concrete Production, Countertop Lamination, Drywall Lamination, Transportation (Automotive Module Sealant, Anti-Fuel Leaking Agent, Anti-Corrosive Agent, Clothing & Apparel (Apparel Laminate, Fabric Combining) and Others (Self-Adhesives Bandages, Circuit Boards Encapsulants)

By End User – Automotive (Passengers Cars, Heavy Commercial Vehicles, Light Commercial Vehicles, Others (Three-Wheeler, Two-Wheeler)), Construction (Residential, Commercial), Aerospace, Wood Industry, Paper, Textiles (Woven, Non-woven), Electronic, Medical and Others (Marine, Plastics)

By Geography - North America (USA, Canada, Mexico), Europe (UK, Germany, France, Italy, Netherland, Spain, Russia, Belgium, Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia, and New Zealand, Indonesia, Taiwan, Malaysia, Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, Rest of South America), Rest of the World (Middle East, Africa)

Key Takeaways

Asia-Pacific dominates the global adhesives & sealants industry as the region consist of major end users of adhesives and sealants like plastic, construction, automotive, electrical in major economies like China, South Korea, and Australia.

Rheology Modifier is used in water borne, solvent borne adhesives and sealants of all types, to control viscosity, provide coating performance and build thick adhesion between components.

In dentistry filed, polycarboxylate cement is used in the fixation of dental crowns, inlays, and along with cavity linings which provide a good adhesion to the tooth structure.

Inquiry Before Buying

Adhesives & Sealants Market Segment Analysis – By Type

Polyurethane held a significant share in global adhesives & sealants market in 2021, with a share of over 22.0%. Polyurethane adhesives are UV, water, and chemical resistant while polyurethane sealants provide long term elasticity and durable adhesion. Polyurethane adhesives are majorly used in automotive windshield while polyurethane sealants are used in sealing gaps and joints in components and structures. The rapid development in automotive and construction sectors has increased their scale of productivity which has positively impacted the usage of adhesives and sealants. For instance, as per European Automobile Manufacturers Association, the production and registration of passenger cars in the EU increased by 53.4% in 2021 with strong volume seen in Spain, France, and Germany. Further, as per US Census Bureau, in 2021, construction activities steadily increased in US, with residential construction showing an increase of 4.1% in November, up by 1% from 2020 same month. Such increase in productivity of these sectors will lead to more usage adhesives and sealants in the, which will positively impact the growth of global adhesives & sealants industry.

Adhesives & Sealants Market Segment Analysis – By End User

Construction sector held a significant share in global adhesives & sealants market in 2021, with a share of over 19.0%. Adhesives & sealants based of resins like polyamide, epoxy resin and plastisol are majorly used in construction sector as they have resistance to excessive sun, rainfall, provide good steel bonding, and act as cement dispersant. The rapid development in the construction sector in countries has increased the scale of construction activities and the undertaking of new infrastructure projects. For instance, as per European Union, in December 2021, construction of building increased by 4.6% and civil engineering by 3.3% compared to 2020. Also, in 2019 a total of US$ 102.3 billion worth of projects were processed across all GCC countries, compared to US$ 101.8 billion in 2018. Hence, such increase in the construction and infrastructure development activities will lead to more usage of adhesives in cement application while sealants will be used in blocking dust and heat transmission. This will have a positive impact on the growth of global adhesives & sealants industry.

Schedule a Call

Adhesives & Sealants Market Segment Analysis – By Geography

Asia-Pacific held the largest share in global adhesives & sealants market in 2021, with a share of over 27.0%. The region consists of major end-users of adhesives and sealants like construction, automotive, textiles, in major economies like China, India, Japan, and Australia with China having the largest automotive and construction sector. The economic development in these nations has led to increase in the industrial output of these sectors. For instance, as per the 2021 report of the European Automobile Manufacturers Association on global vehicle production, China produced 32% of 74 million cars manufactured worldwide with Japan & Korea producing 16%. Also, as per the State Council for the People’s Republic of China, in July 2021 China has approved projects related to the development of affordable rental homes. Further, as per October reports of Infrastructure Australia 2021, the major infrastructure activity relating to commercial buildings, civil infrastructure, and residential will double in the next three years. Cyanoacrylate adhesives are used in automotive roof pads, engine hose protectors and flex boards while acrylic and polyurethane based sealants are used to seal joints between components like concrete, steel, and masonry wall. Hence, the growing productivity of construction and automotive will lead to more usage of such adhesives and sealants in them, resulting in more growth of global adhesives & sealant industry.

Adhesives & Sealants Market Drivers

Growing Construction Activities

Emerging economies, rapid urbanization, and various infrastructural developments undertaken by countries have increased the scale of construction activity. For instance, in preparation for the 2021 Expo, Dubai awarded about 47 construction contracts with a total value of US$ 3 billion to local and foreign companies. In 2019 National Development and Reform Commission of China approved 26 infrastructure projects estimated to be completed by 2023. Also, in 2021, Oman’s Ministry of Housing and Urban Planning five new integrated projects that would provide 4800 housing units. Adhesives and sealants in building construction are used as the bonding layer for floor fixing, countertop lamination and wall covering. Hence, the increase in construction activities and infrastructure development projects will lead to more usage of adhesives and sealants, which will have a positive impact on the growth of the global adhesives & sealants industry.

Growing Production of Automotive

Automotive adhesives and sealants are used by automotive original equipment manufacturers (OEMs) to bond different substrate of metal, eliminating the need for welding and mechanical bolts, welds and rivets. The increase in purchase capacity, improvement in living standards, and rapid urbanization have led to an increase in the demand for new automotive vehicles, thereby increasing their production volume. For instance, as per the International Organization of Motor Vehicle Manufacturing, the global production volume of vehicles increased to 57 million in 2021 from 52 million in 2020. Also, as per the November 2021 report of the Europe Automobile Manufacturer Association, the new passenger car registration in the first ten months of 2021 increased up to 2.2% with an increase shown in European Union markets like Italy showed 12.7%, Spain showed 5.6% and France showed 3.1%. Such an increase in automobile production on account of high demand will increase the usage of adhesives and sealants like cyanoacrylate adhesives, which will have positive impact on growth of global adhesives & sealants industry.

Buy Now

Adhesives & Sealants Market Challenges

Stringent Government Regulation

One of the significant issues related to adhesives and sealants is that, their formation causes VOC emission which can lead to serious problems like skin irritation, sour throat and long-term damage to lungs & kidneys. Hence, in order prevent such problems various government organization have imposed certain regulation relating to VOC emission. For instance, Title 40, Code of Federal Regulations of US, Environment Protection Agency deals with EPA’s mission of protecting human health and the environment from VOC emission. Such regulation can restrict the production volume of adhesives and sealants, which can hamper the growth of global adhesives & sealants industry.

Adhesives & Sealants Industry Outlook

The companies to develop a strong regional presence and strengthen their market position, continuously engage in mergers and acquisitions. The global adhesives & sealants top 10 companies include:

Henkel Corporation

Sika AG